CLX - Clorox: We See Limited Gains

2023-03-20 12:43:58 ET

Summary

- Clorox is a consumer goods business with a significant presence in cleaning products. Shares rose impressively during COVID-19 and have subsequently declined.

- Further economic decline will likely result in a flatlining of performance.

- The business looks to be stagnant with a bloated cost base. Our view is that margins should improve but growth may continue to be slow short-term.

- Management has funded dividends through debt, with their current pay-out ratio in excess of 100%. Our view is that cuts are ahead.

- Our view is that Clorox is overvalued relative to comparable businesses which are outperforming them.

The Clorox Company

The Clorox Company ( CLX ) is a global manufacturer and marketer of consumer and professional products, divided into four segments:

- Health and Wellness - Offers cleaning, home care, and disinfecting products.

- Household - Offers cat litter products, bags and wraps, professional food service, vitamins, and supplement products.

- Lifestyle - Offers dressings, dips, seasonings, and sauces, as well as natural personal care products.

- International - Offers products from all segments globally.

Similar to many of Clorox's peers, the business offers a range of consumer goods products across a range of segments. The business is famous for its cleaning products but owns some household staples, including Brita , Fresh Step, and Glad.

Share price

CLX's share price has performed extremely well over the last decade, gaining significantly in 2020, as a result of the COVID-19 pandemic. Many cleaning / sanitation businesses benefited from greater institutional and consumer spending in the area. Since then, the stock price has gradually regressed as markets reprice the asset for a post-COVID world.

This paper intends to consider if CLX has once again reached an attractive valuation. To assess this, we will consider current economic conditions and how they could impact the business, the current positioning of the business, as well as financial and qualitative analysis of the business.

Clorox's financial performance

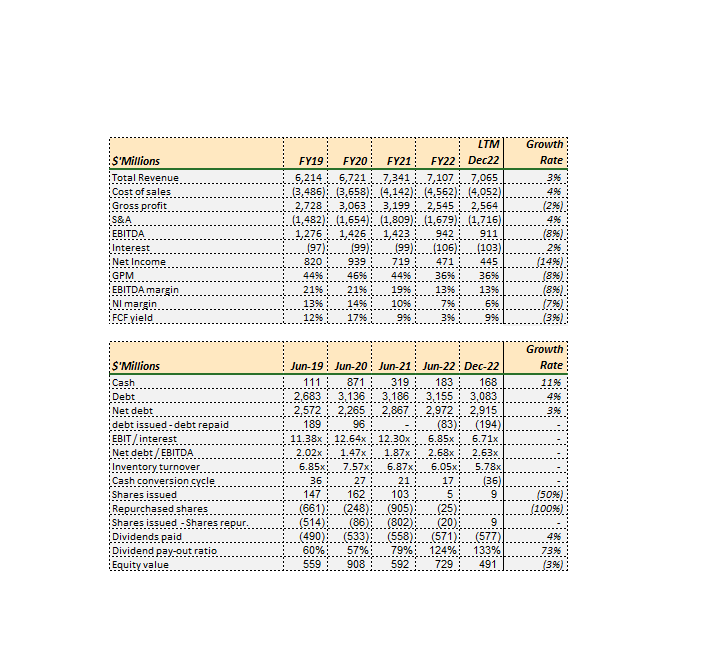

{kind=link}

CLX Finances (TIkr Terminal)

P&L

Over the past decade, CLX's top-line performance has been unremarkable, with a growth rate of only 3%. Given that the industry is mature, significant growth was not expected, but the target should always be a healthy buffer to the sustainable inflation rate of 3%.

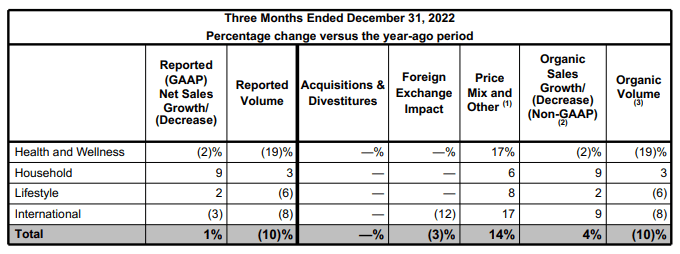

In the latest Q4-22 investor presentation, a concerning trend emerged. The business appears to have strong pricing power with a 14% increase, but it came at the cost of a 10% decline in volume. We would expect the business to be far more inelastic. Management has stated in their Q4 remarks that they plan to raise prices further, which could result in more of the same - marginal growth at the expense of volume.

{kind=link}

3MDec22 Revenue Bridge (Q4 Press release)

Given the limited revenue growth, the business must ensure efficiency to grow profitability on the bottom line. However, the opposite seems to be true, as GP, EBITDA, and NI have all declined. The only silver lining is that the unlevered FCF yield has remained relatively stable.

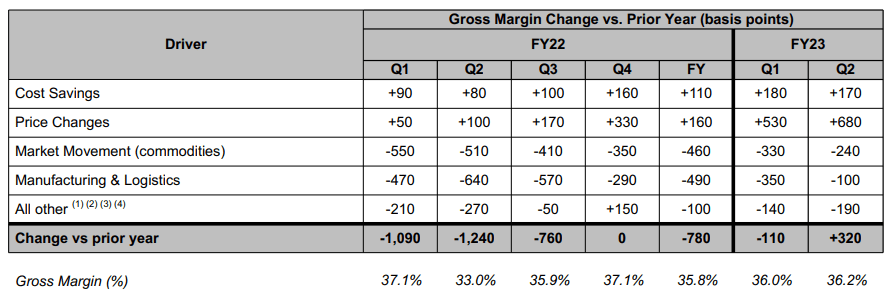

The main culprit behind this performance is poor operational control, with S&A expenses remaining constant at approximately 24% of revenue in recent years. Management has acknowledged this issue and has started a "hallmark cost savings program" to address it (Q4 Remarks). Although some progress has been made, it is not significant enough. Our target for the business is an EBITDA margin closer to 22%, which the business has been closer to in the past (average of 20% historically) but is far from its current position.

{kind=link}

Margin drivers (Q4 Press release)

However, there is a reason for optimism as the supply-side issues, such as increased transportation and production costs, are still ongoing but subsiding. With the weakening of economic conditions and the improvement of the COVID situation in China, these costs may start to decline.

Balance sheet

The inventory turnover rate of CLX has slightly decreased, going from 6.9x to 5.8x, indicating a potential slowing of demand or overstocking of inventory. Management plans to decrease inventory by 10% compared to the previous year, which may result in discounts and shrink margins, especially if demand continues to slow.

CLX's financial structure raises concerns. The company's debt has increased at a CAGR of 4% and the net debt to EBITDA ratio has risen to 2.63x, which is not necessarily a credit risk, but the use of the funds is questionable. CLX has increased its dividend payments faster than its revenue, using capital to directly fund the pay-outs on Dec21 and LTM Nov22. This has resulted in a pay-out ratio exceeding 100%, which means Management are essentially borrowing money to pay shareholders. This decision is unusual and suggests that dividend cuts in 2023 are probable.

Economic conditions

Consumer demand began to decline in 2022 due to several factors. Firstly, the lingering effects of lockdowns and subsequent overspending have played a role in demand brought forward at the time. However, the primary driver has been the surge in the inflation that occurred in the same year. This inflationary trend can be attributed to a decade of loose monetary policy, energy price disruptions due to the War in Ukraine, and supply chain challenges caused by lockdowns. Businesses are facing squeezed margins as their production costs rise their employees demand greater wages. Meanwhile, consumers are grappling with declining discretionary income as their cost-of-living increases.

In response to this trend, central banks have raised interest rates to curb demand. However, this approach has been challenging as the balance between supply and demand is heavily skewed towards the former due to energy prices and production ramp-up being the driving force. These factors are less responsive to interest rate changes.

Our outlook on economic conditions is much of the same, central banks will continue to use interest rates to bring inflation under control. US inflation expectations remain elevated, which supports our thesis that rates must rise.

Our view is that interest rates will peak in the US around 4.75% in Q2'23 / Q3'23, before beginning a decline rapidly in early 2024. Having already experienced an extended period with heightened rates and inflation, this will likely trigger a recession. The yield curve has inverted , supporting this.

Consumer goods businesses like CLX, have a unique advantage in a declining demand environment. These businesses offer products that are essential or bring low-cost enjoyment to people's lives, such as pet food, soda, and cleaning products. While consumers may have reduced disposable income, they are unlikely to cut back on these necessities. Less income does not stop someone from feeding their cat (hopefully). This allows consumer goods companies to maintain profitability by adjusting prices somewhat to compensate for additional costs, without sacrificing total revenue. Our view would be that growth in revenue, a slight decline in GPM, and flat profits would be a good performance.

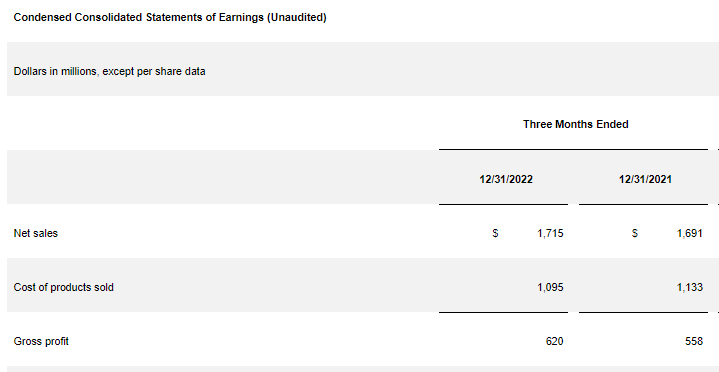

Looking at CLX's recent performance, it is impressive to see both sales (1.4%) and gross profit margins (3.1pp) have grown. This is evidence of its relative resilience, giving the business pricing power to beyond inflationary pressures. As we have seen, this does come at the cost of volume. Furthermore, the company's earnings before taxes margins have risen from 5% to 7.5%, which is a significant increase for a mature business.

{kind=link}

CLX 3MDec22 FS (CLX Quarterly press release (Q3))

This said, with only marginal revenue growth, it is very unlikely that 2023 will be a standout year as things are more likely to worsen than improve. The onus will thus be on Management to find efficiencies.

Relative performance

Comp set financial comparison (Tikr Terminal)

Consumer goods businesses operate in many different sectors and so qualitative analysis can be difficult, but they are generally similar on bottom-line financials.

What we see is a noticeable underperformance in EBITDA margin. The next closest business is Kimberly-Clark ( KMB ), which is 4% higher than CLX. Even if we were to take CLX's 10-year average, it would still be below the peer average.

When looking at unlevered FCF yield, the difference is far smaller with the average distorted by Reckitt Benckiser's (RBGPF) outstanding return. Most of these businesses maintain a pay-out ratio between 65-85%, which is a more stable use of generated cash.

CLX is also more leveraged than its peers, making its capital allocation less favorable. This is further proof that the business is underperforming in comparison to its competitors.

Investors can look at the business in two ways: they can either value the business based on its current metrics, with a large discount to its competitors, or they can assign a smaller discount, assuming margins will quickly recover, given its history of consistent EBITDA margins around 20%.

Valuation

Comp set valuation (Seeking Alpha / TIkr Terminal)

CLX's current valuation at 21x NTM EBITDA is 3x higher than its 5-year average and is above the valuations of its peers, despite the recent decline in its EBITDA performance. Our view is that the stock's share price has not reflected this drop in earnings.

Further, Management's desire to pay dividends through debt is only to achieve a yield of 4%, which is marginally above the average and so does not offer a compelling risk-reward for investors.

Our view is that it is unlikely for CLX to sustain its current high valuation for a prolonged period, given its underperformance compared to peers. The question is whether earnings will improve or if the price will drop. Given the unfavorable economic conditions, a price decrease is more likely.

For investors considering an alternative, UL looks far more attractive at its current valuation.

DCF

As a secondary analysis, we have conducted a DCF valuation for CLX. Our key assumptions are:

- FCF yield of 8-11%, picking up into the later periods, in line with prior levels achieved.

- Revenue growth picking up from <1% in FY23 to 4% in the later periods, normalizing at 2.25%.

- WACC of 9%.

Based on this, CLX is overvalued by 9%. The consensus price target from analysts is in a similar ballpark, believing the business is overvalued by 6%.

Key risks to analysis

The company's worsening profitability profile and near-term revenue decline are the primary reason we view the company as unattractive. If Management's cost initiatives are successful in the coming 12-24 months, we could see margins improve to their pre-pandemic levels. When comparing an EBITDA/FCF margin of c.21%/17% to CLX's peers, suddenly the company is far more attractive. This will be evidenced by a declining S&A expense as a percentage of revenue, which will need to decline by 1-2%. Although this remains a risk to the bearish view, we have yet to see sufficient evidence of this.

Final thoughts

CLX is a consumer staple, but we struggle to see those characteristics. Demand looks to be quite responsive to a price change, which makes us concerned with where demand could go if economic conditions weaken further.

Further, profitability has been unusually volatile for a business of this nature, declining in recent periods. Our view is that it should pick up with Management's cost initiative, but the degree is difficult to quantify.

We do not like how Management allocates the company's capital, with dividend cuts expected.

Finally, we are of the view that the business is overvalued, with better-performing businesses trading at a discount to CLX.

For further details see:

Clorox: We See Limited Gains