CNXC - Concentrix: More Room Left To Run

2024-01-05 10:11:31 ET

Summary

- After a terrible start to 2023, Concentrix's stock has made a turnaround in the 2nd half of the year, outperforming the S&P 500.

- Concentrix's share price has shown a clear divergence from main peer Teleperformance over the past few months.

- We take a brief look at the reasons for this much-improved performance.

Introduction

Concentrix (CNXC) will be reporting its FY23 results (It has a November year-end) towards the end of the month, on the 24th of January .

In light of this event, this brief article is aimed at exploring the recent share price performance of Concentrix, which has shown a clear divergence with main peer Teleperformance (TLPFY) over the past couple of months. I will attempt to pinpoint the reasons behind this performance, with a view on the earnings release later this month.

Brief Background

For those not familiar with the stock, Concentrix is essentially a business services outsourcing company. They specialize in what is commonly referred to as customer engagement. Essentially, this is an umbrella term for a number of client services functions, and it originated in the call center space, from where their area of expertise has since broadened. The customer engagement software market is expected to grow at roughly 11% p.a. over the next 5 years - depending on the different sources you use. Within this overarching segment, there are a number of different expected growth rates for subsectors. Concentrix has exposure to sectors growing in line with the overall segment, but they are also challenging in segments where growth is expected to be much faster.

For those looking for a much more detailed description of the business, its segments and operations, you are welcome to take a look at my first article here .

Strong Recent Performance

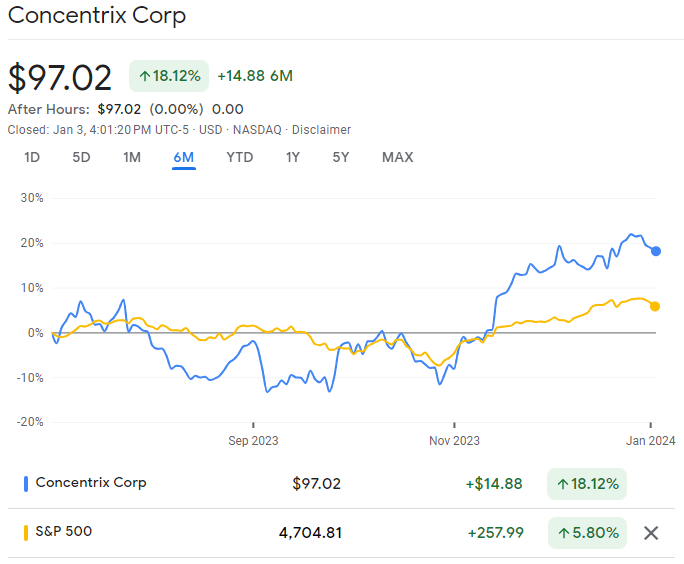

At the time of writing, Concentrix trades at $97/share. This is roughly 30% higher than when I first wrote about the company on Seeking Alpha on the 15th of September 2023. (See article here ). This rally has led to the stock handily outperforming the S&P 500 over the last 6 months, see graph below.

Concentrix vs S&P 500 (Google Finance)

{kind=link}

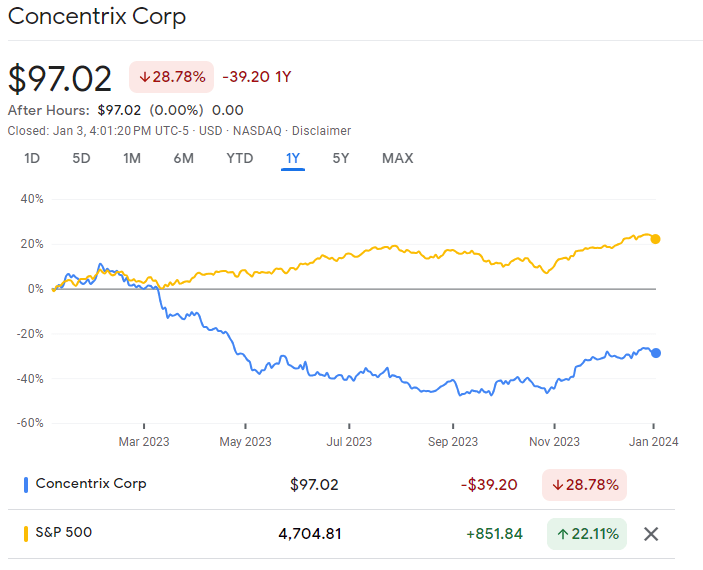

Prior to this rally though, the stock had a torrid time, and over one year, it is still down almost 30%, not a particularly pretty picture, and an absolute mile behind the S&P which is up 20% over this period.

Concentrix vs S&P 500 (Google Finance)

{kind=link}

So what has been the driver of this recent rally, and how does it compare to peers?

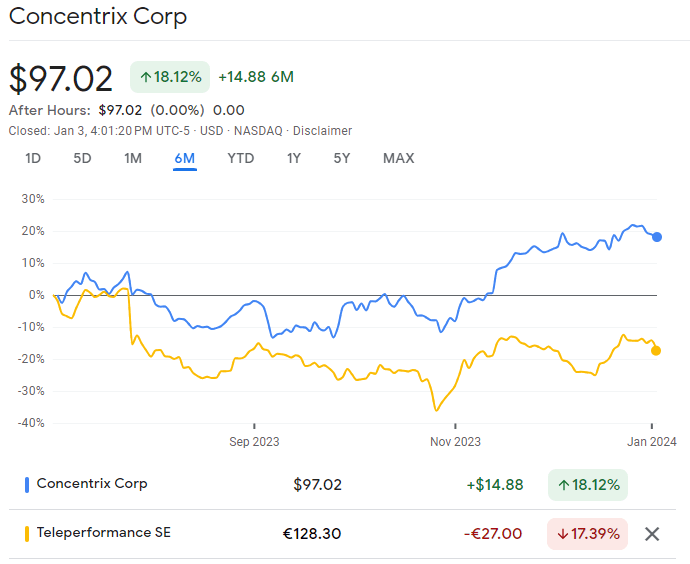

From the graph below, it is clear that over the last 6 months (the same period where Concentrix outperformed the S&P), it has also outperformed its largest peer, Teleperformance, by a country mile. So fairly safe to assume that it was not simply a case of the entire sector catching a breath and going on the trot, as the divergence over the last 6 months is in the range of 35%.

Concentrix vs Teleperformance (Google Finance)

{kind=link}

It is worth noting, though, that during December, Concentrix has been fairly muted, with the price briefly touching $100, but mainly hovering in the high $90 range.

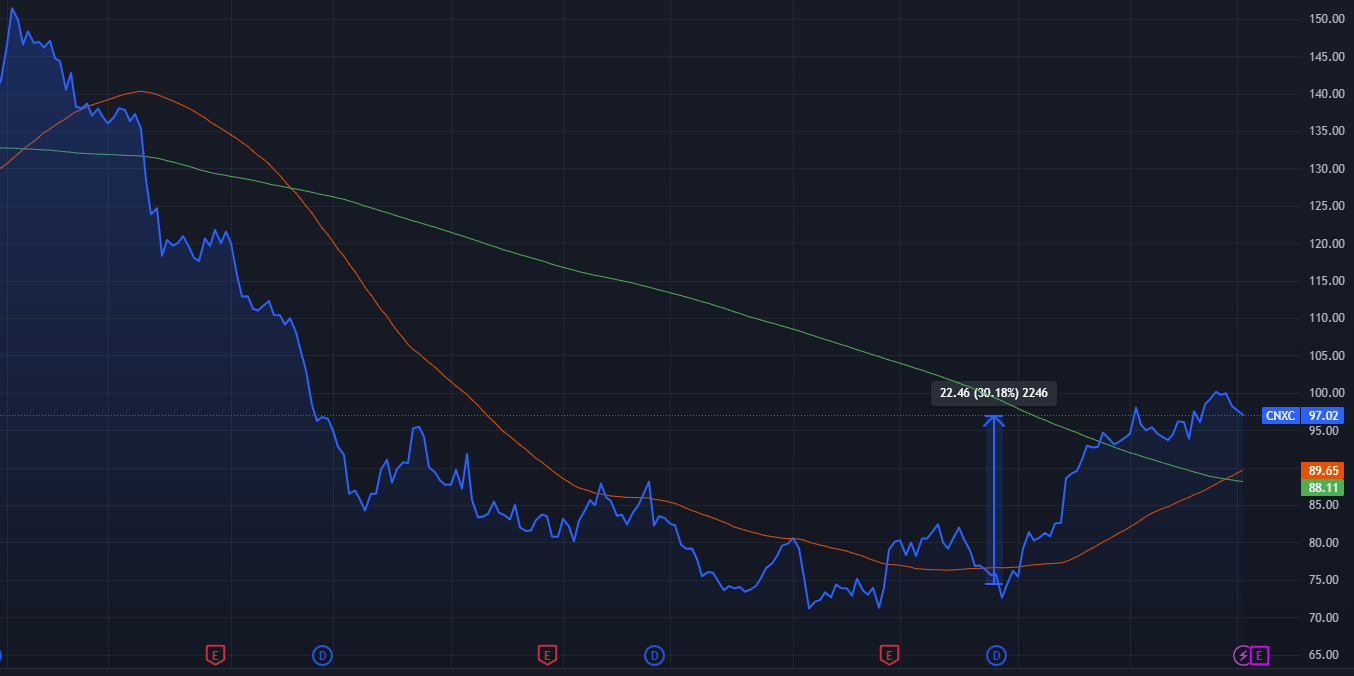

For the proponents of technical analysis - another green light has recently started flashing. While the stock has swiftly moved above both its 50,100 and 200-day Moving Averages ('MA'), there has also now been a golden cross, where the 50-day MA (orange) moves higher than the 200-day MA (green). This is regarded by many traders as a strong buy signal. (See chart below)

Concentrix Golden Cross (TradingView)

{kind=link}

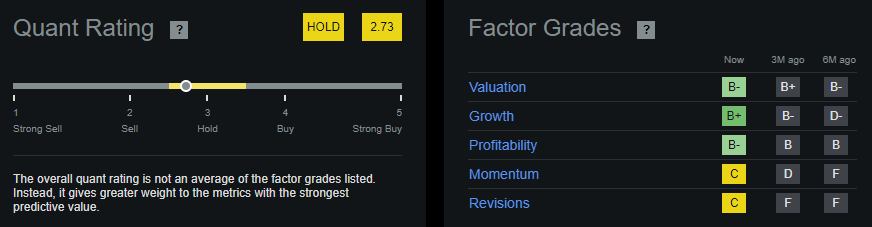

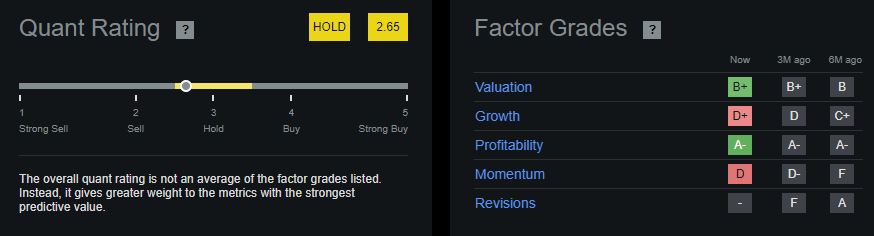

There is no real discernible difference between the two stocks when using Seeking Alpha's factor grades. Both stocks are currently rated as a "Hold", and both have in recent months steadily moved through the ranking from "Strong Sell" to "Sell" to their current rating of "Hold".

Concentrix does have more favorable momentum and growth factors, though, so slightly edges this contest.

Concentrix Factor Ratings (Seeking Alpha) Teleperformance Factor Ratings (Seekign Alpha)

{kind=link}

{kind=link}

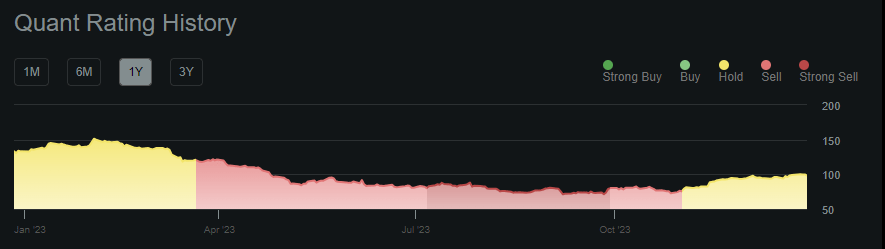

Concentrix's improved rating can be seen below, although the stock is still not rated as a buy at the moment.

Concentrix's Quant Rating History (Seeking Alpha)

{kind=link}

So what then has been the difference between these two stocks, in the same industry, with much of the same threats and drivers, over the last 6 months?

There could be a number of other contributors, such as the market's perception about each company's prospects post their recent acquisitions. Concentrix acquired Webhelp , while Teleperformance announced it was merging with Majorel .

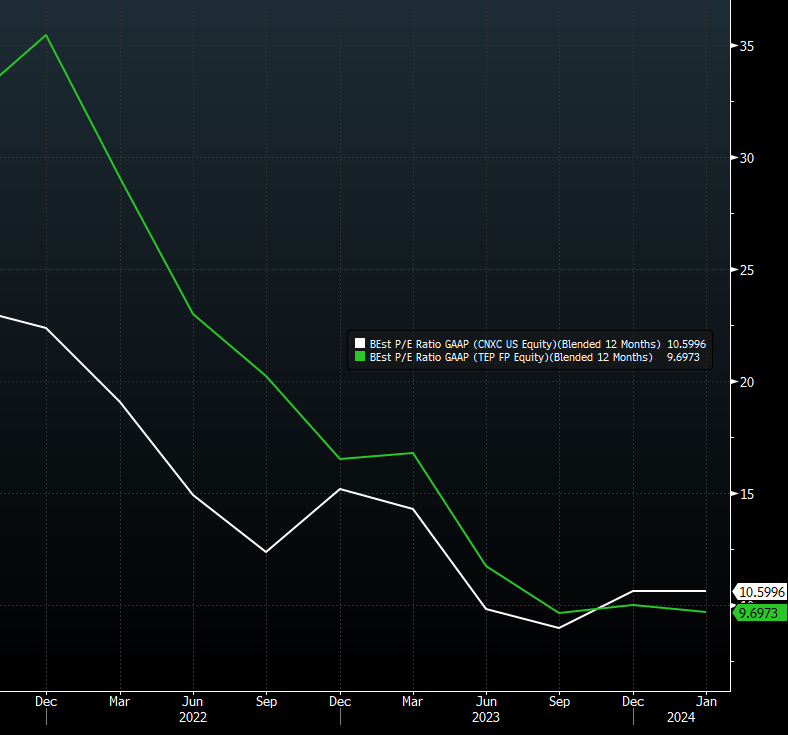

More likely, though, is that it is simply a case of their relative starting valuations. Post acquisitions, these are, in some ways (scale, industry and certain drivers, for example) fairly similar companies, so they should probably trade on multiples that are in the same ballpark. Up until very recently, this has not been the case, as can be seen in the graph below. At its peak, Teleperformance was trading on a forward earnings multiple North of 35x, while Concentrix didn't breach 25x over the same period.

The effect has been that Teleperformance had much further to fall in order to trade at a similar type of multiple, which is what we see today, with both companies now trading at roughly 10x forward earnings.

CNCX vs TEP forward PE Multiples (Bloomberg)

{kind=link}

In conclusion, where to from here?

Given all of the above, where does this leave us? Is there more upside left, or is it time to take some profits?

I believe there is still enough of a compelling argument in favor of Concentrix. Using the same valuation method as in my previous article, I believe there is still at least another 20% left, and those were fairly conservative estimates. After the recent rally, it is still only trading at a forward PE of 10x, with a PEG ratio of less than 1x - this is still bargain-basement territory, especially if you look at Wall Street Analyst estimates that revenue could grow at a CAGR of 19% over the next 3 years, while margins could expand by around 200 basis points. Concentrix also generates a lot of free cash, so servicing the higher debt load post-acquisition should not be an issue.

Of course, there are some threats in this industry, notably the relevance of this business given the emergence of AI, as well as slower project implementation by customers given a possible macro slowdown. I've previously made the case that AI could in fact be more of an enabler than a competitor to these companies, while tough economic times often lead to clients outsourcing more functions in an attempt to cut costs, which provides Concentrix with a small buffer in case a recession does come knocking.

Their full-year earnings report and guidance should provide a lot of context and insight into the year ahead, as well as updates regarding the integration with Webhelp. Given the market's skittish start to 2024, weak guidance will probably be punished, and some traders might consider taking some profits here. However, I believe that most metrics are trending in the right direction for Concentrix, and if they deliver a decent set of results, I do not plan on taking profits just yet.

For further details see:

Concentrix: More Room Left To Run