RBBN - Clearfield: If You're Looking For A Bargain Here's One To Consider

2023-12-26 17:05:30 ET

Summary

- Clearfield, Inc. stock has had a horrific year: it's down almost 70 % this year.

- Given the fall, Clearfield stock now looks cheap and is available at an enterprise value to revenue (EV/R) ratio of just above 1.

- Steps taken by management to support growth aid the quantitative factors suggesting future outperformance. I'm issuing a Buy rating but recommend holding Clearfield, Inc. stock in a diversified portfolio.

Investment thesis

Clearfield, Inc. (NASDAQ: CLFD ) designs, manufactures, and distributes fiber optic connectivity and management products, helping service providers reduce the costs associated with establishing a fiber optic network.

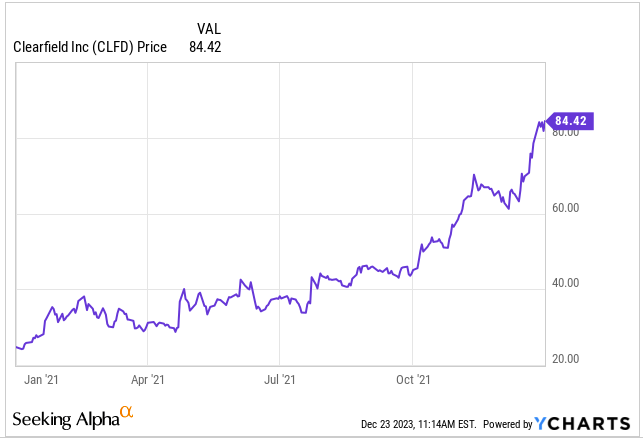

Fiber optic Internet saw surging demand during the COVID pandemic, and Clearfield's stock price followed suit:

{kind=link}

This year, however, the common stock of Clearfield has suffered greatly.

The share price is down ~70% to near record lows:

{kind=link}

In this analysis, I examine what caused Clearfield's poor performance, and I take a look at quantitative factors pointing to future outperformance. I also evaluate steps management has taken to address the issues.

Based on my findings as outlined below, I'm issuing a Buy rating for Clearfield, and I suggest holding it in a portfolio of similar issues.

Reasons for the poor performance

With the exception of the summer months, 2023 has seen Clearfield's stock in an almost unbroken downward spiral. It started in January, with much of the drop probably relating to a late 2022 public offering of 1.2 million new shares. The proceeds from the public offering were to be used for working capital and general business purposes. But any issuing of new shares has a dilutive effect on existing shareholders.

Then in May came another substantial drop following months of a sliding stock price. Clearfield slumped 24 % as it guided much lower full-year results. The company attributed the lower guidance to customer order trends and an anticipated normalization of inventory carrying practices at customer sites. In other words, demand had been extraordinary in the previous couple of years but have since normalized.

The stock performed well during much of the summer, but started sliding again after Northland downgraded the issue from "Outperform" to "Market Perform." It has only recently recovered some.

Priced very cheaply along with its industry

On a statistical level, Clearfield is priced cheaply. It trades at an enterprise value to revenue (EV/R) ratio of 1.1.

This means a buyer for control would - theoretically - only have to pay a purchase price approximately equivalent to Clearfield's revenue to gain full control of all assets (through the purchase of all equity and debt at market).

I've often analyzed companies that trade at even more depressed levels, but Clearfield's EV/R ratio appears in line with its industry, and this industry appears to be out of favor in general as Clearfield's peers trade at similar EV/R ratios:

| Company |

| EV/R ratio |

| Clearfield |

| 1.1 |

| Netgear (NASDAQ: NTGR ) |

| 0.3 |

| Ribbon Communications (NASDAQ: RBBN ) |

| 0.9 |

| Aviat Networks (NASDAQ: AVNW ) |

| 1.1 |

| AudioCodes (NASDAQ: AUDC ) |

| 1.5 |

| Gilat Satellite Networks (NASDAQ: GILT ) |

| 1.0 |

I'm using the EV/R ratio because more traditional metrics - such as price-to-earnings (P/E) or price-to-free cash flow (PFCF) - often aren't meaningful when analyzing distressed enterprises. As seen, Clearfield's EV/R ratio and the EV/R ratio of its peers seem quite attractive.

Further, Clearfield is a small-cap company, and this descriptive fact alone underscores how - from a statistical level - the market seems to have overreacted against the issue. I believe this happens more frequently to small caps than larger companies.

Some qualitative factors suggest we've seen the bottom

I don't suggest trying to pick the bottom of a market, but some factors on both a macro and micro level suggest better times could be upon Clearfield: First of all, projections show significant growth potential for fiber internet over the coming decade. Between 2022 and 2028, fiber optics markets in the U.S. and Europe have been projected to grow as much as ~75 %. There's a clear secular trend here that former means of internet access, including the coaxial cable connection, are being replaced by new and faster fiber optical connections. On a macro level, companies like Clearfield should benefit from these trends.

On a more company specific note, management seems to agree that the stock has gotten too cheap. Clearfield's board of directors recently authorized an increase to the company’s common stock share repurchase program from $22 million to $40 million. The company said in the announcement that:

This strategic move reflects the Board’s strong conviction that our current share price is undervalued relative to our long-term opportunity. - Cheri Beranek, CEO Clearfield, Inc.

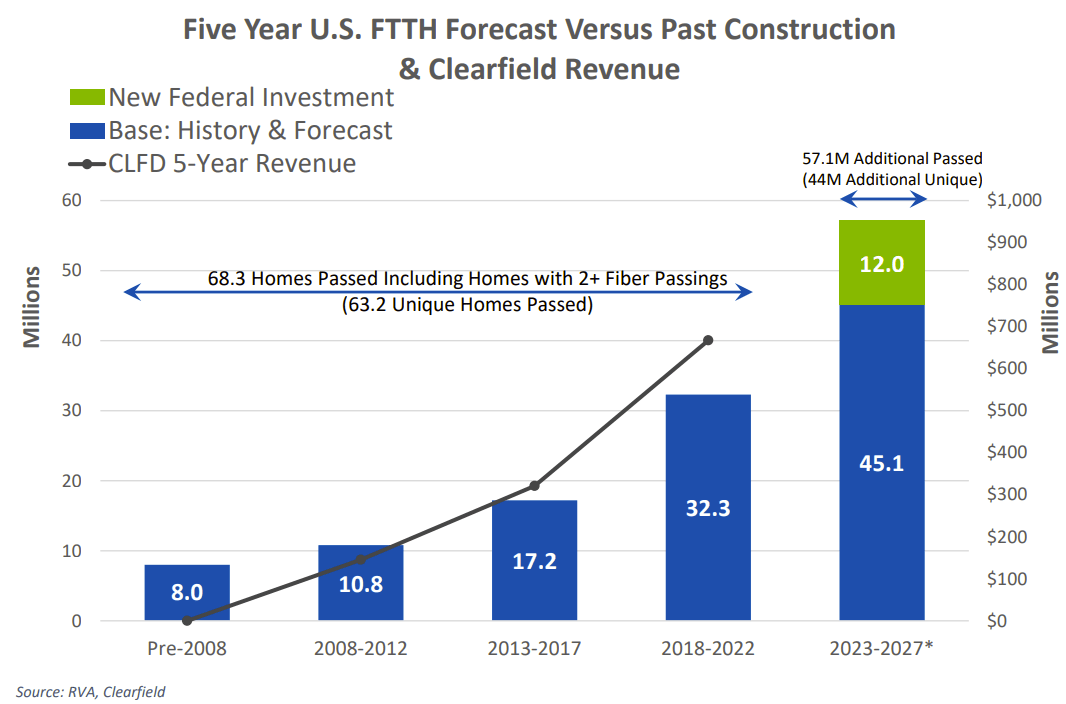

In terms of operations, Clearfield sees growth in its FTTH ("Fiber To The Home") segment in particular, in part because of expected federal funding for this initiative. Put simply, the government supports expansion of fiber Internet access to various areas in support of economic growth, remote working abilities etc. in such areas - and Clearfield expects to continue growing as part of that:

Clearfield investor presentation

{kind=link}

In other words, Clearfield can be projected to grow both on a general company level - through FTTH and other initiatives - and on an EPS level through buybacks. This development is further supported by a general trend towards transitioning internet access to fiber.

On a final note, I'll highlight that Clearfield is a very financially stable company. Clearfield has ~$168 million in cash and equivalents against just $40 million in total liabilities (that's including all accounts payable, leases etc.), and the company has no long-term debt. This should also support Clearfield going forward.

Risks

Given Clearfield's recent performance, I think it's fair to label it a "distressed security," if not fundamentally then at least at a technical level. Buying distressed securities can be extremely lucrative since they are often avoided by the market at large. This can lead to very substantial upside if the individual investment works out. On the other hand, any individual such issue carries with it the risk that just that particular case doesn't work out.

To manage this risk, I suggest buying distressed issues when they are available at very cheap levels fundamentally and technically, and they should only be bought alongside other similar issues. This diversification spreads the risk while maintaining the statistical advantage.

On a more business or operational level, I see competition as a main risk. As pointed out above, Clearfield faces competition from several other actors. Maintaining good customer relationships and remaining innovative will be key for the company to manage this risk. Clearfield's strong balance sheet should also help it navigate the competitive environment.

Key takeaways

Clearfield is engaged in the fiber infrastructure business. The share price performed incredibly in 2021. This year, it's taken a heavy beating.

Some quantitative factors suggest the issue has now become too cheap. These include its low EV/R ratio.

There also appears to be a beneficial growth environment in the fiber industry going forward. Management recognizes this and has initiated a substantial share repurchase program. Management also expects growth from federal funding of FTTH initiatives.

With Clearfield's strong balance sheet, it should be able to navigate the competition that I see as its main operational risk.

For the individual investor, the main risk in buying a distressed security like Clearfield is the downside risk in any such issue. I suggest holding Clearfield in a well-diversified portfolio of similar issues. I’ve rated a few other such issues here on Seeking Alpha, including Hawaiian Electric Industries (NYSE: HE ) and Cambium Networks (NASDAQ: CMBM ).

For further details see:

Clearfield: If You're Looking For A Bargain, Here's One To Consider