CLW - Clearwater Paper: Operations Are Improving And Debt Should Keep Decreasing

2023-10-10 00:24:23 ET

Summary

- Sales are expected to remain stagnant in the second half of 2023 and 2024, keeping investors cautious.

- Gross profit and EBITDA margins improved significantly during the first half of 2023, boosted by product price raises.

- The company should keep deleveraging its balance sheet as inventories are higher than usual.

- The company's two segments complement each other well, offsetting potential declines in one segment with increased demand in the other during recessionary times.

- This represents a good opportunity to buy the company's shares and wait for its prospects to improve.

Investment thesis

Operations of Clearwater Paper ( CLW ) have recently shown early signs of recovery after a few years marked by stagnant revenues and weakening margins. Both gross profit and EBITDA margins increased significantly during the first half of 2023, and revenues are higher compared to pre-pandemic years boosted by product price raises. Despite this, sales are expected to remain stagnant in the second half of 2023 and 2024, which is keeping investors on the sidelines as the P/S ratio is 28% lower than the average of the past 10 years. Meanwhile, a potential recession as a result of recent interest rate hikes also poses a risk for the short-to-medium term, but the two reportable segments of the company complement each other very well in the sense that demand in the Consumer Products segment tends to increase in difficult times due to increasing sales of private label tissue products, thus offsetting potential declines in the Pulp and Paperboard segment.

In recent years, Clearwater has invested heavily to optimize its manufacturing facilities and launch new products, and long-term debt has been reduced significantly since 2020. Furthermore, the recent increase in inventories suggests that cash from operations will be strong in the near future as the management has already started their conversion into actual cash, so long-term debt should continue to decrease thanks to higher-than-usual cash from operations. If we add to this that pessimism currently reigns among investors due to the current macroeconomic context (in terms of expected stagnant revenues) and that the company has been successfully operating for more than a century, we have a company that, in my opinion, will provide potential capital returns to investors patient enough to wait for the company's prospects to improve along with the improvement of the macroeconomic panorama and a further reduction of debt. Additionally, lower pulp prices are expected to remain a tailwind for the foreseeable future.

A brief overview of the company

Clearwater Paper is a manufacturer of bleached paperboard and consumer and parent roll tissue. The company was founded in 1900 (and spun off from PotlatchDeltic Corporation ( PCH ) in 2008) and its market cap currently stands at $615 million as it employs around 3,000 workers. The demand for the company's products has some resilience even in difficult times as they are used for essential products, such as at-home paper tissue products, food packaging, pharmaceuticals, and cosmetics, while their sustainable nature means that trends play rather in Clearwater's favor in the long term.

The company operates under two main business segments: Pulp and Paperboard and Consumer Products. Under the Pulp and Paperboard segment, which generated 55% of the company's total revenue in 2022, the company manufactures bleached paperboard for the high-end segment of the packaging industry, as well as solid bleached sulfate paperboard. Under the Consumer Products segment, which generated 46% of the company's total revenues in 2022, the company manufactures at-home tissue products, including bath, paper towels, facial, and napkin products for private labels of large retailers.

Despite recent revenue increases and improved profit margins, the share price remains partially depressed as a result of more moderate expectations in the short and medium term which, in my opinion, represents a good opportunity for investors with enough patience to wait for the company's prospects to improve.

In this regard, shares are currently trading at $36.79, which represents a 51.39% decline from all-time highs of $75.69 reached on January 29, 2015, as revenues have remained stagnant in the past 10 years despite recent improvements. Also, the investments made in recent years have not led to a noticeable improvement in profit margins in the long term, although in the short term, profit margins have shown strong signs of improvement. To this, we must add that long-term debt continues to be at relatively high (but very manageable) levels, despite the recent strong deleveraging progress, as a consequence of the strong investments carried out in recent years.

Despite this, it seems that the situation is beginning to improve, as reflected by the recent increases in the share price, as revenues are starting to recover boosted by product price increases while the profitability profile is also improving. Also, higher inventories are expected to deliver stronger cash from operations in the coming quarters, which should translate into even lower debt.

Revenues are increasing boosted by product price raises

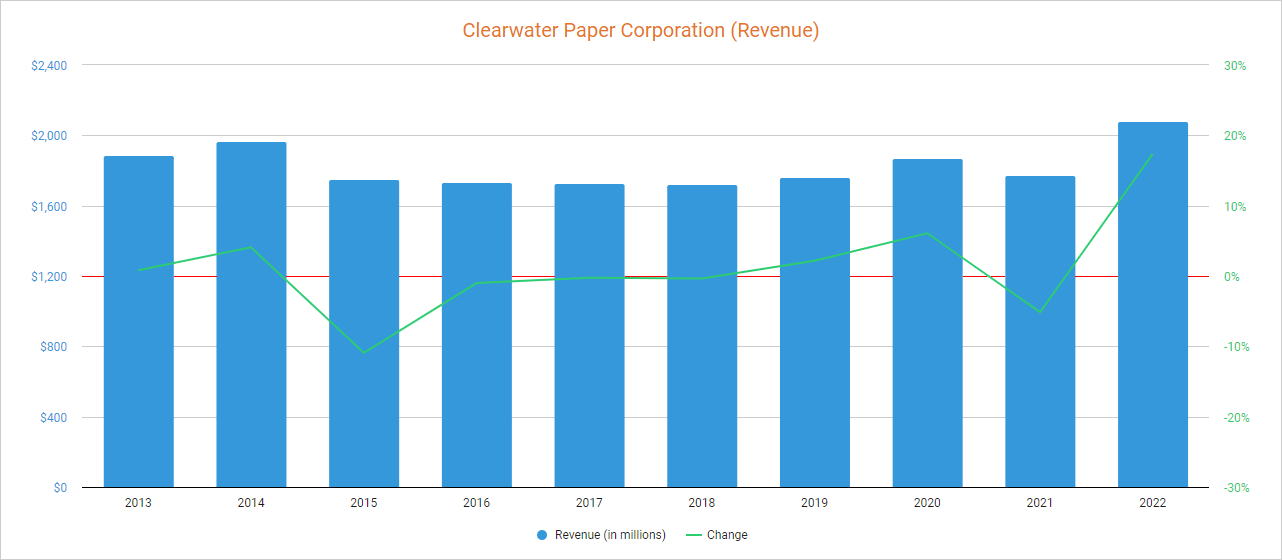

The last few years have caused a lot of frustration among Clearwater Paper's shareholders as revenues remained stagnant, but this trend started its reversal in 2022 as they increased by 17.35% compared to 2021, thus surpassing previous years.

{kind=link}

As for 2023, revenues increased by 7.62% year over year during the first quarter but declined by 0.34% year over year during the second quarter, which should not be a cause for concern as these figures are compared to a strong 2022. Also, the private branded share reached all-time high figures in the past quarter due to consumers looking at ways to offset how inflation is affecting their purchasing power while the company keeps increasing the price of its products to offset higher input costs. Still, paperboard demand remains weak due to customer destocking as consumer spending is decreasing, and revenues are expected to remain flat for 2023 and 2024.

Despite recent operational improvement, in terms of both increases in revenues and profit margins, as well as lower net debt and higher inventories, expectations of flat revenues have kept the P/S ratio at low levels at 0.299, which means that the company generates annual sales of $3.34 for each dollar held in shares by investors.

This ratio is 28.47% lower than the average of the past 10 years and represents a 62.48% decline from 10-year highs of 0.797 reached in 2014, which effectively reflects low expectations for the short and medium-term as investors are placing less value on the company's sales. As for the management, it expects volumes to start improving in the second half of 2023, but a potential recession as a consequence of recent interest rate hikes makes expectations not as promising, at least for the Pulp and Paperboard segment. Despite this, recent product price increases, as well as operational optimization through aggressive investments carried out in recent years have allowed the company to remain profitable.

Margins are improving as price raises have offset higher input costs

Overall, the company has remained profitable over the years as the gross profit margin usually danced at around 12% and the EBITDA margin at slightly lower (yet positive) rates. In recent years, the company has carried out strong optimization initiatives that consisted of the closure of its Oklahoma City converting facility , the sale of its Ladysmith, Wisconsin facility in 2018, and the closure of its Neenah, Wisconsin facility in 2021 due to underperformance.

Profit margins continued improving during the second quarter of 2023 as the quarterly gross profit margin increased to 16.37% and the EBITDA margin to 13.74% boosted by higher volumes in the Consumer Products segment and increased product prices, as well as lower fiber, energy, and transportation costs as pulp costs have steadily declined since the beginning of 2023, which enabled an EBITDA $8 million higher compared to the same quarter of 2022 to $71 million.

Pulp prices are expected to keep declining in the second half of 2023 and stabilize in 2024, which should drive profit margins even higher or at least offset potential impacts from a more recessionary environment. This, together with higher inventories, should increase cash from operations in the foreseeable future, which should surpass expected capital expenditures of $70 million to $80 million for 2023.

Regarding capital expenditures, the company has made significant investments in recent years as it announced a $160 million upgrade to its Lewiston Mill in 2015. It also announced a new tissue machine and converting facility in 2017 with an estimated cost of $283 million and a ~$57 million investment for the purchase and expansion of an existing warehouse.

Also, the company launched its NuVo brand in 2019, a cup stock paperboard with specific properties to adapt to particular food service needs, and in January 2022, the company launched NuVowithBioPBS a compostable alternative to hot cups under the brand. Apart from these launches, in July 2020, the company also launched ReMagine, a folding carton paperboard brand with up to 30 percent post-consumer recycled fiber, which means the company keeps expanding its product portfolio in the sustainable paperboard industry.

But apart from an expected capital expenditure of $70 million to $80 million, we should not forget that the company needs to cover expected interest expenses of $25 million to $27 for the full 2023.

This means that, despite steady declines in interest expenses in recent years boosted by reduced debt, the company still needs to keep deleveraging the balance sheet in order to free up more cash and thus be able to improve the company's prospects in the long term, which should be possible thanks to recent margin improvements and the current inventory destocking process.

The company has the capacity to keep paying down its debt pile

Apart from the aggressive investments carried out in recent years, the company also acquired Manchester Industries , a leading, independently-owned paperboard sales, sheeting, and distribution supplier to the packaging and commercial print industries, for $68.25 million in December 2016. However, in 2020, the company began deleveraging its balance sheet, which resulted in a long-term debt reduction of 19.28% in 2020, an 11.07% reduction in 2021, and a further 12.66% reduction in 2022. As for the past quarter, an increase in cash and equivalents to $41.70 million enabled a net debt reduction of $25 million which, on the other hand, has not helped to improve the balance sheet so far this year as long-term debt remains relatively high at $565.7 million due to higher inventories.

However, the improvements of the past quarter were achieved thanks to improved profit margins and a $5.1 million reduction in inventories through temporarily limited production capacity. These production limitations are expected to remain in force during the second half of 2023 as the management plans to keep converting inventories into actual cash, which should allow for further debt reductions as inventories are very high at $340.4 million.

This means the company is expected to keep deleveraging its balance sheet in the coming quarters as cash from operations should remain high for as long as it keeps emptying its inventories. During the second quarter of 2023, it reported a net income of $29.7 million (compared to $14.7 million during the same quarter of 2022) as cash from operations was $46 million (vs. capital expenditures of $12.8 million and interest expenses of $7.9 million), and although inventories declined by $5.1 million quarter over quarter, accounts payable declined $9.4 million while accounts receivable increased by $7.7 million, which means operations are very sustainable in the current landscape.

In this regard, higher total receivables and lower total payables should also help in providing stronger cash from operations in the coming quarters, so considering positive cash from operations (by operations themselves), high inventories of $340.4 million, and high total receivables of $196.6 million (compared to total payables of $169.7 million), long-term debt has the potential, in my opinion, to be halved within 3 to 4 years, which should release significant value for the company's shares as it would translate into improved prospects.

Share buybacks should eventually return, but it's not a guarantee

The number of shares outstanding declined by 20.64% in the past 10 years boosted by share buybacks, but the decrease stopped in 2017 as profit margins suffered a period of contraction while revenues remained stagnant until 2022 at a time when the company found itself with a relatively high debt exposure as a consequence of aggressive investments and the Manchester Industries acquisition.

During the past quarter, the company repurchased $8 million worth of shares, and $15 million remains on its buyback authorization, and although the management failed to decrease the number of shares outstanding since 2017, the company should have the capacity to continue decreasing the share count as soon as long-term debt reaches even more sustainable levels as it should free up significant cash due to lower interest expenses. However, this is only one possibility because despite having the long-term capacity to continue repurchasing shares, the management could use the cash from operations, once the debt exposure is reduced, for other items such as new acquisitions or further investments in capacity expansion. In this sense, although the management has a tradition of buying back shares during good times, this is never a guarantee.

Risks worth mentioning

In the long term, I consider Clearwater Paper's risk profile to be relatively low thanks to very manageable debt and the essential nature of the products it manufactures, but there are certain risks in the short and medium term that I would like to highlight.

- Recent interest rate hikes could cause a global recession, which could have a direct impact on the company's operations. Fortunately, it is quite likely that a weakening of consumers' purchasing power will make them opt more often for private-branded products, which could lead to an increase in sales in the Consumer Products segment. Nevertheless, there are no guarantees that this trend would fully compensate for potential lower demand in the Pulp and Paperboard segment and a more responsible (austere) use of paper products.

- If demand is reduced and/or the company is unable to maintain a significant reduction in production capacity, it could have difficulty continuing to empty its inventories, which would hinder the ongoing deleveraging process as it would have a direct impact on cash from operations.

- A worsening of the current macroeconomic situation, for example through an increase in pulp or transportation prices or through a drop in demand, could have a negative impact on the company's share price. We must not forget that we are currently living in times of high volatility in the markets. In this regard, the most cautious investors could consider averaging down from current prices by investing in tranches as the share price keeps declining (if it does so).

Conclusion

It is true that the recent changes in Clearwater's metrics are many (and too recent) and that we cannot yet speak of a change in trend, especially due to the macroeconomic context that we are currently experiencing. That is why it is understandable that investors remain on the sidelines. Sales have improved significantly in 2022 and are remaining robust in 2023, but it is also true that this responds to recent product price increases, and not to an increase in demand in both segments. It is also true that profit margins have improved significantly during the first half of 2023, although high volatility in the markets and a potential recession do not ensure that this will continue to be the case.

Be that as it may, I would like to summarize below the four main reasons why I consider that the recent pessimism and caution among investors represent a good opportunity for more patient (and opportunistic) investors. First, the impact of a potential recession would not be as significant as one might expect since the company's two segments complement each other well: during good times, demand for Consumer Products decreases (or stabilizes) and demand for Pulp and Paperboard increases, and the contrary happens in bad times. Second, the balance sheet has strengthened very significantly in recent years as inventories increased while long-term debt declined since 2020, demonstrating that Clearwater Paper is a profitable and highly viable company, and this improvement also put the company in a robust position to face a potential recession. Third, the company should be able to begin a new stage of growth as soon as its long-term debt is significantly reduced from current levels, which should be possible in a relatively short period of time not only due to higher revenues and margins but also due to high inventories. And last (but not least), investors should not forget that the company has successfully operated since 1900, which demonstrates its viability in the long term.

Despite this, those investors with a more conservative risk profile could choose to invest in tranches in order to reduce the average share purchase price in case the share price decreases from current levels since we must not forget that we are currently living in times of high volatility in the markets and there are currently many variables into play.

For further details see:

Clearwater Paper: Operations Are Improving And Debt Should Keep Decreasing