CNVAF - Companhia Brasileira de Distribuicao: Negative EV With Catalysts On Exito Spinoff With Food Retail Resilience

2023-05-16 07:00:00 ET

Summary

- CBD is exposed mainly to food retail in Brazil but also has e-commerce exposures in France and food retail exposures in other LatAm countries, both through holdings in listed companies.

- Food retail is resilient, moreover, Brazilian inflation is back under control, allowing for dovishness supported by Lula, and finally, CBD has a negative EV valuation by SotP analysis.

- Most importantly, clear catalysts due to an explicit spin-off of shares in Exito could close the negative EV valuation gap soon by providing a dividend in excess of 100% yield.

- The other holding is the non-consolidated Cnova, which is an e-commerce platform in France which we discount by 50%. Still, if it got monetized, it could be another 33% payout.

- The core business is expanding its store footprint, so even without the catalyst, shareholder returns through earnings growth are likely. Resilience at a negative EV valuation with growth potential. Buy.

Published on the Value Lab 05/09/23.

While some might follow Warren Buffett into The Kroger Co. (KR), we focus on a more exciting and deeper-value proposition in terms of valuation in the under-the-radar Companhia Brasileira de Distribuicao ( CBD ). CBD is tradeable as an ADR with $800 million in market cap and several millions in daily USD liquidity.

The idea is clear and simple: on a sum-of-the-parts (SotP) basis, CBD is extremely undervalued when adding up the market-valued holdings in a company called Cnova N.V. ( CNVAF ), a French ecommerce platform that is widely used there, and a company called Almacenes Éxito S.A. ( ALAXL ), which also owns some supermarket, hypermarket and convenience stores in other Latin American countries. CBD's core business is supermarkets, gas stations and convenience stores in Brazil.

Critically, Exito, currently consolidated, is planned to be spun-off into the hands of CBD shareholders. This spinoff will mean that shareholders effectively get a dividend that will yield more than 100% (assuming Exito holds its current market value post spinoff) while leaving plenty of assets still in the CBD operation. If Cnova ever spins off or is monetized and paid out in the same fashion, that event would be another dividend which, if valued at current market cap, would be close to offering a 33% yield to CBD shareholders, while again still leaving the entirety of the 3rd largest Brazilian food retail businesses in CBD's hands.

The widening liquidity post-spinoff is a plausible catalyst for those handed-out Exito shares to appreciate somewhat as well, since it'll be more available for institutions - but the thesis does not require that this happens, in fact even if Exito declined meaningfully once it trades more broadly, CBD would still be a no-brain buy.

At the very least there is downside protection since Brazilian economic conditions aren't bad at all with inflation nearing policy levels again despite five months of paused rate hikes. Decent consumer conditions coupled with the fact that CBD's business is in one of the more resilient sectors of food retail is a great gift for an opportunity that presents this much of a margin of safety from a valuation perspective as well. With CBD also investing substantially in new stores to create scale and leaning into a more premium and perishable strategy that improves their position in the industry structure, earnings growth is high-probability in interaction with the Brazilian economic environment. A negative EV proposition in a food retail business in an advantaged economy based on market-valued holdings or less (requiring almost no assumptions) makes it a no-brain and high conviction buy.

Core Business

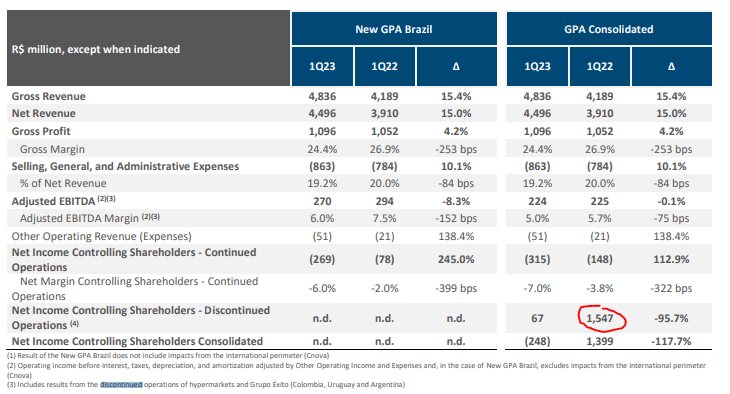

Let's focus first on the core businesses of CBD, which include some supermarket chains, convenience stores, and also retail gas stations, all in a phase of pretty heavy CAPEX and expansion. Below are the most recent quarterly sales data for the core business, which excludes Exito's results since it's slated for spinoff, as well as the hypermarkets business which was its own reported segment and is getting disposed of in parts. The hypermarket business was doing reasonably well, extremely well once COVID-19 hit, and the logic was to move it into non-food retail (electronics, apparel and home appliances) and bolster the ecommerce offering. It was a fine strategy but became most valuable to the company as a discontinued operation being sold in parts to financial and strategic sponsors that wanted infrastructure and facilities in this space. The gains on these disposals have been very meaningful and have offset massive 2022 CAPEX.

Headline Same-store Sales Growth (Q1 2023 PR)

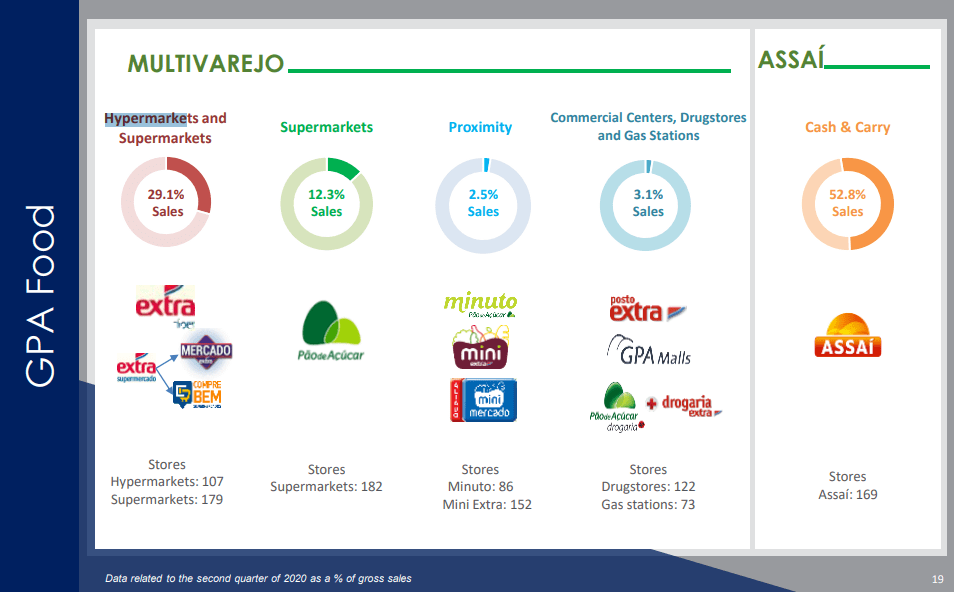

In the typical food retail channels, CBD's core business performed well as the third largest player in Brazil, behind cash and carry player Assai, which also used to be owned by CBD, and Carrefour ( CRRFY ), which is the top player in the market with about 3x the market share of CBD at 20%.

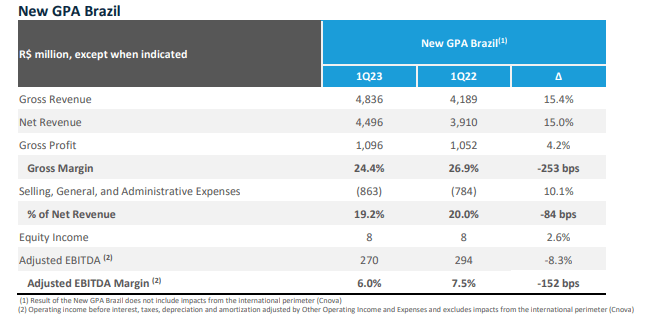

Pao de Acucar is the more premium banner with more pricing power, and it saw very robust 7.5% growth YoY in same store sales. This is important since a lot of incremental growth also came from CAPEX in 2022 and new store openings. Actual revenue obviously grew by more than the same store sales figure, which indicates very resilient food retail markets in Brazil despite double-digit interest rates and general inflation.

{kind=link}

Sales Growth (Q1 2023 PR)

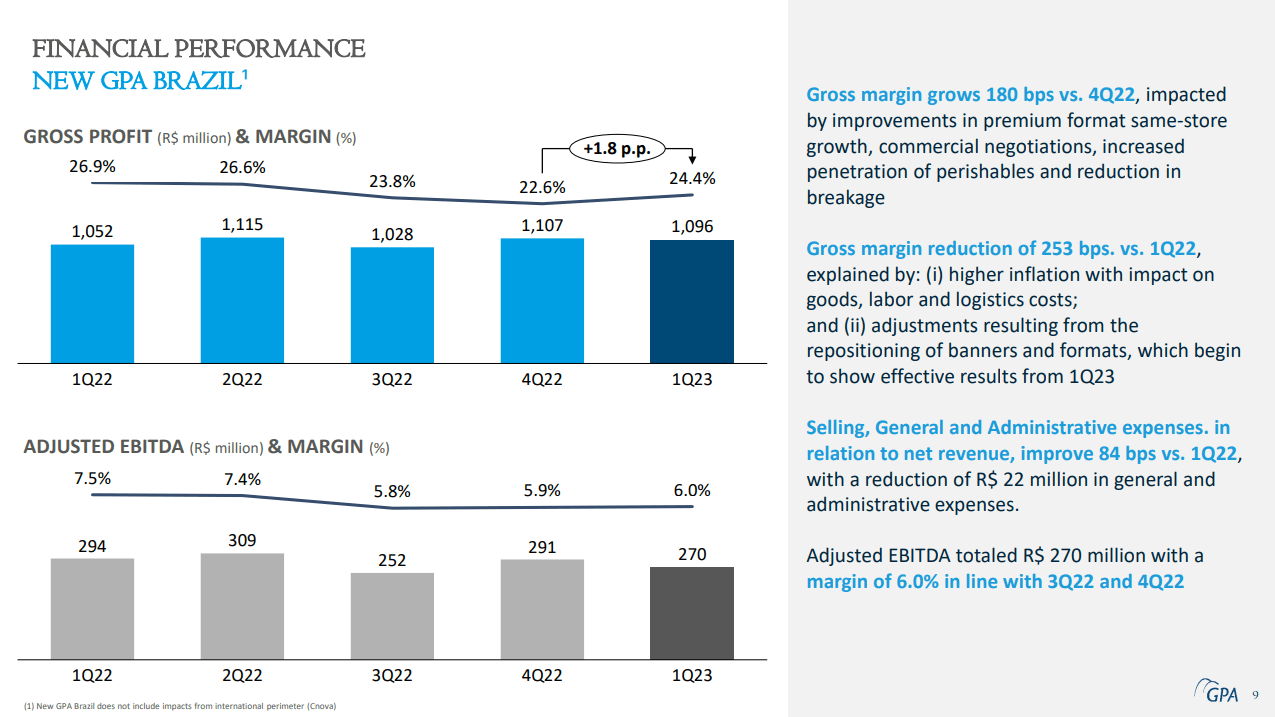

CAPEX (financed by the hypermarket exits) has been focused on this business in order to continue to premiumize this supermarket banner with more stores, able to house more perishables businesses like butcheries, highlighting domestic produce which has been less inflated by logistics and energy prices and are sourced from partners with less bargaining power. Moreover, the focus on perishables and rotisseries and other supermarket initiatives that focus on non-ecommerce experiences are well-timed with the virtual end of the pandemic, although e-commerce (which already has ~10% penetration) GMV also grew by 7% and benefited from the sales focus on perishables. Indeed, premium customers, who spend on average 4x times more, grew by 10% in the return to normal with incremental profit contributions looking promising from the more premium segments.

{kind=link}

Investments in FY 2022 (FY 2022 PR)

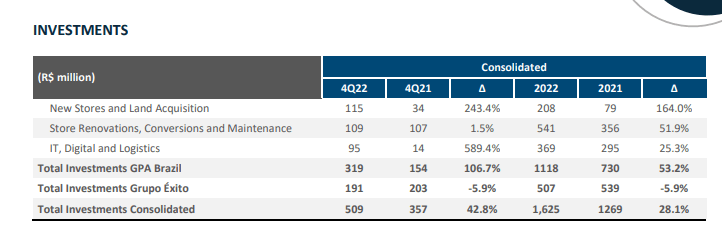

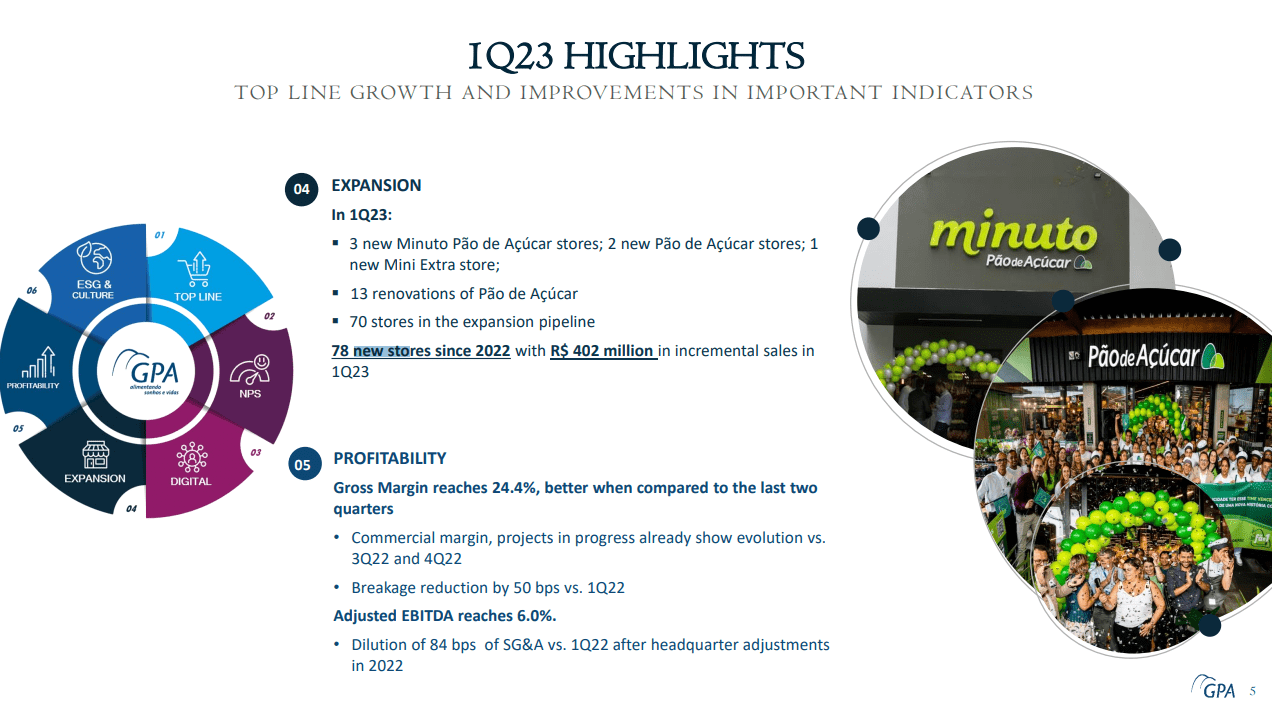

Some hypermarket facilities, part of the discontinued business, have also been converted into large Pao de Acucar supermarkets, and in general this operator has been seeing the most meaningful growth in stores which across segments was at 78, with 71 new stores in the pipeline. Conversion investments were up 50% in FY 2022 and dominated the investment spend as they close the book on the remnants of the hypermarket business. All other types of CAPEX had increased by double or even triple digit rates too. Investment in 2022 was almost 25% of the current CBD market cap, excluding the consolidated Exito investments which are non-core. YoY CAPEX growth continues as of the Q1 2023 as well, focused on new store development which has added about 10% incremental sales to the company in Q1.

Investments in Q1 2023 (Q1 2023 PR)

{kind=link}

Growth In Stores (Q1 2023 Highlights)

In the other supermarket banners, specifically Mercado Extra and Compre Bem, which is more for the mainstream, there was decent growth, especially in Extra, but the overall results were brought down slightly by some idiosyncratic repositioning happening at Compre Bem, where focusing on lower income groups has required those stores to reorient and sacrifice growth in order to maintain profitability. Excluding Compre Bem, this segment would have seen 7% growth, more consistent with Pao de Acucar.

As noted, hypermarkets and still-consolidated holding Exito are not actually included in the above headline growth rates, since they are a discontinued operation by accounting treatment. The hypermarket business of Hipermercado Extra, a segment that is not strategic anymore, is still getting its assets sold nicely to major buyers, with multiple Extra hypermarkets being sold recently to the Singaporean sovereign wealth fund, GIC . This is in addition to the strategic sales they made of 71 hypermarkets to Assai in 2021 . The 2.1 billion BRL price for the 17 locations sold to GIC helped finance CAPEX in 2022 to convert some remaining hypermarkets as well as build new Pao de Acucar facilities, and also created a massive capital gain that makes the last year a more difficult comp on a bottom line basis.

{kind=link}

Example of old segment reporting with hypermarkets (Q2 2020 Pres)

{kind=link}

Q1 2023 IS (Q1 2023 PR)

Proximity (convenience) stores which are composed of Pao de Acucar's "Minuto" brand as well as Mini also saw growth, albeit decelerated since the die-down of the pandemic has meant an exodus this year from metropolitan areas for resumed summer vacationing. However, proximity stores have benefited prior to the holiday season from a return to mobility in metropolitan areas as the pandemic has calmed down. There is quite a lot of investment going into this segment as well, especially in cities with a lot of verticality like Sao Paulo, in order to maximize capillarity.

In the core business there are finally the gas stations. They are usually located at the Extra hypermarkets, and general increase in mobility as well as some idiosyncratic station re-openings connected with the Assai transactions has meant 18% YoY volume increases on a same-store basis. However, falling retail gas prices have reduced revenues, but this means nothing really since the economics of gas stations are invariably based on flat markups , so the profit has grown in line with volumes and the result is greater profit contribution. This is a great segment.

The final comments on the financials are that gross profits are improving thanks to increased premiumization, solid performance in gas stations on a volume and profit basis, as well as some economies of scale involved in expansion and the push to perishables and easier negotiating with domestic suppliers who are also less subject to logistics inflation. However, gross margins are tightening due to general inflation, also affecting SG&A, so there is a decline in EBITDA.

{kind=link}

Gross Profit (Q1 2023 Pres)

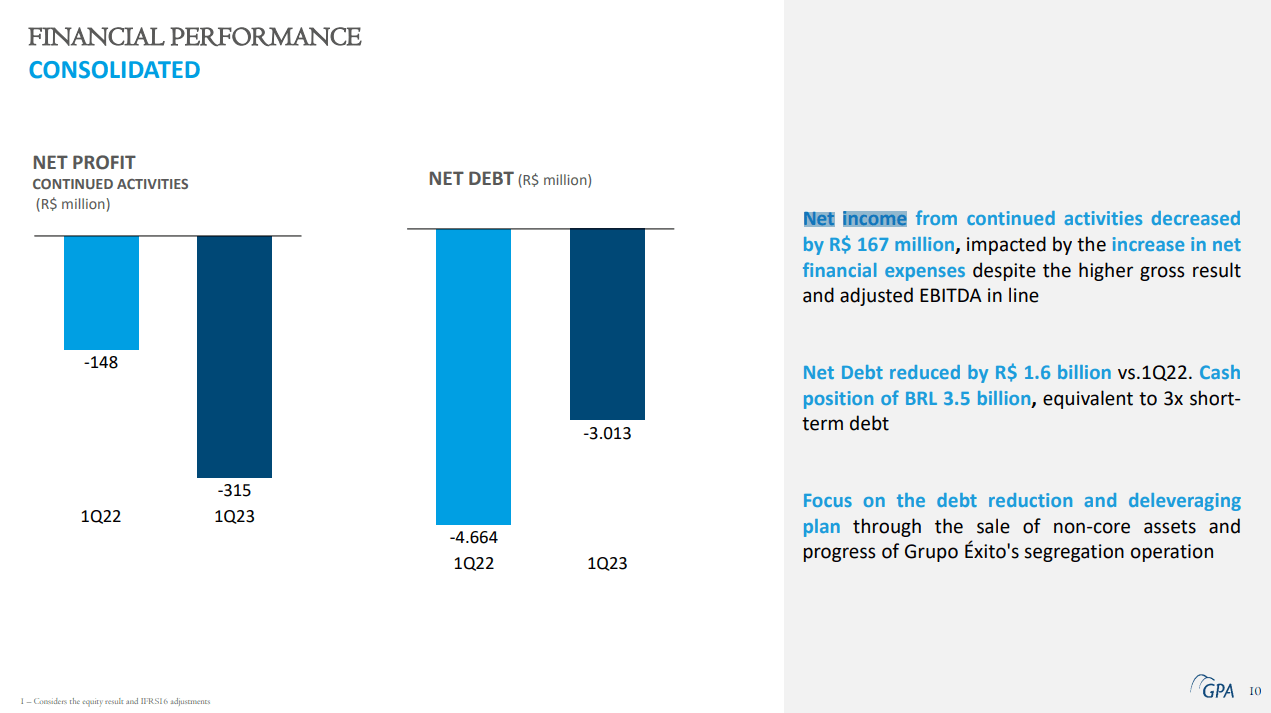

We should mention that the company is EBITDA profitable, but not net income profitable. The reason for net unprofitability is substantially due to financing costs associated with the company debt. Net debt (calculated as debt minus cash balances only)/ EBITDA is around 2.3x, which in a totally developed Western economy would be entirely tenable, but with double-digit interest rates in Brazil it is less so. There are no maturity issues to be worried about, though, and once the incremental working and fixed capital investments die down following the expansion, and these newly-built assets come online in an environment where inflation is also calming down, operating cash flow will return closer to a zero-level despite interest, meaning debt will be amortizing sustainably.

Incidentally, inflation is coming down so much in Brazil that it could very well lead to increased dovishness, since inflation is only slightly above the policy rate by about 1%, which is actually within the 1.5% tolerance range. Moreover, the new president Lula, who is considered left-wing, is hoping that the central bank goes more dovish and allows for funds to be injected into the system again, meaning more accommodative financing costs for companies like CBD. Lula is specifically looking at Petrobras ( PBR ), which is substantially publicly owned, and measures to target energy prices could continue to keep inflation at much lower levels to make space for central bank accommodation to relieve debt pressure on companies like CBD.

{kind=link}

Net Income (Q1 2023 Pres)

Exito

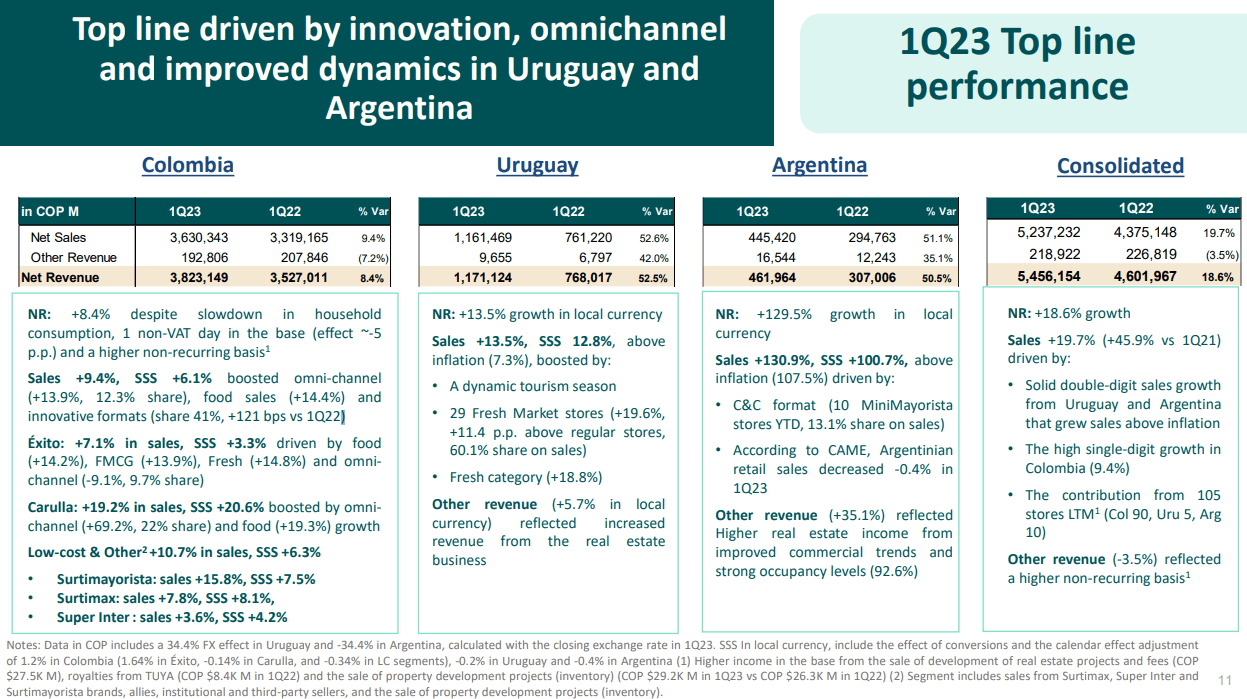

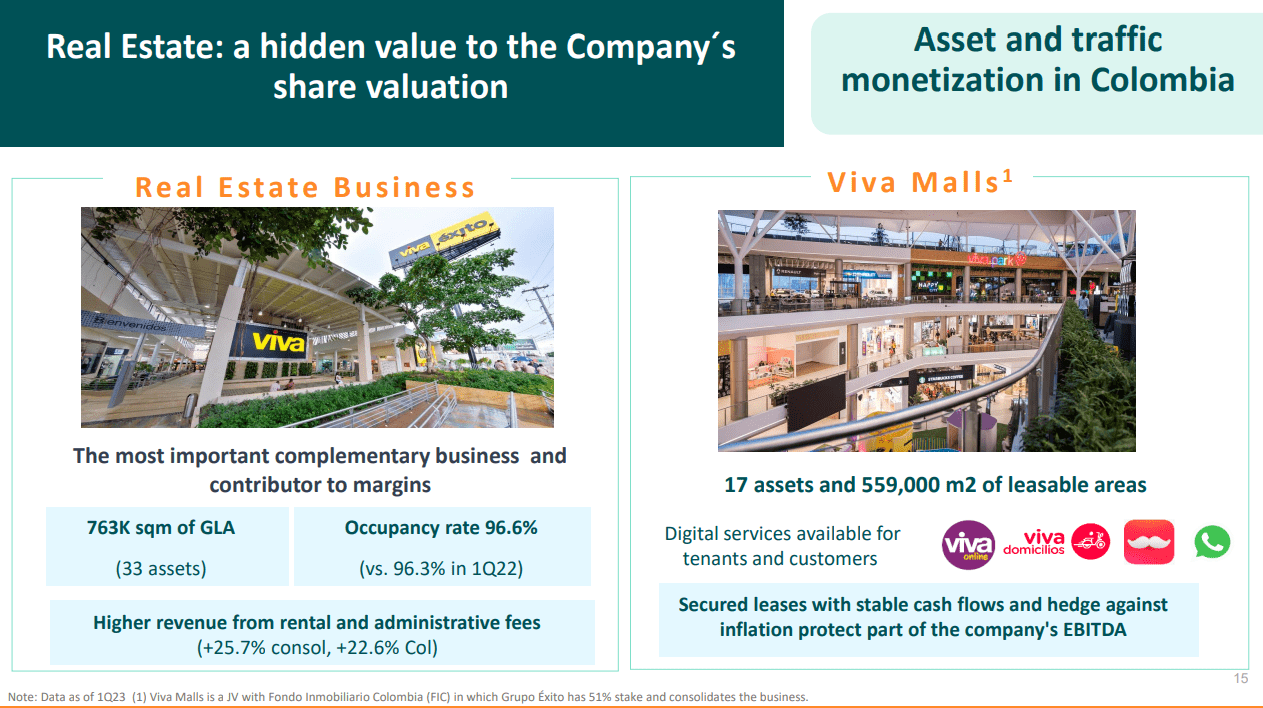

Exito is the major catalyst for the CBD case, and an important part of the SotP analysis and the case for severe fundamental undervaluation of CBD. Their markets are not Brazil, but other parts of Latin America like Colombia, Argentina, and Uruguay, still in the businesses of hypermarkets, convenience stores and supermarkets. They also have a pretty substantial portfolio of retail real estate in Colombia, meaning that their profile is skewed towards assets that in general would command lower required returns than an operating business, and consequently higher valuations.

{kind=link}

Exito Sales (Q1 2023 Pres)

Argentina is a troubled geography in general for any LatAm company that operates there due to unbelievable inflation coupled by exchange controls, and the Colombian Peso depreciated quite a bit this year (10% against the USD) which meant the Uruguay business (subject to more NCI ownership) grew a lot in the mix, since the Uruguayan peso even appreciated against the monster 2022 USD. But as an operator, Exito performs well and manages to deliver growth at its locations based on same-store results, even in somewhat troubled economies, which is a testament to the resilience of food retail even in tougher economic conditions as well as the value of having a diversified business in FX terms in LatAm, since comprehensive results ended up being pretty in-line with same-store performance even in USD terms. Its sales growth outpaced the 10% COP depreciation against the USD, and Exito actually produced respectable sales growth in USD terms around 10%, which is consistent with CBD's core sales growth.

These LatAm currencies haven't been too volatile, and now is not the time to be worrying about further declines since the USD is more of a speculative target due to the continuing impasse over the debt ceiling and the fact that rates may be peaking soon as the U.S. gets weaned off easy credit post regional banking failures. With a monster 2022 for the USD and an inflection in global economic conditions, it is more likely that the USD goes lower than goes higher. We do not think these FX considerations should be a sticking point for today's buyer at all.

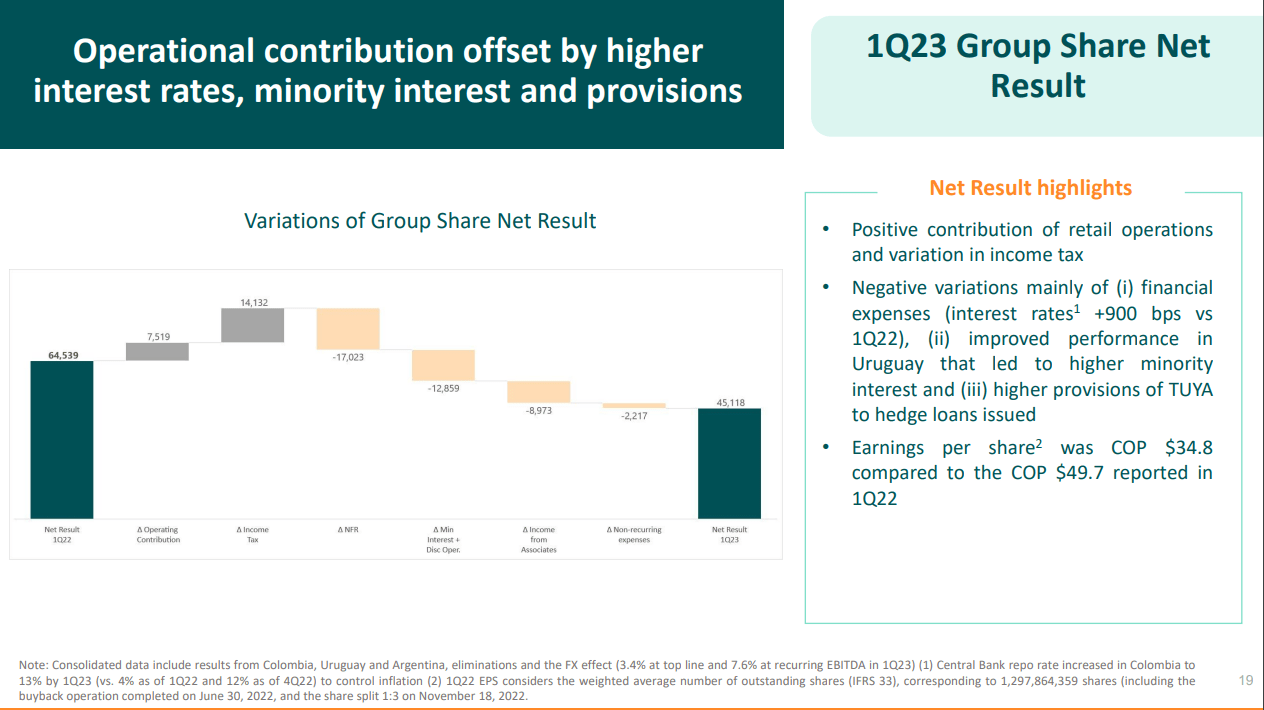

Operating profit rose without issues, driven by growth in gross profit as a testament to the resilience of food retail. But higher net leverage due to buybacks and dividends grew finance costs and hurt net income. Still, net income margins remain positive.

Additionally, because of the COP decline, the Uruguayan business which has a large minority interest grew in the mix on a COP basis but had a more limited contribution to the positive net income vectors for owners of the parent company due to the NCIs. But with USD-based sales growth comprehensively, even after de-consolidating the NCI, the main negative has been on the financial costs side, because much like Brazil, Colombia has raised rates by 10% to control inflation. This had about a -33% effect on the parent company net income.

{kind=link}

Net Income Evolution (Q1 2023 Pres)

{kind=link}

Exito Real Estate (Q1 2023 Pres)

We should also mention that Exito is pretty asset rich and has real estate assets that should in general be higher multiple, but we won't belabor this case since these malls are in Colombia and we don't want to apply broad retail real estate multiples to these assets. They also have J.Vs in a couple of payments and card companies in Colombia called Tuya and Puntos Colombia, which are assets that could be worth about 10% of the current market cap if valued independently. But again, we aren't going to develop this case.

They are valued at approximately a 5x EV/EBITDA including NCIs in the valuation. That more or less accounts for the FX risks, even if diversified and limited at this point, that are inherent to the business, trading off the more consistent economics that come with real estate. There's no reason to believe that Exito is overvalued.

CBD owns 96.5% of Exito at this current time, and they have announced plans to spin this off sometime in 2023 with plans to retail only 13% of the company. It is pending approval, and whether the spin-off happens or not doesn't change the value case, only the catalyst case.

Cnova

Cnova owns Cdiscount which is a French ecommerce platform. Not being Amazon.com, Inc. ( AMZN ) it's of course tier II, but it does have some unique offerings such as doubling as a travel website where you can buy travel packages, as well as phone plans. Otherwise, it is simply an Amazon imitator but for the French market, that offers lower prices on its marketplace to try to entice some more marquis French customers to focus on their platform rather than Amazon's for selling their products - things like luxuries and perfumes, products that you don't typically go to Amazon for and with producers that are often residents in France, and also technical goods and home equipment like appliances. Needle-moving French companies are more likely to support a local platform over Amazon, especially if the offering is cheaper.

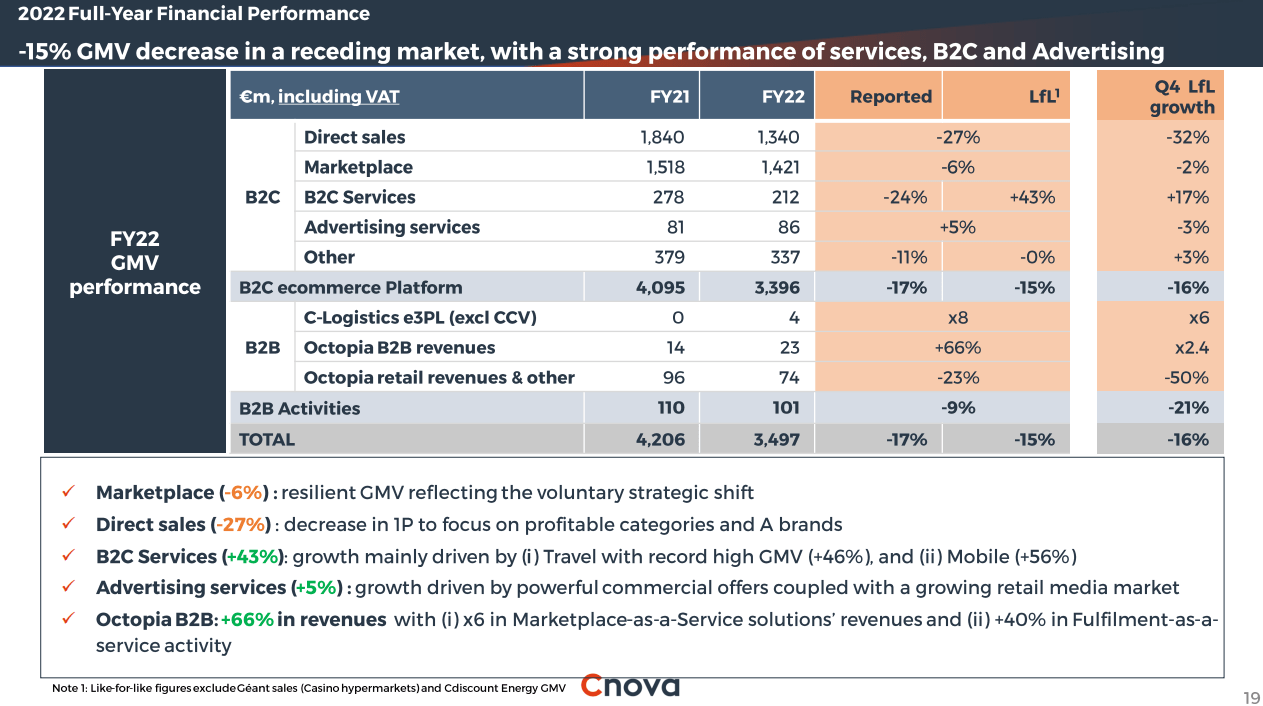

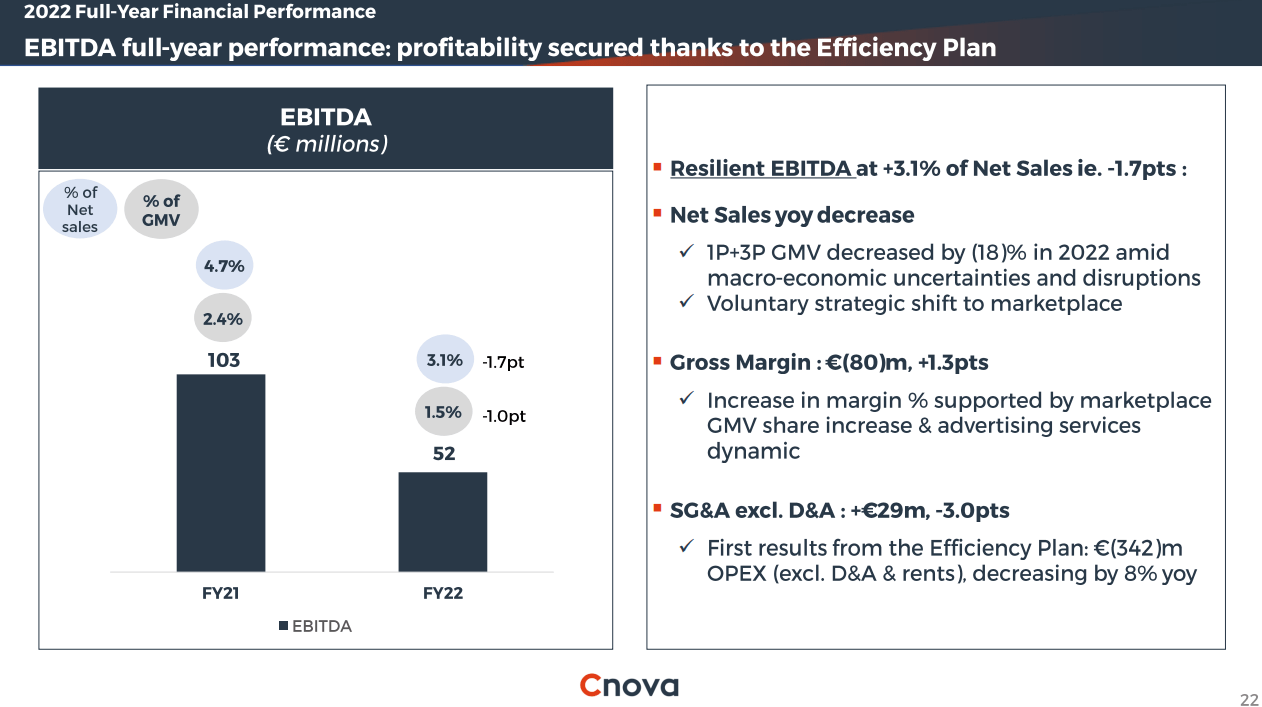

The company has taken a pretty substantial GMV hit . Part of it is that the end of the pandemic has generally struck ecommerce players, but it's also that Cnova has dialed down its inventory for direct sale and is rationalizing that business in order to grow marketplace in the mix and start slashing SG&A costs. Direct sale will continue but more focused on higher margin products. This is a brand new initiative, and while EBITDA is falling substantially YoY at the moment, further SG&A declines as well as further marketplace growth, which has been gross margin accretive, should start upping the EBITDA again soon enough.

{kind=link}

GMV (FY 2022 Pres Cnova)

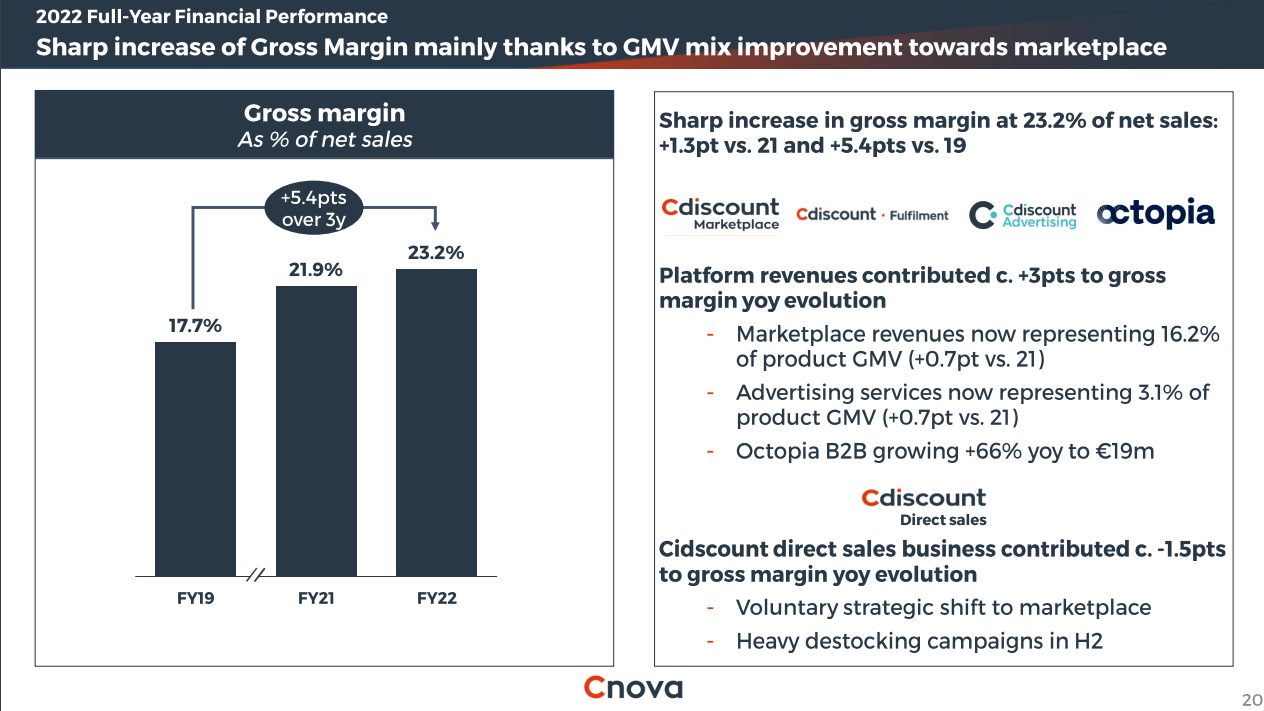

To be clear, this was a voluntary move by the company as they try to build their marketplace and advertising offerings and try to leverage platform economics. Considering that no one can compete with Amazon as a one-stop online shop, especially where Amazon.fr exists to address the French market, focusing on the marketplace which is very profitable, and providing full-service logistics offerings for marquis clients who want to sell their products on Cdiscount rather than Amazon for a higher margin due to lower marketplace commissions, seems like a somewhat reasonable pivot - although we don't like that EBITDA has dropped.

{kind=link}

Gross Margin Mix Effects (FY 2022 Pres)

{kind=link}

EBITDA (FY 2022 Pres)

On the plus side, the whole model is going to have minimal working capital intensity, and probably be less intensive on a fixed capital basis too, at least incrementally since there's a lot of indivisibilities in logistics assets that take a lot more scale before they are utilised fully and require new investment. Operating cash flows are up YoY, and some asset disposals allowed for a bit of deleveraging. They have undrawn credit and there's no issue in the maturity profile whatsoever.

CBD owns about 36% of Cnova. With a 1.8 billion EUR market cap and a 50 million EUR EBITDA, the valuation is pretty high at more than 30x EV/EBITDA. Too high in our opinion. Halving the equity value gets us to a more reasonable figure given the current economic environment. If management delivers on its platform strategy, a 17x multiple would be a little low since the platform economics could be really good if Cdiscount can defend its space. In the end, Cnova doesn't have a huge impact on the upside case, so we won't quibble here - if you gave Cnova a zero value you'd still have a 71% upside in the valuation we're about to show you.

Valuation

Let's finally put together the valuation. We use the core EBITDA of CBD that excludes the Exito contribution. Our comps are supermarket players, with a special focus on Carrefour which actually sees 15% of its global revenues come from Brazil. As the leader in the Brazilian market, it's an important benchmark. Since Exito is also a supermarket player in LatAm, we map its individual multiple as well. In the end, we use Carrefour's multiple as a comp since it's the lowest, and we want to be conservative.

We have halved the equity value of Cnova to be conservative, since it currently trades thinly and in principle, despite there being a premium on liquidity, price discovery could see it move the wrong way - although this is being very harsh on the valuation, since market values tend to be the most conservative benchmark. For Exito we use the market value, which is somewhat conservative as well since greater liquidity after a spin-off could mean higher valuations for them. We get the following for the valuation.

CBD Valuation (VTS)

Bottom Line

The risks are on the finance cost side, although we do believe that dovishness will come due to Lula and the fact that inflation is actually under control according to the CB policy in Brazil. Even if it doesn't, as with what happened in the Assai spin-off, some of the debt of CBD could be moved over to Exito, since Exito actually has positive net income margins still and has some additional debt capacity, which would relieve the pressure on CBD margins. Otherwise, operating cash flow is going to normalise since major store CAPEX and conversion CAPEX should start trending down soon, and the full benefits of the perishable strategy should start becoming a little more evident in the margin and organic debt servicing picture of the company. Currently there's quite a bit of WC intensity that should go down with their strategy change, and their -2.5% net margin should also thin out to zero soon. The operating and investing cash flows should settle down to a sustainable plateau until Brazilian rates have space to come down again and grow the net income.

{kind=link}

Finally, we are in a situation where inflation is after all coming down, and that isn't yet reflected in the margins, with COGS still seeing some latent rises as well as SG&A as vendors, often with less immediate bargaining power, are probably passing through inflation onto CBD with a little bit of delay. So that should stop over the next 6 months while CBD continues to raise prices thanks to its premiumisation strategy. So regardless, the debt isn't an existential problem, and no financial distress discounts should be considered at all.

FX risks are also reasonably limited. BRL has been doing very well, up slightly against the dollar YoY, and even some of the Exito currencies are doing well against the dollar, offsetting the weaker LatAm currencies. A big thing is that Brazil is much more unaligned with respect to the Ukraine war, and the Brazilian consumer is benefiting from that. The BRL should see concrete backstops thanks to the greater purchasing power of the currency as it hasn't alienated Russia completely , or frankly at all if you look at surging diesel import figures. In this way, Brazil shares its position vis-a-vis structural energy prices with countries like India, that have also stayed unaligned are exceptionally well positioned for this next geopolitical leg.

Within Exito, the greatest concern is the Colombian Peso, since Petro, the new leftist progressive president, has been a concern for markets - less so for his leftist politics, but more so for his progressive politics, including ill-timed rhetoric around weaning Colombia off profitable fossil fuels and the Amazon deforestation in a time where pulp is also very highly valued. The Colombian CB is also taking a wait-and-see approach with rate hikes, which is probably the right decisions, but compounds weakness of the Peso which has lost 20% value last year. On the bright side , the government is formed of a very broad coalition, so radical concentration is very unlikely; in fact what is most likely is that the government will be ineffective in reforms, but that would be fine for the markets.

The spinoff is still pending approvals, and it is the catalyst for the valuation case. We see no reason for it not to happen, especially since shareholders of CBD, dominated by Casino Group ( CGUIF ) which owns 40% of CBD, are going to essentially guarantee the shareholder approval. It's also possible that Exito loses some value after the spin-off, but we don't see that happening given the Exito valuation. At any rate, it could fall a lot and still leave meaningful upside since residual CBD would be highly unlikely to fall enough in in value once losing Exito to maintain Miller-Modigliani value conservation through the spinoff - in the end there's just too much margin of safety. Finally, even if the spinoff doesn't happen, it doesn't change the SotP case and there's scope for earnings growth with lower rates eventually and a more premium strategy.

With good direction for earnings as well due to the store investments and relatively strong consumer conditions for Brazil, Companhia Brasileira de Distribuicao would still be a buy on an earnings growth basis. With the potential for frontloaded returns on a spinoff catalyst, where the spinoff is unlikely to get derailed, at such an obvious SotP valuation CBD stock is a no-brain buy.

For further details see:

Companhia Brasileira de Distribuicao: Negative EV With Catalysts On Exito Spinoff, With Food Retail Resilience