CHDRF - Compagnie Financière Richemont: Overcorrection On Increased Uncertainty

2023-09-29 08:12:30 ET

Summary

- Richemont's stock has fallen by 26.6% since June, underperforming other luxury stocks.

- Factors contributing to the decline include higher volatility, concerns about demand, and a reduced outlook.

- Despite the risks, the author believes that Richemont's stock has overcorrected and sees potential for an upswing in the luxury sector.

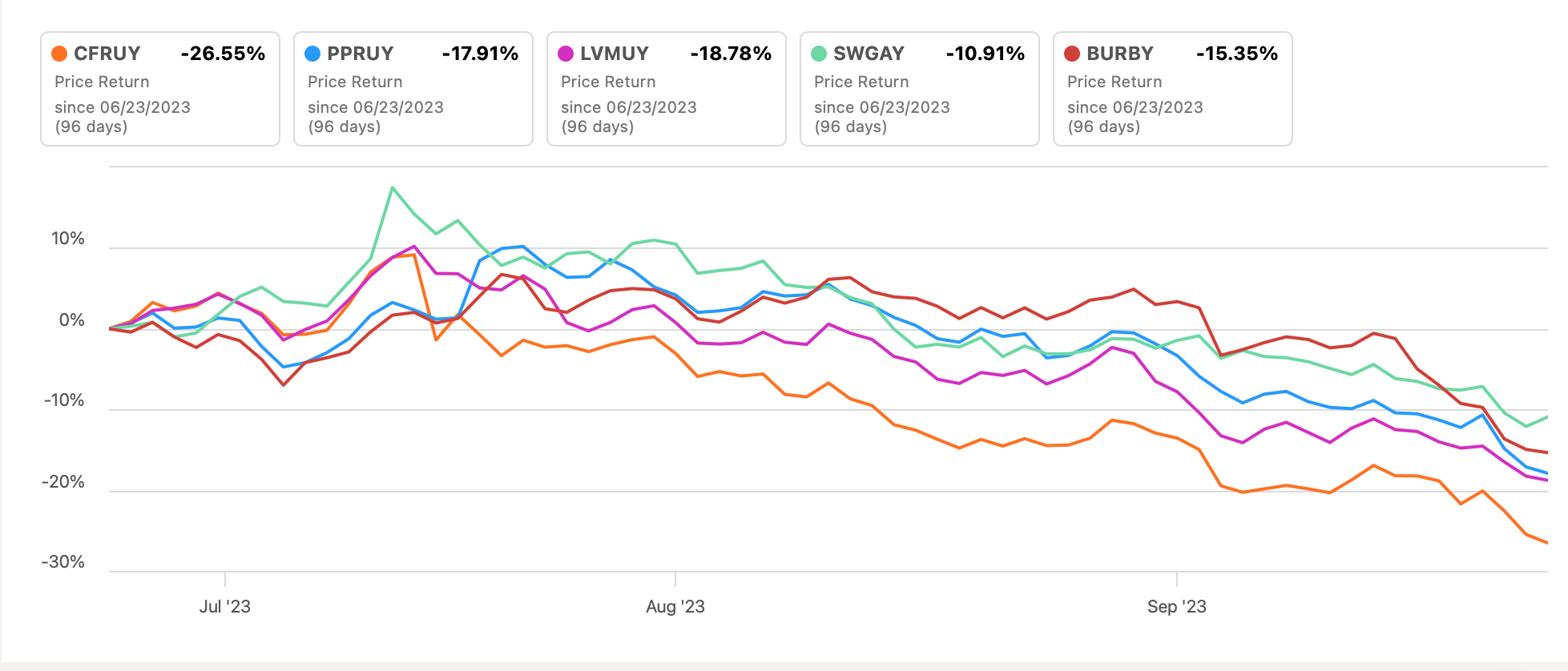

Since the last time I wrote about the Swiss luxury jewellery and watchmaker Compagnie Financière Richemont (CFRHF) in June, its price has fallen by 26.3%, which flies in the face of my Buy rating on it. This of course is mirrored in the performance of the Cartier owner's ADRs (CFRUY) as well. This is a significant decline in itself. If the price had remained unchanged since, its one-year returns would have been north of 60%, compared to 22% now. But it's even more glaring in comparison with other luxury stocks (see chart below).

{kind=link}

While all luxury stocks have declined since June, on account of weakening demand in the US and uncertainties about China's economic prospects, Richemont has performed the worst of the lot. Significantly, its performance is even worse than that for Gucci owner Kering (PPRUY), which has actually reported near stagnant sales and management changes , that really didn't bode well.

Why has the Richemont stock fallen so much?

There are multiple reasons why Richemont has fallen so much, including its inherent attributes, concerns about demand and a reduced outlook.

Higher volatility

Richemont stock or ADRs have a higher volatility as such compared to other luxury stocks. The average beta value for the five biggest luxury stocks by market capitalisation is 1.26. Note that I have eliminated Christian Dior (CHDRF) from this calculation since it's closely related to LVMH (LVMUY), which is already among the set of considered stocks.

Richemont's beta is higher by a margin, at 1.47, compared to the others which are essentially clustered around the average (see chart below). It follows then, that a sentimental change for the sector is likely to impact it more.

Source: Seeking Alpha

Inflation warning

Additionally, it could also have been particularly affected by its Chairman Johann Rupert's recent remarks warning about the impact of inflation even on wealthy customers in Europe. 22% of Richemont's sales were from the region in 2022. While it's nowhere close to the Asia Pacific market, which accounted for 40% of the sales, further weakness in Europe combined with the already shrinking sales in the US are risk factors to consider.

On that very day (September 6) Rupert made the remarks, that the CFRUY dropped by 5.3% and it has fallen by another 8.8% since as investors started losing confidence.

Reduced outlook

Further, the outlook for Richemont has reduced substantially since I last checked. Analysts had expected an 8.9% revenue growth for 2023 then, which is now less than half that at 4% . For my estimates, I've been more optimistic, assuming a revenue growth of 7%, which is the same as the company's 10-year compounded annual growth rate [CAGR].

The assumption is despite the strong growth seen in Q1 FY24 (ending June 30, 2023). The company reported robust sales at a constant currency of 19% year-on-year (YoY). This is higher than the 14% seen for FY23 (ending March 21, 2023) and also shows an acceleration from the 12% sales growth seen in Q1 FY23.

Key Financials (Source: Compagnie Financière Richemont)

{kind=link}

But, at actual exchange rates, sales slowed down to 14% in the latest quarter (Q1 FY23: 20% and FY22: 19%). This is a significant difference from the constant currency growth rate, indicating that even if demand sustains, reported growth can be slower purely because of the exchange rate effect. And going by the company's latest warning, some softening in demand needs to be factored in too, which explains the relatively subdued revenue growth assumption.

Since the company has mentioned inflation, even if only from the consumer's perspective, I've also taken into account a slowing net margin. Here I've considered the margin from continuing operations, which was at 19.6% for the full year 2022. Otherwise, the net margin would be skewed to the downside on a drag from its discontinued operations, after it sold its online sales platform YNAP to Farfetch (FTCH).

I've assumed the margin to be the average of the FY23 and FY22 at 17.1%. This results in an EPS (or, as in this case, earnings per ADR) of USD 0.71 for the full year FY24, an 8.5% decline over the figure for last year, when the number of shares is kept constant at present levels.

What the market multiples say

This results in a forward price-to-earnings (P/E) ratio of 16.9x, which is lower than the 18.7x it was at the last time I checked. It's still higher than the 16.5x as per other analysts' estimates. But it's still competitive compared to peers like LVMUY at 20.7x and Hermès (HESAY) at 42.9.

It is, however, much higher than that for Kering, which has now dropped to abysmal levels of 1.4x on exceptional uncertainty around its near-term future. It's also higher than that for Burberry (BURBY), the next biggest company by market capitalisation for whom forward earnings estimates are available, at 14.8x. Although I believe Burberry is also due an uptick , there are good reasons for a higher premium in that it's a far bigger company by market capitalisation, and has a better historical growth rate as well.

Further, Richemont's trailing twelve months [TTM] P/E at 16.1x is far lower at 22.1x since I last checked and is even lower than its past decade's average of 28.6x . I had last estimated an upside of 25% to CFRUY. I believe that the rise can be even bigger now, despite the possible come-off in its EPS in FY24.

What next?

It's not as if there aren't risks to Richemont. All its key markets can slow down over the remainder of the year. We will know more about how much when it releases its interim report on November 10. But even accounting reasonably for a sales growth decline and lower margins, it has overcorrected considering its market multiples.

Besides higher volatility compared with peers, a warning on its European market and reduced outlook are the likely reasons for this. Moving forward, there could well be further softening based on the current sentiment toward luxury stocks. But I believe that it's only a matter of time before the sector sees an upswing again, even with no improvement in demand conditions. I reiterate a Buy on Richemont.

For further details see:

Compagnie Financière Richemont: Overcorrection On Increased Uncertainty