OXLCZ - CLO Equity CEFs: A Round-Up Of The Highest-Yielding CEF Sector

2023-09-26 03:09:35 ET

Summary

- We review the CLO Equity CEF sector, which got a new addition recently with CCIF.

- The sector's valuation has deflated recently, though most funds continue to trade at premiums.

- CLO Equity CEF returns have beaten nearly all other credit CEFs over the longer term; however, they lag the yields of the funds.

- We remain upbeat on CCIF despite a double-digit gain on our strategy over the last 6 weeks.

In this article we review the CLO CEF sector, particularly those funds that allocate in large measure to CLO Equity. This niche subsector recently got a new addition with the Carlyle Credit Income Fund (CCIF) joining the group so we take the opportunity to review the broader space.

CLWha-?

This article is not going to be a CLO primer - there are good sources readily available on the internet. We will only sketch the broad outlines of a CLO for our purpose here.

A CLO is just the combination of a portfolio of loans (i.e. the asset portion of the CLO) and a set of liabilities (i.e. the bits that are called CLO Debt). The CLO Debt securities (also called tranches) have a varying number of protections and collateralization which is why some can be rated AAA and others B/BB despite referencing the same portfolio of loans.

As expected, the higher the tranche in the capital structure the less risk it carries and the lower its yield. The difference between the CLO assets and its liabilities is, unsurprisingly, called CLO Equity and this tranche earns the excess spread that the loan assets deliver over its liabilities.

{kind=link}

CLO Equity has two basic attractions. First, its very high yield across the entire credit market with implied yields often around 15%+. And two, its robust performance across market meltdowns, something that is not immediately intuitive but remains a fact of the asset class.

Wells Fargo

The reasons CLO Equity tends to remain robust over difficult market periods has to do with two key features. First is the fact that CLO portfolios tend to be higher quality than the broader loan market, a function of the various quality tests each CLO needs to pass. And two, CLO Equity have a number of embedded options that include an ability to refinance, reset or redeem the CLO which are very valuable over the market cycle.

Lay Of The Land

Until recently there were four CEFs that focus primarily on CLO securities.

These include the:

Investors who have followed our recent articles are aware that recently a new fund joined this group - the Carlyle Credit Income Fund ( CCIF ).

There are many other funds that hold CLOs, primarily CLO Debt, in their portfolios such as XFLT, ARDC, AIF, KIO and many others. However, here we focus on funds that hold primarily CLO Equity and not much else.

The legacy funds above hold CLO Equity at 70-100% of the portfolio. There is a question mark around CCIF. In its communication the fund mentioned a plan to hold both Equity and Debt however so far it seems to have only acquired Equity. We should know more as the fund puts the rest of its capital to work over the coming weeks.

All the legacy funds use leverage , almost exclusively via fixed-rate debt and preferreds. This combination of floating-rate assets and fixed-rate liabilities is fairly unusual in the CEF space and is the best combination for growing net income in an environment of rising short-term rates. It's not surprising that all the legacy funds have boosted their distributions over the past couple of years.

The leverage of the funds tends to be elevated at around 30-40%. Although a high level of leverage does boost net income of the funds it also increases the risk of a forced deleveraging which the funds have repeatedly gone through. In a forced deleveraging the funds will typically sell assets in down markets only to buy them back in rising markets, creating a headwind for longer-term returns.

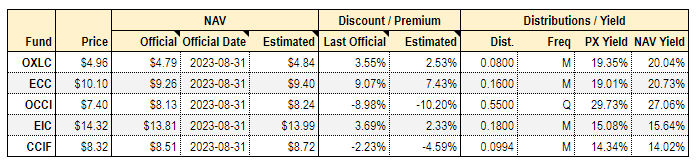

The key metrics of these funds are shown below as an extract from our service CEF Tool.

{kind=link}

Although most of the funds trade at premiums, these valuations are not as high as they have been - with funds like OXLC and ECC typically trading at double-digit premiums over the last couple of years.

The chart below shows that the premium of a fund like ECC has shrunk significantly - in part due to the recent rise in the NAV as well as a drop in price. Although the valuations are elevated in absolute terms (most other credit CEFs trade at high single-digit or double-digit discounts) this is reasonably attractive in relative terms as the valuation gap to the rest of the CEF space has been wider in the past.

Systematic Income CEF Tool

All the CEFs feature double-digit yields with 3 having NAV distribution rates north of 20%. Although there is much debate around whether this is "real" or not, with CLO Equity yields in the neighborhood of 15% this is not an unreasonable payout level.

The sub-sector has fairly high fees for CEFs which are akin to the BDC fee structure having both high management fees (roughly 2x that of credit CEFs) as well as incentive fees. The management fee cannot be directly compared to that of CEFs because it is not charged on total assets, in effect, excluding assets financed with debt for two of the CEFs. To get a rough sense of scale, ECC, for example, reported management fees of around 6% on NAV which comes out roughly 4x that of nearly all other credit CEFs.

Systematic Income

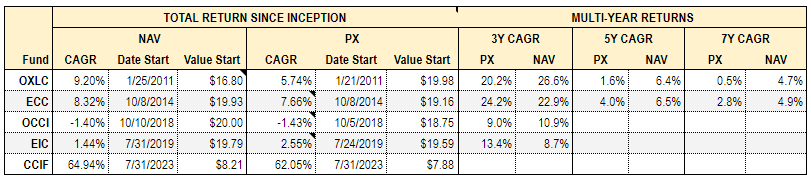

Total returns of the legacy funds are pretty strong as far as credit CEFs go. 5Y total NAV returns of around 6.5% for OXLC and ECC are well above the 3.8% and 2.5% returns for loan and HY bond CEFs respectively over the same period. At the same time, it's clear that these returns are also well below the yields of these funds. This suggests that investors shouldn't expect double-digit returns over the medium term from these funds.

{kind=link}

CLOs and Recessions

It's fair to say that CLOs and CLO Equity, in particular, are highly leveraged plays on credit. This raises the question of whether they are reasonable holdings in an event of a recession - something that is top of mind for many investors.

This view is very intuitive. After all - CLO Equity is a leveraged play on bank loans. And loans, as well as other credit assets, tend to struggle during recessions. The chart below shows that loan defaults tend to spike during recessions as they did during the GFC, the near Energy shock recession and the COVID recession.

S&P

However, this is another example of where a little knowledge is a dangerous thing. The point is that CLO Equity is not just a leveraged play on loans. As we suggested above it is more akin to a dynamic allocation strategy. Specifically, CLO Equity benefits from a number of embedded options such as the reinvestment option and the call option which allow CLO Equity to generate additional returns in a weak market environment.

Specifically, in a period of elevated default rates, CLO Equity benefits from reinvested principal prepayments and amortization payments into loans trading at depressed prices. Since the majority of these loans tend to redeem at par, this accrues directly to the CLO Equity tranches. The chart below shows that CLO Equity delivered stellar results through the GFC specifically because of this dynamic.

Wells Fargo

Total NAV returns over the COVID shock were very strong as well - they are highlighted in the table below from our CEF Tool.

Systematic Income CEF Tool

It's important to understand why results over the GFC and the COVID shock were so strong and why they did not align with the simple intuition that holding leveraged exposure to bank loans in the form of CLO Equity over a recession is dumb.

What's important to understand is that there is a self-correction element to both CLO Equity and CLO Debt. The self-correction elements of CLO Debt securities are baked into the CLO structure in the form of various performance tests, summarized below.

Neuberger Berman

CLO Equity, on the other hand, benefits from a number of options which become highly valuable during periods of high volatility. The chief among these, and the one most relevant in the current market environment, is the reinvestment option which allows CLO managers to reinvest principal and amortization payments on loans in the portfolio into loans trading below par.

A loan acquired at $90 which redeems at par sees the entire $10 go right to the bottom line of CLO Equity. This is why a distressed loan environment can be highly advantageous for CLO Equity since skilled managers can acquire loans at a steep discount and enjoy the full accretion back up to par. Granted, some loans will suffer defaults and the loan prepayment rate typically slows in a difficult market environment but the history is very clear - CLO Equity has performed exceptionally well during periods of distress because of this important feature. Neglecting the power of the reinvestment option also causes many investors to wrongly conclude that it is "obvious" that holding CLO Equity in a tough market environment is a dumb thing to do.

Other options enjoyed by CLO Equity include the refi option, also called the "call" option as well as the reset option. The refi option allows managers to refinance the transaction after the non-call period, allowing them to lower the cost of leverage and restructure the CLO with debt at lower levels. This is particularly powerful in an environment of strong risk appetite such as the one we saw in 2021. A reset allows managers to extend the term of the CLO deal. These options combine to deliver a much stronger performance potential for CLO Equity than the usual view that some investors have that they are just dumb leveraged portfolios of loans.

Risks To Consider

As we suggest above, many of the misconceptions about the CLO Equity asset class come from the bearish side. At the same time, this doesn't mean the asset class is without risk. It's just that the things that tend to be highlighted are not the kind of risks that investors should focus on.

One key risk for investors in CLO Equity CEFs is the risk of deleveraging. All three CLO Equity CEFs (OXLC, ECC and OCCI) leverage themselves exclusively with senior securities, i.e. preferreds and senior unsecured debt. There are regulatory rules which prevent the funds from making distributions on common shares if the asset coverage of these leverage instruments falls below a certain level. And because these funds don't like suspending distributions on common shares, they will tend to deleverage during periods of stress. This creates a drag on the performance of these funds.

The second key risk is that CLO Equity net interest margin remains at currently low levels. Lower excess spreads for Equity may result in lower returns going forward, all else equal.

The third risk is that prepayments fall significantly. A lower prepayment rate will make the reinvestment option less valuable for CLO Equity tranches. So far the prepayment rate is holding up well but it could fall in the future.

Fourth, defaults may increase but loan prices could hold up, meaning CLO Equity is hurt by rising defaults but cannot benefit as much from the reinvestment option. This seems very unlikely as credit markets usually price in a hefty premium for losses. In other words, loan prices tend to be significantly below actual realized losses over the cycle and this dynamic benefits CLO Equity.

Fifth, rating agencies expect loan recoveries to be lower in the next default cycle relative to historic averages. This is the result of an increase in cov-lite issuance, various structural features such as sidecars as well as an increase in no bond loan issuers, EBITDA addbacks and others.

Finally, it seems possible that the CLO 2.0 structure which is prevalent now in the market may be less advantageous for CLO Equity investors. As the following table shows CLO 2.0 has generated a lower level of returns than CLO 1.0 which was more prevalent prior to and through the GFC. Clearly, the two market periods were not identical but there could be something there.

Citi

Takeaways

CLO Equity CEFs remain popular options across the broader income space owing to their high yields and relatively strong performance. These funds are most attractive when underlying loan prices are depressed and discounts are wide. Since neither is true at the moment, we would avoid overweighting this sector at the moment.

That said, we remain upbeat on CCIF, even after a double-digit gain on the strategy we discussed across two recent articles. The fund's discount lags that of most other funds in the sector and we think there is more potential to the fund's distribution despite the recent 75% hike. CCIF trades at a 2% discount and a 14.3% distribution rate.

For further details see:

CLO Equity CEFs: A Round-Up Of The Highest-Yielding CEF Sector