CMSD - CMS Energy: It Might Be Worth Picking Up Shares Of This Utility Today

2023-08-22 10:00:11 ET

Summary

- CMS Energy Corporation is one of the largest regulated electric and natural gas utilities in Michigan, serving almost the entire state.

- The company's stock price is currently trading at a more attractive valuation than earlier this year, making it potentially appealing to value-oriented investors.

- CMS Energy's stable cash flow, long history of dividend increases, and growth prospects through rate base expansion make it a reasonable investment option.

- The company should have no difficulty sustaining its distribution yield going forward.

- The company is well-positioned to deliver a 9% to 11% total average annual return through 2027.

CMS Energy Corporation ( CMS ) is one of the largest regulated electric and natural gas utilities in the highly populated state of Michigan. The company serves almost all of the state except for the Upper Peninsula and the city of Detroit:

{kind=link}

Utility companies like CMS Energy have long been popular investments for retirees and other conservative investors due to their stability and relatively high yields. CMS Energy, unfortunately, only yields 3.47% at the current price so it does not offer a particularly attractive yield in today’s environment. After all, a money market fund is paying around 5% right now and does not come with the risks involved in purchasing common equity. The company does have a long history of raising its dividend on an annual basis, so anyone that is willing to hold the position for a little while will eventually end up receiving a higher yield on cash than the money market fund would deliver. In addition, the company’s most recent results did show the overall stability that we normally associate with the sector as its revenues were down year-over-year, but cash flow was up. As is the case with many other utilities, CMS Energy’s stock price is down year-to-date, but that has also made its valuation and dividend yield more attractive than earlier this year. In fact, CMS Energy is currently trading at a much more attractive valuation than it was when we last discussed this company in June, which might cause a value-oriented investor to be interested in it. This is especially true when we consider that this company is unlikely to be affected very much by a recession, and multiple signs are pointing to the likelihood of such an event either later this year or early in 2024.

This is, admittedly, a very similar thesis to what was presented the last time that we discussed this company, however, the company has since released its second-quarter earnings report , which reinforces our thesis about the overall stability of the company's finances regardless of economic conditions. This article is intended primarily to provide an updated analysis of the company using these new figures, as well as new evidence regarding current economic conditions that could strengthen the need to have a financially stable company in your portfolio.

About CMS Energy Corporation

As stated in the introduction, CMS Energy Corporation is a regulated electric and natural gas utility that serves most of the state of Michigan. In fact, it serves nearly the entire state except for the Upper Peninsula and the city of Detroit. This is shown quite clearly in the map of the company’s operations above. This is a fairly populated service territory, after all, Michigan is the tenth most populated state in the United States. CMS Energy serves a total of 6.7 million people, but naturally, its customer count is not that high. This is because that figure includes children and other people that do not live alone. In total, the company has 1.9 million electric and 1.8 million natural gas customers.

There may be some readers that are somewhat concerned with the fact that the company’s electric and natural gas businesses are quite similar in size. After all, politicians, media personalities, activists, and others have been promoting the concept of electrification for quite some time. At its core, electrification refers to the conversion of things that are historically powered by fossil fuels to the use of natural gas instead. Two of the things that are envisioned for conversion are space heating and cooking, which are the two primary uses for utility-supplied natural gas. As such, the widespread adoption of electricity for these purposes could eventually render the company’s natural gas utility business obsolete. However, that is highly unlikely to happen at the speed that promoters of electrification claim. As I pointed out in a previous article , American consumers are actually willing to pay tens of thousands of dollars more for a natural gas house than an all-electric one right now. This is mostly due to the fact that natural gas is far more efficient at heating a structure than electricity, which means that it is cheaper to operate. The U.S. Energy Information Administration points this out, stating that it costs almost four times as much to heat a home with electricity as with natural gas:

New Jersey Resources/Data from US EIA

As such, it seems highly unlikely that anyone will willingly convert to electric heat if they already have a natural gas heating system. That is particularly true for people of lesser financial means or who are already struggling with bills. When we consider that about 64% of Americans are living paycheck-to-paycheck , it seems unlikely that they will be willing to have their energy bills increase to the degree that an all-electric system would impose. While it is possible that things will change at some point in the future, it seems unlikely that CMS Energy’s natural gas business will be going anywhere in the near future. Rather, it will simply generate the revenue, cash flow, and profits that it always has.

Unfortunately, one disadvantage of the company’s substantial natural gas business is that its revenues are seasonal. We can see that here:

{kind=link}

(all figures in millions of U.S. dollars)

As we can clearly see, the company tends to have higher revenue during the first and fourth quarters of any given year than it does during the second and third quarters. This is because the first and fourth quarters contain most of the days in which the temperature is cold enough to require the use of space heating. As such, natural gas consumption tends to be much higher during those quarters than at other times during the year. The fact that the company’s natural gas bills correlate with consumption means that the natural gas utility will receive most of its revenue during the winter. This extends to the company as a whole. While it is true that electric consumption tends to be higher in the summer than in the winter due to the use of air conditioners, the seasonal differences in electric bills are not nearly as much as natural gas bills. This results in lumpy quarter-to-quarter revenues.

The fact that CMS Energy’s revenues vary from quarter to quarter does not change our thesis about this company’s finances being remarkably stable over time. As proof, let us have a look at its twelve-month operating cash flows. Here are the company’s figures for each of the past eleven twelve-month periods:

{kind=link}

(all figures in millions of U.S. dollars)

While we do see some occasional variations here, for the most part, the company’s operating cash flows are pretty stable when we look at any given twelve-month period. The reason that we are using twelve-month periods is naturally to eliminate the seasonal variations, as just discussed.

The reason for the company’s general stability over time is that CMS Energy provides a product that is generally considered to be a necessity for our modern way of life. After all, there are very few people in the United States that do not have electric service in their homes and businesses. In fact, most of us take it for granted that the lights will come on when we flip a light switch. The same necessity status applies to natural gas for anyone that is living in a home that is heated by natural gas. We expect that our furnace will come on when we want it to and largely take it for granted that the furnace will have sufficient fuel to do so. As such, most people will prioritize paying their utility bills ahead of discretionary expenses during times when money gets tight. This is the situation for a lot of households right now, as high inflation has forced many people into desperate measures to survive. The fact that CMS Energy’s cash flows are largely stable over time regardless of conditions in the broader economy should thus endear it to any investor that is seeking a safe haven to ride out the challenging economic conditions that will likely arrive in the near future.

Growth Prospects

Naturally, as investors we are interested in more than simple stability. We like to see a company in which we are invested grow and prosper with the passage of time. Fortunately, CMS Energy is well-positioned to accomplish that. There are two primary ways for a company like this to grow its revenue and earnings. The first is by adding new customers and the second is by growing its rate base.

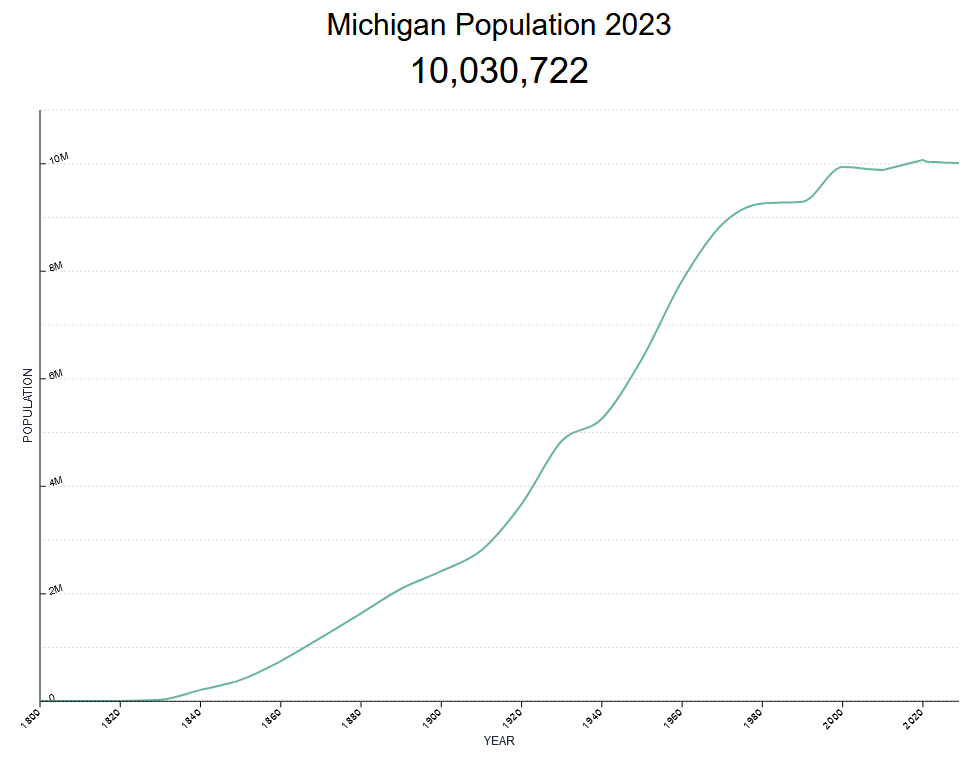

Unfortunately, CMS Energy will probably have some difficulty growing its revenue by adding new customers. As we have already seen, the company’s service territory is limited to the state of Michigan. This state’s population is stagnant, at best:

{kind=link}

The U.S. Census Bureau states that the state’s population is declining at a 0.03% rate and will likely continue to do so for the near future. That has a certain amount of support from other sources that state that people are moving away from the Northern states upon retirement in favor of the Southern states. The fact that many people have been able to convert to remote work ever since the pandemic lockdowns has somewhat exacerbated this trend, as people are now free to live where they want as opposed to where they have to live due to work. CMS Energy’s natural gas utility might be able to get a few new customers that choose to convert from other heat sources and the company might get a few new customers if people opt to move away from Detroit but stay in Michigan, but for the most part, the demographics are not favorable here. The company itself makes no mention of customer growth as a driver of forward earnings growth, so it seems likely that CMS Energy agrees with this assessment.

That leaves rate base growth as CMS Energy’s primary driver of revenue and earnings growth. The company is quite well-positioned to deliver this going forward. As I pointed out in my previous article on the company,

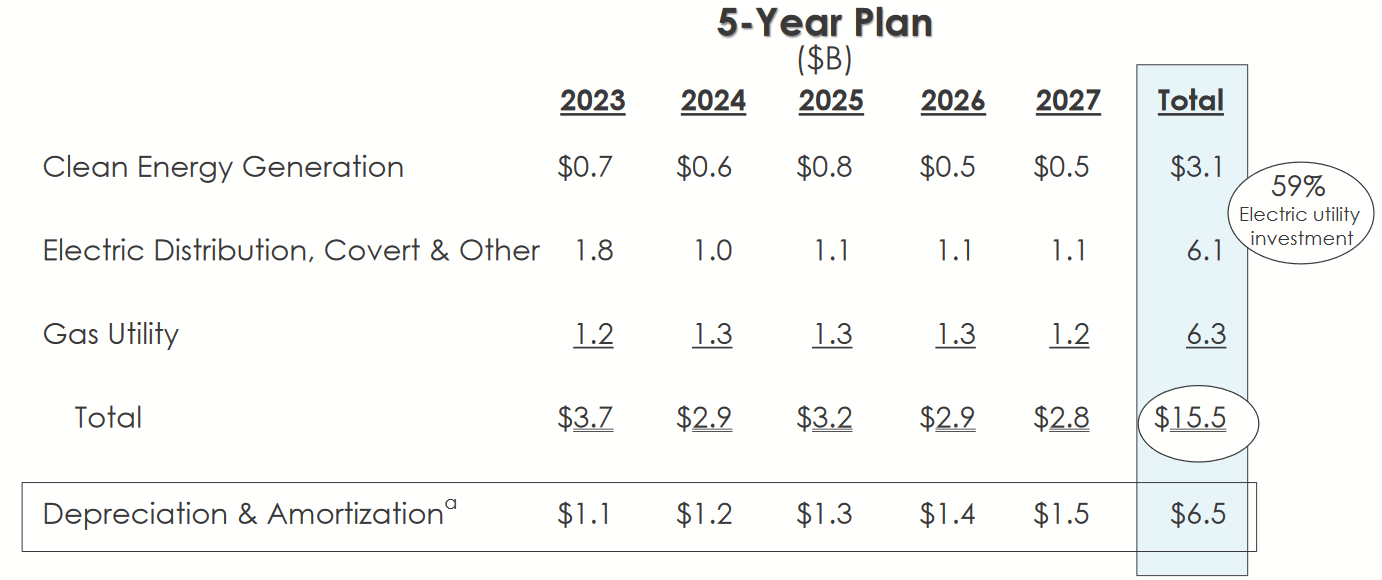

The company’s rate base is the value of its assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the amount that it charges its customers in order to earn that allowed rate of return. The usual way through which a utility grows its rate base is by investing money into upgrading, modernizing, or possibly expanding its utility-grade infrastructure. CMS Energy is planning to do exactly that, as the company has presented a plan to spend a total of $15.5 billion over the 2023 to 2027 period on improving its infrastructure.

The previous article also included this chart that shows exactly how this spending will be distributed across the company's various businesses:

{kind=link}

The company’s rate base growth will unfortunately be much less than this $15.5 billion in total capital expenditure. One of the reasons for this is depreciation, as shown above. Depreciation is constantly reducing the value of the assets that the company has in service. In fact, if CMS Energy were to spend nothing on its infrastructure, its rate base would actually decline. Thus, it needs to spend at least enough to cover the depreciation, as well as extra to grow the rate base. In addition, the company is planning to shut down its last remaining coal plant in 2025. When it does this, the full remaining value of the plant will be deducted from the company’s rate base. That will naturally offset some capital spending during that year.

CMS Energy has stated that this capital spending program should be sufficient to grow its earnings per share at a 6% to 8% rate over the five-year period. When we combine this with the current 3.47% dividend yield, the company should be able to deliver a total average annual return of 10% to 12% over the period. That is quite reasonable for a conservative utility company, although it is only in line with the figure that we saw the last time that we discussed this company. That is because the stock is down since then, but it is not down sufficiently to affect the total return.

Financial Considerations

From my previous article on CMS Energy:

It is always important that we investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is normally accomplished by issuing new debt and using the proceeds to repay the existing debt since very few companies have the ability to completely pay off their debt with cash as it matures. Unfortunately, this can result in a company’s interest expenses going up following the rollover in certain market conditions.

As of the time of writing, the effective federal funds rate is higher than any level seen since 2007, and the target federal funds rate is higher than has been seen since 2001. As such, it seems almost certain that any debt rollover today will result in a company’s interest expenses going up. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. Thus, any event that causes a company’s cash flows to decline could push it into financial distress if it has too much debt. While companies like CMS Energy tend to enjoy remarkably stable cash flows over time, there have been bankruptcies in the sector before so we should not ignore this risk.

Also from the last article on this company:

One metric that we can use to analyze a company’s financial structure is the net debt-to-equity ratio. This ratio basically tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company’s equity will cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of June 30, 2023, CMS Energy has a net debt of $14.733 billion compared to $7.706 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.91 today. Here is how that compares to some of the company’s peers:

| Company |

| Net Debt-to-Equity Ratio |

| CMS Energy Corporation |

| 1.91 |

| DTE Energy ( DTE ) |

| 1.89 |

| Avista Corporation ( AVA ) |

| 1.21 |

| Eversource Energy ( ES ) |

| 1.58 |

| Entergy Corporation ( ETR ) |

| 1.92 |

Unfortunately, we can see here that CMS Energy appears somewhat heavily leveraged relative to its peers. This has been the case ever since we started discussing this company, and I could list a few more comparable companies that have much lower debt ratios than the ones shown above. CMS Energy’s debt situation appears to be getting worse too, since its current ratio is quite a bit higher than it was the last time that we discussed this company back in June. It is trending in the wrong direction, especially considering that interest rates are going up. As such, this is something that we will want to keep an eye on going forward and a risk that we want to consider before making an investment in the company.

Dividend Analysis

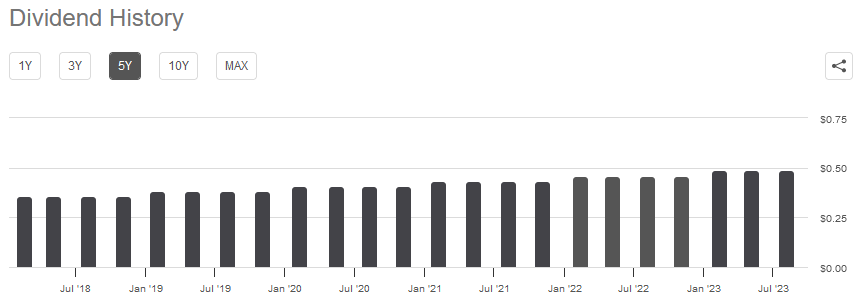

One reason why many investors purchase utilities like CMS Energy is because of the fairly high dividend yields that these companies tend to possess. That is caused by the fact that these companies have fairly slow growth, so they pay out a substantial percentage of their cash flows to the shareholders in order to provide an acceptable rate of return. The market tends to not assign high multiples to these companies due to their low growth rates, so the dividend ends up being a significant percentage of the stock price. CMS Energy’s yield is only 3.47%, so it is not as high as some of its peers, but it still beats the 1.49% current yield of the S&P 500 Index ( SPY ). As mentioned earlier in this article, CMS Energy also has a long history of raising its dividend on an annual basis:

{kind=link}

As is always the case, we want to ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and almost certainly cause the company’s stock price to decline.

The usual way that we judge a company’s ability to afford its dividend is by looking at its free cash flow. Free cash flow is the amount of cash that was generated by a company’s ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the money that is available to benefit the stockholders via debt reduction, share buybacks, or dividends. During the twelve-month period that ended on June 30, 2023, CMS Energy had a negative levered free cash flow of $1.6330 billion. That is clearly not enough to pay any dividends, yet the company still paid out $564.0 million to its shareholders over the period. At first glance, this is likely to be concerning as CMS Energy did not have sufficient free cash flow to cover its dividends.

However, it is not unusual for a utility to finance its capital expenditures through the issuance of debt and equity. It will then pay its free cash flow out of operating cash flow. This is done because of the incredibly high costs of constructing and maintaining a utility-grade infrastructure network over a wide geographic area. Basically, these costs are such that the company could never provide any sort of return to its shareholders if it had to finance everything internally. During the trailing twelve-month period, CMS Energy reported an operating cash flow of $1.5010 billion. That was more than enough to cover the $564.0 million that was paid out in dividends with a substantial amount of money left over for other purposes. Overall, this dividend appears to be sustainable, and we have little reason to be concerned.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like CMS Energy, we can value it by looking at the price-to-earnings growth ratio. I explained how we use this ratio the last time that we discussed this company:

This is a modified version of the familiar price-to-earnings ratio that takes a company’s earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that a stock may be undervalued relative to the company’s forward earnings per share growth and vice versa. However, there are very few stocks that have such an attractive valuation in today’s richly valued market . As such, the best way to use this ratio today is to compare CMS Energy to its peers in order to determine which company has the most attractive relative valuation.

According to Zacks Investment Research , CMS Energy will grow its earnings per share at a 7.80% rate over the next three to five years. That is in line with the earnings per share growth that the company should be able to deliver from its rate base expansion, so it seems pretty reasonable. At this growth rate, the company’s stock has a price-to-earnings growth ratio of 2.35 at the current price. That is quite a bit better than it was the last time that we discussed this company. However, let us see how CMS Energy compares to its peers:

| Company |

| PEG Ratio |

| CMS Energy Corporation |

| 2.35 |

| DTE Energy |

| 2.85 |

| Avista Corporation |

| 2.29 |

| Eversource Energy |

| 2.60 |

| Entergy Corporation |

| 2.52 |

Here, we can see that CMS Energy looks quite promising as an investment opportunity. The company’s stock appears to be trading at a very reasonable valuation compared to its peers. This might be due to the company’s weaker balance sheet, but it also might be due to the market disliking its natural gas exposure. Regardless of the reason, the company does appear to be a very reasonable purchase today.

Conclusion

In conclusion, CMS Energy appears well positioned to weather through the uncertain environment that seems to be worrying the markets more with every passing day. The company boasts remarkably stable cash flow from year to year, as well as a respectable growth rate that should be pleasing enough for most conservative investors. The company also boasts a sustainable dividend and a yield that is well above the market. When we combine this with a respectable valuation, it might be worth picking up shares today.

For further details see:

CMS Energy: It Might Be Worth Picking Up Shares Of This Utility Today