CLW - Clearwater Paper Corporation: Lower Q4 Guidance

Summary

- The company announced lower 2022 estimates. This was due to higher maintenance requirements.

- Here at the Lab, we believe that the company was overly discounted on Q3 reporting day.

- There is a capacity constraint issue to report and will not be able to gain higher market share.

- This will support price over volume. Valuing Clearwater with a 5.5x EV/EBITDA, we derive a buying opportunity.

Here at the Lab, we've never been optimistic about Clearwater Paper Corporation ( CLW ). Last time, we decided to follow up with an analysis called - we totally missed it ; however, today, after having investigated the company's Q3 results and its latest development (the company just released Q4 warning on lower EBITDA and Fiscal Year 2022 projection), we can confirm that we were not totally wrong in our previous publication. Unfortunately, we are following the stock price evolution and that's never a good thing.

In detail, Clearwater Paper announced an update on the company's guidance for Q4 and FY2022 numbers. Financially speaking, due to higher maintenance requirements, Clearwater forecasts an adj. EBITDA between $28 and $34 million in the last year-end quarter, and projects a yearly adj. EBITDA at €230 million. Operationally speaking, the company declared that the Lewiston mill is now in full operation, whereas the Idaho and Arkansas mills are reporting issues that have been identified but are still not resolved. In addition, it is important to report that the company is planning a new intervention in the Lewiston mill to replace a boiler tube in 2023 Q1. For this reason, Clearwater Paper's share price declined by more than 2%.

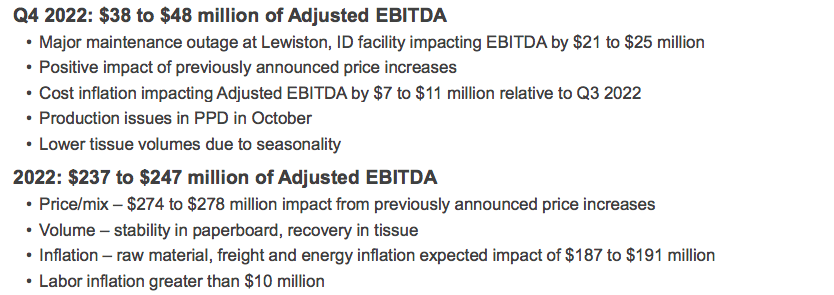

Looking at the Q3 results , at that time, the company was forecasting adj. EBITDA estimates between $38 and $48 million and between $237 and $247 million on a quarterly and yearly outlook. The negative investor sentiment continues and is definitely not supportive of the company.

Clearwater Paper Corporation Q4 and FY 2022 Guidance (Clearwater Paper Corporation Q3 Results Presentation)

{kind=link}

After the Q3 reporting day, the company declined by more than 20% and fully offset what positively happened during the half-year release. To be fair, we believe that this negative stock price reaction was overly pessimistic. Here are our key takeaways:

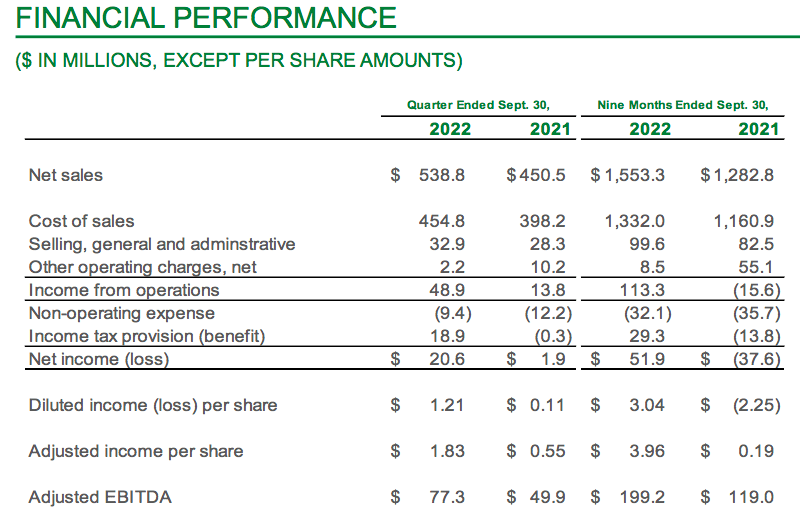

- In Q3, the company's top-line sales reached $539 million and were up by 20% versus last year-end quarter (Fig 1). Good performances were recorded both in the Pulp & Paperboard division and also in the Consumer Products segment;

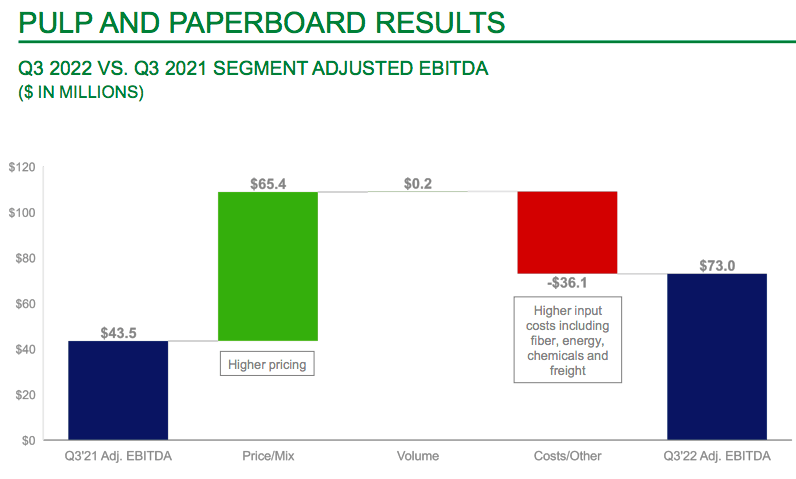

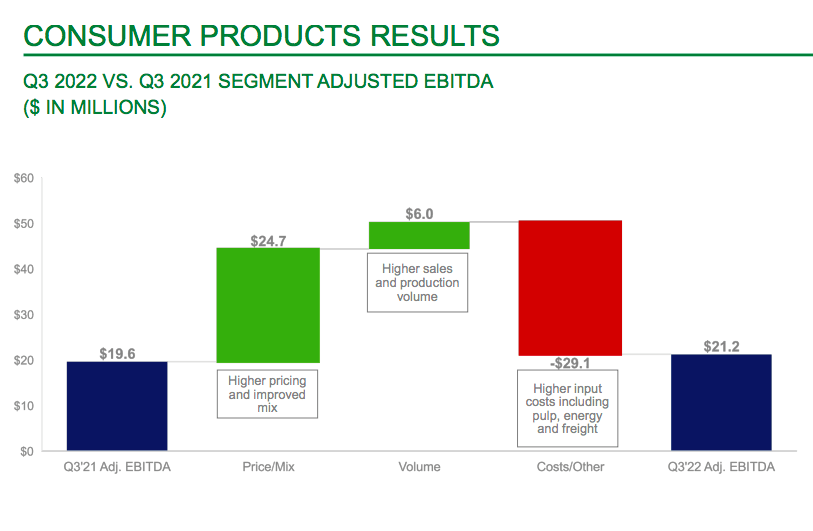

- The company's adj. EBITDA recorded $77 million and was up thanks to a positive pricing delta. And again the two divisions were supportive in the Q3 accounts (Fig 2 and 3);

- Clearwater Paper continued to lower its debt position and year to date, it was reduced by $106 million. In detail, the company repurchased $25 million of notes due in 2025. As already noted, the company has no maturity until 2025 and a stable rating of Ba2 just reaffirmed by Moody's;

- On the buyback, the company repurchased a value of $1 million in shares in Q3, with $25 million worth of stock still remaining on the plan.

Fig 1

Clearwater Paper Corporation Financials

{kind=link}

Fig 2

Pulp and Paperboard Positive Pricing Delta Evolution

{kind=link}

Fig 3

Consumer Product's Positive Pricing Delta Evolution (Clearwater Paper Corporation Q3 results presentation - Fig 3)

{kind=link}

Conclusion and Valuation

As reported in the Q&A, the company is running at full capacity and higher maintenance outages heavily impacted Clearwater's financials. According to the latest disclosure, we are updating our internal number, and we forecast higher expenses in the range of $25 million. CAPEX will grow over the next few years, and we now foresee a number between $65 and $70 million (higher than the last years). More important to note is the company's share in private labels. Due to the macroeconomic slowdown and inflation effect, there is an acceleration toward non-label products. The CEO pointed out the European market evolution and how private branded shares are north of 50%.

However, he does not think Clearwater will get to 50% in the near term in the US. In the Q3 Q&A, he said that this target is unrealistic, but he emphasized :

There are still plenty of runways to gain for private brands to gain share. We have also noticed consumers gravitating towards lower-cost items, smaller pack sizes. So some of that is happening. But I think that remains to be seen exactly how consumers behave in heading into next year.

Currently, there is a capacity constraint and inorganic acquisition optionality. Regarding the valuation, updating our numbers, and still valuing the company with a 5.5x EV/EBITDA, we derive an enterprise value of $1.26 billion. Calculating the equity value, deducting debt-like obligations, and adjusting for the cash (that reached $50 million in Q3), we arrive at an equity value of $750 million, and then we imply a 20% upside from today's price.

For further details see:

Clearwater Paper Corporation: Lower Q4 Guidance