SVOL - Composing Your Own Short Volatility Strategy With ETFs

2023-11-23 05:04:38 ET

Summary

- Recreating Simplify Volatility Premium ETF's strategy using short volatility ETFs is possible and provides us insight into SVOL's potential flaws.

- ProShares Short VIX Short-Term ETF and Volatility Shares' -1x Short VIX Futures ETF offer investors access to ETF-only portfolio strategies that can provide short volatility exposure.

- These strategies are unique because they give investors access to gains via capital gains, not current income. The strategies perform wildly different based on varied backtests.

- Backtesting these strategies reveal soft spots in short volatility ETFs' armor and raises questions about safety from black swan wipeouts.

Introduction

Ever since the Simplify Volatility Premium ETF (SVOL) entered the market, retail investors have had access to a strategy traditionally reserved for sophisticated options and futures traders, commodities trading advisers (CTAs), and hedge funds: short volatility. SVOL is actively managed and typically provides exposure ranging from 0.2x to 0.3x short the VIX.

This article is not about SVOL and instead is about replicating its strategy using short VIX ETFs. If you want to learn more about SVOL, please check out my coverage about their bond holdings or their recent shift of distribution types . In the past, I have given SVOL a buy. As of now, my stance is a hold. (This may not age well.)

I was inspired by a comment on my last SVOL article that mentioned putting on your own short position and hedging manually. While this could be done with futures, this led me to wonder what a retail trader who only wanted to use ETFs could put together as a replication of SOVL's strategy.

Inverse VIX Funds

Since April 2011, investors have had access to a passively short strategy. This is ProShares Short VIX Short-Term ETF (SVXY). The fund aims to offer 0.5x short exposure, rolled on a daily basis.

The fund also gives us insight into what could happen to an unhedged short VIX strategy in a dramatic black swan event.

Launched in April 2022, Volatility Shares' -1x Short VIX Futures ETF ( SVIX ) has taken allowed investors to gain incredible exposure to short volatility, double what SVXY has been offering. It's unclear whether holding this is prudent or not if we have a crash like SVXY had.

Using these two funds in conjunction with a portfolio of bonds, we could recreate SVOL's strategy.

The Strategy

For this to work, we need to understand why SVOL is attractive to investors. It offers a few things:

- Short VIX exposure between 0.2 - 0.3x

- An underlying portfolio of bonds

- Monthly income

- A hedge against severely adverse movements in the VIX (crashes)

Those are going to be our objectives. If we can hit those and benchmark with good metrics against SVOL, we might have a viable strategy.

The strategy that I've come up with works with the following rules in mind:

- The portfolio may only consist of ETFs

- Short VIX exposure with a target of 0.25x

- Automatic rebalancing occurs when any asset has an absolute deviation of more than 5% from its target weight in the portfolio

- For example: if SVIX's target weight is 25% of the portfolio, a rebalance would occur if it grew to 30% or fell to 20%, and we would buy/sell other assets to return to target weights

- Automatic rebalancing occurs when any asset has an absolute deviation of more than 5% from its target weight in the portfolio

- All other holdings should be bonds

- Ideally, short duration bonds like T-bills, the (BIL) ETF will be used for this

- A hedge should be employed

- In an ideal world, we could use VIX calls as they are the most capital efficient, but ETFs only means we will be using a hedging ETF. I'm going to use the Cambria Tail Risk ETF (TAIL)

So what do these portfolios look like?

SVIX Replication Portfolio:

25% SVIX | 70% BIL | 5% TAIL

SVXY Replication Portfolio:

50% SVXY | 45% BIL | 5% TAIL

These two allocations result in our average exposure being 0.25x short VIX and anywhere between 0.45x - 0.7x average exposure to long T-bills, and 0.05x exposure to tail-risk hedging strategies.

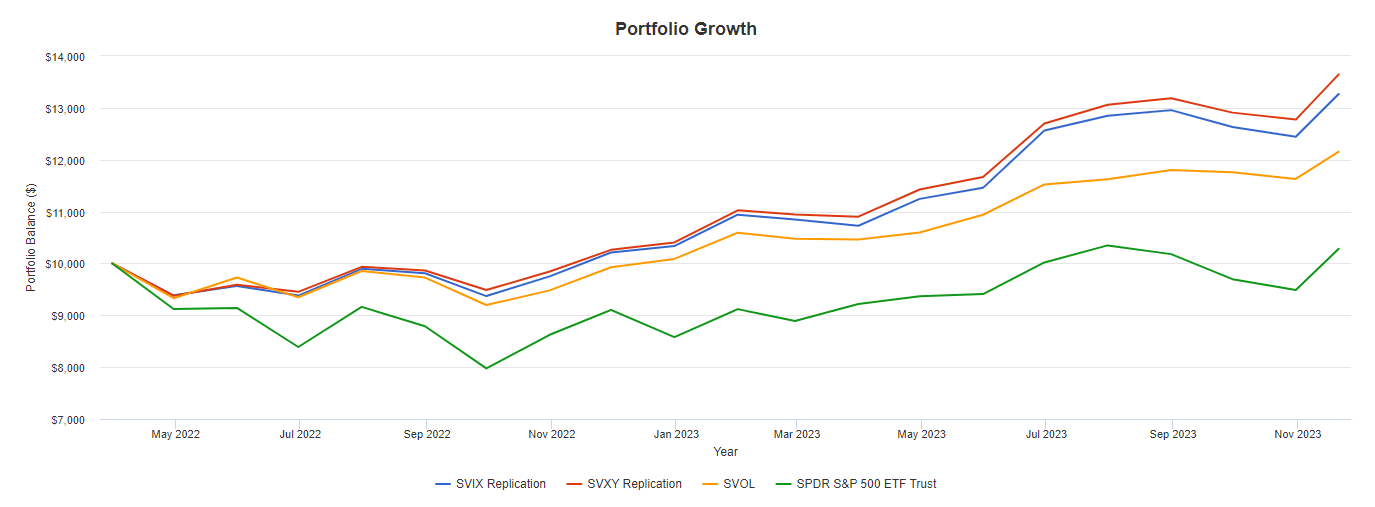

Backtesting Results

These backtests are done assuming all dividends are reinvested at the time of distribution. Here's how they stack up against SVOL.

For those who would like to see the backtest for Figure 3, here you are .

{kind=link}

In this very short timeline, both versions of the strategy outperformed SVOL. Short volatility outperformed the S&P 500 in this same timeframe, too, interestingly enough.

| 4/1/22-11/21/23 |

| CAGR |

| STDEV |

| Beta |

| Sortino Ratio |

| Max Draw. |

| Max. Draw. Length |

| Rebal. Events |

| Income |

| SVIX Rep Portfolio |

| 18.48% |

| 13.89% |

| 0.58 |

| 2.03 |

| (6.29)% |

| 6 Months |

| 4 |

| $430 |

| SVXY Rep Portfolio |

| 20.50% |

| 13.08% |

| 0.55 |

| 2.45 |

| (6.23)% |

| 2 Months |

| 2 |

| $293 |

| SVOL |

| 12.42% |

| 12.42% |

| 0.51 |

| 1.12 |

| (8.02)% |

| 6 Months |

| 0 |

| $2,651 |

| S&P 500 |

| 1.68% |

| 20.65% |

| 1 |

| 0.00 |

| (20.25)% |

| 6 Months |

| 0 |

| $216 |

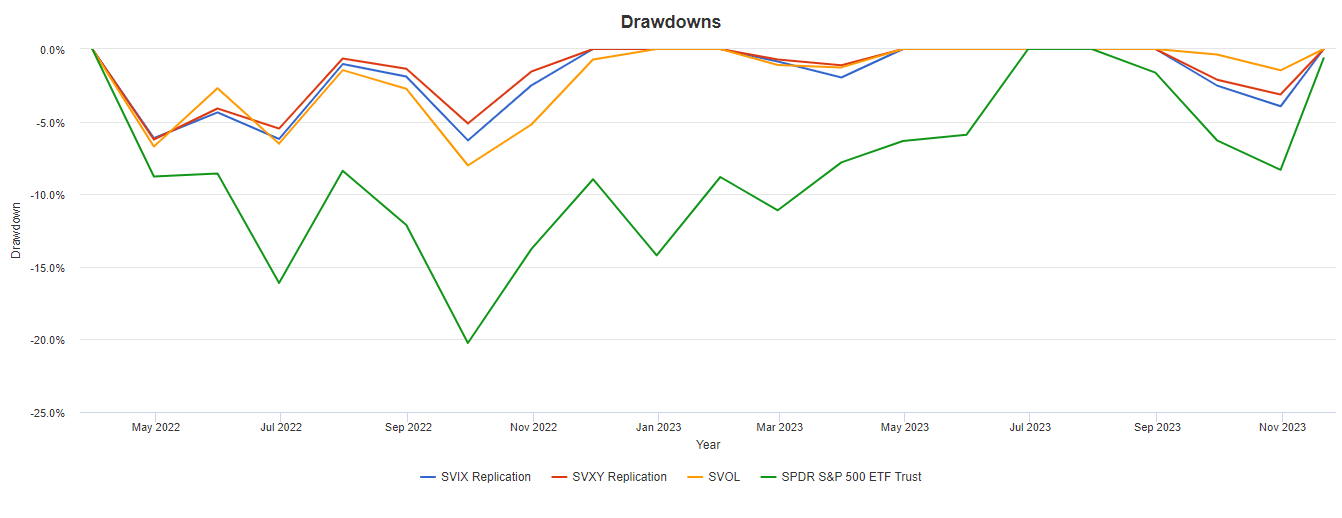

It's easiest to see those drawdowns in visuals. The numbers don't always have the same gravitas as graphs do.

{kind=link}

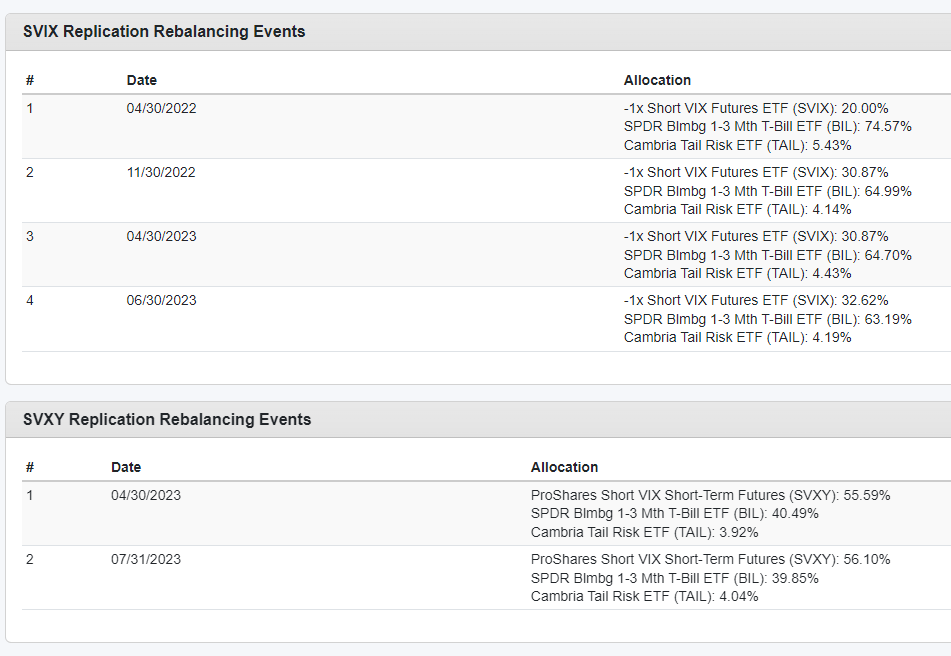

For those interested in how much rebalancing was needed, here are the events and the allocation that triggered the rebalance.

{kind=link}

This strategy is systematic, which means it can be automated fairly easily, and the backtest shows promising results. To be a true replacement for SVOL, we need to evaluate how the portfolios compares not just to SVOL's return but its objectives as well.

As a reminder, those are:

Short VIX exposure between 0.2 - 0.3x

An underlying portfolio of bonds

Monthly income

A hedge against severely adverse movements in the VIX (crashes)

As far as exposure goes, we can see from Figure 6 that our exposure never exceeded the bounds egregiously, and our exposure was kept to an average 0.25x. The systematic nature of the strategy means we rely on rebalancing luck far more than the actively managed SVOL does, but this didn't seem to make too much of an impact in this backtest.

This shows in several statistics:

- Similar standard deviation, beta, maximum drawdowns, and drawdown length show that the strategy is no more volatile than SVOL proper

- Similar drawdown patterns show that the strategy is performing on par, but has a different risk profile than SVOL proper. Both the SVIX and SVXY portfolios have a 0.91 monthly correlation with SVOL

We did achieve an underlying exposure to bonds in all portfolios, which should only improve moving forward if the Fed's higher for longer narrative is to be believed.

Where we fail is monthly income. This could be achieved by investors selling holdings, and some monthly income is generated via BIL, but not too much. If I were to construct this portfolio for myself, I would use (SGOV) instead of BIL. I gave that short duration bond fund a strong buy last month.

Even with the substitution, there is no way the same level of income could be generated by this portfolio without manual selling of shares to cover distributions. The short VIX ETFs do not distribute their gains and instead add them to NAV, so capital gains would be able to offer that replacement for income.

Longer Timelines Raise Concerns

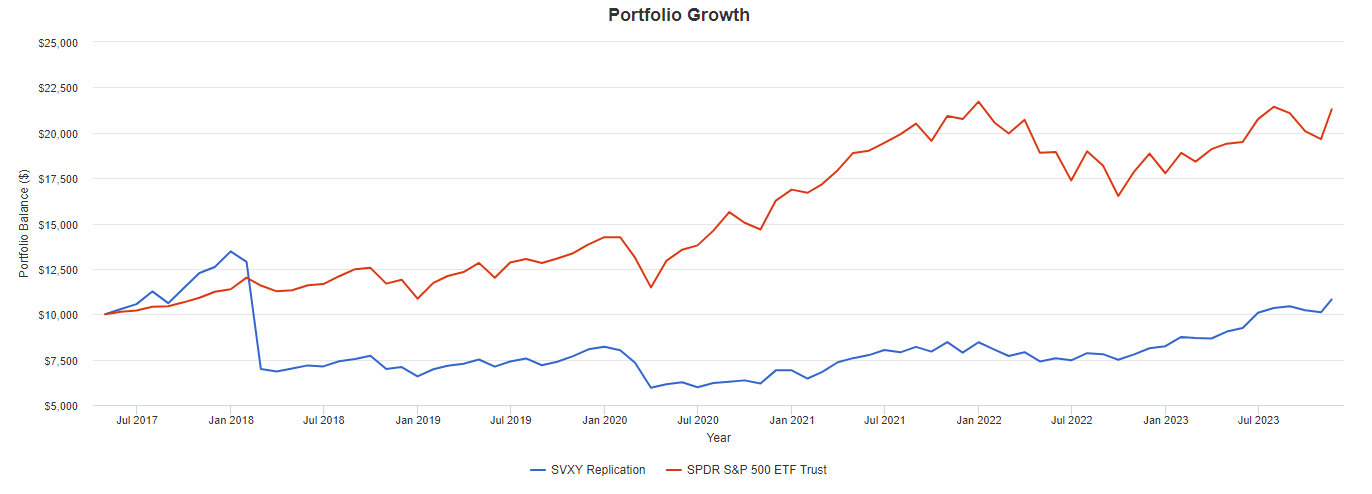

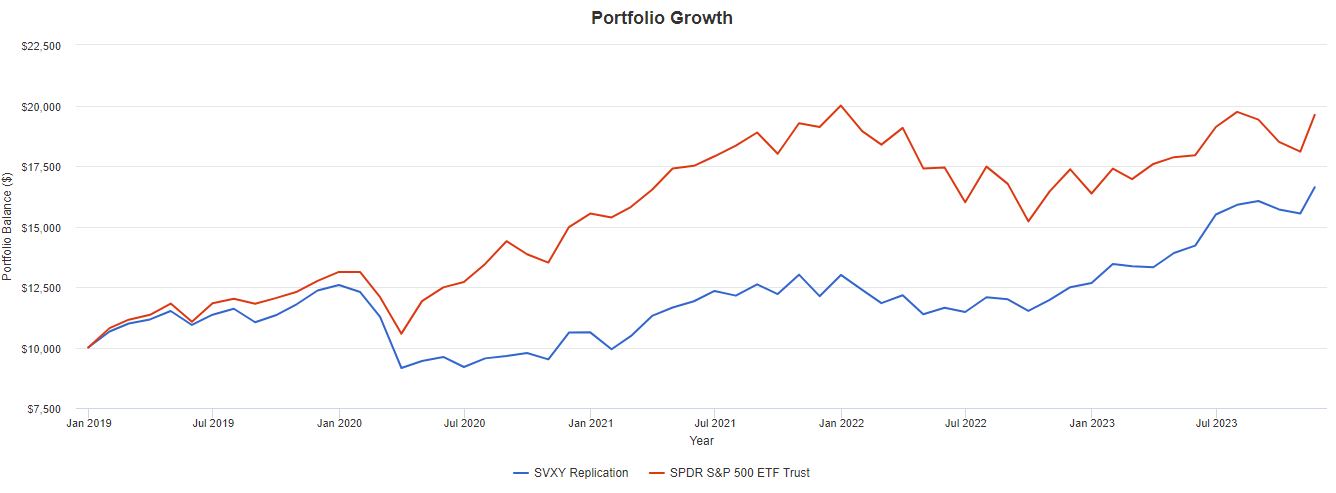

SVIX being so new makes backtesting very difficult. I am able to take the SVXY portfolio much further back. Here are the results for as far back as TAIL allows us to go, from 5/1/17 - 11/21/23 .

{kind=link}

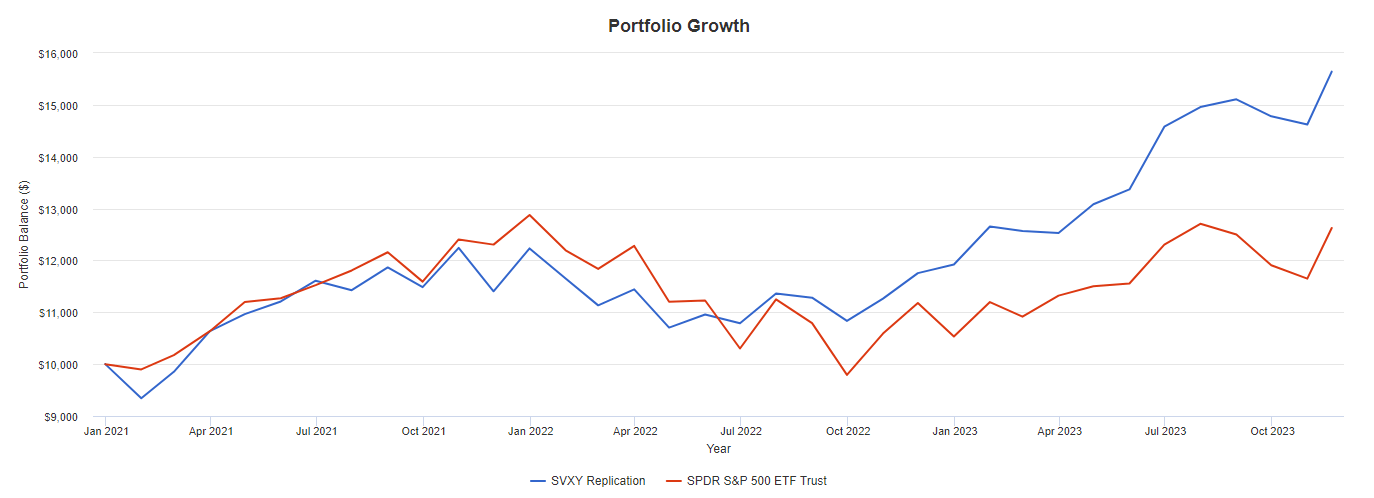

That massive VIX spike during Volmageddon really hampers all future returns to the portfolio. If we start on 1/1/19, the year after that drop, the story changes.

{kind=link}

The largest risk to this strategy is the tail hedge not being enough to cover massive drops like that. Volmageddon was a black swan that tanked the portfolio. The March 2020 crash also did a number on the portfolio, as you can see in Figure 8.

{kind=link}

Moral of the story, don't trust backtests, I guess. SVOL cannot be backtested through the timelines of Figures 7 and 8, so we don't know how it would have performed during those crashes against the ETF strategy.

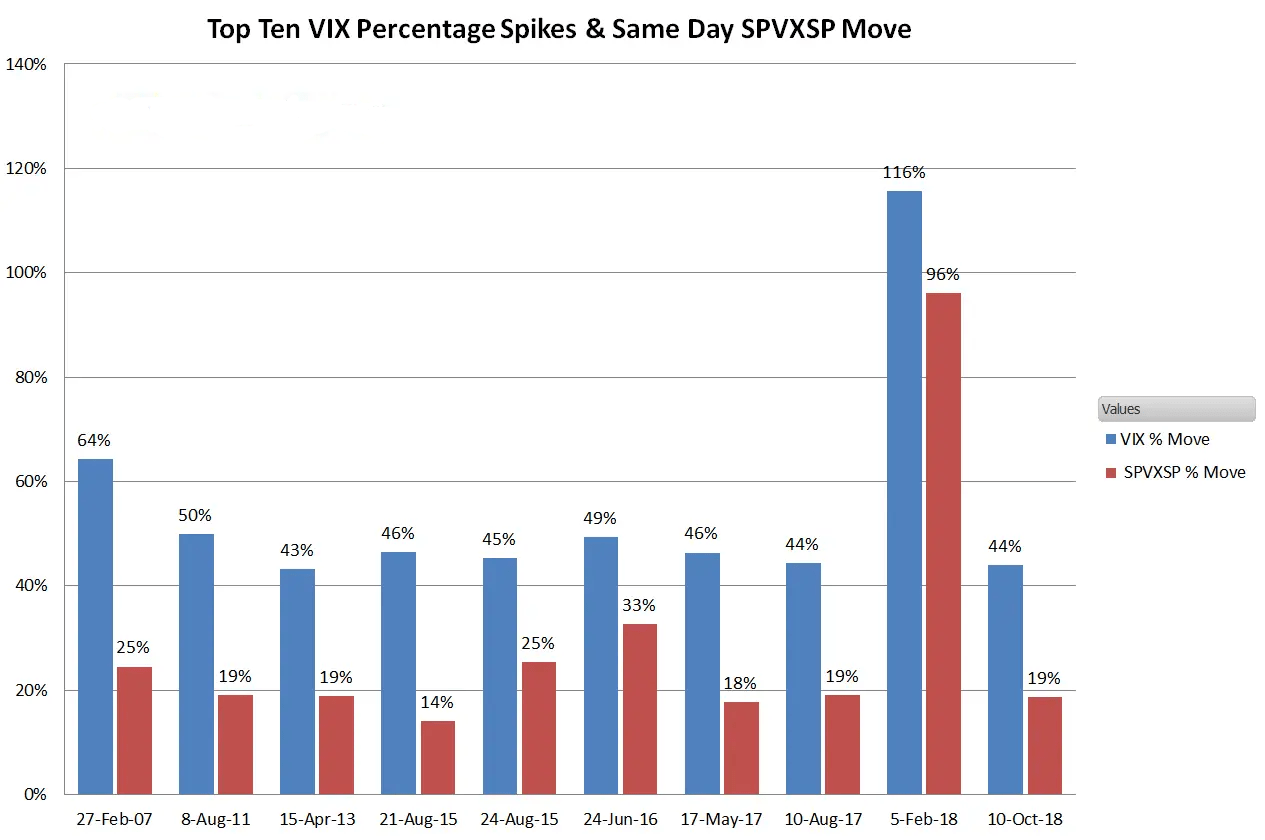

There have been several other events with massive VIX spikes that should serve as a reminder of the crazy risk VIX ETFs possess.

{kind=link}

Hedging with ETFs is Inefficient

The hedging required to be more safe from those events may be too much of a drag on portfolio returns. Unfortunately, TAIL only returned 0.16% during Feb. 2018 and 11.41% in March 2020.

These are not returns that could offset the 89.65% and 38.88% respective losses for SVXY in those months.

More modern hedging ETFs like Alpha Architect's (CAOS) and Simplify's (CYA) could offer increased protection in a similar black swan event, but it is unclear.

There will be, over time, lots of drag with this strategy that the ETF structure allows SVOL to avoid. For example, the income problem. There will also be the issue of capital inefficiency due to the use of capital for ETFs. SVOL is able to write VIX futures using bonds as collateral, but this strategy relies on SVXY's and SVIX's bond holdings, which are not actively managed in the same way SVOL's is.

VIX call spreads are also incredibly better hedging instruments than tail-risk ETFs. These spreads are held by SVOL, which could serve as much better protection in a future black swan. Simplify's risk management is definitely better than this strategy.

Timing

It is to note that now may not be the best time to start this strategy. Note that the VIX is very low currently. While this strategy is designed to be able to be used in any market condition and systematically managed via the rules listed, it still will suffer from whatever condition the market is in on the start date.

That's just conjecture, though.

Conclusion

Would I employ this over SVOL? I don't think so, and I maintain that in the current environment, SVOL is still a hold.

I do like SVIX and SVXY and will watch them moving forward if this strategy can be refined or worked on to provide some advantages over SVOL. SVIX has my attention in particular because of it holds VIX calls directly as its own hedge. Neither SVIX nor SVOL have seen a VIX spike like in Figure 10, so we don't know whether their hedges would be enough to save investors skins.

For further details see:

Composing Your Own Short Volatility Strategy With ETFs