CMU - CMU: Our Game Plan For This Muni CEF Tender Offer

2023-10-25 12:27:30 ET

Summary

- MFS Municipal CEFs, High Yield Municipal Trust and Investment Grade Municipal Trust, are undergoing tender offers.

- Shareholders have the option to participate in the tender offers or reduce their allocation due to strong relative performance.

- The breakeven discount widening for the tender offer is 2.2%, meaning investors will make money if the discount does not widen more than 2.2% from current levels.

In this article we take a look at the pair of MFS Municipal CEFs - High Yield Municipal Trust ( CMU ) and Investment Grade Municipal Trust ( CXH ) that are undergoing tender offers. Shareholders should have already received the notifications from their brokers. We currently hold CMU in our High Income Portfolio and is the fund we'll be mostly focusing on in this article.

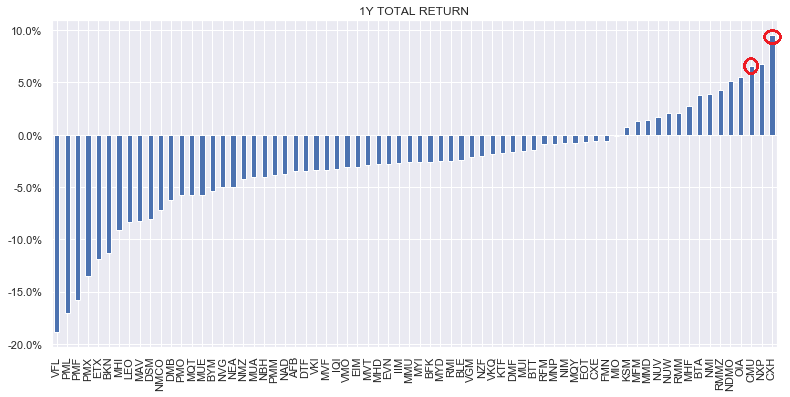

The two funds have outperformed the sector sharply over the past year as the chart below shows, primarily due to discount outperformance. An important question facing investors is whether it makes sense to maintain the allocation and fully participate in the tender offers or to pare down the allocation in light of such strong relative performance.

{kind=link}

The tender offers for the two funds are to repurchase up to 10% of the outstanding shares at 98% of the NAV through November 6.

Price action has been fairly volatile over the past couple of weeks - in part due to rapid interest rate shifts. When some brokers notified shareholders last week, CMU dropped 5% in overnight action. This is an odd reaction to a tender offer as the typical price reaction is usually positive. This is because investors have the opportunity to sell shares back to the issuer at a significantly tighter discount than at the time of the announcement.

The initial tender offer plan was filed in late August - something we could see in the CEF Tool. This was a quid pro quo to satisfy Saba which holds 12% of the fund and who proposed to nominate two people for election and ask for a vote on a liquidity event.

In exchange for not putting up its own directors, CMU agreed to hold this tender offer and let shareholders vote on another liquidity event in 2025 unless the average discount from the current tender offer through 2025 is less than 7.5%.

An important question is what to do with the shares. Tender offer announcements tend to see a bit of a discount rally through the end of the tender offer followed by discount underperformance as tactical investors get rid of shares that were not accepted in the offer that they don't want to hold for fundamental reasons.

Assuming the discount remains fairly wide through the end of the tender offer period as it is at present, investors who don't like a lot of portfolio turnover and like CMU should tender all their shares and then simply buy back the number of their shares that were accepted.

For more tactical investors the calculation is a bit harder and involves balancing the upside (the gain on the tender offer from accepted shares) and the downside (the likely widening of the discount post tender).

The key figures in this calculation are laid out below (from the TO worksheet in our CEF Tool). We populate the known figures - the 98% of NAV buyback price and the 10% of shares to be accepted. We also assume that 50% of the shares are tendered (fairly typical of CEF tender offers). The net result is that the breakeven discount widening is 2.2%.

What this means is that the entire roundtrip tender offer makes money for investors in discount terms (i.e. given we don't know what the NAV is going to do over this period) if the CMU discount does not widen more than 2.2% from current levels. If shares widen more than 2.2% from current levels then the loss on the discount widening will offset the gain on the 10% of shares tendered at a 2% discount.

Systematic Income CEF Tool

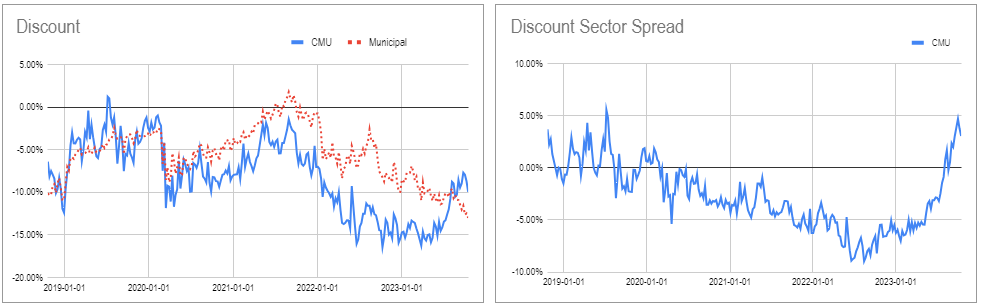

Now it's important to know how likely we are to see a 2.2% widening from current levels? At the current discount of 10% this means a discount move to 12.2% which would still be 3.1% tighter than the sector median level.

Given CMU has tended to trade at a wider discount than the sector average for the last 3.5 years it would not be at all surprising to see its discount move back to its "usual" level.

{kind=link}

In other words, if the CMU discount reverts back to its "typical" behavior, investors will have been better off selling CMU now than participating in the tender offer and holding the remaining shares.

What could hold the discount in is the possible 2025 liquidity event but it's unlikely to be a strong anchor. In short, if we see a single-digit discount through the rest of the week and especially some tightening from here, there is a strong case to rotate the CMU position to another Muni CEF.

Given the risk/reward we decided to pare down our position in CMU. That said, we haven't exited entirely as we could see further discount outperformance through the tender offer period which would allow an even better exit point.

For further details see:

CMU: Our Game Plan For This Muni CEF Tender Offer