CRZBF - Commerzbank: Cheap For A Reason

2023-06-23 21:32:32 ET

Summary

- Commerzbank has one of the lowest valuations in the European banking sector due to structural issues and weak profitability levels.

- Despite restructuring efforts and recent improvements in financial performance, Commerzbank still lags behind its peers in efficiency and profitability.

- The bank's shares trade at a significant discount to the sector average, but this is justified by its structural woes, making it a less attractive long-term investment.

Commerzbank ( CRZBF ) ( CRZBY ) has one of the lowest valuations across the European banking sector, but this is justified by the bank’s structural woes that aren’t easy to fix.

Company Overview

Commerzbank is a German bank, being the second-largest private banking institution in the country. At the end of last March, it had close to €500 billion in assets, being by this measured a mid-sized bank in Europe. Its operations are mainly focused on the German and Polish banking markets, being highly geared to retail and commercial banking. Its current market value is about $14 billion and trades in the U.S. on the over-the-counter market.

Its largest shareholder remains the German state with a stake of 15.6%, which was built after the global financial crisis of 2008-09, when Commerzbank had to receive public money to stay afloat. While the German government eventually wants to dispose of this stake, Commerzbank’s share price remains below the State’s breakeven price (around €17 per share), thus it’s likely to remain the bank’s largest shareholder for some more time.

Including its Polish subsidiary, Commerzbank serves nowadays more than 16 million small and private business customers, plus around 28,000 corporate customers in around 40 countries. Its business is segmented across two main units, namely the Private and Small-Business Customers and the Corporate Clients units.

Commerzbank has been a bank in constant transformation over the past decade, having downsized considerably its operations and de-risked its balance sheet. However, it remains one of the European banks with weaker profitability levels, a profile that is justified in large part by the structure of the German banking sector.

Indeed, the country’s banking industry is characterized by a relatively low level of concentration, low market share controlled by listed banks, including both Commerzbank and Deutsche Bank ( DB ), and significant public involvement, especially among the public banks segment. Moreover, labor laws in the country are also unfavorable for employers, making large redundancies difficult to do. This leads to structural low margins and poor efficiency levels among the German banking sector, of which Commerzbank is no exception.

The bank has developed several restructuring programs to improve its fundamentals over the past few years, but a large part of its woes come from its large exposure to the domestic market, which is not expected to change its profile in a meaningful way over the medium term.

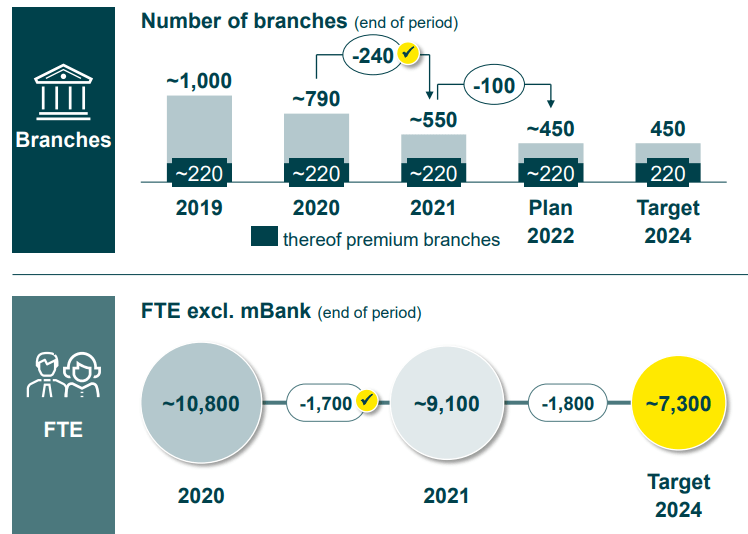

Its previous restructuring plans were focused mainly on reducing the bank’s size and simplifying its structure, reducing its branch network and staff numbers. It also reduced some risky activities within its capital markets unit, while investing in digitalization to improve its customer service and reduce costs across its operating units.

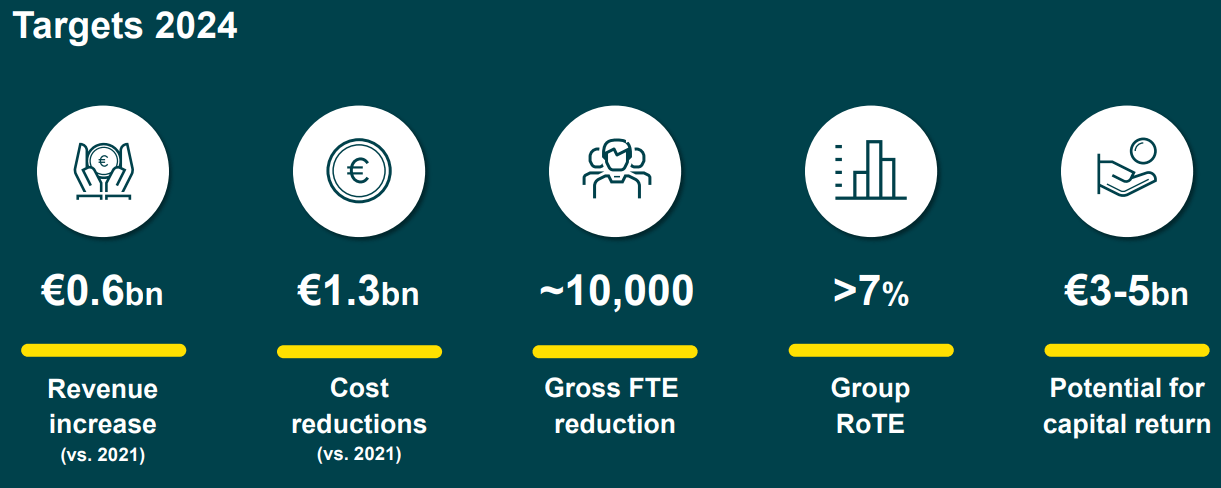

Its most recent business strategy was presented in March 2022, maintaining a focus on improving customer service, increasing digital penetration among its customer base, reducing headcount, and achieving higher profitability in the coming years. However, its return on tangible equity (RoTE) ratio target is only to be above 7% by 2024, which is below the European banking sector average, and shows that Commerzbank’s profitability level is expected to remain quite muted in the near future.

{kind=link}

Financial Overview

Regarding its financial performance, while Commerzbank reported weak results for many years, this has changed more recently due to rising rates in Europe. As the bank has changed its business profile toward retail and commercial banking in recent years, it’s nowadays somewhat geared to interest rates, which have been a good tailwind for higher revenues and earnings in recent quarters.

In 2022 , its revenues amounted to €9.4 billion, an increase of 12% YoY, boosted by rising rates. Its net interest income ((NII)) was up 36% YoY to €6.3 billion, which means NII represents some 67% of total revenues, a relatively high weight on total revenues compared to its European peers. On the other hand, Commerzbank reported a small decrease in fee income and its trading result was also lower due to weak capital markets during the past year.

On the cost side, Commerzbank has done a good job reducing operating expenses, through staff reduction and optimization of its sales channels, which led to lower operating expenses in the year. However, higher compulsory contributions related to regulatory commitments led to total costs of close to €6.5 billion, a decrease of 3.2% YoY.

Its cost-to-income ratio, a key measure of efficiency within the banking sector, was 68.6% in 2022 (vs. 79% in 2021), still a poor level compared to the most efficient banks in Europe that have cost-to-income ratios between 40-45%. This shows that Commerzbank has a structural issue regarding efficiency despite its efforts in recent years to reduce its number of branches and overhead numbers, as shown in the next graph.

{kind=link}

Even though Commerzbank still aims to further reduce its number of employees to save costs, its target is only to have a cost-to-income ratio of 61% by 2024, not particularly a great level. However, this target was set without considering rising rates compared to 2021, thus there is room to achieve better efficiency than expected over the next couple of years, if interest rates remain at relatively high levels during the next eighteen months.

Regarding asset quality, while provisions remained at relatively low levels in Germany, the bank reported again significant provisions in Poland related to CHF mortgage loans. The bank increased provisions related to this issue by €650 million, bringing its total provisions to some €1.6 billion. Its total CHF loan portfolio is about €2.5 billion, thus Commerzbank has a good coverage related to this issue, but further losses aren’t ruled out in the coming quarters as customers go to court on an individual basis, which can take some time to resolve given that Commerzbank has thousands of customers in this situation.

This was the most relevant headwind for the bank’s bottom-line last year, which despite being hit by higher provisions, still increased to more than €1.4 billion (vs. €430 million in 2021) and its RoTE ratio increased to 4.9% (compared to just 1% in the previous year).

During the first three months of 2023, the bank maintained a good operating momentum, supported by rising rates in Europe. However, its total revenues were slightly lower because Commerzbank included CHF loan provisions as ‘other income’ in its P&L statement, instead of considering it on ‘risk result’, which is not the best way to report this issue in my opinion.

Without considering CHF provisions as part of revenues, the bank’s ‘underlying revenues’ increased in Q1 due to higher NII (€1.95 billion vs. €1.36 billion in Q1 2022), while commissions and trading results remained weak and reported a decrease compared to the same quarter of the previous year.

On the cost side, the bank reported a small increase in total expenses to €1.46 billion, leading to a cost-to-income ratio of 65%. Its risk result was €-68 million, a significant improvement from Q1 2022, due to lower provisions related to its Russia exposure. Its net profit was €580 million in Q1, an increase of 23% YoY, and its RoTE ratio was 8.7%.

While most of its key financial targets are progressing well and Commerzbank’s is likely to reach its 2023 guidance, Commerzbank still remains below average regarding both efficiency and profitability, as the effect of rising rates is a tailwind for the whole sector.

Indeed, according to analysts’ estimates , its revenues and earnings growth should be strong in 2023, but moderate considerably in the following years as the market is currently expecting the European Central Bank to reach its peak rate by the next few months. This shows that without the tailwind from higher rates, Commerzbank’s growth prospects aren’t great and are likely to reach peak earnings during the next couple of years.

Regarding its capital position, its CET1 ratio was 14.2% at the end of last March, a comfortable position that is within the European banking sector average. This capital position allows the bank to distribute a good part of its earnings to shareholders, both through dividends and share buybacks .

Related to 2022 earnings, its total payout ratio was 30%, but Commerzbank’s goal is to increase the payout to about 50% in 2023, and probably maintain at this level going forward.

{kind=link}

Its last annual dividend was €0.20 per share, resuming annual payments after a hiatus of some years, as the bank suspended dividend payments in 2020 due to the pandemic and didn’t resume payments until this year (related to 2022 earnings). At its current share price, its dividend yield is less than 2%, much lower than compared to most of its peers.

Conclusion

Commerzbank is one of the European banks with weaker fundamentals, a profile that is not easy to change despite the bank’s efforts to turnaround its business over the past decade. Reflecting this profile, its shares are also among the cheapest in the European banking sector, trading at some 0.46x book value and at a significant discount to the sector’s average (0.8x book value), but this seems to be justified by the bank’s structural woes and therefore Commerzbank is not a good long-term play within the European banking sector.

For further details see:

Commerzbank: Cheap For A Reason