CINF - Cincinnati Financial: Highlighting The Importance Of Valuation A 'Buy'

2023-05-23 08:39:59 ET

Summary

- I last wrote about Cincinnati Financial back in December of last year - on Christmas, actually. The company is a currently-minor position in my conservative dividend portfolio.

- Any outperformance to the market is worth highlighting - and CINF, since the very first article I published, has outperformed.

- In this article, I will provide you with an update to this stance, and why I'm keeping my CINF and may actually buy more of the company.

Dear readers/followers,

So, I've been writing on Cincinnati Financial ( CINF ) twice at this time. Both times, the company had posted or generated some good results. It's an attractive company. We do have new results here to look at and consider an updated thesis for this company.

Let's look at what we have going for us here if we were to invest more in Cincinnati Financial.

Cincinnati Financial - an update for 2022

Cincinnati Financial isn't exactly the most undervalued financial. As I wrote my first article on the company, there was some undervaluation there, and there is still some undervaluation here today. This is a qualitative business, with plenty of appealing upside. If you consider the forecasts and the premiums for this above-average, BBB+-rated insurance company to be valid, then you could make good money here.

But the situation has also changed somewhat. We're no longer in a position in the market where it is hard or complex to find undervalued quality businesses. There is a multitude of such businesses available today - and this is perhaps the largest change for CINF at this time.

The company's fundamental margins are good - but like many of the insurance companies out there, trends and macro have seen their previously above-average margins dip to just around average for the time being. It's still very solid in terms of safety and capitalization, but the degree of valuation premium that we usually have with CINF means that you're being asked to pay a relatively high multiple - 23-24x P/E - for an industry that around the world you can buy for below 10x at this time. And that's with BBB safety. Also, CINF has no more than 2.86% yield, which for this sector, and these valuations, is on the low side.

The company is in the field of P&C insurance, and it's a solid business that typically outperforms or at least matches its peers, both insurance and the P&C subsector specifically.

{kind=link}

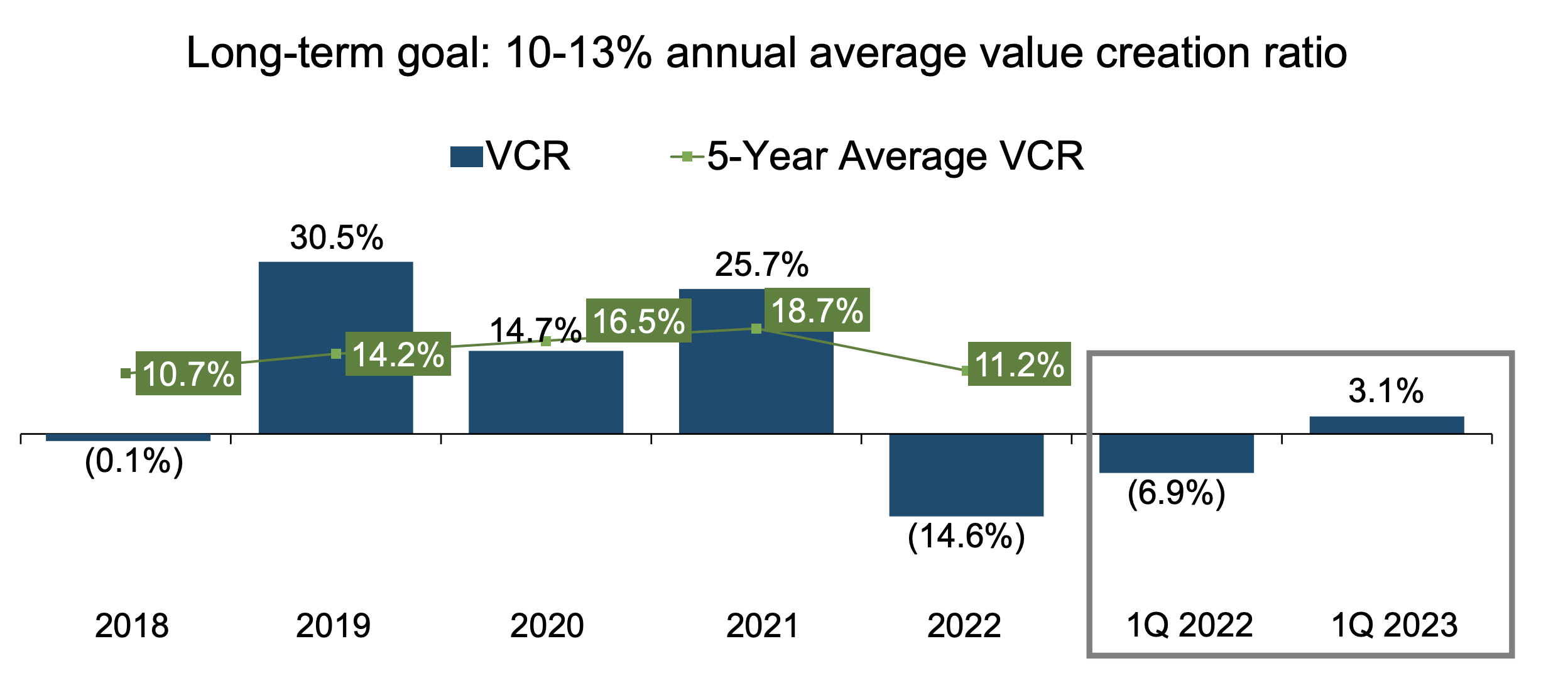

The company's targets are lofty and positive - CINF targets a value creation ratio of around 10-13% over the coming 5 years, which in this context means an annual growth in book value inclusive of the percentage of dividends to beginning BV. This growth is expected to come from the following sources:

- Above-average premium growth next to the industry

- Good combined ratio

- Solid investment contributions from the company's conservative investment portfolio, compounding CAGR for exceeding average S&P500 returns.

This in itself does not much differ from the strategies adopted by virtually all P&C and healthcare insurers in the industry. What's important to understand with insurance companies, in the context of discussing finance companies in today's market are a few things. I say this because I know investing in finance businesses at this time is a somewhat sensitive subject due to the recent instability in banks. However, consider a few things.

First off, insurance companies have completely different maturity structuring in their bond investments compared to banks. Banks invest on a much longer time frame, which increases the risk for unrealized losses when we see massive yield curve shifts as we have for the past few months and about 1-2 years. Insurance companies invest in much shorter-term dated portfolios and bonds/investments, which lessens this risk somewhat.

Secondly, while you may think that insurance companies may need sudden influxes of cash in order to meet risk payments in the case of substantial emergencies or a sudden need for payments, such in the case of a natural disaster or a pandemic, this really only applies if you ignore the concept of reinsurance.

In short, Insurance companies are far less vulnerable to such things, because they match liabilities and assets far better. Sudden "runs" on the companies are unlikely, which is what we've seen on banks. Their risks are matched with reinsurance protection, which really means that comparing asset/liability matching in the two industries is incredibly difficult, and shouldn't really be done. Because insurance companies don't face the liquidity risks seen by banks, they can typically sit out any unrealized losses on bond investments they may have - and some do have these at this time.

That's why generally, I actually like investing in insurance plays far more than in straight bank plays. Their structures are more appealing and many of them are, paradoxically, safer than banks.

The company has had some less-than-ideal years. We're talking about things like below-target VCR, due to negative contributions from non-operating items. However, the net premium growth and the core activities in insurance continued to be solid. The company doesn't have much in the way of pandemic effects - those haven't been material since late 2020, and have resulted in a slight reduction in premium growth, but by mid-21 this was trivial.

One question I had that was company-specific was regarding commercial property policies and the business interruption claims that have been going on, as this could have posed a non-trivial claims risk against the company. However, in the vast majority of trials, the respective appellate and state supreme courts have ruled that losses arising from the pandemic are not covered by these commercial property policies.

As for the EPS and VCR during 1Q23, the company saw some recovery here. It's not at the level the company is looking for just yet - 3.1%, but it's better than we saw during all of 2022 and on a YoY basis.

{kind=link}

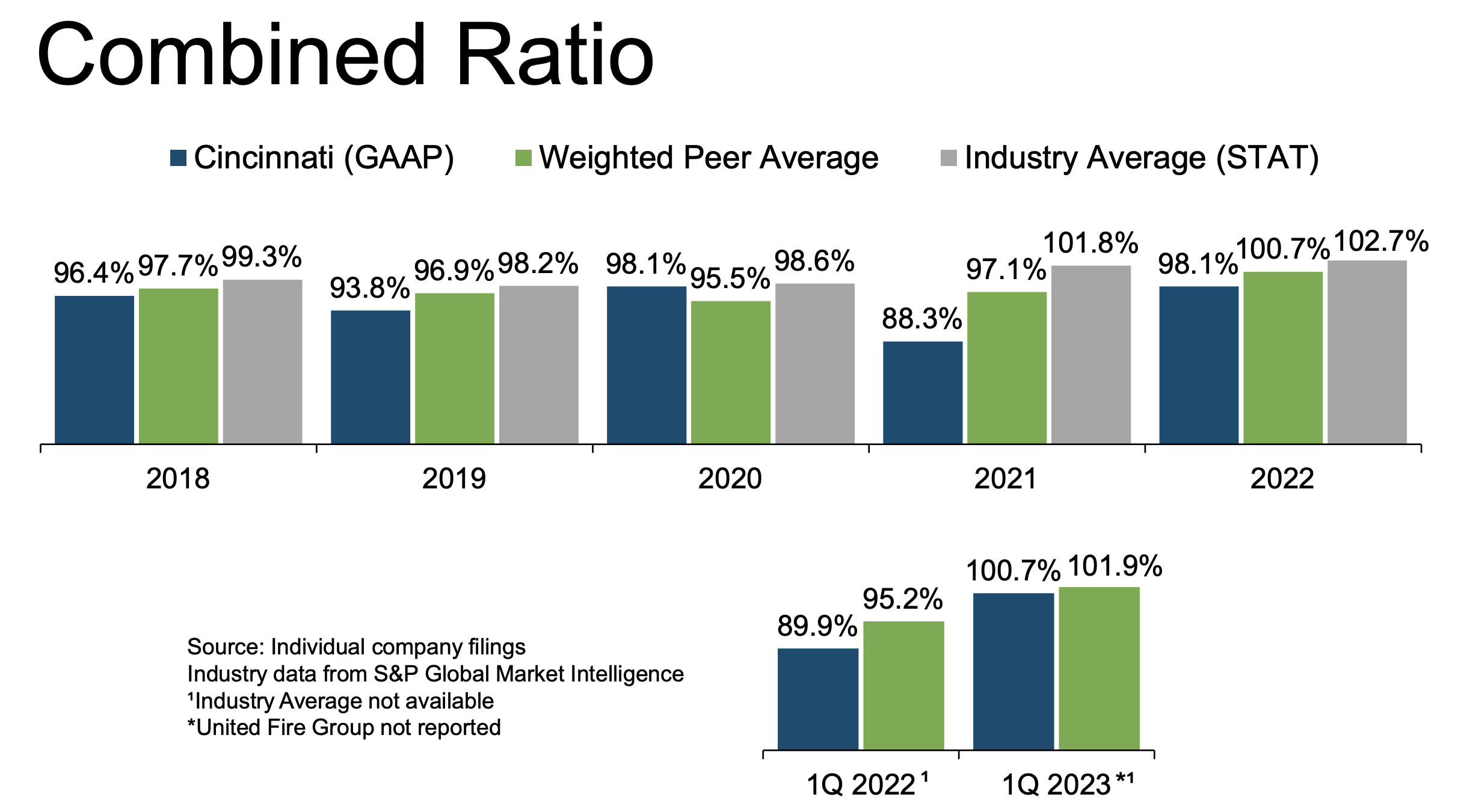

Company combined ratios are, generally speaking, better than averages, and that continues going forward. Lower combined ratios are better.

{kind=link}

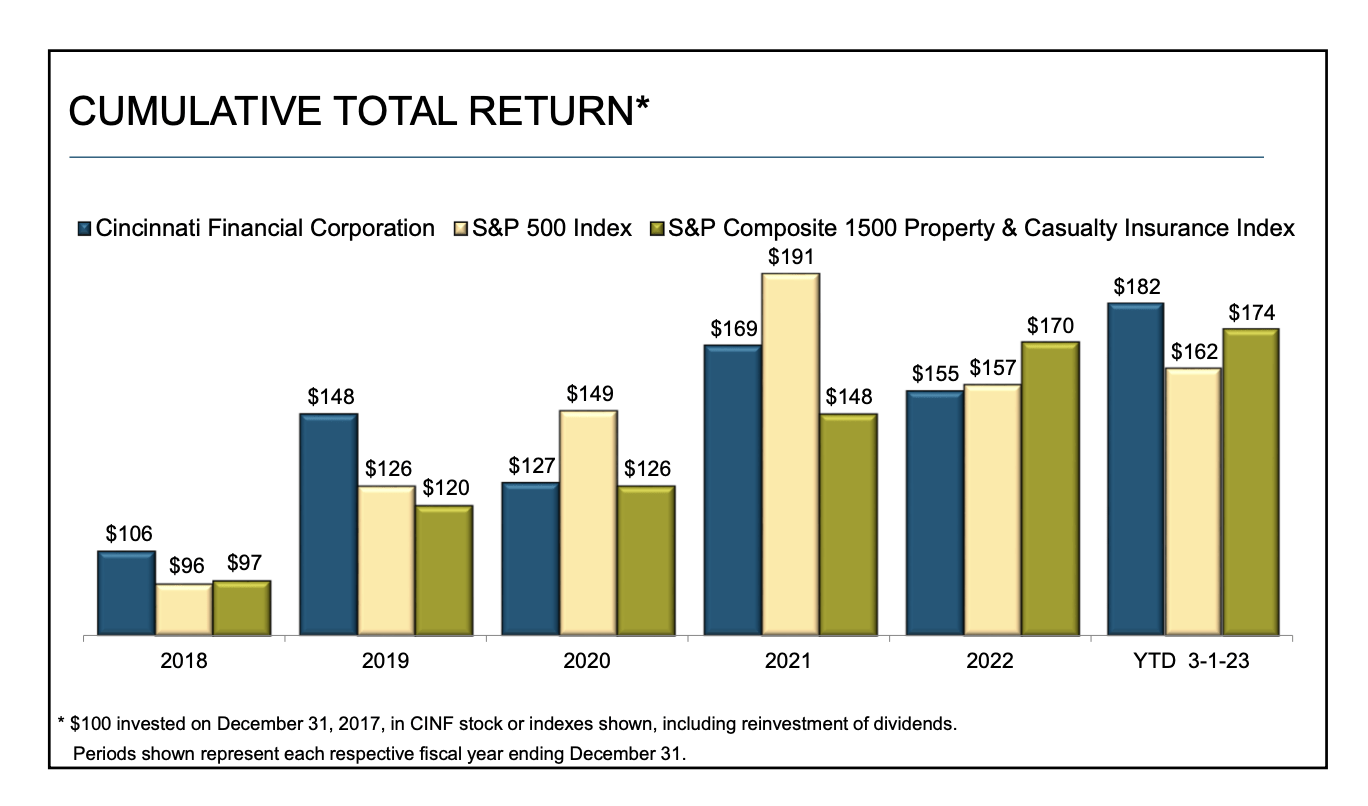

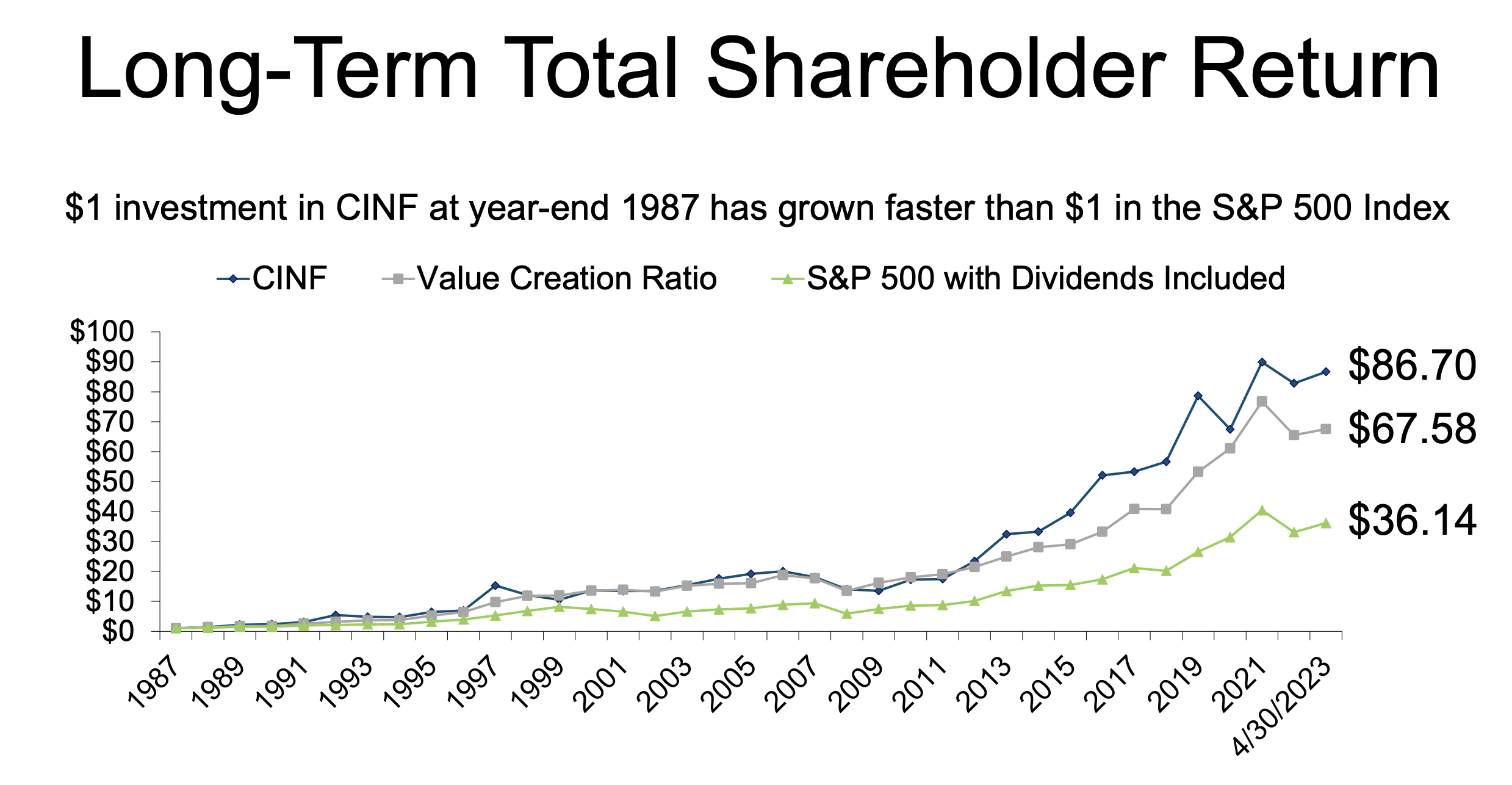

And the company's net written premiums are solid. Also, while the company's yield is not high, the company is a dividend king with over 60 years of increases under its belt. Very few companies can lay claim to this type of track record, and CINF has managed annualized shareholder returns of 9.2% since 2022, which is respectable compared to most investor performance track records you could have looked at. The company is a high-single-digit dividend increase, and on this basis, the company is very attractive indeed. TSR since 1986 has been absolutely stellar, because it has massively outperformed the S&P500 even inclusive of dividends here.

{kind=link}

So, all in all, the company had a good 1Q23, but it's far from where it wants to be in terms of growth. It's likely that this will take time to see realized. I do see some issues and troubles with the company valuation - at least insofar as it's not as great as some of the investments out there. But it is complemented by a solid longer-term growth rate going into 2024, of over 25% in terms of forecasted adjusted EPS.

Let's see where this puts our valuation thesis for CINF.

Cincinnati Financial - Plenty to like, but valuation might be a bit high

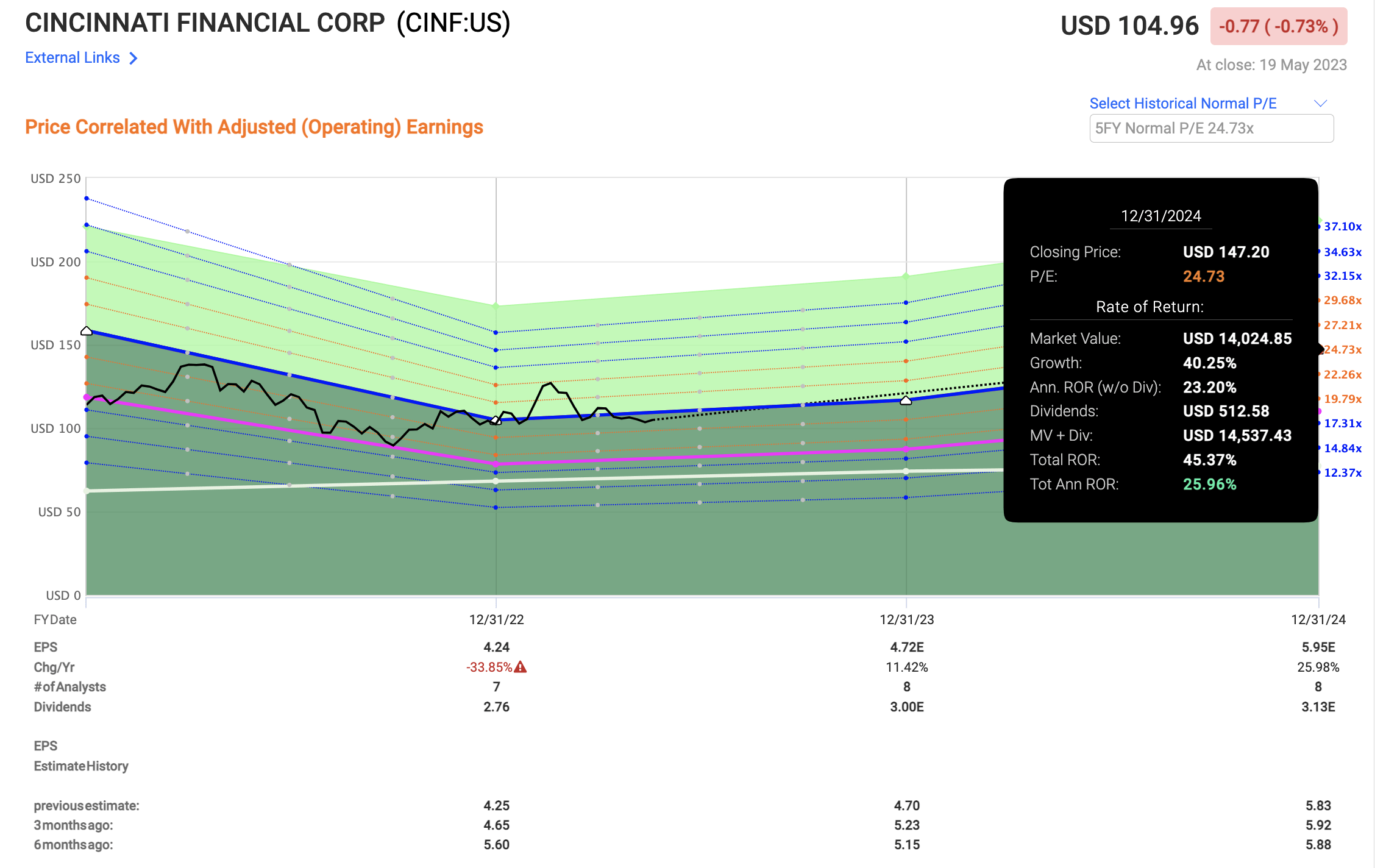

The past few years have been substantially more volatile than we might be used to from a dividend-king type of company. The company has gone up and down as the trends in earnings have, with 2020 seeing a decline of more than 20%, and 2022 yet another decline of 34%, though a significant upswing in 2021. The current expectation is for another upswing to come in 2023 and 2024, coming to 11 and 26% respectively. Should these trends materialize, it's likely that you'll see the share price stabilize at historical levels - it is what it typically does, after all.

In this case, that means an upside of around 25% per year, though much of that is based on what happens in 2024E.

{kind=link}

So, this is a very solid upside. The problem I'm having is two-fold, at least insofar as to why I am not more vocal in my buying of CINF at this time. First off, CINF is overvalued compared to peers. On a P/E-basis, as well as a forward P/E and EV/EBITDA/revenue and other multiples, the company is at a level that's higher than over 86% of the peers in the sector. These are peers that include far larger businesses, such as Chubb ( CB ), Travelers, Allstate ( ALL ), and others, which are several times as large as CINF. This doesn't necessarily make them better, but given for instance that CB is actually at a substantially more appealing valuation relative to its historical and it also beats CINF in margin efficiencies, a question arises whether investing in CINF at this time may be worth it.

Depending on your expectations for the company, it might be. The company, after all, has a strong history of outperforming analyst expectations, which could turn into a higher upside for CINF than what is forecasted above. However, I'm always very careful basing my expectations on companies beating expectations. It's a bonus, but it doesn't mean you want to rely upon it.

Current street targets for CINF come to around $120/share on average from a range of $115 to $130, a fairly tight range. But only 1 out of 5 analysts currently consider the company a "BUY", despite a near 15% upside based on this target. That is why I believe the upside to potentially be smaller than we might expect.

With inflation, the market and a looming recession included in your considerations, I believe you may be well-served to look at higher-quality cheaper companies in the sector for a safer and more profitable upside. However, for those very conservatively-minded wanting to invest in a dividend king, CINF offers this to you, and an investment in the business may certainly result in outperformance (as I believe that it indeed will).

To conclude, I believe CINF does have an upside - but that upside needs to be viewed in the context of what is available on the market and in the insurance sector at this time. Because there are so many attractive companies available with better upsides or at least better yields and comparable safeties, I do not see a convincing reason to go with CINF above some of the other ones. So my choice would go to other companies above CINF.

However, from a valuation and upside perspective , CINF is currently undervalued to its real potential. For that reason, I still give it a "BUY" here with the following overall targets.

Thesis for Cincinnati Financial's Common Shares

- This is a conservative, appealing insurance company and one of the market leaders in insurance in the USA. The company has some of the most qualitative portfolios and track records out there, being a dividend king with more than 60 years' worth of dividend increases under its belt.

- At the right valuation, this company becomes a "must-buy". Even at today's valuation, CINF has a decent overall upside to a conservative valuation based on average historical valuations.

- Based on this, I consider CINF to be a "Buy" here. I give the company a current conservative share price target of $110/share.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them. ( italicized )

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

It's not cheap, but it does fulfill the other criteria, making the company a "BUY" at this time.

For further details see:

Cincinnati Financial: Highlighting The Importance Of Valuation, A 'Buy'