STN - Comfort Systems USA: Growth At A Reasonable Price

2023-08-02 12:00:37 ET

Summary

- Comfort Systems USA is a construction services company experiencing rapid growth through acquisitions and organic growth.

- The company offers a range of services including mechanical contracting, off-site construction, and electrical installation.

- Despite concerns about a potential recession, Comfort Systems USA has a diverse market exposure that should help mitigate any downturn.

- Shares are pricey, but growth is strong enough to make this an interesting prospect.

As a rule of thumb, I tend to be very skeptical when it comes to growth-oriented investments. Although I love picking up a growth stock at a low price, many of the opportunities out there require significant premiums in order to participate. But if growth is robust enough, that premium can sometimes be worth it. One company that fits this description, at least in my opinion, is Comfort Systems USA ( FIX ), an enterprise that's focused largely on various construction services. Even though the stock looks very expensive at the moment, the backlog is robust and shares are getting cheaper rather rapidly. While I would not be so bold as to claim that the company will make you rich, I do think that the combination of growth and price is just enough to justify a soft 'buy' rating at this time.

An interesting business achieving rapid growth

Even though describing Comfort Systems USA as a construction services firm would be technically appropriate, at its core, the company centers around a very specific range of services. For instance, it provides mechanical contracting solutions centered around HVAC systems, plumbing, piping and controls, and more. It also offers off-site construction, monitoring, and Fire Protection services. Under its electrical operations, the business engages in the installation and servicing of electrical systems.

{kind=link}

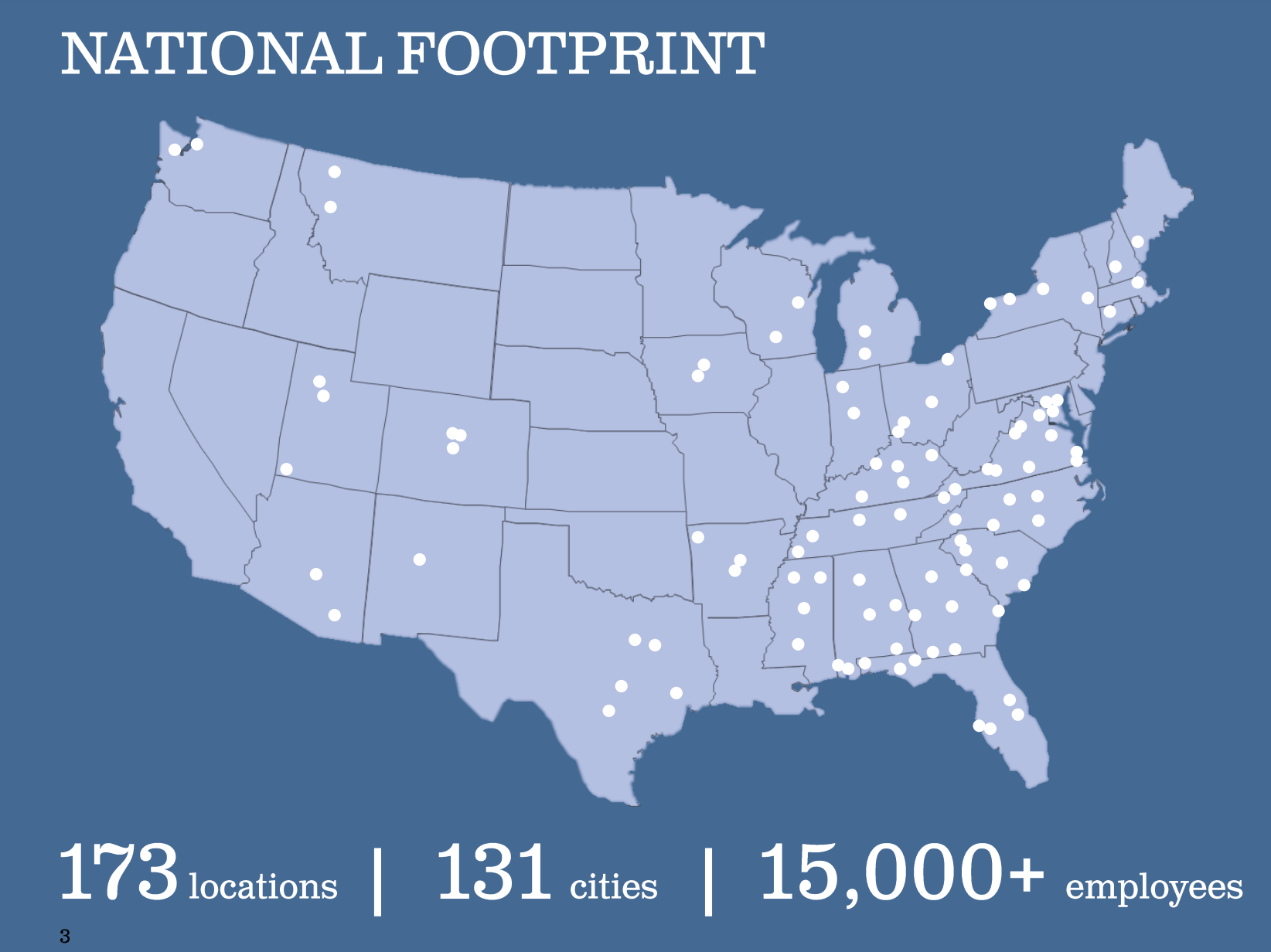

It really is best to think about Comfort Systems USA as two separate sets of operations put together. The bulk of the enterprise is comprised of its Mechanical Services segment, which in 2022 was responsible for 76.8% of the company's overall revenue. The rest of sales, totaling 23.2% in all, came from its Electrical Services segment. The business has grown to be rather large in size, with 173 locations spread across 131 different cities. 43 distinct operating companies throughout the nation oversee these sites with the help of roughly 15,000 employees.

{kind=link}

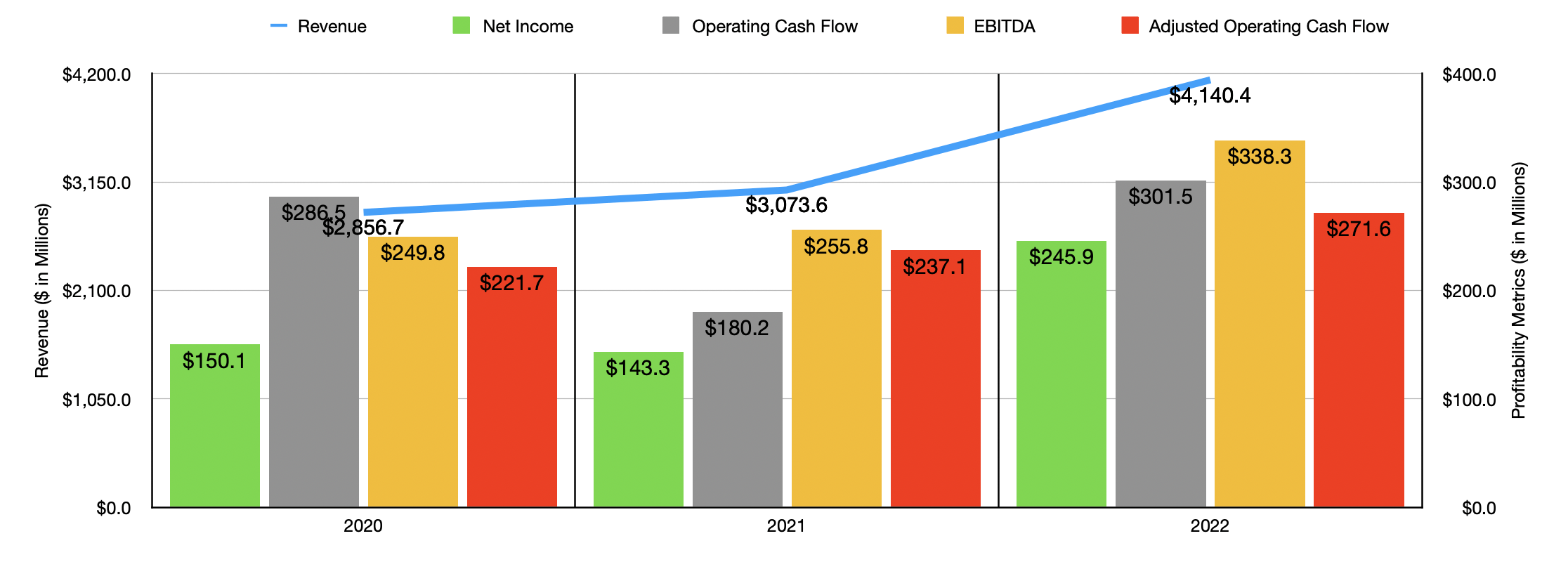

Over the past few years, management has done a great job growing the company. Revenue shot up from $2.86 billion in 2020 to $4.14 billion in 2022. That translates to an annualized growth rate of 20.4%. Truthfully, that's not the kind of growth you would expect from a business in this space. Perhaps unsurprisingly, a good chunk of revenue growth has been driven by acquisition activities. For instance, from 2021 to 2022, revenue under the Mechanical Services segment shot up from $2.54 billion to $3.18 billion. $164.9 million of this increase was attributable to a single acquisition. And that acquisition only brought the company eleven additional months instead of 12 additional months' worth of revenue because of the timing of its closing. Revenue under the Electrical Services segment, meanwhile, nearly doubled from $531 million to $961.9 million. $232.4 million of the $430.9 million increase was driven by 3 acquisitions that the company made.

This is not to say that the company is not growing organically. In fact, under the Mechanical Services segment alone last year, same-store sales growth was a whopping $471 million. The company benefited to the tune of $79.5 million from industrial sector growth seen in North Carolina. Strong demand for its offerings in Texas accounted for $59.1 million of sales growth, while retail establishments, restaurants, and the entertainment sector, all helped to add $35 million in revenue for the unit. The company also benefited from strength in Arizona during the year. For the Electrical Services segment, same-store growth was also strong, totaling $198.5 million, thanks in large part to $172.5 million coming from the industrial sector at its Texas electrical operation.

On the bottom line, the business has also done very well. Over the three-year window covered, net profits jumped from $150.1 million to $245.9 million. Operating cash flow was a bit more volatile, but if we adjust for changes in working capital, it grew consistently over the three years, climbing from $221.7 million to $271.6 million. Meanwhile, EBITDA for the business expanded from $249.8 million to $338.3 million.

{kind=link}

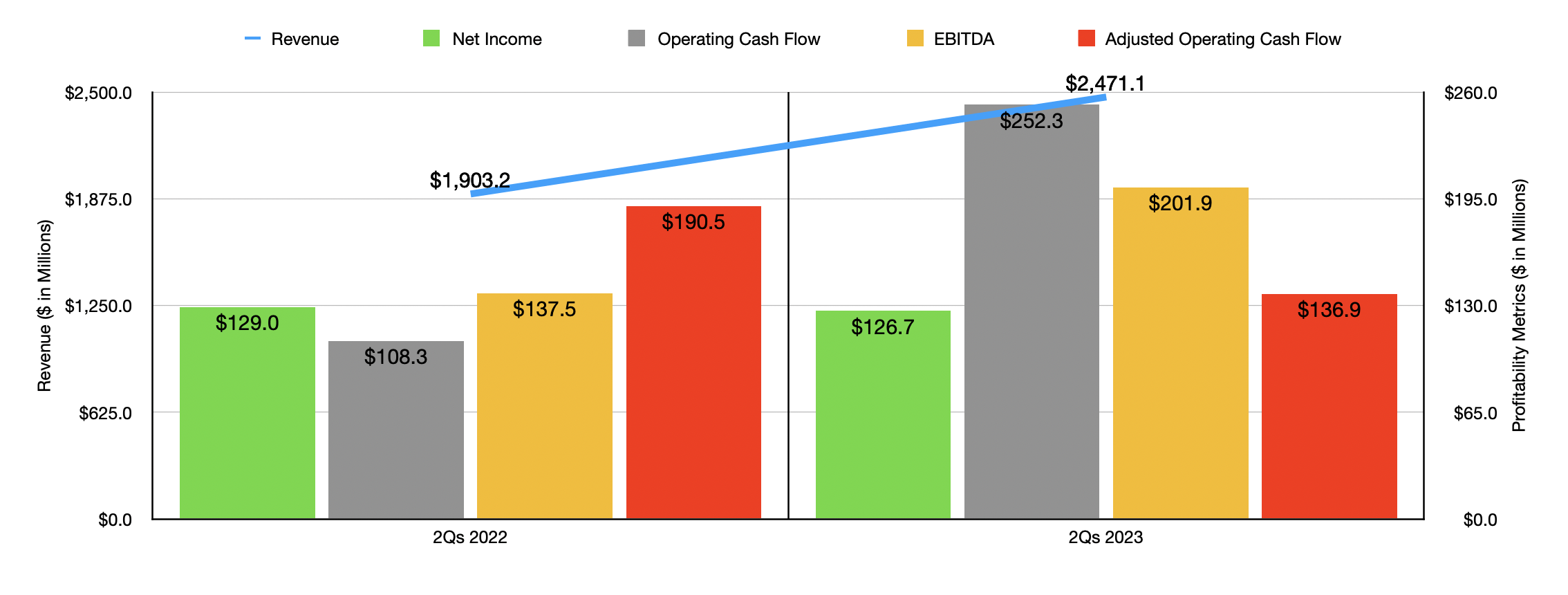

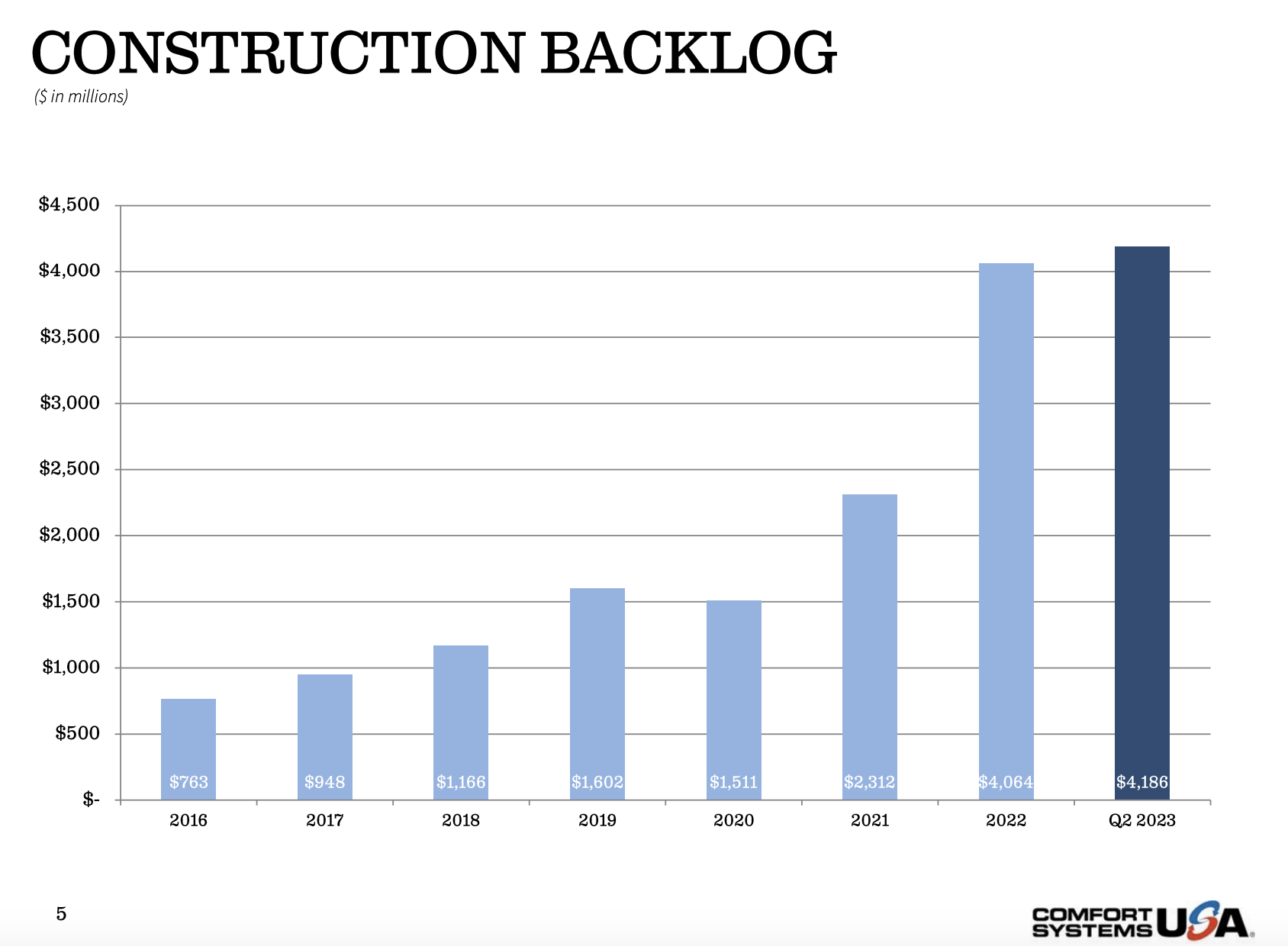

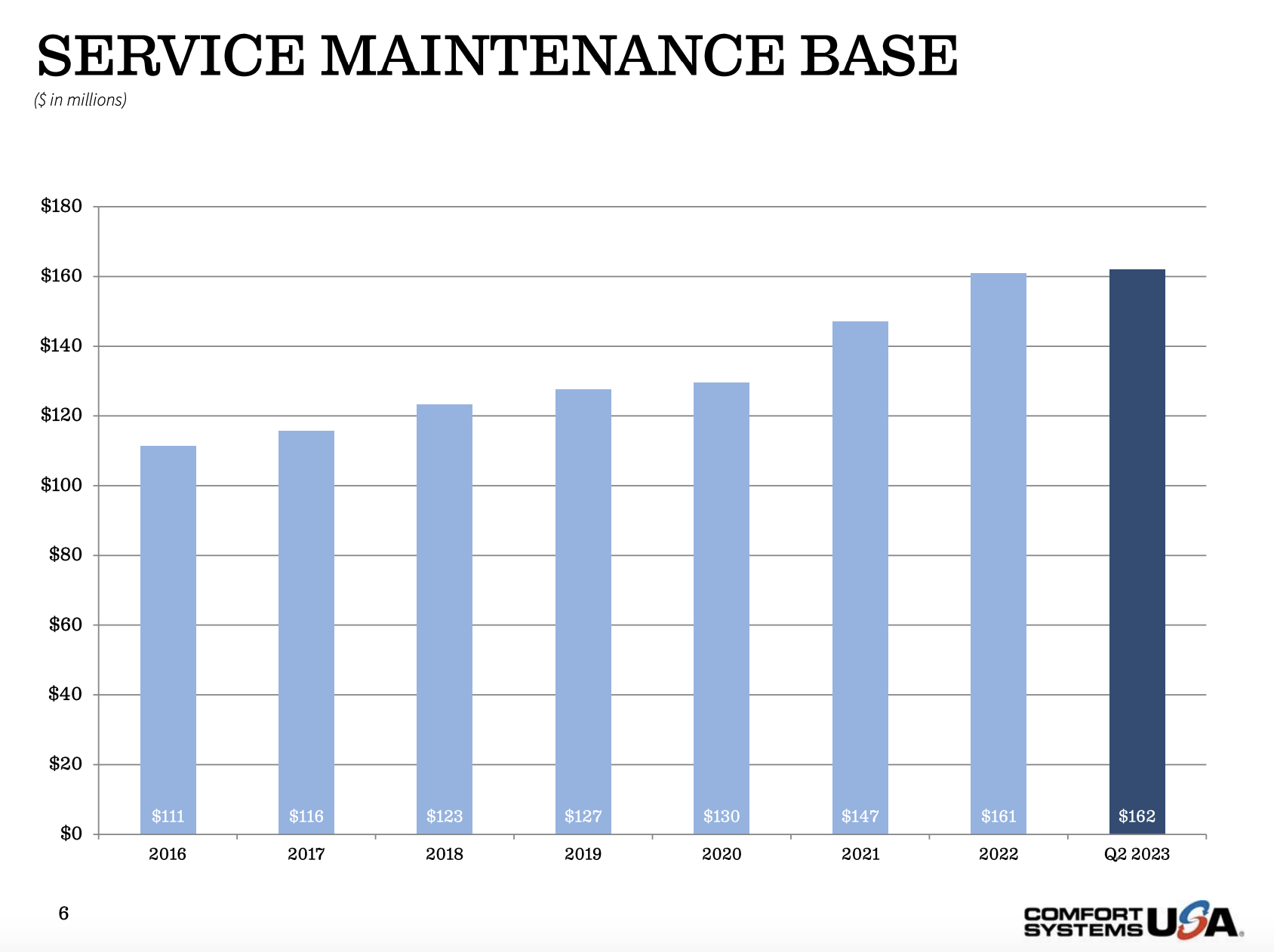

While the past is important, it's more significant for us to look to the future. And the good news for shareholders is that the picture looks good here as well. For starters, as you can see in the chart above, topline growth during the first half of the 2023 fiscal year was rather strong. Sales of $2.47 billion significantly surpassed the $1.90 billion the company generated one year earlier. The great thing about the company is that this growth looks set to continue. As you can see in the first image below, backlog for the company hit $4.19 billion under the construction category in the most recent quarter. That's up from $2.31 billion at the end of 2021. Although nowhere near as significant, the second image below shows a service maintenance base for the company of $162 million as of the most recent quarter. That's up slightly from $161 million at the end of 2022, and it stacks up nicely against the $147 million reported for the end of 2021.

Comfort Systems USA Comfort Systems USA

{kind=link}

{kind=link}

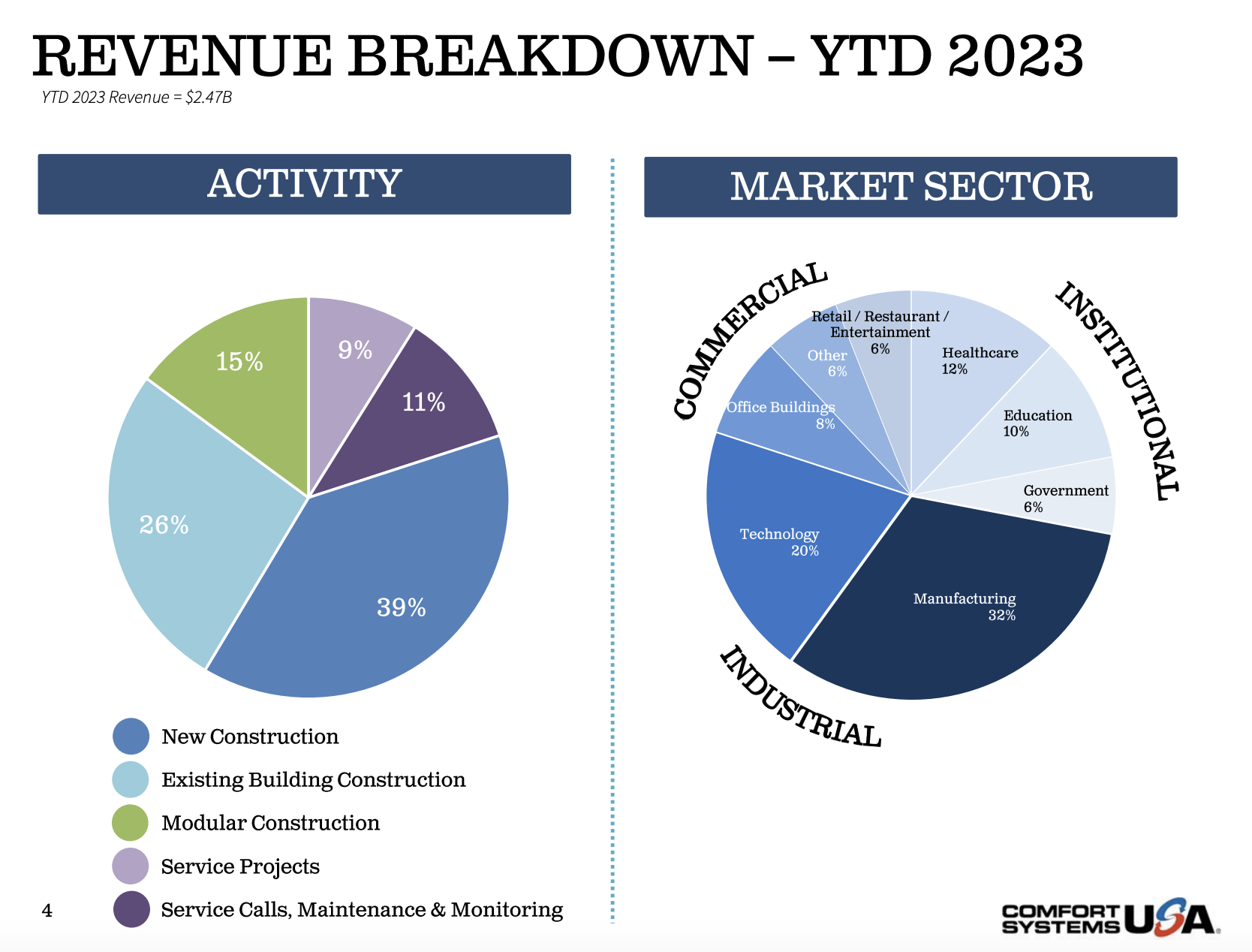

Of course, some investors or market participants might be concerned about the broader economy. Management even said in their annual report that they were thinking about the prospect of a recession in the not-too-distant future. What might be particularly alarming is the fact that 39% of the company's revenue so far this year has been attributable to new construction projects, while 15% has been chalked up to modular construction activities. In the event of a true recession, you would expect a reduction in spending. But the good news is that the company is very diverse in terms of the market sectors it's exposed to. Yes, 32% of its revenue is attributable to the manufacturing space. Another 8% involves office buildings, a category that has many investors concerned because of high vacancy rates across the country. However, the company also benefits from 20% of its exposure falling under the technology category. Health care is another hot item at 12%. Government comes in at 6%, and we can all rely on the government to keep spending no matter what the economy does. And another 10% falls under the education category, which likely also includes public funds. This provides a nice balance that should help the company in the event of a broader economic downturn.

{kind=link}

The bottom line, however, was challenged to some extent. By looking at these numbers only, you end up with a distorted outlook. For instance, when it comes to net income, the decline from $129 million to $126.7 million completely overlooks the fact that the company had a tax bill of $24.3 million in the first half of 2023. This compares to a $37.8 million tax benefit that it booked at the same time one year earlier. That's a swing of $62.1 million from one year to the next. You see the same kind of thing pop up in cash flow. Operating cash flow was hit to the tune of $55.3 million from a deferred tax provision in the first half of this year. That compares to a $6.3 million benefit reported at the same time one year earlier.

After making a few adjustments, I estimated that adjusted net profits this year should probably be around $407.1 million. I'm not as confident in the adjusted operating cash flow reading that I got of $283.4 million. If earnings are where I expect them to be, I would imagine that this metric would be higher than what I forecasted. But the numbers that I forecasted are the best good faith effort that I can offer. Meanwhile, my forecast for EBITDA is a reading of $496.7 million.

{kind=link}

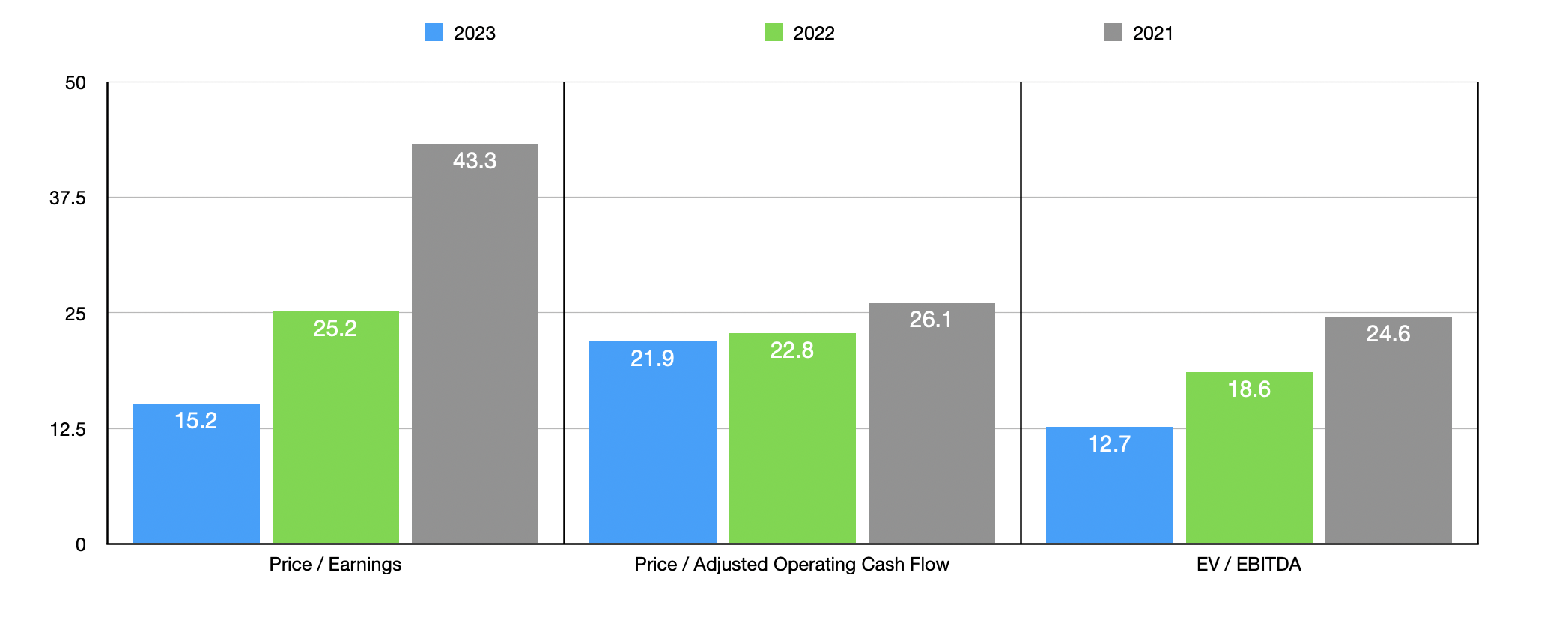

Using these figures, we can easily value the company. In the chart above, you can see how shares are priced on a forward basis for 2023 compared to how shares are priced using data from both 2021 and 2022. Although the price to operating cash flow multiple still makes the stock look pricey, both the price to earnings and EV to EBITDA multiples make it look more attractive. Even if we ignore this forward analysis, I would say that shares look no worse than fairly valued when stacked up against similar firms. In the table below, I took the 2022 figures for the enterprise and compared them to five similar firms. On a price to earnings basis, two of the five companies were cheaper than Comfort Systems USA. Using the price to operating cash flow approach, this increases to three of the firms, while the EV to EBITDA approach results in four of the five companies being cheaper than our prospect. Of course, if we use the forward estimates, the picture does change some. The stock becomes the cheapest of the group using the price to earnings approach and the second cheapest using the EV to EBITDA approach. When it comes to the price to operating cash flow approach, it maintains its ranking.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Comfort Systems USA |

| 25.2 |

| 22.8 |

| 18.6 |

| APi Group ( APG ) |

| 138.8 |

| 20.1 |

| 16.6 |

| Valmont Industries ( VMI ) |

| 20.5 |

| 15.5 |

| 11.6 |

| Stantec ( STN ) |

| 37.0 |

| 27.8 |

| 17.4 |

| Watsco ( WSO ) |

| 25.0 |

| 21.6 |

| 17.8 |

| AAON, Inc. ( AAON ) |

| 48.6 |

| 79.4 |

| 30.9 |

Takeaway

Based on all the data I see, it looks as though Comfort Systems USA is doing a really solid job. Management continues to grow the company both through organic growth and acquisitions. I must emphasize the word 'continues' because management continues to make acquisitions. In February of this year, for instance, the company announced the purchase of a company called Eldeco that should generate annualized revenue for it of between $130 million and $140 million. These small bolt-on acquisitions should add value as time goes on. Yes, shares of the business do look pricey through the lens of the 2022 fiscal year. But given the performance achieved so far in 2023, the stock looks quite affordable. I definitely wouldn't say that this is a company that will go on to make you rich. But for somebody who's interested in this space and who craves growth, this is definitely a candidate to consider.

For further details see:

Comfort Systems USA: Growth At A Reasonable Price