ENFN - Clearwater Analytics Holdings: Valuations Have Run Up Ahead Of The Fundamentals

2023-09-13 11:03:09 ET

Summary

- Clearwater Analytics Holdings, Inc. is trading at a high valuation despite having a small addressable market and limited sectoral focus.

- The company offers B2B SAAS investment management solutions primarily to the buy side and large corporations.

- The valuation of Clearwater is significantly higher than its peers and is expected to undergo a downward re-rating.

Summary

Clearwater Analytics Holdings, Inc. ( CWAN ) or Clearwater trades at over 12x of its revenue, despite having a rather small share of its addressable market and somewhat limited sectoral focus. We think the premium that the company enjoys is overdue for a correction. We detail out our thesis below.

Business

Clearwater offers B2B SAAS investment management solutions offered primarily to the buy side (asset management) and large corporations.

August 23 Clearwater Investor Presentation

{kind=link}

Some of Clearwater’s competitors include:

- SS&C (Advent, Camra, Maximus, and Singularity products),

- State Street (PAM and outsourced service offerings),

- SAP,

- BNY Mellon’s Eagle product,

- Simcorp’s Dimension,

- BlackRock’s Aladdin,

- FIS’s iWorks

- Northern Trust

- Enfusion

- Outsourcing providers and internal IT teams

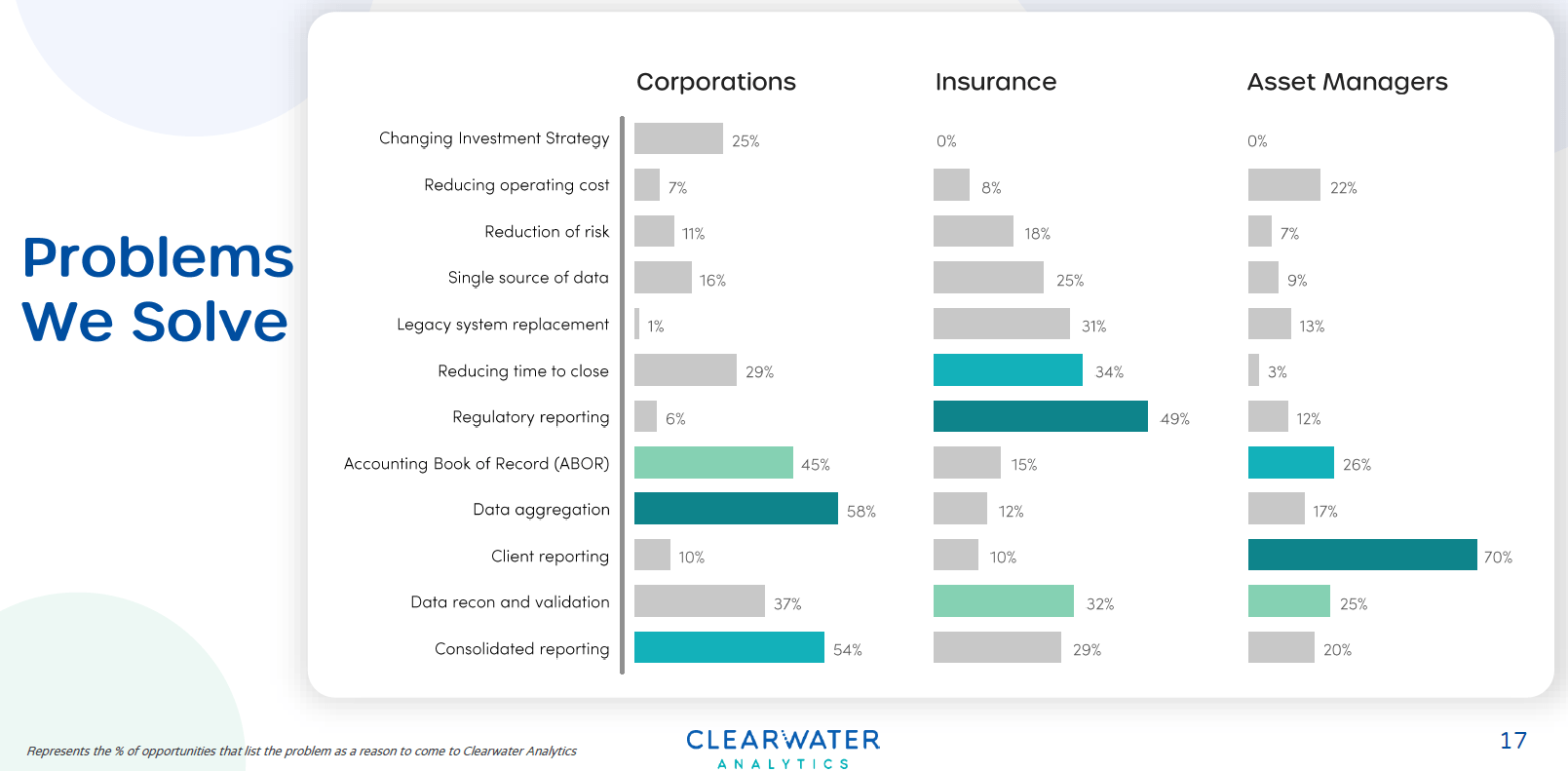

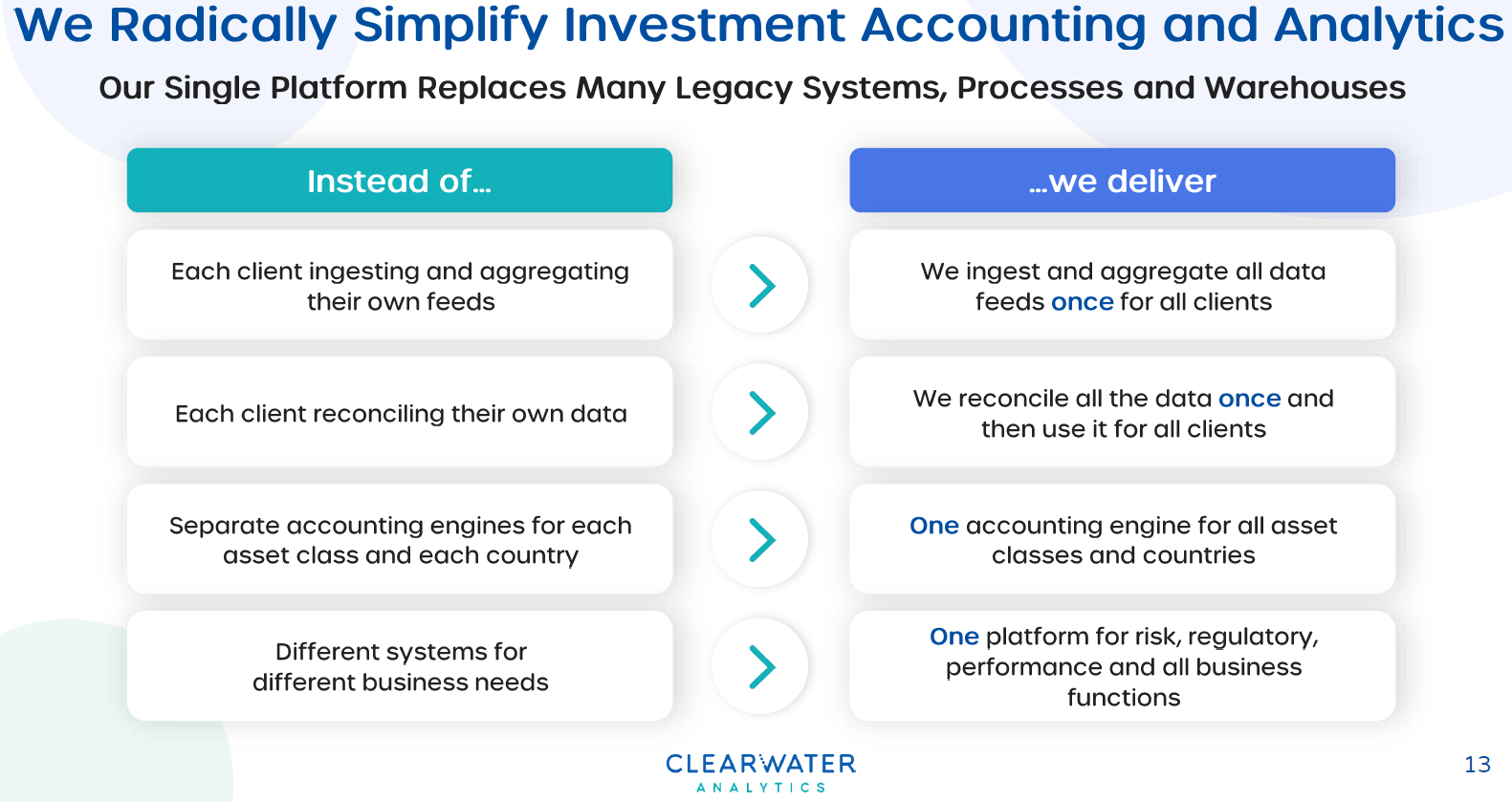

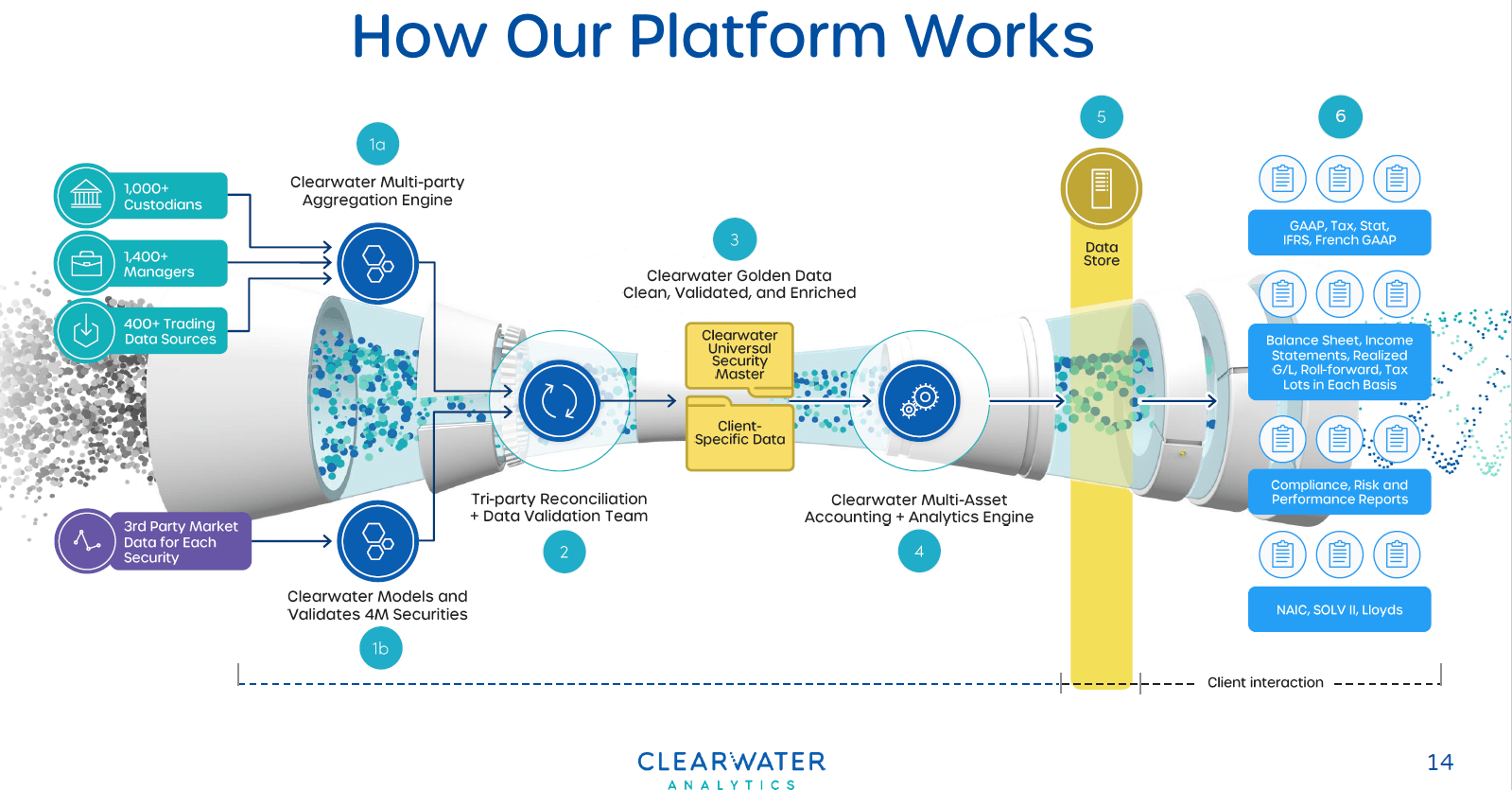

Simplifying the technology, Clearwater’s systems help to:

- gather information from disparate sources

- clean up data

- standardize data to be fed into analysis engines

- deliver per clients’ requirements

August 23 Clearwater Investor Presentation August 23 Clearwater Investor Presentation

{kind=link}

{kind=link}

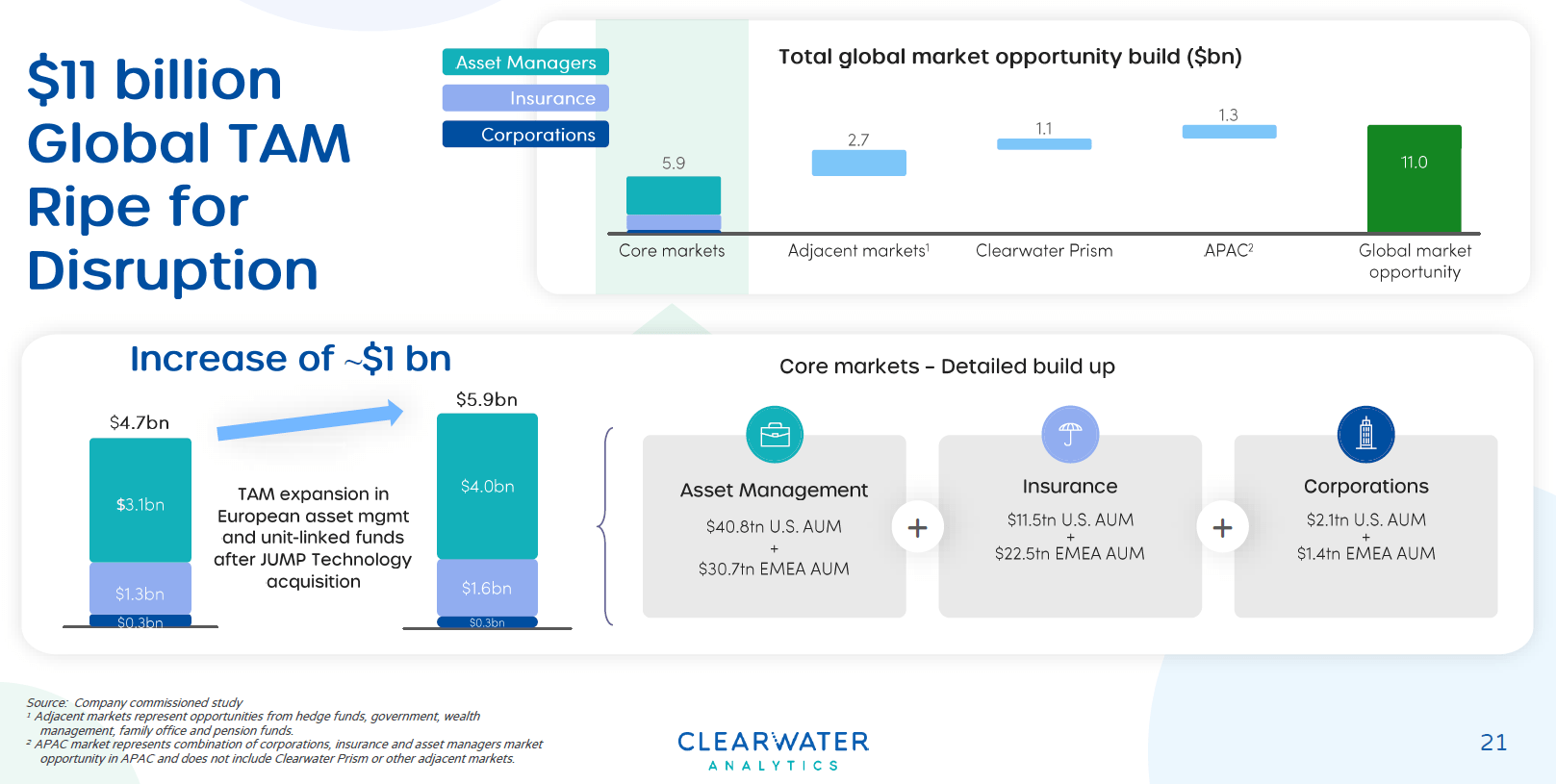

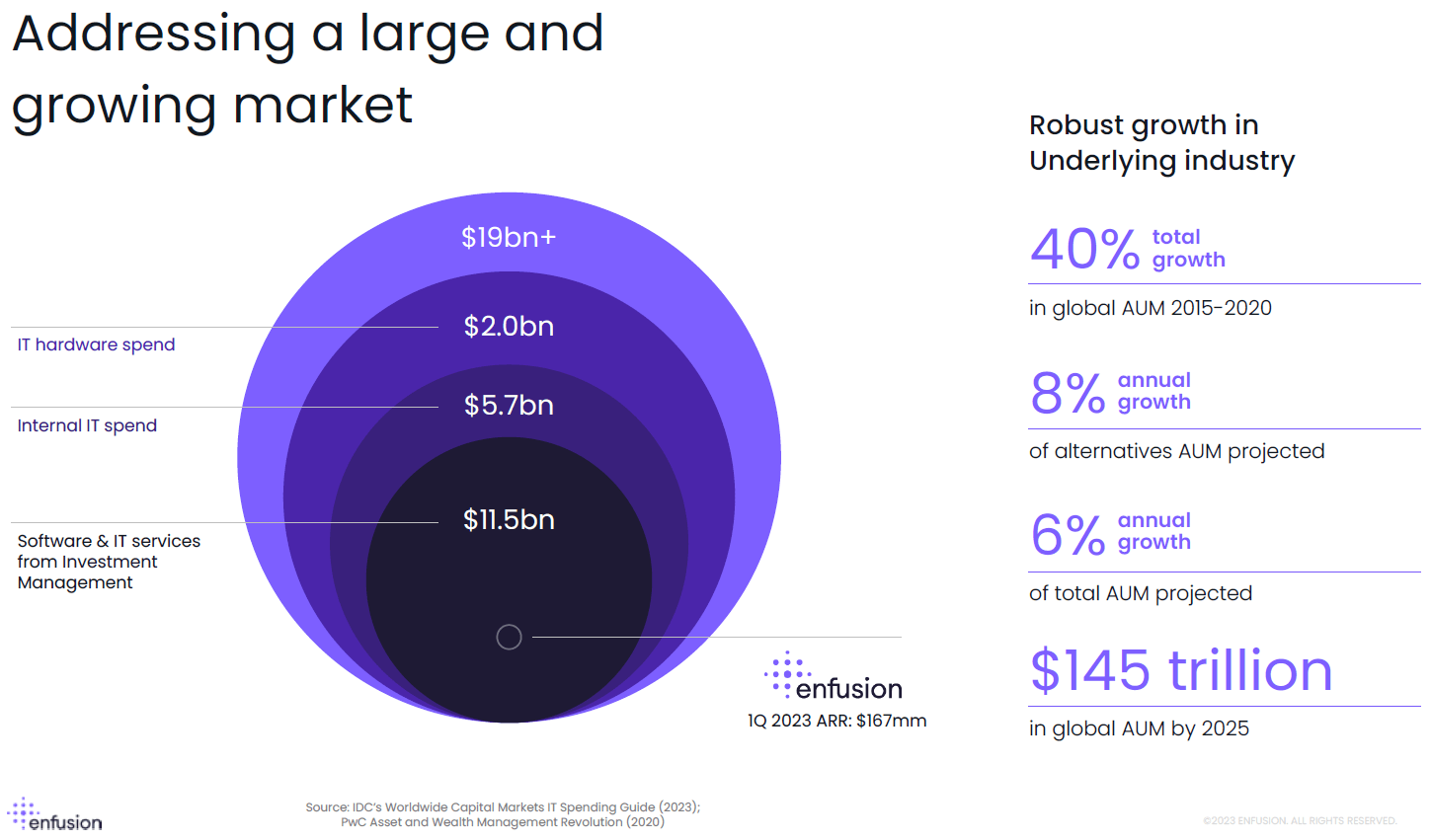

While it may seem rather simple, the complexity associated with the varied data feeds across different asset classes to be reported across several regulatory regimes is a herculean task and has led to an $11-12 billion total addressable market or TAM.

August 23 Clearwater Investor Presentation

{kind=link}

Enfusion ( ENFN ) a near direct competitor also supports the TAM claim.

Enfusion 1Q 2023 Shareholder Letter

{kind=link}

Of this annual $11-12 billion, Clearwater expects to garner $365 million (mid-point of guidance) or 3% of the TAM.

August 23 Clearwater Investor Presentation

{kind=link}

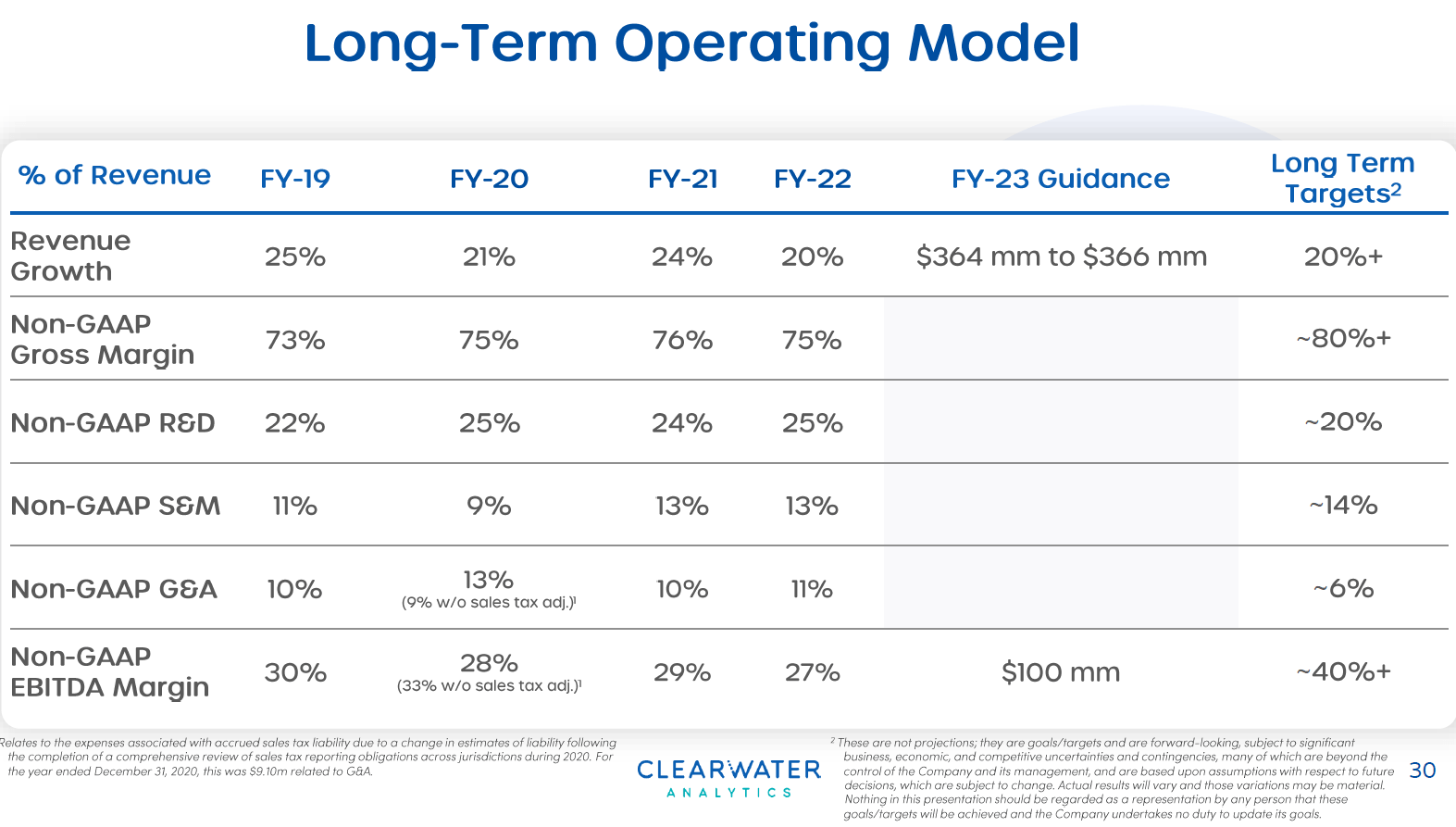

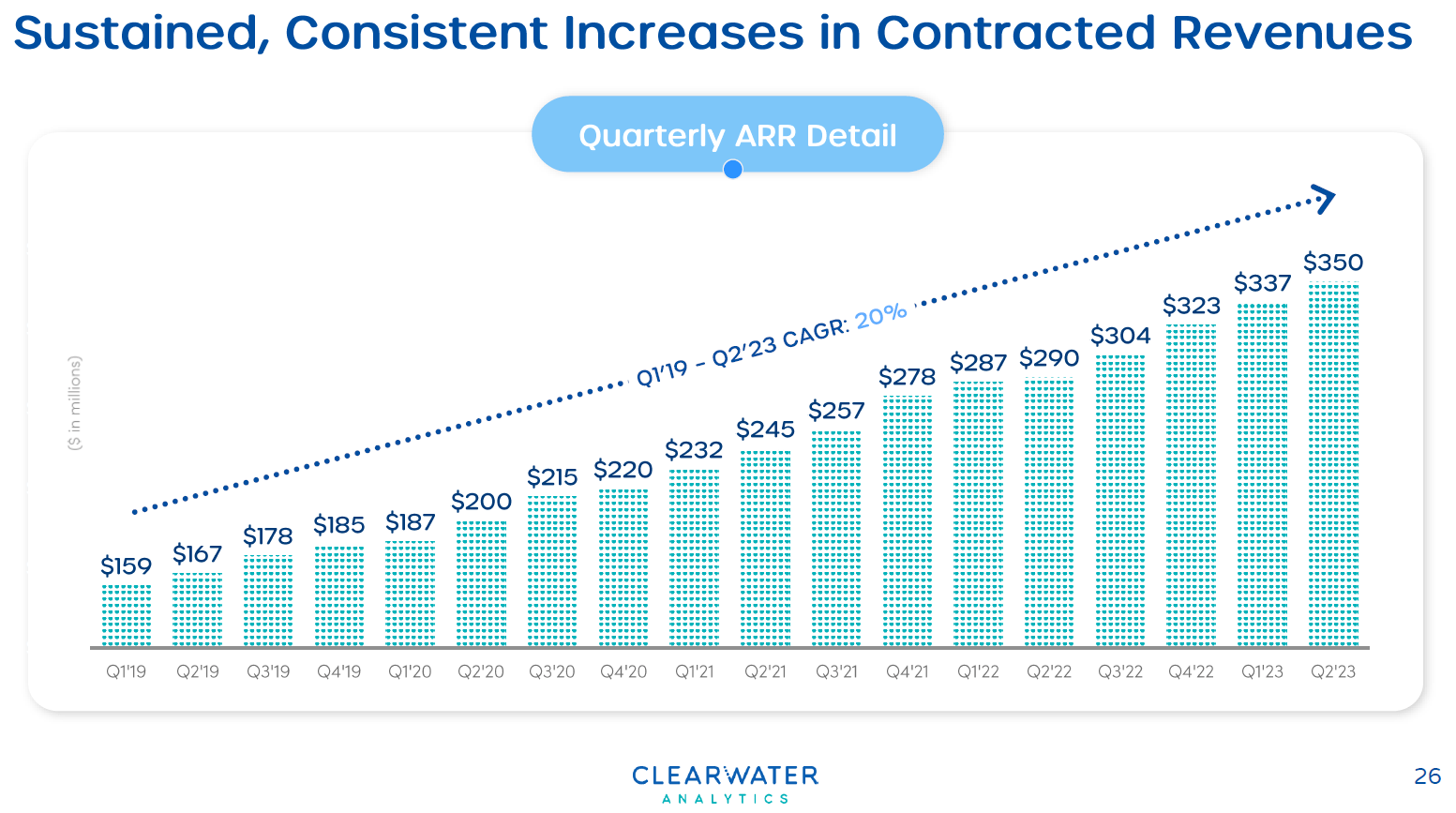

The strength of the company’s operating model can be seen in Clearwater’s ARR growth, gross margins, and strong retention rates.

August 23 Clearwater Investor Presentation

{kind=link}

So far so good, coming to the elephant in the room – valuation!

Investment thesis

{kind=link}

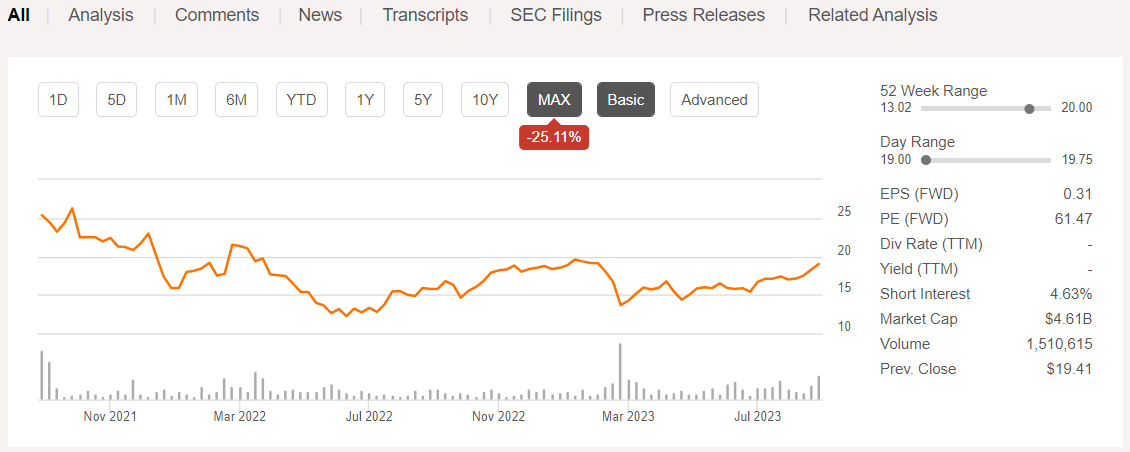

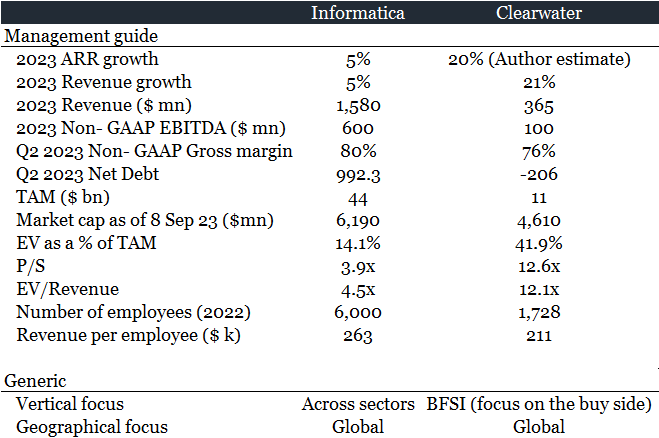

As of 8 th Sep 23, Clearwater had a valuation of $4.6 billion. Compared to the expected revenue of $365 million, it translates into an EV/Revenue of 12.1x for end of 2023 and 10.1x for the end of 2024.

Seeking Alpha, Management guidance, Author’s analysis

{kind=link}

The Bessemer Venture Partners Cloud Index, of which Clearwater is also a part of, shows a median of EV/Revenue of 5.5x-6.1x.

Bessemer Venture Partners Cloud Index (8th Sep 23)

{kind=link}

Hence, a company having 3% of the annual TAM trades at double of where the peers are trading at.

Can a company growing at the market average rate trade at double the market multiple? Hardly.

In addition to the valuations, when sector leaders trade at much lower multiples, we find it hard to see why Clearwater should trade at its current multiples. Let us try to expand upon this answer.

In a crude way, Clearwater’s business model can be thought of as a vertical focused version of Informatica (INFA).

We previously wrote on Informatica here.

IDMC helps collate, curate and correlate data across an organization's data assets. This data and analysis can then be used to manage user experiences, develop automation strategies, and build out analytics to infer behavioural trends better.

Source – Informatica: Significant Upside Potential

From a vertical focus, Informatica is spread across the board.

Informatica Q2 2023 Investor Presentation

{kind=link}

On the key metrics, here is how the two of them stack up:

Seeking Alpha, Clearwater, Informatica and Author Analysis

{kind=link}

The market is either paying Clearwater an abnormal multiple for revenue growth, with complete disregard for the addressable market, profitability etc or Clearwater’s multiple can be attributed to its focus on the buy side.

In either case, we think a correction is needed. As shown above, Clearwater’s valuation reflects 42% of its TAM and hence the scope to go up against larger and more well-established competitors is limited, which is likely to lead to a correction.

In case it is the market’s love for the buy side, the cost of money has undergone a significant change and asset managers today are fighting for every bps of that management fee.

The McKinsey Global Private Markets Review ( March 2023 report ) notes that the AUM growth declined in 2022.

Furthermore, a recent Pitchbook article notes how management fees have been under pressure .

In the backdrop of declining AUMs and falling management fees, the overall fall in revenues is likely to translate into greater cost pressures for asset managers.

Hence, continuing to pay the likes of Clearwater in such a macro is quite an ambitious assumption. Furthermore, growing competition is unlikely to let Clearwater continue the margins it has in the past.

As an example, if Clearwater were to start doubling down on the asset management space Clearwater would have a serious challenge. Of-course, Generative Artificial Intelligence or Gen AI has been changing the landscape for all, but not to an extent where it can upend the technological advantages of older players.

Informatica's AI differentiation in this market comes from three factors. First, is an understanding of the enterprise data ecosystem. Very few vendors can claim an understanding of an enterprise's data ecosystem, which comes from being able to have a metadata inventory. But beyond that, being an independent and neutral and at-scale vendor in this space. The second is, training LLMs on metadata from thousands of data management projects. Again, only a handful of vendors if any, can do that at scale. And third is, comprehensive data management capabilities. When enterprises think of data management, they just don't think of ELT pipelines or ETL pipelines or just data catalog or just data quality in isolation. And enterprise data management project requires all these capabilities, working in tandem and on top of a metadata powered platform, which is only available with IDMC.

Source: Informatica Q2 2023 earnings call on Seeking Alpha

Another aspect where Clearwater can get disrupted is from the migration focus it has.

I do think it can completely change how we think about onboarding. And as you know onboarding is the hard part. And once you have done the transformation then of course Clearwater gives you the full functionality you could want and the agility and the analytics. And so we feel like GenAI could transform how we onboard it.

To take an example let's say we move a client to onboard them from a competitive legacy platform, while we probably have done 30, 40 of those transformation onboarding exercises from that same legacy platform. You point GenAI to that and the next onboarding you're doing and it can do it meaningfully faster, right? Because it has learned from all those 30 onboarding exercises you've done.

So we do think that's transformative. We do think it changes the risk profile of the onboarding exercise and really time to value meaningfully. So look we think it is actually perhaps the biggest use case when it comes to on the efficiency side of it, not on the revenue side but just on the efficiency side.

Source: Clearwater Q2 2023 earnings call on Seeking Alpha

Migration is really the key to build trust with a client for Clearwater. Once the data is moved, reconciled, and standardized, this is when the analysis on top of it can begin. Hence ensuring that the data movement phase is seamless is where trust builds up.

Informatica (and some others) have automated process that can do such migrations efficiently. Hence while the Clearwater management thinks it now has a strong product in the area, it is somewhat like relying on a rather commodity offering (in context of the technologies under discussion) to sustain network effects and growth. Again, in our opinion, Clearwater is pinning its hopes on winning in a market where it is rather new and existing players (who already have a head start) might find it easy to disrupt.

In the same breath, we will also want to highlight that most of these are developing and there definitely are risks to our thesis of Clearwater getting disrupted.

Risks to our thesis

- Sectoral understanding: The asset management world is a bit different from the non-buy side. The eccentricities of this sector demand sectoral knowledge and if Clearwater can continue to differentiate itself, the company may avoid disruptions.

- Interest rate environment: The rise of the asset management industry was a function of cheap money. Should the Fed take a more benign view of things, the mere act of signaling will send assets under management or AUM soaring, which will then lead to an upward revision in the TAM.

- Gain of market share from 3% to 6%: We expect the company to grow at 20% and hence should potentially double its share by 2027-28 . However, we still think the valuation even on a 2024 basis is expensive.

- Potential acquisition: While the valuation remains elevated, Clearwater becoming a potential acquisition target would need a complete revisit of our thesis.

Outlook

Irrespective of the risks of Clearwater not getting disrupted, we think a downward re-rating of the company (given its financial metrics and lack of GAAP profitability) is around the corner.

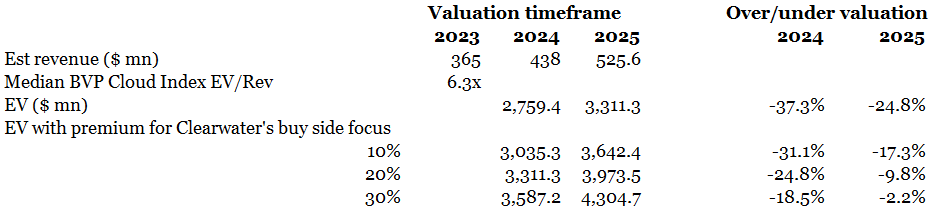

Looking out to 2025, we find that even after applying a premium for Clearwater’s buy side focus, it is overpriced.

Seeking Alpha, Management guidance, Author’s analysis

{kind=link}

While we like the narrative around Clearwater, we continue to believe that is significantly overvalued and would avoid the stock.

For further details see:

Clearwater Analytics Holdings: Valuations Have Run Up Ahead Of The Fundamentals