COLM - Columbia Sportswear: Pressure On Revenue Growth And Margins Resumes

2023-08-10 22:22:42 ET

Summary

- In the second quarter, the company's revenue increased by 7.4% YoY, while operating margin decreased to 1%.

- The company cut guidance for 2023 due to weak trading trends in the US market, which accounts for 64% of total revenue in 2Q 2023.

- I expect revenue growth and operating margin to be under pressure in the coming quarters.

Introduction

Shares of Columbia Sportswear ( COLM ) have dropped 16% YTD. Despite the fact that the company showed strong reporting for the 2nd quarter of 2023, the company's shares are under pressure due to the decrease in the company's guidance. I believe that now is still not the best time to go long.

Investment thesis

In my personal opinion, we may see continued pressure on the company's financials in the coming quarters because: first, the company expects demand in the US market to recover more slowly than previously expected. I believe if we see inflation slow down in the second half of the year, then demand will be delayed as consumers continue to face higher spending on food and rent. Secondly, a slowdown in revenue growth in the US market (64% of total revenue) may lead to a deleverage effect, since part of operating expenses is fixed (rent, salary). Thirdly, inventory levels are still at a relatively high level, which, in my opinion, could lead to an increase in promotional activity and have a negative impact on operating margins. In addition, management's comments on the prAna and Mountain Hardwear brands' revenue growth are not encouraging, as the company expects revenue to continue to decline.

Company overview

Columbia Sportswear sells sportswear, shoes and accessories for men and women. The company's main brands are Columbia, SOREL, prAna and Mountain Hardwear. The company operates in the markets of the USA, Canada, Latin America, Europe and Asia.

2Q 2023 Earnings Review

The company reported better than investors expected . The company's revenue increased by 7.4% YoY . The Europe, Middle East and Africa and Latin America and Asia Pacific segments made the largest contribution to revenue growth, where revenue grew by 75% YoY and 28.2% YoY, respectively. However, in the US and Canadian markets, the company's revenue decreased by 3.2% YoY and 21.3% YoY, respectively. You can see the details of the revenue mix change in the chart below.

{kind=link}

If we look at the revenue categories, the main contributor to revenue growth was growth in the footwear category, where revenue grew by just over 20% YoY, while revenue in the apparel category grew by 4.4% YoY. In terms of sales channels, sales to the Wholesale segments grew by 9.5% YoY, while DTC sales grew by only 5.2% YoY. You can see the details in the charts below.

{kind=link}

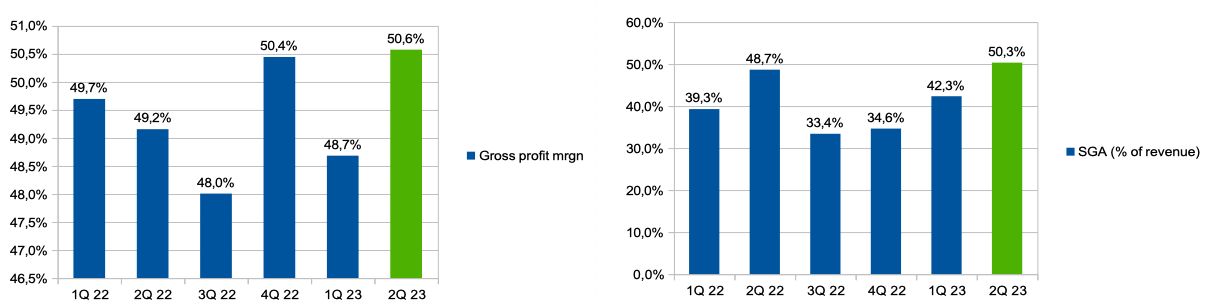

Gross profit margin increased from 49.2% in Q2 2022 to 50.6% in Q2 2023, driven by lower freight costs and inventory optimization. SGA spending (% of revenue) increased from 48.7% in Q2 2022 to 50.3% in Q2 2023 due to increased supply chain spending and development of DTC sales channels.

{kind=link}

Thus, the operating margin decreased from 1.5% in Q2 2022 to 1.0% in Q2 2023.

Operating margin trend (Company's information)

I would also like to draw attention to the level of stocks at the end of the quarter, which is still at a high level relative to historical data. I believe that higher inventory levels could lead to additional promotional activity and price investment in the coming quarters, which could put pressure on operating margins.

{kind=link}

In addition, the company cut its guidance for 2023, both on revenue and operating margin, in view of the expectation of a slowdown in sales in the US market, which accounts for about 64% of total revenue in 2Q 2023.

{kind=link}

My expectations

Despite the fact that the company's financial performance in the markets of Europe, Asia and Latin America currently looks more optimistic, sales revenue and profitability in the US continue to be one of the main drivers/risks, since the US accounts for almost 65% of total revenue for the 2nd quarter of 2023.

As I noted in my article earlier, the company's inventory level is still at a relatively high level, which may indicate the possibility of additional investment in prices and increased promotional activity to reduce the amount of inventory in stock, as a result, this may have a negative impact on the operating business profitability. I would like to note that my assumptions are confirmed by management's comments during the Earnings Call , where the CEO of the company says that destocking is one of the top priorities.

As I mentioned on the last call, reducing inventory is our top priority. Inventory exiting the quarter was up 21% year-over-year.

I expect that the decline in US revenue due to macro headwinds may put pressure on the business's consolidated financials in the coming quarters. I think consumer spending will lag behind even if we see inflation slow down in the second half of 2023 because consumers will continue to face higher spending on rent, interest and food. In addition, I think that the decline in US revenue could lead to pressure on operating margins as a result of the deleverage effect, because some of the costs of logistics, rent and wages are fixed.

Risks

Margin: decreasing economies of scale in the US market could lead to a deleverage effect, and relatively high inventory levels could boost the company's promotional activity, which could have a negative impact on the operating margin of the business in the coming quarters.

FX: an unfavorable change in exchange rates (strengthening USD) may lead to a decrease in revenue in the geography of Latin America, Europe and Asia, expressed in dollar terms.

Macro (general risk): high inflation and a decline in real incomes could help reduce consumer spending in the discetionary segment, which could put pressure on the company's revenue growth in the US market.

Valuation

Valuation Grade is C-. Under multiples of P/E ((FWD)) and EV/EBITDA ((FWD)), the stock trades at 16x and 10x, respectively, which is 5% higher than the sector median and 1% lower than the sector median, respectively. In my personal opinion, the company's current valuation still does not look cheap, while we may see a decline in forecasts and actual financial results in terms of both revenue and EPS going forward.

{kind=link}

Conclusion

On the one hand, the company's share price has already declined, and the valuation in accordance with P/E and EV/EBITDA multiples provides investors with a discount to the 5-year average, so I avoid the Sell recommendation. However, I expect revenue growth and operating margin to be under pressure in the coming quarters, and I see no additional growth catalysts/drivers, so my recommendation is Hold.

For further details see:

Columbia Sportswear: Pressure On Revenue Growth And Margins Resumes