COMP - Compass: Risks Have Multiplied But Market Share Gains Are Encouraging (Ratings Downgrade)

2023-11-12 01:32:16 ET

Summary

- Compass, the largest brokerage in the US, has seen its share price plummet due to the real estate market dampening and the recent lawsuit against the NAR.

- The lawsuit questions the fee-based real estate agency model and may lead to changes in fee structures and commission rates.

- Despite the risks, Compass has shown improvement in revenue declines, market share growth, and success in bringing down operating expenses.

- Moving to the sidelines with a neutral rating.

Few industries have been as shaken up this year as the real estate industry. Coming off a historic price burst during the pandemic as demand for moving compounded with low housing inventory, the real estate market dampened significantly this year due to skyrocketing mortgage rates. Then, to add insult to injury, the recent lawsuit against the NAR puts the entire fee-based real estate agency model in question.

Against this backdrop, shares of Compass ( COMP ), now via acquisitions the largest brokerage in the U.S. by transaction volume, has seen its share price plummet from midsummer highs above $4.

More risks have emerged for Compass, but some bright spots still remain

I last wrote on Compass in September when the stock was trading closer to $3. Since then, the stock has shed over a third of its value, sinking below $1 billion in market cap, while the historic fee-collusion judgment was passed to the NAR. Amid continued revenue declines and an uncertain future for the industry, I'm now dropping my rating on Compass to neutral.

The biggest driver here is the ruling against the NAR. The background behind the lawsuit: as many already know, in the U.S. the most common way to compensate real estate agents is via a sellers' fee. The sellers' agent usually collects ~6% of a home's gross price and splits that revenue with the buyers' agent. The class action suit claimed, among other complaints, that the NAR's requirement for the sellers to compensate agents of both parties, as well as the inability of buyers' agents to make a sale contingent upon the negotiation of that commission, has artificially kept real estate commissions both opaque and high - benefiting the NAR and realtors at the expense of American consumers.

It will take time for the downstream impacts of this decision to play out, and there is a wide breadth of outcomes that industry watchers are projecting. Aside from flattening fee structures and potentially lowering commissions, this may prompt many agents to switch away from a percentage-based "success fee" to an hourly model, similar to how more lawyers charge for time instead of on contingency. But either way, one thing is clear: the gravy train of 6% fees between buyers' and sellers' agents may have a short shelf life, especially in this market environment where consumers have pushed back on price inflation and some quintessential institutions such as tipping have come under attack.

Another risk for Compass: mortgage rates may remain elevated for an extended period of time. Most of the people now entering prime home-buying age grew up in an era of ultracheap money - and high rates may encourage renting versus buying for longer.

Q3 results show moderation of revenue declines and market share growth

This all being said, there are bright spots to call out. Compass' Q3 results showcased that revenue declines are moderating sequentially, while the company also continues to gain market share, building on its existing leadership position in the U.S. market.

{kind=link}

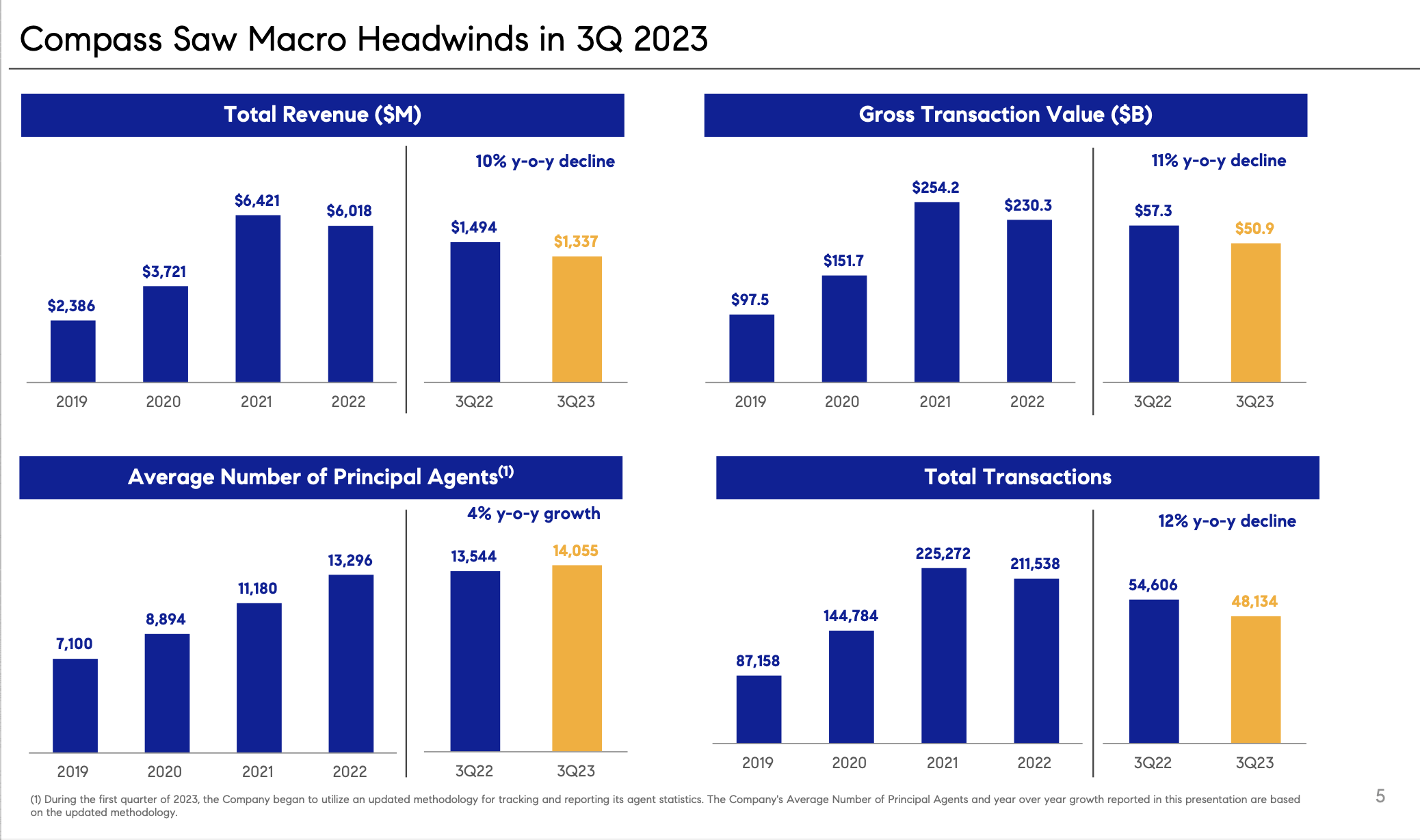

As shown in the chart above, Compass saw a -10% y/y revenue decline in Q3, which was far better than a -26% y/y decline in Q2 (in part driven, however, by easier comps in the year-ago period). Gross transaction volumes, similarly, declined -11% y/y to $50.9 billion.

In spite of this, Compass reported that it had a 4.4% of the U.S. real estate market in Q3, a 26bps increase y/y. This says that while Compass is still facing sharp declines, it is suffering at a more muted pace than its peers.

The second major thing to laud Compass for: its success at bringing down operating expenses. Since the start of its cost-cutting process in the second quarter of last year, management notes that it has cut out $550 million of annual opex with a target of reaching an annualized opex run rate of $900 million by the fourth quarter this year.

Per CEO Robert Reffkin's remarks on the Q3 earnings call :

We have worked hard to position Compass to be able to ride out this period of macroeconomic uncertainty and position Compass for even greater success when the market recovery begins. We are working from a position of strength. As the number one, brokerage by sales volume in the United States over the past two years, we have built an amazing business with the best agents serviced by a highly dedicated team of professionals at Compass that is laser-focused on delivering excellence at every level.

Although the market has not improved over the past year, Compass is a much stronger company with a lower cost base, higher principal agent retention, a revitalized post-pandemic culture, enhanced technology platform in a larger agent to agent client referral network. I am proud of the fact that our team has thoughtfully and skillfully been able to reduce OpEx run rates by approximately $550 million since the second quarter of 2022. We said we would do it and we did it.

We expect to achieve our target $900 million OpEx run rate as we exit Q4 as planned. This is more than a $0.5 billion of expense cutting while still growing the number of agents, improving agent retention, and adding important new features to our technology platform."

This expense discipline has helped Compass reported $21.8 million of positive adjusted EBITDA in the quarter despite revenue softness, representing a 1.6% margin - and a 440bps y/y improvement.

{kind=link}

YTD free cash flow of $3.9 million is also substantially better than a cash burn of -$230.8 million in the first three quarter of 2022. In other words, Compass is not blind to the state of the market and it has prudently shaved expenses in order to enable profitability during lean times - which will serve it well if the real estate market rebounds.

Key takeaways

My downgrade on Compass is driven by my discomfort in investing in any real estate broker amid a massive potential industry disruption in fees - but among all brokerages, Compass is the most likely to survive a transition, given its market share gains and profitability expansion amid a tough year. That being said, I'd prefer to move to the sidelines and invest elsewhere at this point.

For further details see:

Compass: Risks Have Multiplied, But Market Share Gains Are Encouraging (Ratings Downgrade)