UNLYF - Colgate-Palmolive: Stagnation And Debt-Fueled Dividends

2023-06-01 12:25:11 ET

Summary

- CL's business has suffered from supply chain issues, with margins contracting across the board, but evidence suggests this is slowing.

- Our view is that the Filorga transaction several years ago is likely a failure, with much of its value now written off. This should normalize future EPS.

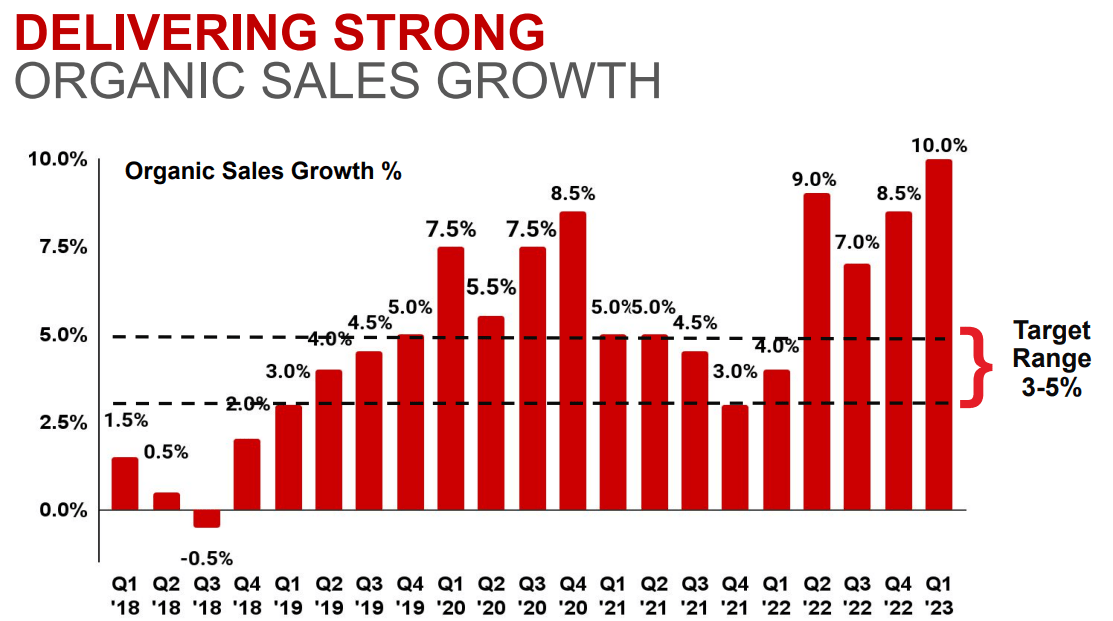

- Q1 performance is attractive, with 10% organic growth.

- Although their relative performance against peers is good, the business is operating in an unsustainable way with its capital allocation.

- Our biggest issue is that the business looks to be funding dividends / BB through further debt and reducing cash to record-low levels. Pay-out ratio sits at 107%.

Company description

Colgate-Palmolive (CL) manufactures and sells consumer products worldwide. The company operates through two segments Oral, Personal, and Home Care; and Pet Nutrition.

- The Oral, Personal, and Home Care segment offers toothpaste, toothbrushes, mouthwash, and other home/consumer goods. Brands within this segment include Colgate, and Darlie, among others.

- The Pet Nutrition segment offers pet nutrition products Under the Hill's Science Diet brand; and a range of therapeutic products under the Hill's Prescription Diet brand.

CL's share price has been relatively flat over the last decade or so, trading between $64 and $80 for the majority of the period. This reflects an uneventful period and stagnating revenue. The purpose of this paper is to assess whether CL is in a position to turn this around and generate healthy growth going forward. As a mature business, investors are unlikely to see a significant upswing but a change in fortunes could yield consistent dividends and growth in line with the market.

We will consider the current market conditions, the financial performance of the business currently, a view on the outlook, and conclude with an assessment of the company's current valuation.

Economic considerations

Demand within many industries spiked during the lockdown period of 2020-2021 as consumers were provided income support and looked to entertain themselves.

This began to subside in 2022 as inflation began to bite. A decade of record low interest rates, excessive money printing in '20/'21, the Russian invasion of Ukraine and supply chain issues were all contributing factors. This has continued to squeeze consumers' finances into 2023.

In response to this, central banks have raised interest rates to cool demand, as a means of bringing inflation down. Inflation is now declining but slowly.

We believe that growth will continue to trend downwards in 2023, as inflation remains persistent. Both inflation and interest rates will be whittling away at discretionary income, potentially triggering a recession.

In most cases, this is bearish for a business, but this is not necessarily for consumer goods businesses. During a recession, people do not stop brushing their teeth or stop feeding their pets. If we use the 2008 financial crisis as an example, CL did not suffer a single year of negative revenue growth but did see profits grow.

The risk this time around comes from the desire to substitute. The difference between now and other recessions / downturns is that things look to be reversed. What usually happens is that lots of people lose their jobs and businesses struggle, but a decent chunk of the population is mostly fine. Whereas now, unemployment remains low ( 3.4% ), but the vast majority of the population is suffering from high-interest rates / inflation to varying degrees. This could mean consumers begin looking for cheaper options, as they seek to save money where they can. Which could potentially lead to greater competition. Management has identified recent months as a "difficult consumer environment" in their Q3 investor pack, with Europe being particularly bad.

Supply chain issues

One situation that is very problematic for consumer goods businesses is supply chain costs. Due to the quantum of goods they produce and their geographical footprint, these businesses are highly sensitive to changes in costs.

CL is not immune to this. The company's raw material costs have accelerated, seemingly stabilizing at these heightened prices. Further, they have also experienced rising logistics costs. In the most recent quarter, GPM has declined 160bps.

This is not all bad news, however. Management began to observe stabilization in raw material costs, believing GPM expansion will occur in the full year 2023.

With inflation easing, we have likely seen the "top" of expense levels. This said it is yet to be seen if non-volume-based price depreciation will be possible in 2023. The impact of this has been a contraction in CL's margins since FY20, with GPM falling to 57% from 61%.

Filorga

CL purchased French skincare brand Filorga for $1.69BN, as part of a strategic expansion into the skincare industry. The business is in the premium segment, with a strong presence in Asia and Europe. This always felt like a slightly strange transaction as Filorga brought very little incremental economics while being purchased at a premium. Further, we struggle to see what CL planned for the transaction as we have yet to see any concrete strategic vision from Filorga.

The deal so far has been nothing short of a disaster. Although revenues are not disclosed, Management note they experienced declining sales in Europe and China, its key geographies. This is not surprising given the weakness we are experiencing in the economy. This said sales were already on the decline in 2021, suggesting there is a systemic issue here. CL took an impairment charge of $571M in 2021 and a further $721M in 2022, almost completely wiping out its value.

Giving CL a slight bit of leeway, this is a terribly timed deal in hindsight. COVID-19 lockdowns came soon after, followed by inflationary pressure alongside China struggling with COVID is clearly not a great environment to operate in. Further, the company's products have very good reviews and certainly have a place in the market, with scope for growth. We cannot feel too sorry for CL however as this is why it is imperative to price a deal based on fundamentals.

Where does that leave CL x Filorga now? Well, this business is such a small part of the overall Group that they are unlikely to commit significant resources to turn this around. It is very likely that we never hear of this business again and it remains in its niche.

Financial performance

Q1

CL has recently released its Q1 results, which came in fairly positive. Top-line sales growth for the final quarter was 10%, beating analysts' consensus.

With consumer goods businesses, any growth beyond long-term inflation / population growth is impressive. Organic sales suggest the business has been successful in partially offsetting costs through pricing.

{kind=link}

Presented below is a breakdown of CL's sales by division. CL has strong regional diversification, which will allow for less volatility in sales based on regional cyclicality. Europe continues to be an issue, with yet another quarter of declines.

Further, despite aggressive pricing, volume remains positive at a group level, which implies it is still benefiting from elasticity.

Sales by Division (1) (CL) Sales by division (2) (CL)

Historical performance

CL - Financials (TIKR Terminal)

{kind=link}

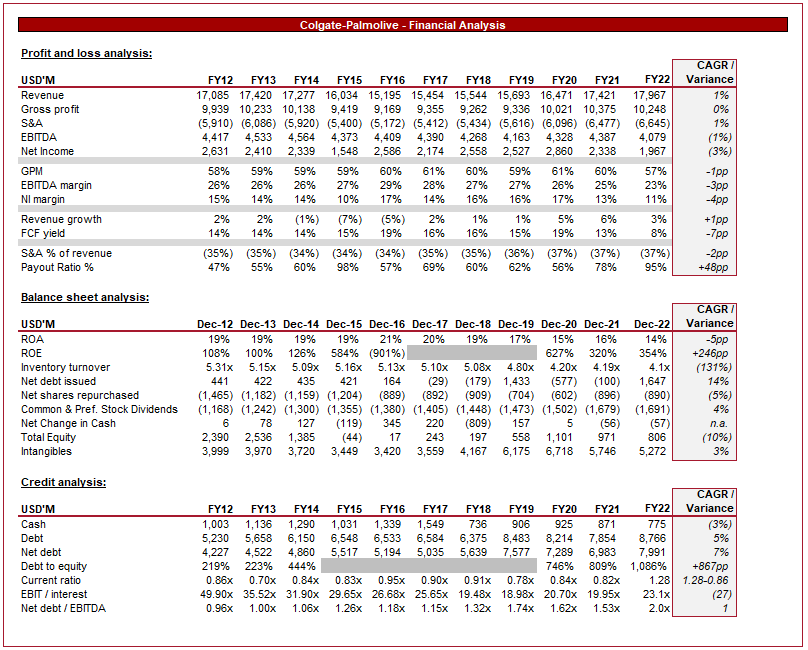

Presented above is CL's financial performance for the last 10 years.

We observe a stagnation in revenue growth, which was driven by a period of declining revenue between FY14 and FY18. During this time, we experienced a strong dollar which caused negative FX movements . The business has moved past this, posting 3 successive years of revenue growth. This said, investors should be wary of a business like this, as earning the level of income it does overseas makes CL very susceptible to a change in exchange rates.

Given the business is fairly mature, we are unlikely to see significant swings in margins. As we have established, the decline is attributable to inflationary costs. This has eaten away partially at EBITDA, resulting in a -1% CAGR decline. Net income is lower than trading would suggest due to the impairment of Filorga.

Moving onto the balance sheet, we are seeing inventory turnover gradually fall, suggesting inventory is slightly more slow-moving. Given that this has been a trend over the last decade, we are not too concerned.

Not unusual for a business this large, we have seen CL consistently issue debt while paying out dividends and buying back shares. We are strongly against funding distributions through the use of debt, even if the business has the capabilities to do this. The business has seen its cash balance gradually decline since the middle of the decade, its net debt balance is now 2.4x EBITDA, and CL has reached a payout ratio of 107% in the LTM. Our view is that dividends and buybacks may have peaked.

CL's overall financial performance is relatively good. We are quite impressed by their ability to consistently grow but are very much concerned by future FX movements and the funding of unsustainable dividends / buybacks.

Peer group analysis

Growth (Seeking Alpha) Profitability (Seeking Alpha)

{kind=link}

{kind=link}

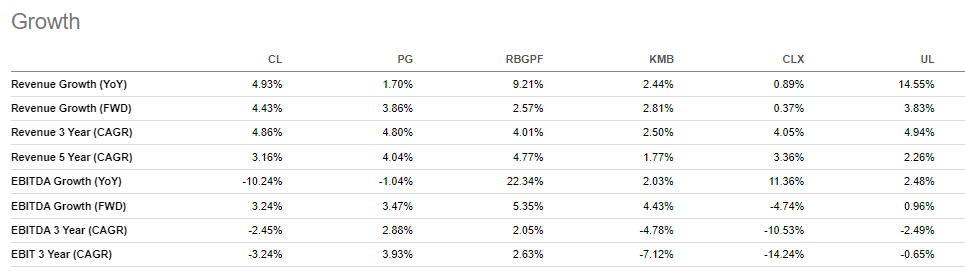

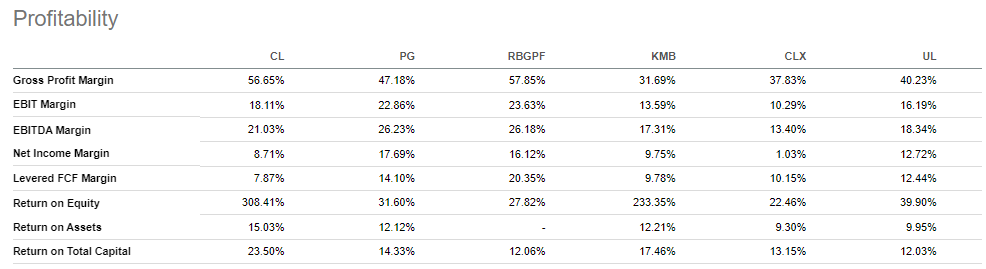

Presented above is a comparison of CL's key financial metrics against a peer group of consumer goods businesses. The differences in the goods sold slightly distort the comparison.

From a profitability perspective, CL stacks up well without standing out. The company has a leading GPM despite the recent contraction and boasts a slightly above-average EBITDA-M. Given the GPM advantage, we would suggest CL is a leading business just below PG, as it is easier to find savings in Opex than in CoS. Growth is in line with its peers, although the company's consistent positive results are a reflection of resilience.

The key to note here is that we have compared the business to a handful of leading CGs businesses, thus is a reflection of CL's leading position.

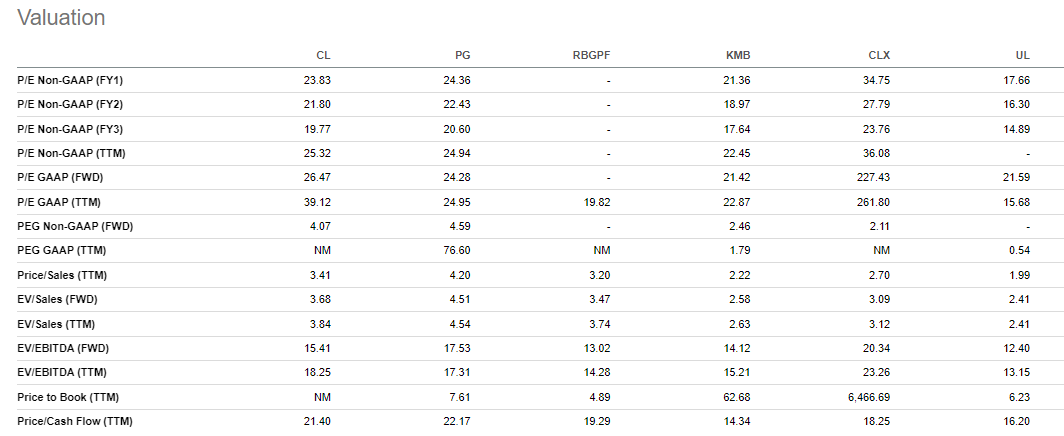

Valuation

{kind=link}

Based on the financial analysis above, our view would be that CL should be valued at a slight premium to the pack, although at a discount to PG.

CL is currently trading at a 9% premium to the average on an LTM EBITDA basis, which looks to be the top end without the business encroaching on PG's valuation.

Outlook is potentially moving toward bullish compared to what was first forecast, but this has yet to be wholly substantiated. The risk remains Europe dragging the Group's performance, as well as margins continuing to decline. Management is forecasting 3-6% growth with a low impact from FX.

If we consider dividend payments, CL is below market average even though it is at its earnings capacity. Unilever ( UL ) for example is only paying out 57%, with PG at 63%. The business is famous for having grown dividends for 59 consecutive years, but this has moved beyond sustainable. With CL's cash and debt balance where they are, we see a likely rebalancing of their capital structure in the coming 3 years, resulting in a reduction in dividends / BBs.

Conclusion

CL has performed relatively well in the last few years, with impressive organic growth. What is slightly concerning is that margins have slipped, with OPM falling from 23.2% in FY19 to 18.1% in the LTM.

We are moderately concerned that performance could worsen in 2023 as demand in key strongholds slows, alongside the potential for unfavorable movements in FX rates. This said, Q1 performance does instill greater confidence that the business has seen the worst of the conditions.

Our biggest issue with CL is its capital structure and financing of dividends/BB. This no longer feels sustainable without consistently raising debt.

CL does perform relatively well against its peers and is valued appropriately but the factors above make the near-term more concerning. We suggest caution.

For further details see:

Colgate-Palmolive: Stagnation And Debt-Fueled Dividends