TDS - Commvault Systems: An Unfortunate Surprise Has Not Pushed Shares Down Enough Yet

Summary

- Commvault Systems took a tumble after announcing preliminary financial results covering the third quarter of the company's 2022 fiscal year.

- The results showed weakness across most metrics and harmed investor sentiment for the firm.

- Some may view this as a good opportunity to buy, but CVLT shares aren't cheap enough yet.

In this modern era, data is perhaps the most valuable resource with the exception of time. Utilizing data, you can make vital decisions that have significant impacts on business outcomes. Data also needs to be protected and stored because of how sensitive it can be to the parties involved. One company dedicated to providing various data management solutions is Commvault Systems ( CVLT ). Normally, this is a healthy and fast-growing space for investors to buy into. But shares of the company plunged 14.3% on January 11th after management released preliminary financial results covering the third quarter of the company's 2022 fiscal year. On top of this, with how shares are currently priced, I believe that there are better prospects on the market for investors to consider.

Commvault Systems - A data-centric firm

As I mentioned already, Commvault Systems operates is a data management solutions firm that aims to help the organizations it services securely manage their data in the most cost-effective and simplistic ways possible. The company does this in a manner that creates an intuitive data management experience across customer-managed enterprise software and SaaS-delivered cloud-native solutions that serves to bring data together, facilitate cloud adoption, and provide customers with a modernized and efficient IT environment. To really understand the company though, we should break its operations up into the three categories of offerings that it provides.

The first of these is referred to as Data Protection. The company achieves this through its Commvault Backup and Recovery offering. This particular service provides backup, verifiable recovery, and cost-optimized cloud workload mobility to its customers to make sure that data is available when and where it's needed. This includes across multiple clouds. Under this same umbrella is the Commvault Disaster Recovery service that provides replication and disaster recovery solutions for its customers. There is also the Commvault Complete Data Protection offering that operates as a comprehensive data protection solution that combines both of the aforementioned products.

Next in line, we have the Data Insights category. This includes a portfolio of solutions That combines the company's Commvault Data Governance, Commvault File Storage Optimization, and Commvault eDiscovery and Compliance Products all with the end goal of being able to offer customers actionable insights from the data that they gather. And finally, we have the Data Storage category. This consists of a few different services, the first of which worth mentioning is called Hyperscale X. This particular offering focuses on providing scalability, security, and resiliency in order to accelerate an organization's digital transformation journey as they move from one environment to another, such as to a hybrid cloud environment. The Commvault Distributed Storage offering stores, protects, and replicates data across private and public cloud data centers and even its own internal technology. And there is also the Metallic Cloud Storage Service provides customers with integrated cloud storage when needed. The company also offers a variety of professional services to its customers like real-time support, technology consulting services, education services, and more.

{kind=link}

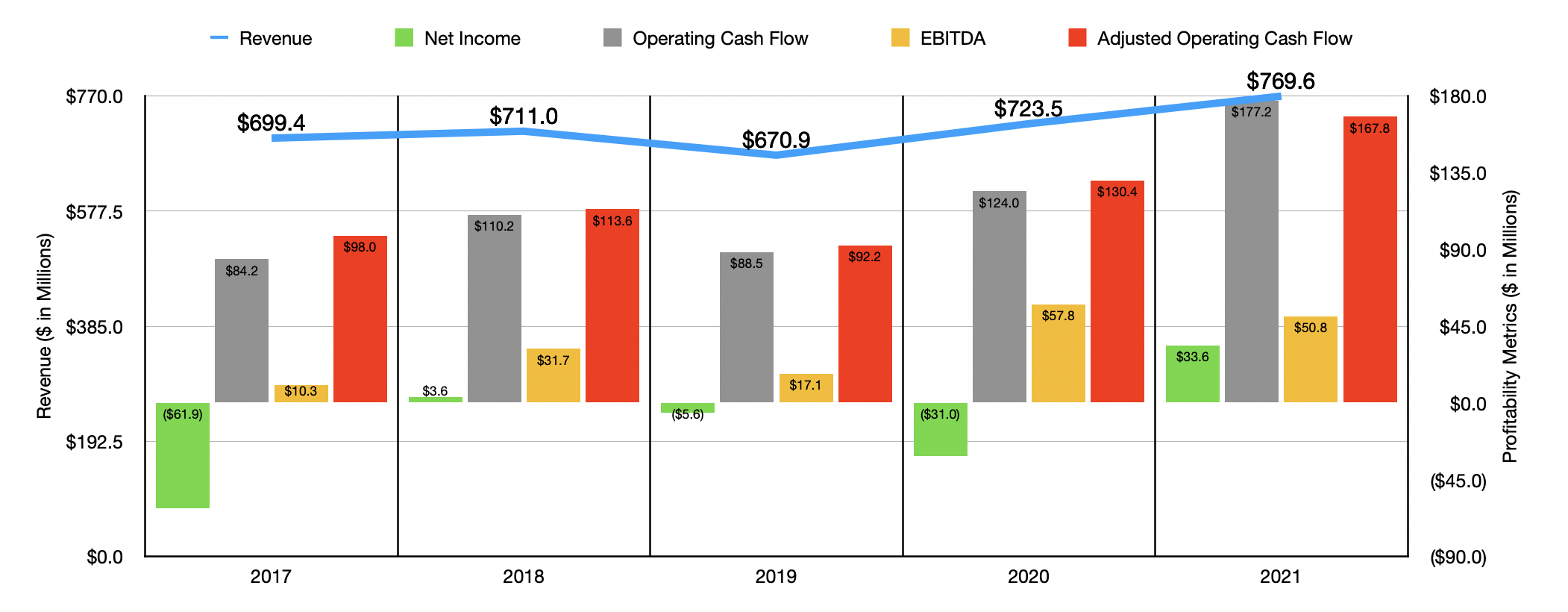

From my financial perspective, the general trajectory that Commvault Systems has been on in recent years has been positive. Between 2017 and 2021, revenue rose in all but one year, eventually climbing from $699.4 million to $769.6 million. From 2020 to 2021, the sales increase for the company occurred across both of the company's largest revenue categories. For the software and products category, sales rose by roughly 9%, with larger deal transactions contributing $30 million to upside services revenue, meanwhile, increased a more modest 4%, rising because of an increase in demand for the company's professional services and software-as-a-service offerings.

Unfortunately, bottom line results for the company have been quite mixed in recent years. Over the five-year window covered, net income has bounced around, with a low point of negative $61.9 million and a high point, that was achieved in 2021, of $33.6 million. Operating cash flow has been more consistent. After rising from $84.2 million in 2017 to $110.2 million in 2018, it dropped to $88.5 million in 2019. Since then, it has been on a constant upswing, hitting $177.2 million in 2021. If we adjust for changes in working capital, we would see a similar trend, with the metric ultimately hitting $167.8 million in 2021. And finally, EBITDA for the company has mostly risen in recent years. In 2017, it totaled only $10.3 million. After peaking at $57.8 million in 2020, it pulled back slightly to $50.8 million in 2021. It is worth noting that investors might point out that there is a significant disparity between operating cash flow and EBITDA. When such a large disparity exists, it's often that EBITDA is the higher of the two because of interest expense. But the fact of the matter is that Commvault Systems has cash and cash equivalents of $273.5 million, with no debt on its books. The big disparity actually has to do with stock-based compensation. Since this is a non-cash item, it gets added back to operating cash flow but not to EBITDA. A case could be made that because it is non-cash, it should be added back to EBITDA in order to more accurately reflect cash flows. On the other hand, a case could also be made that if the company was not incurring that much in stock-based compensation, that it would have to pay employees using actual cash instead. As a compromise, for the purpose of valuing the company, I looked at both scenarios.

{kind=link}

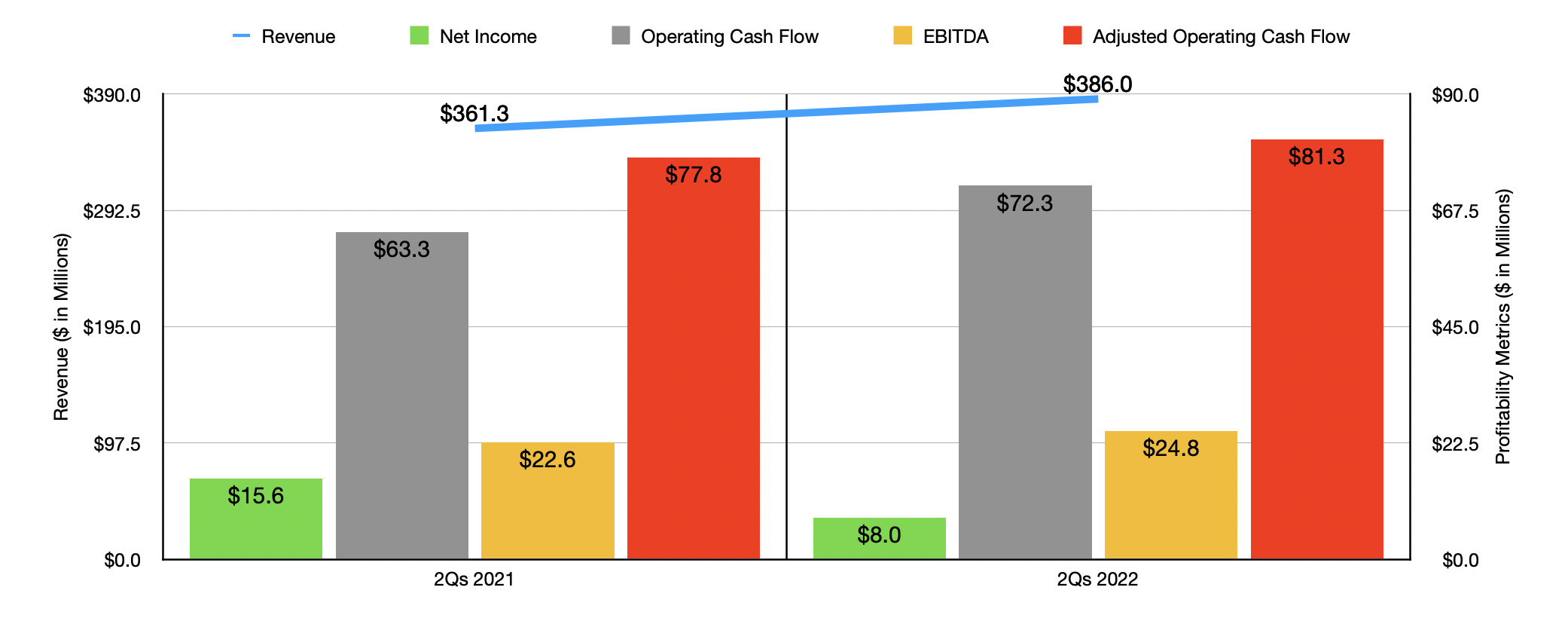

For the 2022 fiscal year, the picture for the company has been somewhat mixed but mostly positive. Revenue of $386 million in the first two quarters of 2022 represented an improvement over the $361.3 million reported one year earlier. On the other hand, net income fell from $15.6 million to only $8 million over the past year. Fortunately, this was the only profitability metric that worsened year over year. Operating cash flow went from $63.3 million to $72.3 million, while the adjusted figure for this went from $77.8 million to $81.3 million. And finally, EBITDA for the company went from $22.6 million to $24.8 million.

Commvault Systems

{kind=link}

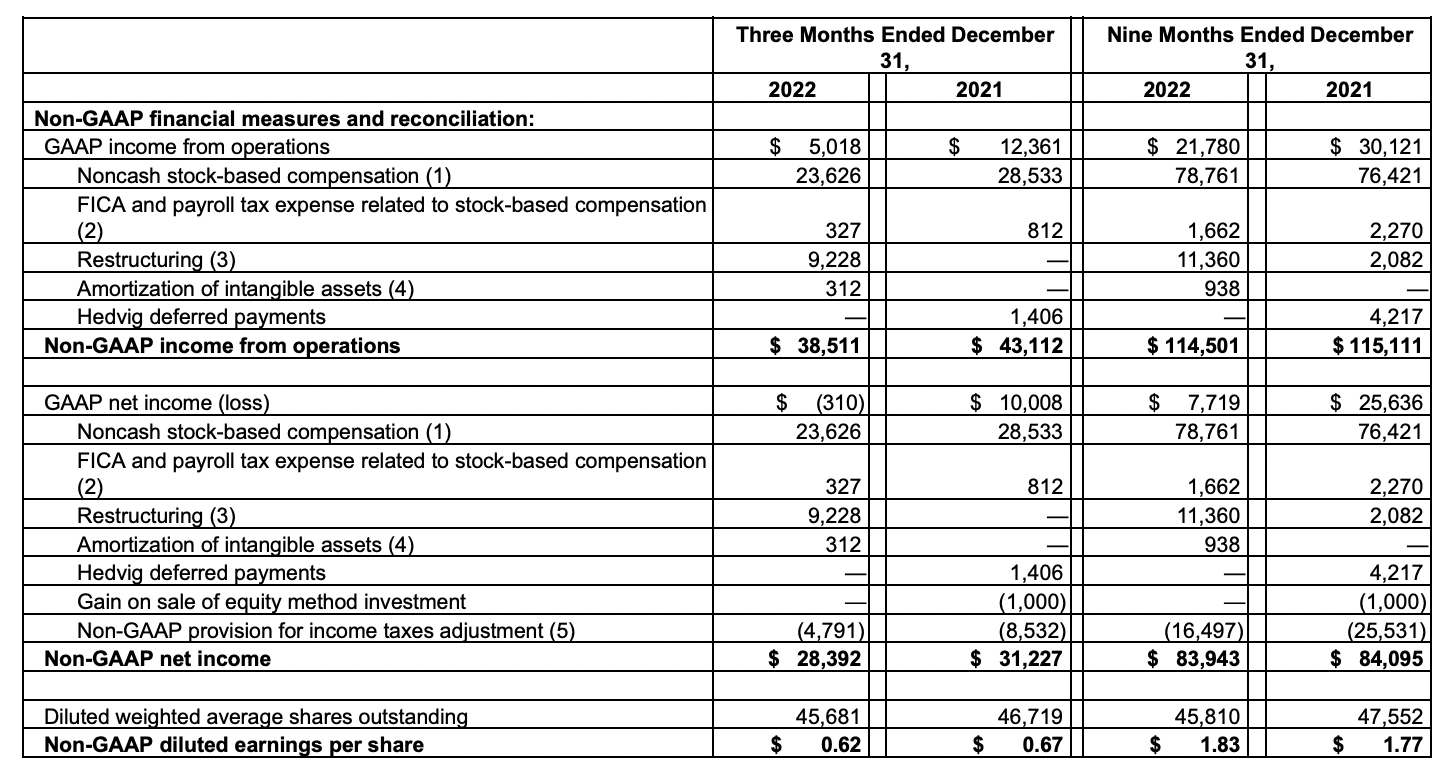

What really got investors frustrated on January 11th was the fact that the company announced some disappointing preliminary results for the third quarter of its 2022 fiscal year. Sales, for instance, were previously forecasted by management to come in and between $202 million and $205 million. Analysts were anticipating a reading of $204 million. Unfortunately, the company reported sales of only $195.1 million. That's down from the $202.3 million reported one year earlier. Although this 4% decline looks horrible, it is worth noting that on a constant-currency basis sales actually inched up by 1%. The company also said that ARR (annualized recurring revenue) Totaled $641 million as of the end of 2022. That was up 14% year over year, with constant currency revenue growth totaling 18%. But the company unfortunately had to struggle with customers and prospects dealing with an uncertain economic outlook that resulted in slower-than-expected buying patterns and close rate execution. Net income also is expected to have come in negative to the tune of $0.3 million. That's down from the $10 million reported for the third quarter of 2021. On an adjusted basis, earnings totaled $0.62 per share compared to the $0.65 that analysts were expecting. And finally, operating cash flow should be $30.2 million. That's the only positive in this seeing as how it represents an increase over the $26.8 million reported the same time one year earlier. While it's great to see this cash flow figure improved, another cash flow figure, non-GAAP EBIT came in at $38.5 million. That's down from the $43.1 million experienced one year earlier. The disparity between it and operating cash flow had to do with an increase in deferred revenue growth that the company saw in the third quarter.

{kind=link}

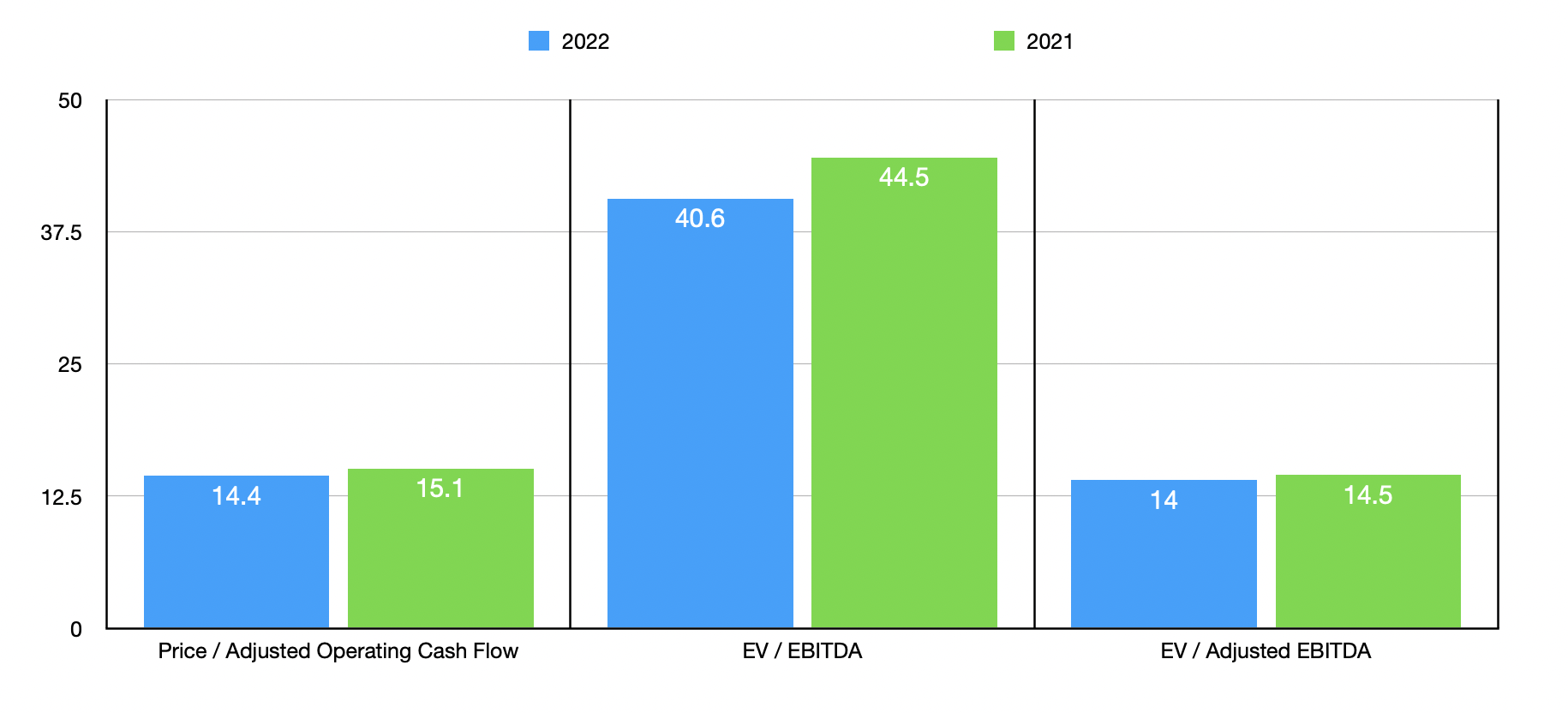

We don't really know what to expect for the rest of 2022. But if we annualize results experienced so far, we should anticipate adjusted operating cash flow of $175.3 million and EBITDA of $55.7 million. Based on these figures, the company is trading at a forward price to adjusted operating cash flow multiple of 14.4 and a forward EV to EBITDA multiple of 40.6. The EV to EBITDA multiple drops to a much more reasonable 14 if we add stock-based compensation back into the equation. As you can see in the chart above, these numbers are a bit lower than if we were to use data from 2021. As part of my analysis, I also compared the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 9.3 to a high of 308.9. Using the EV to EBITDA approach, the four companies with positive results ranged from a low of 12.6 to a high of 153.3. In both of these scenarios, three of the companies were cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Commvault Systems |

| 14.4 |

| 40.6 |

| Varonis Systems ( VRNS ) |

| 308.9 |

| N/A |

| Teradata (TDC) |

| 9.3 |

| 12.6 |

| Progress Software Corp. ( PRGS ) |

| 12.0 |

| 13.7 |

| Check Point Software Technologies ( CHKP ) |

| 13.8 |

| 15.4 |

| KnowBe4 ( KNBE ) |

| 44.2 |

| 153.3 |

Takeaway

Historically speaking, Commvault Systems has been a fairly solid enterprise. But as the preliminary results released by management showed, there is some weakness facing the firm. Frankly, I find this a bit surprising given that I would have imagined that data-centric companies would be more resilient in this kind of environment. But the situation is what it is. As for whether or not the company makes sense to buy into, I would say that it is a decent firm but far from being a prime prospect. Shares are not cheap enough to warrant a value moniker. And until we see a consistent return to growth with improving cash flows, it's likely that investors can find better opportunities out there. Because of all of these factors, I feel comfortable rating the company a 'hold' at this time.

For further details see:

Commvault Systems: An Unfortunate Surprise Has Not Pushed Shares Down Enough Yet