COLM - Columbia Sportswear: A Mix Of Good And Meh

2023-11-06 06:10:32 ET

Summary

- Columbia Sportswear is a well-run, mature company with predictable profitability, modest growth, and absence of debt as its strongest attributes.

- Out of the four brands the company owns, Columbia Sportswear and Sorel are doing well, but Prana and Mountain Hardwear leave a lot to be desired.

- The lackluster performance of Prana is likely to be hiding a lot of potential if the company is able to take some hints from companies like Lululemon.

- A heavy investment in the company at the current stock price should hinge on a strong conviction of improved future growth.

The 10-Second Thesis

Columbia Sportswear ( COLM ) is a Portland-based designer, developer, marketer, and distributor of outdoor, active, and everyday lifestyle apparel and footwear founded in 1938. Because I live in Portland, I would say it is a well-known activewear brand, but with a market cap shy of $5 billion and annual sales of roughly $3.6 billion, I am not sure my geographic location is not influencing how I perceive the company. I have no doubts every single person on the planet knows its next-door neighbor ( NKE ), but I would guess COLM is largely unknown in many parts of the world. About 66% of sales are in the US after all. However, COLM is a high-quality company in its own right. It has grown at about 7% annually since 2007, has no debt on its balance sheet, and has been (earnings) profitable every single year. On top of that, it even pays a dividend: 1.55% yield and a 5-year dividend growth of about 8.2%. With a conservative forecast, an investment made at the current share price is likely to have an internal rate of return ((IRR)) not far from 10%. It's not earth-shattering, but the downside seems limited, thus likely in the wheelhouse of the more risk-averse investors who might also enjoy a more dividend-focused strategy.

Peeling The Onion

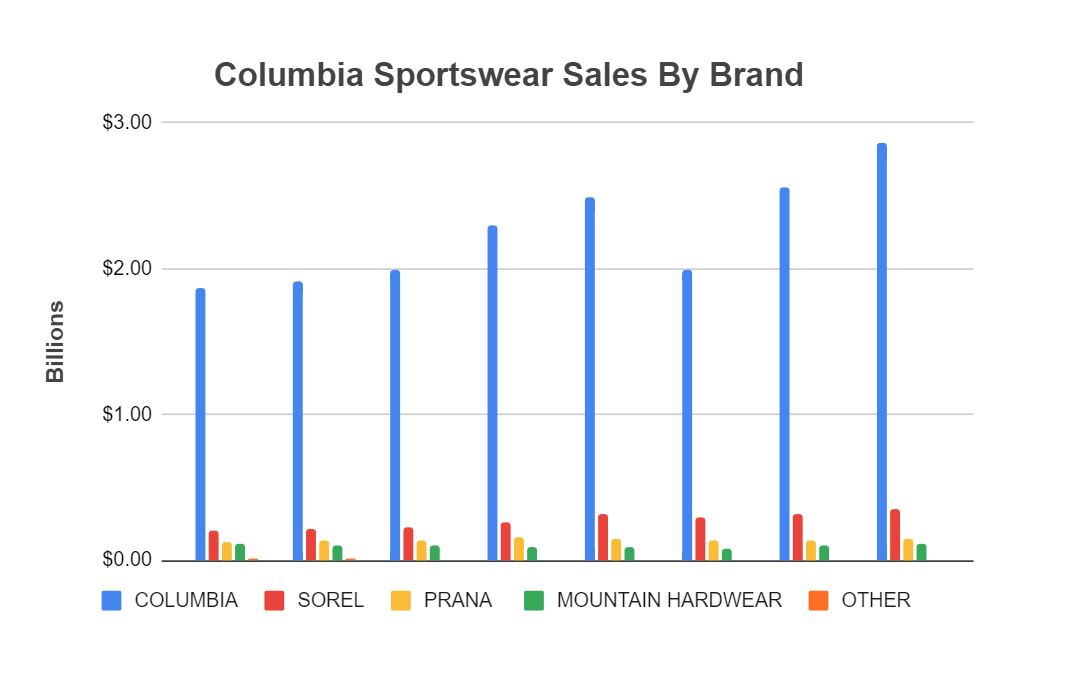

I will start by getting the meh out of the way, and that has to do with the brands the company owns. These are Columbia, Sorel, Prana, and Mountain Hardwear, which, in the same order, represent roughly 82%, 10%, 4%, and 3% of the company's sales using numbers in the most recent 10K. Figure 1 shows how these proportions have changed since 2015. One brand alone seems to be pulling the weight of the company. Although sales have grown at a similar rate for Columbia and Sorel since 2015 (6.3% and 7.5%, respectively), given the huge disparity in sales, we would expect a much faster growth for Sorel, which has not happened in this particular period.

Figure: Revenue By Brand (Author)

{kind=link}

However, if we zoom out all the way back to 2008, the point at which the company started reporting revenue for each brand, we see a growth of about 15.2% per year for Sorel (Figure 2). This is a much more interesting figure, but comparing it to recent performance makes me wonder if Sorel is running out of breath. Let's put Sorel aside though. Sales are growing regardless. The problem is elsewhere. Figure 2 should clearly show where that meh I mentioned is. Something is clearly not working with Prana and Mountain Hardwear. Prana was acquired in 2014 and has grown at an insignificant 1.9% per year since. The picture is even bleaker for Mountain Hardwear with a 1% CAGR since 2008. Both brands seem to be just dead weight.

Figure 2: Growth by brand (Author)

{kind=link}

Despite showing worse growth, Mountain Hardwear has paid for itself. Acquired for $36 million in 2003, it has generated about $115 million in free cash flow if we assume an FCF margin of 6.5%, the overall company's average since 2007. That's a 12% internal rate of return ((IRR)) since the acquisition or a payback period of about 6 years. The initial price saved the investment despite the negative growth since 2012.

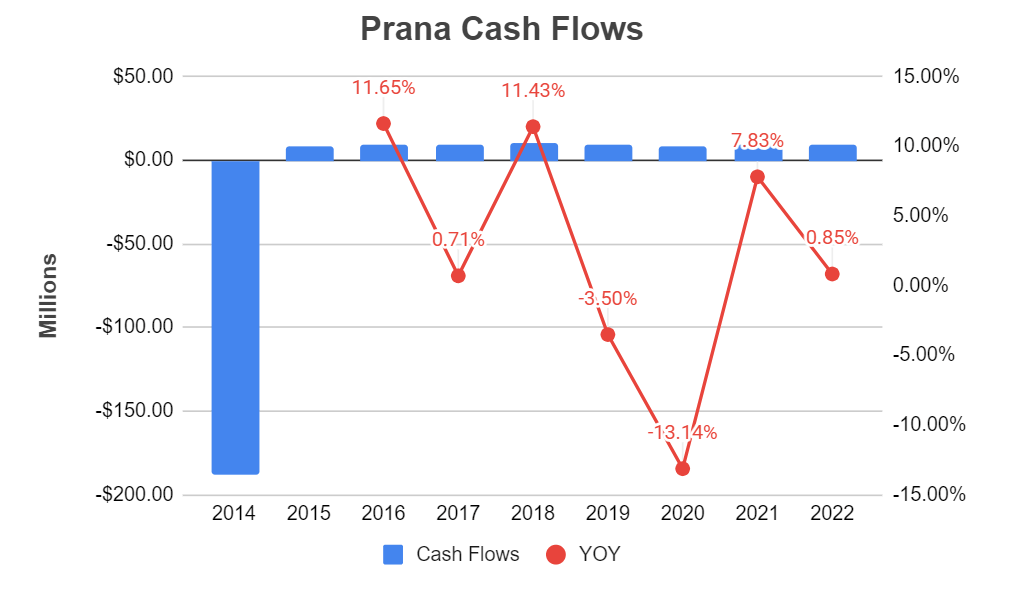

The same cannot be said for Prana. Acquired in 2014, the IRR is sitting at -17%, and at the current cash flows, the payback period will be 20.5 years. I am assuming the same 6.5% FCF margin, which is likely too generous, if nothing else because of higher expenses to make a less-known brand more popular. The reason for the return is once again the price paid for the company, $188.5 million (Figure 3).

Figure 3: Prana Cash Flows (Author)

{kind=link}

To round it up, let's take a look at Sorel from the same perspective. I made some assumptions for revenue between 2001 and 2008 because the company did not report sales for the brand separately during this period. However, that is not significant anyway because the cash flow generated by Sorel in 2019 alone more than covers the paltry $8 million paid for the company in 2000 (Figure 4). If my assumptions are reasonable, the IRR for this acquisition is around 25% over the two decades, clearly the best investment out of the three ancillary brands.

Figure 4: Sorel Cash Flows (Author)

{kind=link}

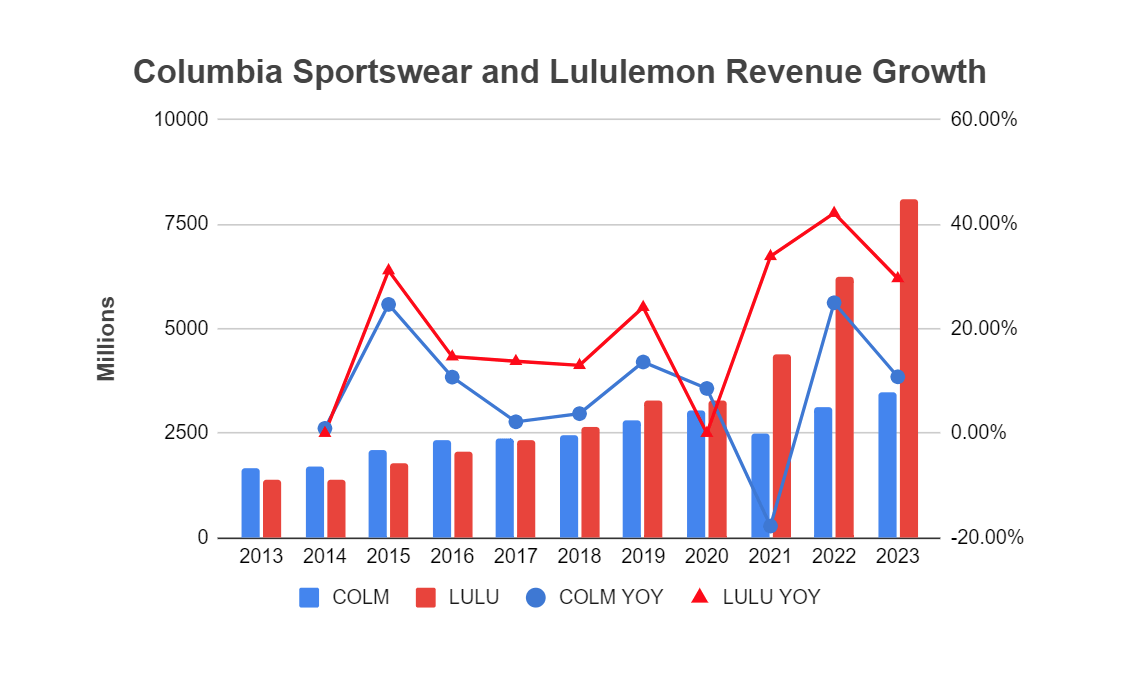

I think we have peeled the onion and identified both the sweet and the eye-irritating parts. Columbia and Sorel deserve a thumbs-up, Prana and Mountain Hardwear seem to need some magic worked into them to become more than dead weight. If I were to guess, Lululemon ( LULU ) as a much better-known brand creates some shadow over Prana's growth with its overlapping offerings. Lululemon's 10-year revenue CAGR of 23% is just astounding in comparison not only to Prana but to Columbia Sportswear as a whole. Surprisingly enough, Columbia had a higher revenue in 2013 but LULU was able to grow slightly faster until 2020, the point at which Lululemon just took off (Figure 5). Lululemon found something after the pandemic that Columbia does not seem to know about, more on that later.

Figure 5: Columbia and Lululemon Growth (Author)

{kind=link}

Putting The Onion Back Together

As a whole, Columbia is a quality company whose weakest point is growth. It's not that the company is stagnant, but the 5.6% CAGR since 2015 up to the TTM is nothing to write home about, especially if compared to Lululemon. Compared to the outdoor segment of VFC, essentially The North Face brand, it's not out of line though (Figure 6). Among publicly traded companies, VFC is one of the most direct competitors to Columbia Sportswear when the company is taken as a whole.

Figure 6: VFC and Columbia Comparative Growth (Author)

{kind=link}

The overall picture is that of a somewhat heavy-footed entity doing its own thing well enough to turn a profit year in and year out, a profile compatible with a company founded in 1938 and under the governance of one family throughout its entire history. The Boyle family controls just under 50% of the company. A bit more irreverence and perhaps a higher degree of outside influence may be what the company needs to replicate the success of Lululemon for example.

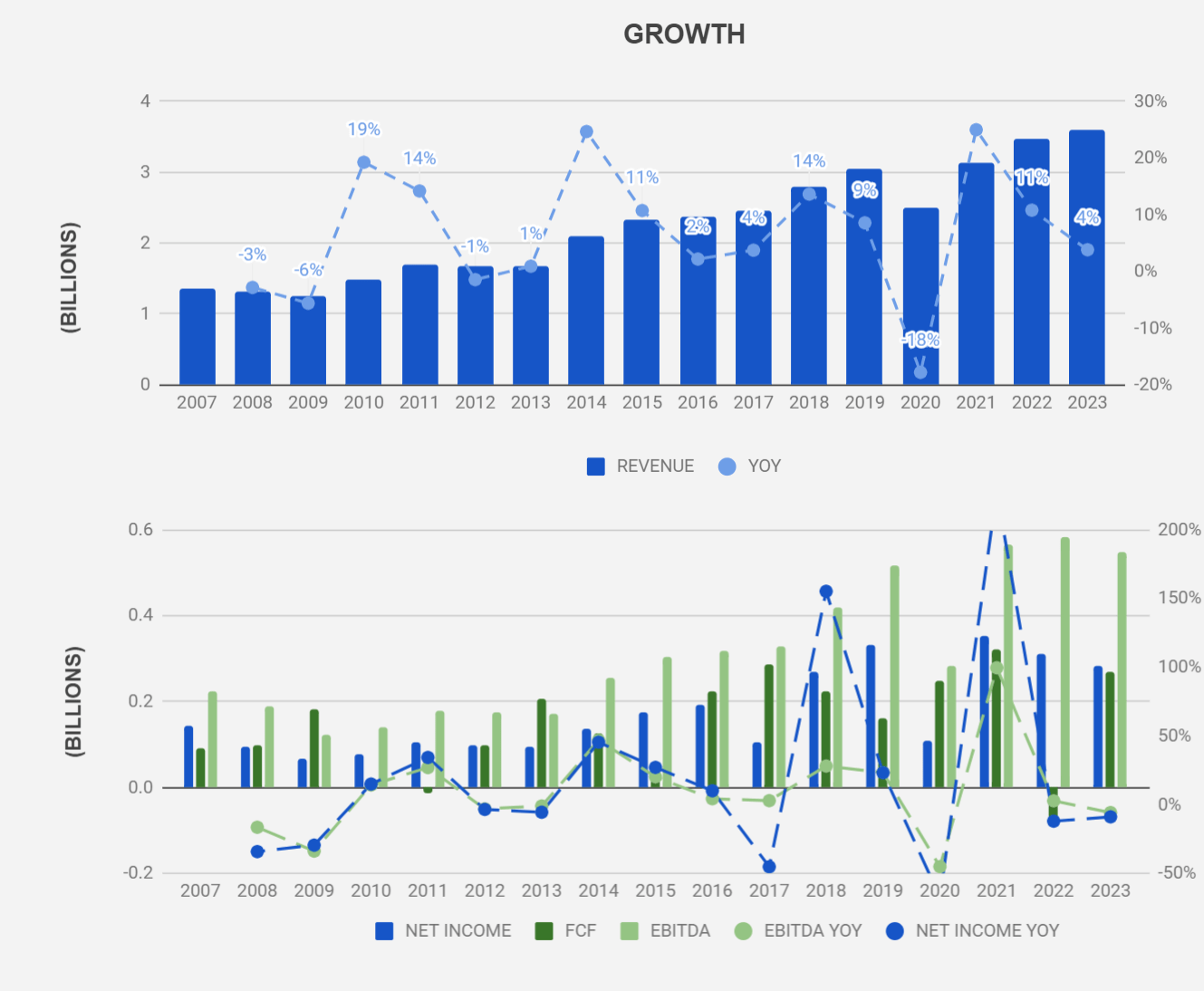

Revenue is growing, margins, both gross and net are stable, and as of 2007, only 2011 and 2020 saw negative free cash flows. From an earnings perspective, there is no history of negative profitability in this same period (Figure 7).

Figure 7: Columbia's Revenue, Net Income and Free Cash Flow (Author)

{kind=link}

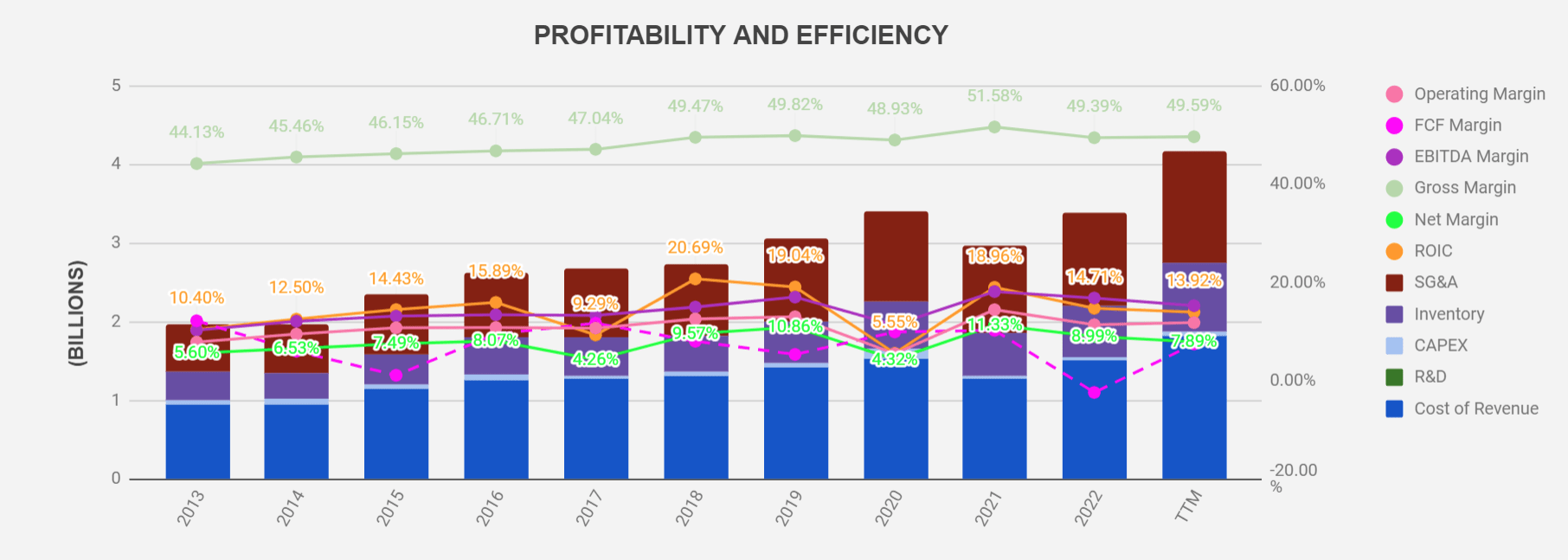

Taking the last 30 quarters as a sample, the 85% confidence interval for the net margin is between 6.3% and 9.1%. As for gross margin, it has gone from about 44% in 2007 to 49.6% in the TTM. The return on invested capital ((ROIC)) peaked at around 20% in 2018 and has since declined to about 13.9%. Because the company has no debt, the weighted average cost of capital ((WACC)) is the same as the cost of equity ((COE)) at around 8.9%. Although value destruction is nowhere near, with the gap between ROIC and COE getting narrower, the company is losing steam in creating value for its shareholders. Margins and ROIC since 2013 are shown in Figure 8.

Figure 8: Columbia's Profitability and Efficiency (Author)

{kind=link}

All in all, the good outweighs the meh , and with a rebound in free cash flow generation after the pandemic and ensuing supply chain woes, the company is trading at a free cash flow yield of about 5.5% or a 17.8 free cash flow multiple. With inflation at 3.7% and the 10-year treasury at 4.6%, given Columbia's solid financial position and historical performance, if no other options existed, I would not have doubts about where to put my money. For reference, the free cash flow yield of the Nasdaq in December 2022 was 4.7%, having risen to 5.4% in the TTM (COLM is listed on the Nasdaq).

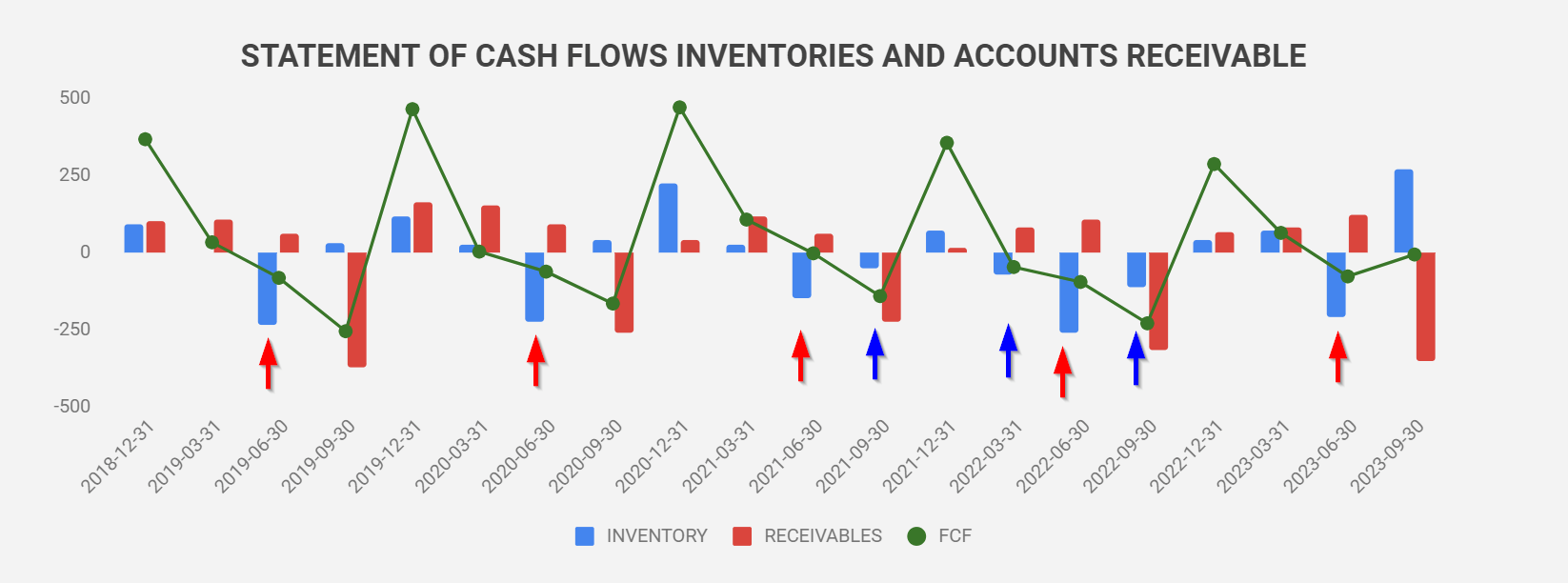

If doubts persist about the predictability of the business, Figure 9 should dissipate those. Invariably we see outflows to purchase inventory in June (red arrows) and FCF peaks at the end of the year (green line). The inventory worries most companies went through after COVID led them to increase inventory levels and that can be seen in the unusual outflows of Figure 9 (blue arrows), the major culprit of the free cash flow dip in 2022 seen in Figure 7. If not for that, Columbia's free cash flow quarter over quarter (green line) is like a healthy and very well-synchronized heartbeat. Once again, we can see the well-oiled machine at work. It's not the irreverent new kid on the block, but it does what it needs to do well enough to spin cash when all is said and done. No adrenaline, but no heart attack either.

Figure 9: Inventories, Receivables and Free Cash Flow (Author)

{kind=link}

The X-Factor

Although Columbia Sportswear and Lululemon do not completely overlap in terms of their market and product offerings, their similar revenue up to 2020 (Figure 5 above) made me look at the strategies behind both companies. And there are some big differences, one being the way they distribute their products. Both companies operate brick-and-mortar stores but whereas Columbia derives roughly 54% of its revenue from selling to wholesalers and distributors, Lululemon's wholesale revenue is less than 9%. Lululemon prefers to sell directly to its customers, which might give them better control over the brand and how it is perceived by customers. This was already true in 2013 when Lululemon actually lagged behind Columbia in revenue but had roughly 50% more retail stores. Since then both companies have grown their physical locations at about the same rate (roughly 10% per year), and in 2022 Lululemon is still betting on its physical locations more than Columbia does (Figure 10). Besides, in 2018, 83% of Columbia stores in the US were outlet locations. Lululemon, on the other hand, keeps their outlet locations at just about 5.9%. Many consumers will be tempted to cheapen their perception of one brand and assign a premium to the other based on how the products are sold.

Figure 10: Lululemon and Columbia Retail Store Growth (Author)

{kind=link}

The big difference though is e-commerce. There is a cliff between both companies here. It is hard to tell what percentage of sales Columbia derived from e-commerce in 2013 because the company did not report it separately until 2020. at that time, the company revealed it to be 19% of its revenue. In 2022 though, e-commerce had not moved anywhere representing 18% of sales or $623 million. Lululemon's online business was almost 6 times larger in 2022 clocking in at $3.6 billion and representing an astounding 45.6% of its revenue. The seeds of this strategy were there in 2013 with online sales of $263 million or 16.5% of sales (Figure 11). That was 42% of Columbia's online sales today back in 2013! I can't resist going back to the idea of contrasting a heavy-footed mature company with the irreverent new kid on the block. One is trying new things, the other doing the old tried and true.

Figure 11: Lululemon and Columbia's e-Commerce Growth (Author)

{kind=link}

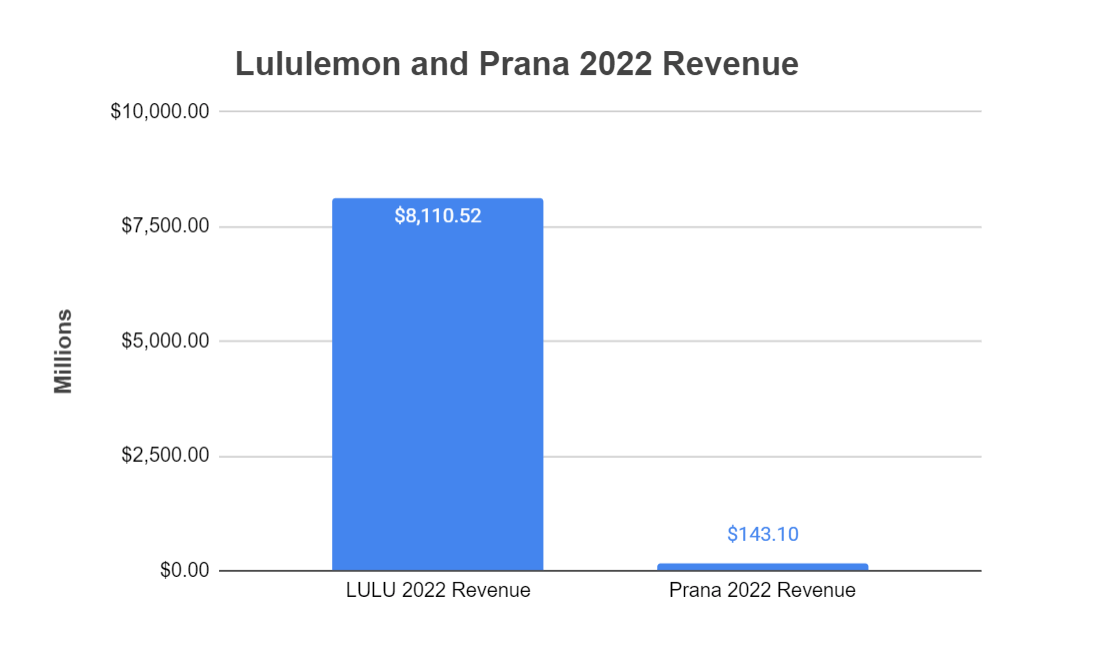

To put my hypothesis of brand power and brand control to the test, I asked my wife if she knew Lululemon. Silly question right? Of course, she did! Then I asked about Prana. She seemed to know it at first, but then I realized she was mixing it in her head with something else. I know, a sample of one, but not a good sign nonetheless... Not a good sign when Columbia spends 5.9% of its revenue on advertising, compared to 3.72% for Lululemon. Not a good sign when almost a decade after the acquisition of Prana, the brand's growth is stuck at 1.9% with $143 million in sales whereas Lululemon has ballooned to $8.1 billion! I know it's not all apples to apples, but there is a lot of apple flavor in the comparison (Figure 12). I will go out on a limb and suggest that no one knows Prana after 10 years. The silver lining here is that there is a lot of potential in Prana if Columbia Sportswear decides to poach some ideas on how to add value to a brand in the eyes of customers. I would say about $8 billion in Potential in the best of the best-case scenarios.

Figure 12: Revenue for Lululemon and Prana (Author)

{kind=link}

Key Takeaways

- Direct-to-consumer and full control of sales seems to be a better strategy than relying on wholesale and distributors.

- A Strong online presence is mandatory. A half commitment to that seems to lead to lackluster results.

- Perception of a brand seems to be influenced by how the brand, not just the products, reaches its potential customers.

- Columbia Sportswear is a profitable and well-run company already. Adding some spice to its strategy can only make it better, potentially a lot better.

What To Do?

That's ultimately each investor's decision, of course. For full disclosure, I do own a small position in COLM with a cost basis of $70 per share and will consider adding to my position at the right price. What is the right price for me? It is around $70, preferably lower, and here is my rationale. Despite recognizing a great deal of potential for growth if some semblance of a Lululemon-like strategy can be even modestly implemented, I am not fully convinced that will happen. Prana alone might be a compressed spring ready to jump at any point, but I will not bank my investment on those hopes. If I am going to invest, I am going to do it based on the heavy-footed but well-run company that Columbia has revealed itself to be. From this angle, my basic assumptions are (blue arrows in Figure 13, from top to bottom):

- I am starting with an FCF of $4.02, $0.37 below TTM FCF per share. It does not hurt to start conservatively given that, although we seem to be past the hiccup of negative FCF in 2022, FCF tends to be a bit more volatile than earnings as seen in Figure 7.

- Over the long run, FCF growth tends to converge with revenue growth. The volatility I just mentioned is seen in the rolling 10-year FCF growth (green line) below the 10-year rolling revenue growth 3 times (red line). The remaining data points overlap the revenue growth. I think this is a fair assumption for a mature company. Rolling revenue growth is at 6%.

- If the price to free cash flow multiple were a random variable with a normal distribution (actually not far from that as seen for the 10-year period), the probability of buying the stock at the current multiple would be about 35%. Not a bargain, but not expensive either. We would normally expect to buy it between 19.63 and 20.84 times free cash flow, and only be able to buy it as cheap as it is now only 35% of the time.

- Although I mentioned that FCF growth seems to converge with revenue growth, I am haircutting the future growth to 5%, again with the mature company image in mind, which leads me to an exit multiple of 17 in 10 years' time, below the 95% confidence interval for the multiple. In the scenario I am painting in my mind, without any spice to the stock, I can't justify the 10-year average.

- Am I a bit too conservative? Perhaps. But with better alternatives in the market, I do not find any reason to be aggressive in my assumptions for COLM. I can wait for hints that the spring is going to jump and, in the meantime, I might be able to snatch some shares at the mature company price. This way, I believe any downside will be limited. In fact, my chances of getting a good return on the "no exciting stuff happening" scenario are decent and increase if the stock price drops below $70, which has happened in the last 52 weeks.

- For this personal valuation, I assume a 10% discount rate as my hurdle rate, the thrown-around long-term market return.

Figure 13: COLM Valuation (Author)

{kind=link}

The Recap

There is a lot to like about Columbia Sportswear and a lot of potential currently wrapped in the meh performance/attributes of the company. With revenue growing in the middle single digits, good and predictable profitability, good ROIC, decent return to shareholders in the form of a growing dividend and share buybacks, and no debt on the balance sheet, buying the company at the price of modest growth is likely to lead to no regrets in the future. If the company is able to uncork a growth punch, investors will be getting an outsized return with this one. I think the stock is not unfairly priced but I am opting to play this one safe given other opportunities in the market.

For further details see:

Columbia Sportswear: A Mix Of Good And Meh