QQQ - Collapsing Inflation Expectation Is Likely Driving The Rally In Stocks

2023-11-08 06:32:56 ET

Summary

- The S&P 500 has rallied 7% from its October low.

- Declining inflation expectations support a view that the Fed has room to cut rates into 2024.

- Stocks can climb higher supported by tailwinds for earnings growth through next year.

The latest rally in stocks has been a vindication for bulls compared to the volatility between September and October. The S&P 500 is up an impressive 7% from a low near $4,100 in just over a week, adding to a solid 15% gain year to date. We see room for even more upside through 2024.

Why Are Stocks Rallying?

There are several reasons to explain this fresh breath of momentum including many of the points we highlighted in our last macro-themed article reaffirming the bullish view on stocks we've held all year. Some of the factors driving the rally right now include:

- Balanced messaging by the Fed downplaying urgency for more rate hikes.

- Easing geopolitical tensions in the Middle East away from "WW3 scenarios."

- Strong Q3 corporate earnings momentum.

- Indications for ongoing disinflation (oil selloff/ slowing wages).

- Resilient economic conditions.

- Stabilizing long-term bond yields.

- Ongoing "short squeeze".

The sense here is that we're entering an improving macro environment that starts with easing inflationary pressures. Comments by Fed Chairman Powell at the last FOMC claimed the group is "data dependent", and the good news here is that the data that matters is moving in the right direction.

The September payrolls report was highlighted by a moderating pace of hiring along with declining wage growth. Separately, an ongoing selloff in oil has provided a sigh of relief compared to concerns it could spark a round of cost-pull inflation just a few weeks ago.

Overall, the biggest development in recent weeks is the growing consensus that the Fed is done with rate hikes translating into stabilizing bond yields as a tailwind for risk sentiment. We can look forward to the upcoming October CPI report as further confirmation of these trends as the next big catalyst to drive momentum in stocks even higher.

{kind=link}

The Oil Price Selloff Gift

While we haven't been surprised by the strength in equities, it's understandable that the move has caught a large segment of the market off guard.

What we find is that there remains a great deal of confusion between segments of investors that still believe inflation is "out of control!" and that the Fed will need to keep hiking, or that economic activity is collapsing. The data suggests otherwise.

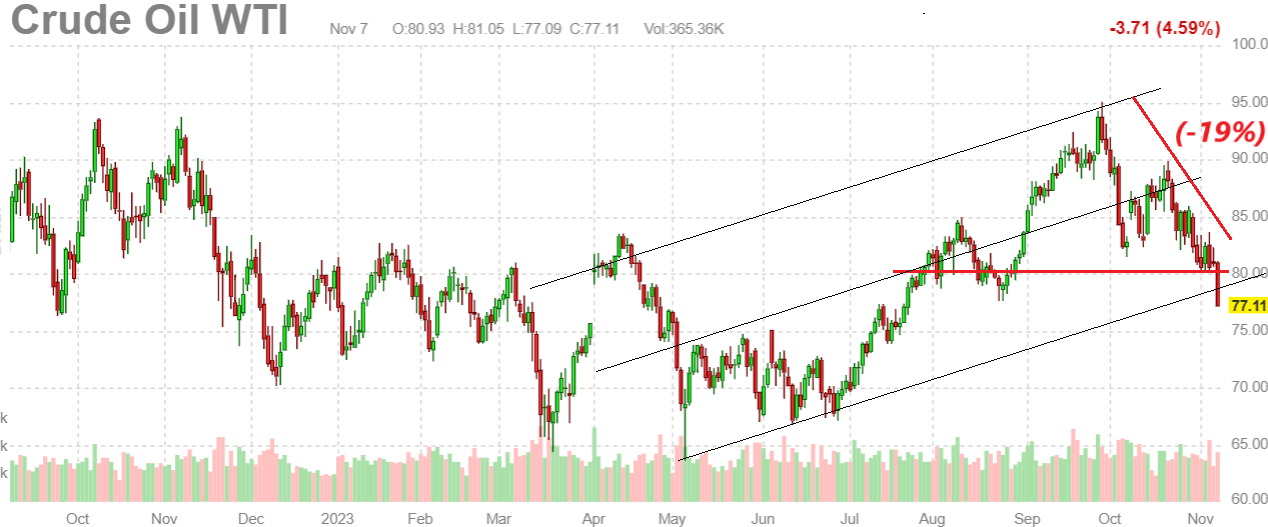

Maybe the biggest turn of events has been the selloff in WTI crude ( USO ), down nearly 20% from its September high. Even with the ongoing Israel-Hamas war, we just haven't seen any supply chain constraints or major production stoppages that would imply a significant breakout higher.

In our view, oil is simply correcting closer to a fair value of around $80.00 which has been the average over the past year. Producers are rushing to take advantage of elevated prices while adding supplies while demand has otherwise been stable.

This is important because it helps reverse the energy spike seen in September that worked its way into a tick higher in that month's CPI. If the narrative by some that inflation was set to re-accelerate with some scenario that oil would climb towards $200bbl, that move has not materialized. We're looking at the chart below as a real-time inflation expectations indicator and it looks convincing to us.

{kind=link}

CPI Is Headed to Lower

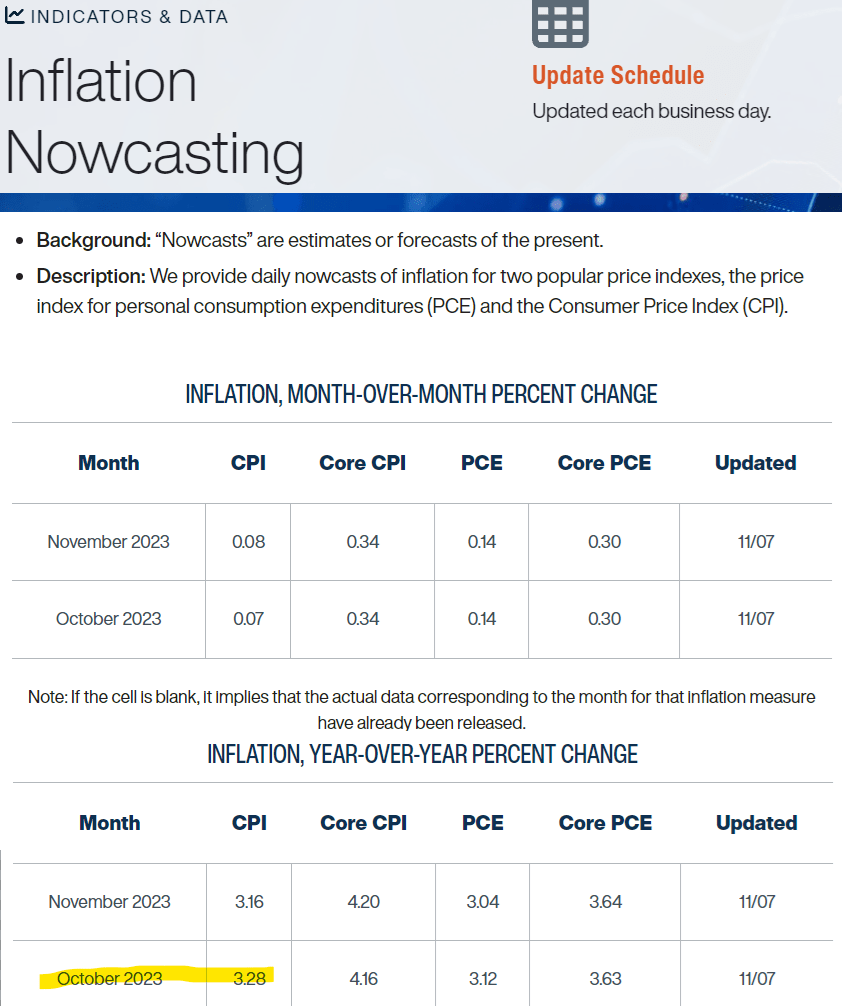

According to the Fed's "Inflation Nowcasting" model, the expectation is that the upcoming October headline CPI will fall to 3.3% compared to the 3.7% September. The data also forecasts another decline of 3.2% in November.

Recognizing that this model has had a hit-or-miss record, we'd say there is a chance the actual number that gets reported on November 14th is even lower. Again, the point here is that it's hard to see why the Fed should be concerned about these numbers.

{kind=link}

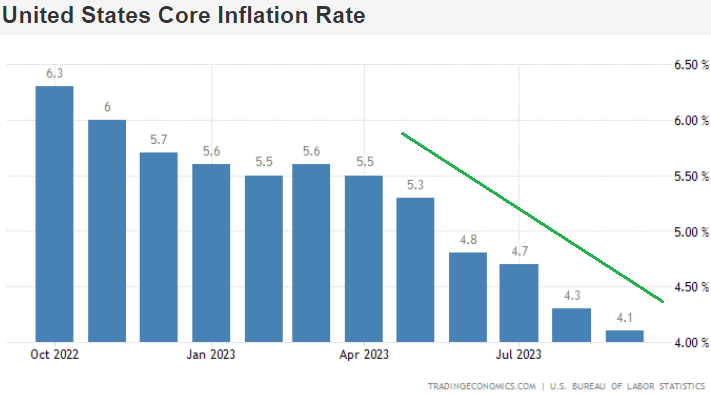

What's even more encouraging in our opinion is the trend lower in the "core-CPI", which excludes food and energy, and hit 4.1% last month. The same Fed model is looking for a 4.2% figure, but well within the margin of error for a flat print compared to September.

We're looking for this figure to continue trending lower over the next several months driven by falling CPI shelter prices, converging with more real-time and private sector housing market data.

Simply put, the official BLS CPI shows "shelter" prices up +6% year over year, while indicators like the Case-Shiller Index, for example, are running at a +2.2% annual rate , effectively already at the Fed's mythical 2% inflation target. Other indicators like the national average for rent prices even show a modest contraction .

{kind=link}

While we're not calling for a housing market "crash", it's clear to us that the impact of the Fed's monetary policy is working through the system is particularly powerful at containing home prices directly through higher mortgage rates. There simply isn't a good reason to see how or why housing prices are accelerating.

From the September payrolls report, where the economy added +150k jobs compared to a +180k consensus, indications are that the labor market is at least cooling off and far from being an inflationary factor.

So what we have here is that while the Fed is likely never going to "declare victory" with a ticker tape parade in its inflation battle, the writing is on the wall that the effort over the past year and a half has already been successful and stocks are responding to that.

Bond Yields Have Peaked

The other major move has been the pullback in bond yields evident by the 10-year Treasury rate currently under 4.6%, down from a high of 5% last month.

We've likely seen it all in terms of interpretations, with some citing a lack of Treasury auctions or a "signal" regarding the strength of the economy. Our more mundane explanation is simply the improving inflation outlook and expectation that the Fed is done with rate hikes.

If rising bond yields with fear that the 10-year Treasury would reach 6% or higher was a major headwind for risk assets in October, the trend is favorable to investors and cold water for bears on the wrong side of the trade.

{kind=link}

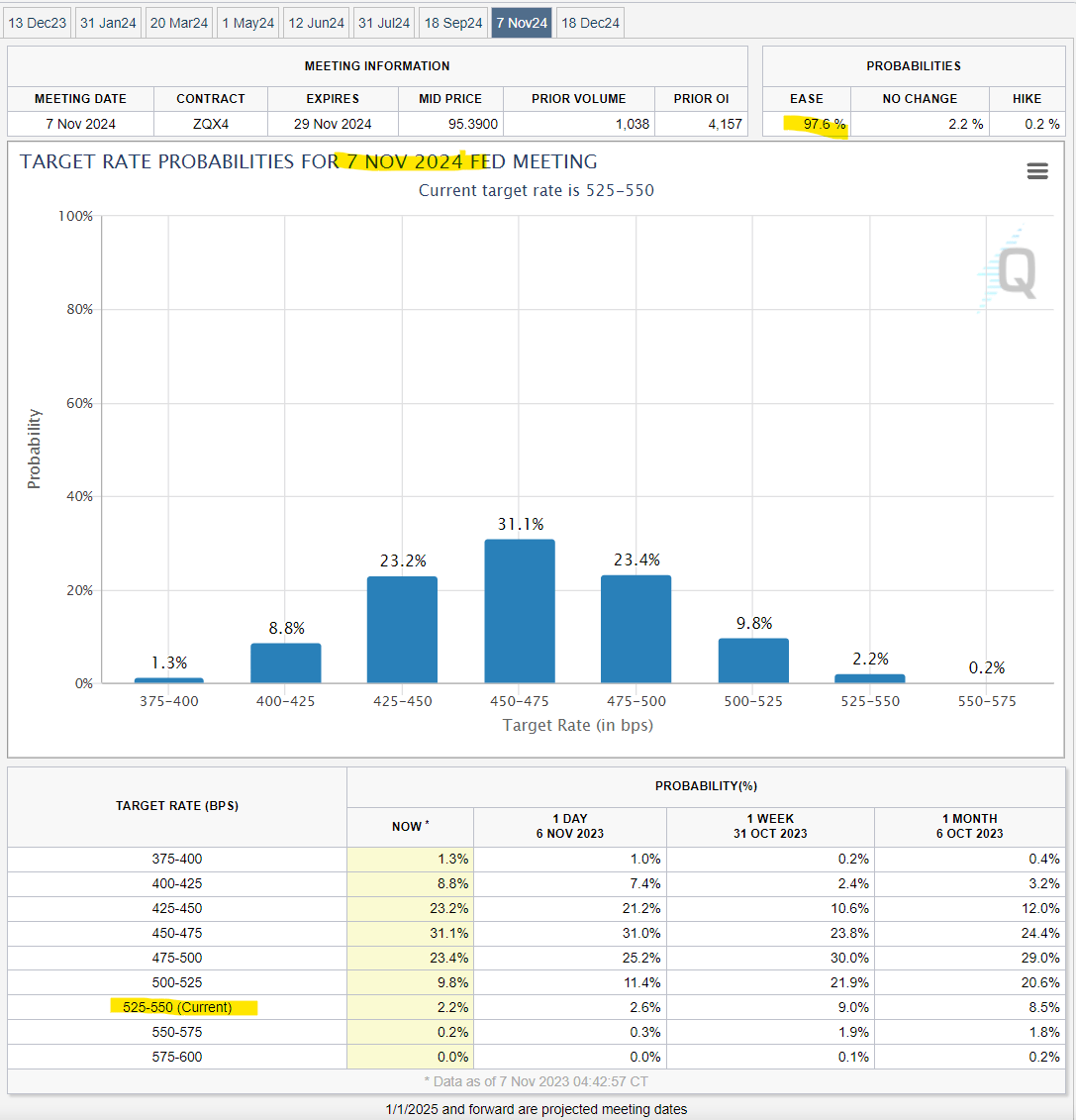

The Fed Can Cut In 2024

The market appears to be pricing in a new reality where inflation will continue to trend lower and the Fed will have the flexibility to cut into 2024. We agree. Indeed, the current consensus is pricing in a 98% probability that the Fed will cut rates by this time next year.

The insight we offer is that this easing backdrop can be achieved -not because the "economy is collapsing" into a deep recession, as stock market bears have been dreaming about since SPX 3500, but simply because inflation expectations can justify that move. This is the soft landing scenario of inflation trending lower while averting a recession many did not believe was possible since 2022.

Consider a point where the CPI is firmly under 3% within the next three to six months. At that point, the current Fed Funds Rate of 5.5% would simply be unnecessary with confidence that inflation expectations are contained. The Fed could cut while staying consistent with its messaging for restrictive monetary policy, assuming the neutral rate is just a bit lower than the current level.

From the chart below, we are in the camp of projecting one or two rate cuts by the end of next year, balancing what remains a resilient economy with a perpetually cautious Fed.

{kind=link}

Stay Bullish On Stocks

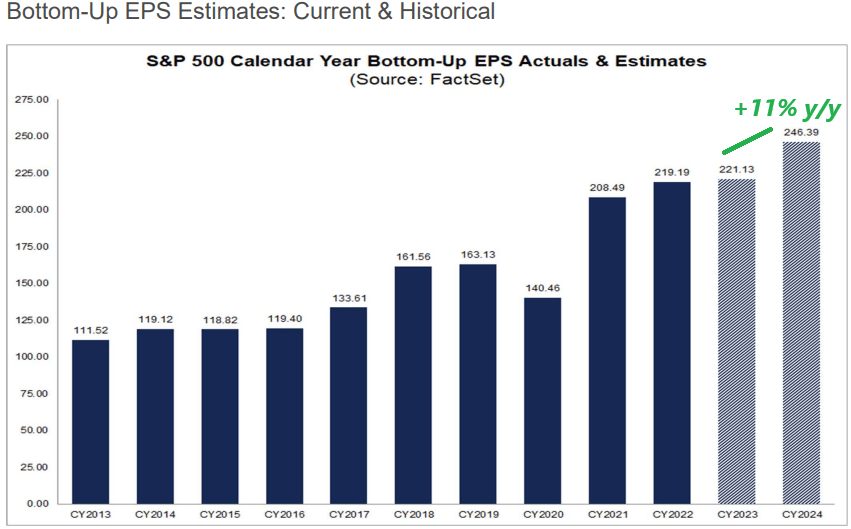

Beyond putting our applied economics degree to good use, the recognition here is that earnings growth remains the primary driver of stock prices. The current consensus is for an 11% increase in bottom-up EPS as an aggregate of S&P 500 companies in 2024.

Naturally, bears don't want to believe these figures but they seem completely reasonable in our view. Keep in mind that companies just posted a historically strong Q3 earnings season where 81% beat consensus estimates.

{kind=link}

In our view, those same market leaders are well-positioned to continue driving profits higher, benefiting from the combination of easing inflationary cost pressures while capturing a new round of top-line growth. Beyond the uncertainty in the timing of Fed rate cuts, just the pullback in long-term bond yields already supports some measure of valuation multiples expansion.

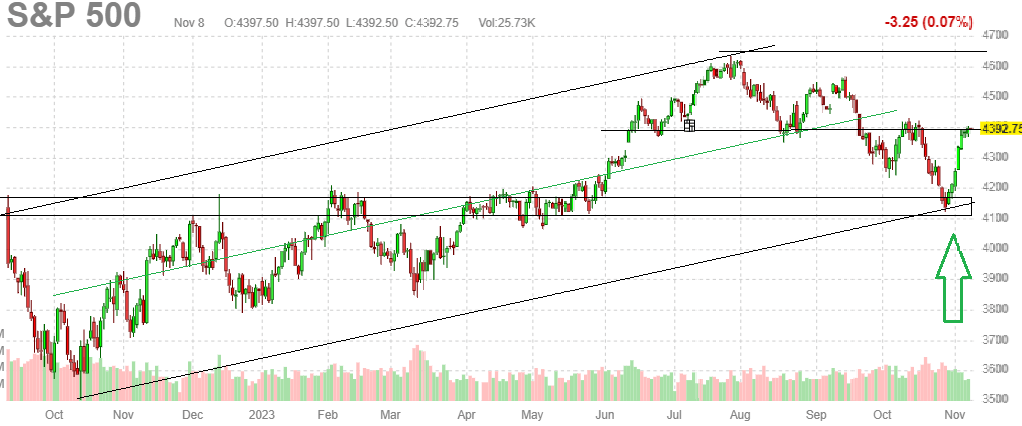

Ultimately, if we're correct in our market assessment, the S&P 500 should have room to climb more than 11% over the next year through improving risk sentiment. Our price target for 2024 at $5,000 implies a 20x multiple on the current 2024 consensus bottom-up EPS for the S&P 500.

In the near term, we see some consolidation around $4,400 until the October CPI report as the next major market-moving indicator. By year end, $4,650 is our price target reclaiming the highs from late July.

{kind=link}

Final Thoughts

The doom-and-gloom narrative that has dominated the market over the last several months is collapsing alongside inflation expectations. We're on the side of investors who are capable of putting aside emotional biases and seeing the big picture. That realization by some is supportive of a short covering as bears begin to accept a more favorable market reality.

Ultimately, we believe there is a good chance stocks have more upside. That being said, it's worth considering the other side of the table as the risks to watch. A break in the S&P 500 under the $4,100 area of technical support would signal a more concerning turn of events.

Bears right now will "need" inflation to re-accelerate and hope for a hot CPI print over the next few months that would unanchor both inflation expectations and the current consensus for the direction of Fed policy. The possibility that economic conditions deteriorate, defined by a sharp contraction in consumer spending, would also undermine our more optimistic assessment.

For further details see:

Collapsing Inflation Expectation Is Likely Driving The Rally In Stocks