CINF - Cincinnati Financial: This Dividend King Is Finally A Buy

2023-12-26 01:31:36 ET

Summary

- When I last covered Cincinnati Financial, I argued that the stock was substantially overvalued. Predictably, it significantly lagged the market during that time.

- The company's financial results for the third quarter were mixed, but still strong in my opinion.

- CINF boasts investment-grade credit ratings from the major rating agencies.

- The stock appears to be trading at a 14% discount to fair value.

- CINF could be positioned to triple the S&P's total returns through 2025.

At just 26 years old, I don't claim to be the most knowledgeable investor in the world. Heck, the investing legends have forgotten more than I even know about this business. As long as I live, though, the beauty of investing is that time and experience will serve as my teacher.

One thing that I have especially learned over the years is the importance of valuation. Those who have read my work over the years know that I put as much stock (pun intended) in valuation as I do in an underlying company's fundamentals.

One example of this that comes to mind is Cincinnati Financial (CINF). When I initiated coverage in October 2019 , my fair value estimates pegged the stock as being nearly 40% overvalued at that time. Thus, I rated shares of the stock a hold at the time. It would appear that I was correct in this argument: Shares of CINF have shed 12% of their value over the last four years and change. This is a stark contrast to the 60% rally in the S&P 500 ( SP500 ) during that time.

Now, I believe that the circumstances are entirely different. Please allow me to elaborate on why I am upgrading CINF to a buy rating.

{kind=link}

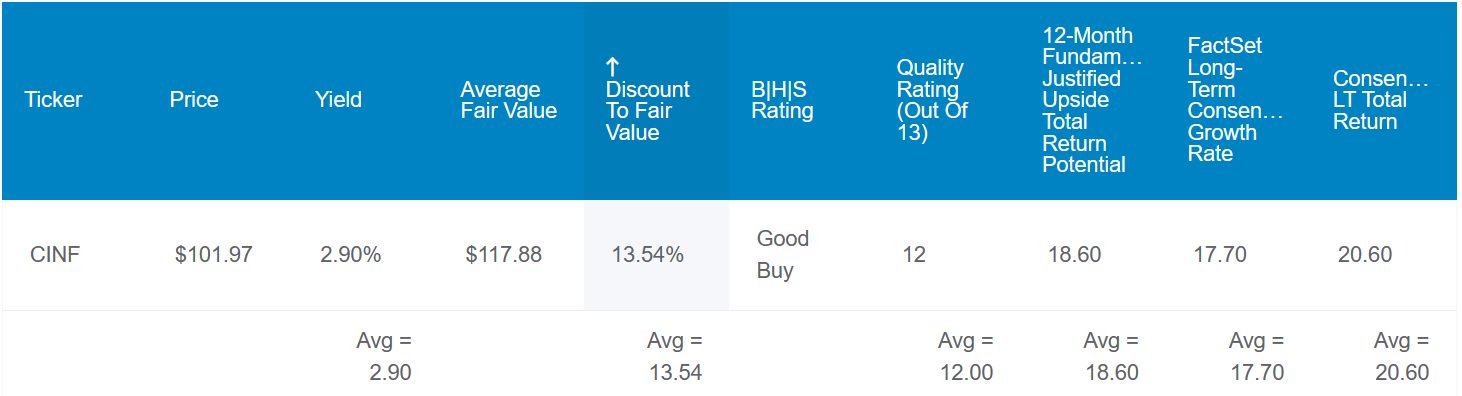

CINF's 2.9% dividend yield is approximately double the 1.5% yield of the S&P 500 index. This superior starting income is something that I do like about the stock. It's also far better than the 1.9% starting yield at the time that I rated CINF a hold.

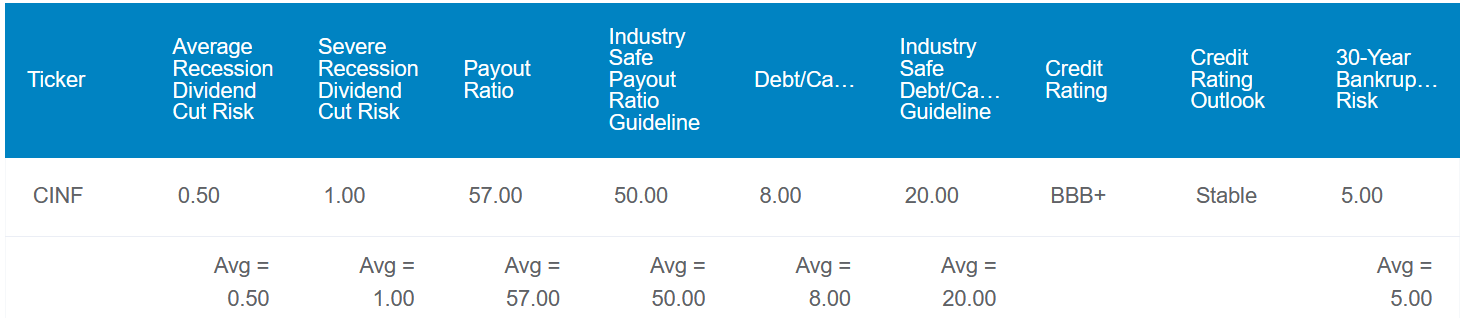

CINF's 57% EPS payout ratio is a bit above the 50% that credit rating agencies like to see from property and casualty insurers. However, the dividend is safer than it initially appears to be based solely on this metric. I will demonstrate what I mean in the dividend section of this article.

Another thing that I like about CINF is that its balance sheet is exceptionally strong. The company's 8% debt-to-capital ratio clocks in at less than half of the 20% industry-safe debt-to-capital ratio desired by rating agencies. This is why S&P awards a BBB+ credit rating to CINF on a stable outlook. That implies the 30-year risk of bankruptcy is 5% per Dividend Kings.

As I will highlight in the fundamentals section of this article, S&P appears to be taking a conservative stance toward CINF relative to its two credit rating agency counterparts. This could mean that the risk of the company going to zero in the next 30 years is less than 5%.

{kind=link}

On the valuation front, CINF of today is a night and day difference versus the CINF of four years ago. A combination of growing its book value and a lower share price has swung the stock from meaningfully overvalued to 14% undervalued from the current $102 share price (as of December 23, 2023).

Using historical valuation metrics including dividend yield, Dividend Kings estimates that shares of CINF are worth $118 today. For context, that's about where shares were trading four years ago. This is just how far ahead of itself the valuation of CINF had become when I initiated a hold rating on the stock in October 2019.

If CINF were to meet the analyst growth consensus and return to its mean fair value, here are the total returns it could produce for shareholders from the current share price:

- 2.9% yield + 17.7% FactSet Research annual growth consensus + 1.5% annual valuation multiple expansion = 22.1% annual total return potential or a 636% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P 500 or a 128% 10-year cumulative total return

An Excellent Insurer Delivering For Shareholders

{kind=link}

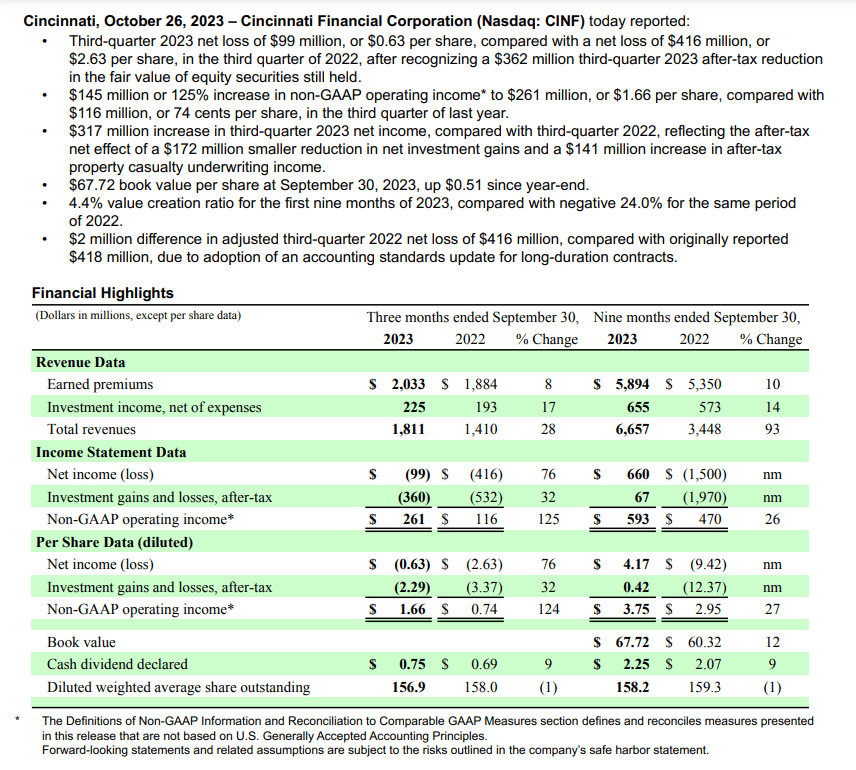

CINF's financial results for the third quarter ended September 30 were decent. The company's earned premiums of $2 billion missed the analyst consensus by $210 million . However, this was still good enough for an 8% year-over-year growth rate in the quarter.

This growth in CINF's book of business was driven by strength throughout the company. Chairman and CEO Steven Johnston noted the following in his opening remarks during the Q3 2023 earnings call :

Estimated average renewal price increases for the third quarter continued at a healthy pace. Our Commercial Lines segment again averaged near the low end of the high single-digit percentage range, while our Excess and Surplus Lines Insurance segment continued in the high single-digit range. Personal Lines for the third quarter included auto rising to the low double-digit range and homeowner rising to the lower end of the high single-digit range.

As has been the case throughout its history, the trust that CINF has built among customers is the foundation of its success. Thus, the company was able to renew policies at high- single-digit increases in its Commercial Lines, Personal Lines, and Excess and Surplus Lines Insurance segments. In other words, customers pay these higher premiums for the peace of mind that a financial fortress like CINF is assuming some of their financial risks.

Additionally, Mr. Johnston noted in the Q3 2023 earnings press release that the company added 193 new agency reporting agencies so far in 2023. That brought the company above 3,000 for the first time in its history.

Insurance agencies aren't just wasting their time adding carriers with policies that customers don't want or need, either. In response to a question from Raymond James' Charlie Peters, CINF's President Stephen Spray hinted that its policies are in high demand. Once added to an agency, the company is the leading or second carrier as determined by premium volume in the majority of agencies it does business with for five-plus years per Spray.

CINF's non-GAAP operating income per share climbed 124.3% over the year-ago period to $1.66 for the third quarter. This exceeded the analyst consensus by $0.52. Sound underwriting and an uptick in premiums contributed to this growth. Looking ahead, CINF's pricing power on its policies and growing footprint at agencies throughout the U.S. should bode well for its growth prospects.

Lastly, CINF is becoming a more financially sound business with each passing quarter. The company's own debt-to-capital ratio metrics have slightly improved from 7.4% as of December 31, 2022, to 7.1% as of September 30. This is why Fitch and Moody's , respectively, award A- and A3 credit ratings to CINF. Given the company's prudent capitalization and savvy underwriting track record, I am more inclined to agree with these credit ratings over S&P's BBB+ rating. However, I do appreciate the differing opinion of the rating agency here versus its peers.

The Longest Dividend Growth Streak Among Financials Is Just Getting Started

Perhaps the most obvious indicator of CINF's overall quality is its dividend growth streak. The company hiked its quarterly dividend per share by 8.7% to $0.75 in January. This represented the 63rd consecutive year that it has paid higher dividends to shareholders than in the prior year. For perspective, no other financial sector company can lay claim to a 60-plus-year dividend growth streak. In the last five years, CINF's dividends paid have cumulatively surged 38.7% higher from $2.12 in 2018 to $2.94 in 2023.

From my perspective, this level of dividend growth should be poised to continue over the next five years. Through the first nine months of 2023, CINF generated nearly $1.5 billion in free cash flow. Measured against the $338 million in dividends paid to shareholders, the company's payout ratio was just 23.1% (details per page 7 of 82 of CINF's 10-Q filing ). Simply put, CINF has both the reputation of putting shareholders first and the means to keep doing so.

Risks To Consider

CINF is a great business, but it has risks as all businesses do. Here are a few that I consider to be most pertinent to the investment thesis.

CINF's products are mostly sold through independent insurance agents. This comes with risks that could hurt its fundamentals. The company must keep offering insurance products that fulfill the needs of these insurance agents and their clients. If CINF can't execute this requirement, it could lose share to its competitors.

A similar risk that could impact the competitiveness of the company versus others is its credit ratings. If CINF can't continue to inspire confidence from agents and their clients, this could also hurt its market share.

Finally, a material deviation between expected claims and actual claims could hurt the company. This could arise through natural disasters or man-made disasters. If such events were severe enough and resulted in unprecedented claims activity, there is a small chance that CINF could be rendered insolvent.

Summary: The Dividend King Now Has Market-Beating Potential

{kind=link}

{kind=link}

As I have alluded to throughout the article, CINF has always been a fundamentally superb business. Valuation is the catalyst that has led me to upgrade the stock to a buy.

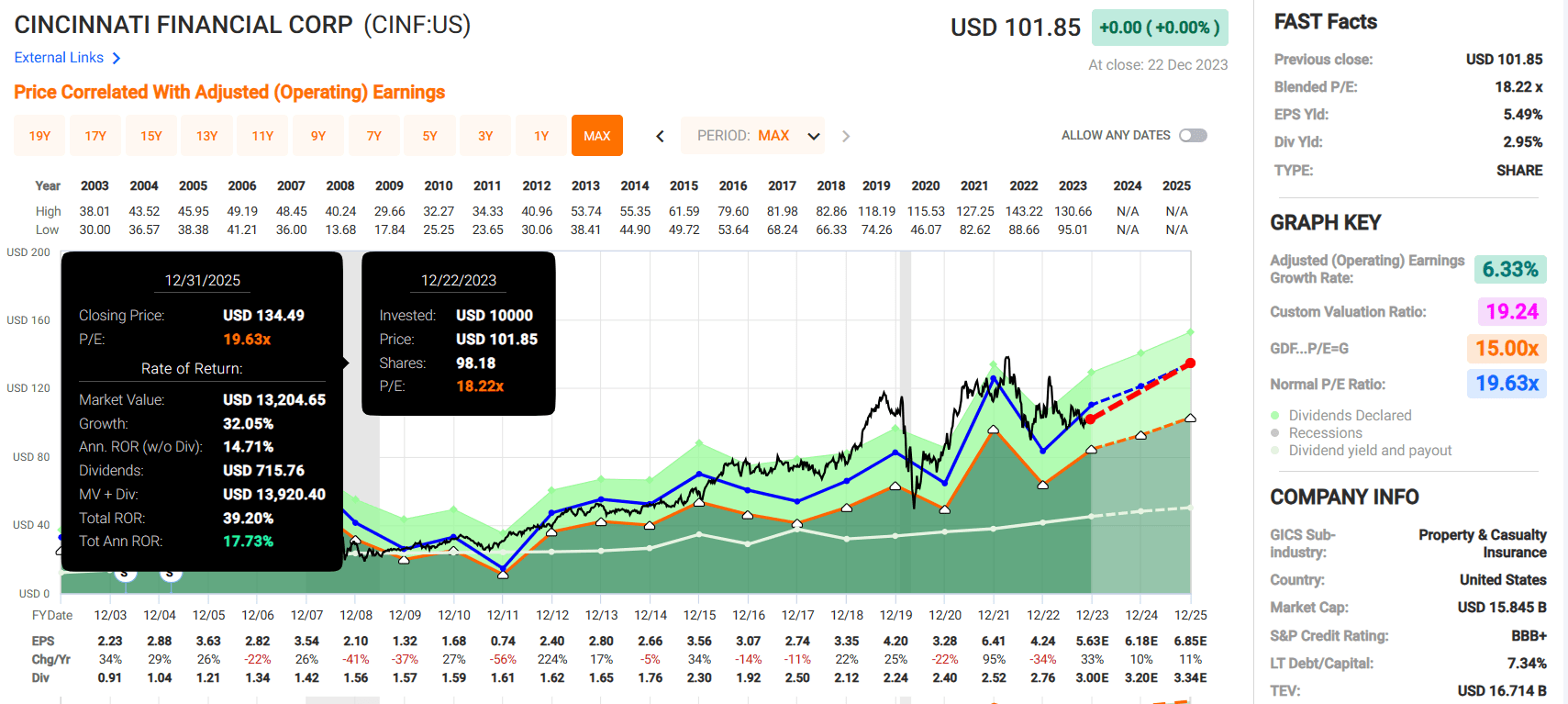

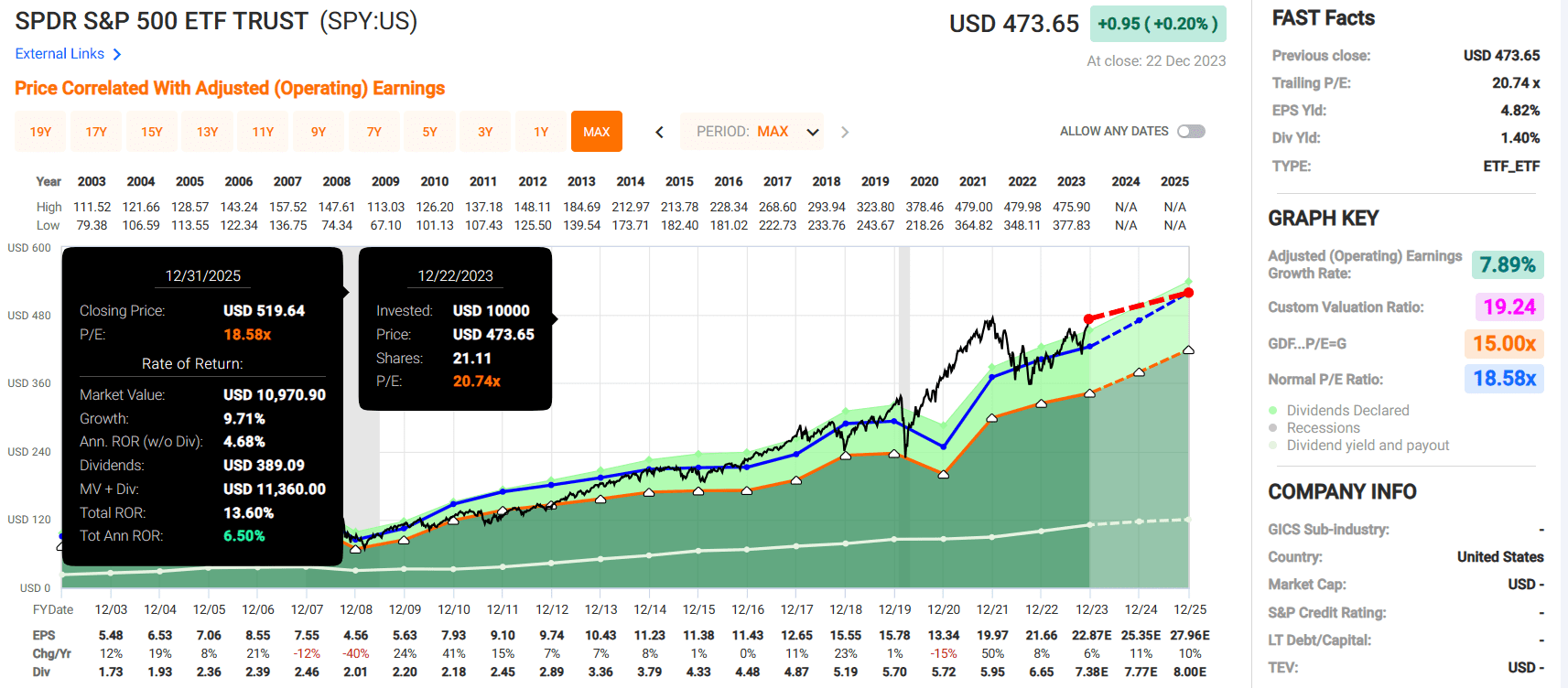

CINF's 18.2 blended P/E ratio is below its normal P/E ratio of 19.6 per FAST Graphs. This below-average valuation combined with its near-3% yield and double-digit earnings growth consensus could generate 39% total returns through 2025 from the current share price. Of course, that is if CINF grows as expected and reverts to its normal P/E ratio during that time. That's nearly triple the 14% cumulative total return potential of the SPDR S&P 500 ETF Trust ( SPY ) through 2025, which makes CINF compelling to me.

For further details see:

Cincinnati Financial: This Dividend King Is Finally A Buy