IBDSF - Consolidated Edison: Dividend Certainty Comes At A Premium Wait For A Lower Entry Point

2023-11-20 13:48:05 ET

Summary

- ConEdison is a utility holding company with three divisions, primarily serving the five boroughs of New York City.

- In 2022, it was the third best performing regulated utility in the US, with a 15.6% rate of return.

- ConEdison has a 49-year history of increasing its dividend, considered virtually guaranteed by investors, but the stock is often overvalued.

- I believe shares are overpriced by 10.0% today, but would be attractive under $81.00, a level last seen in October 2022. Wait for a discount.

Consolidated Edison (ED) is a utility holding company with three divisions: Consolidated Edison Company of New York ((CECONY)), Orange and Rockland Utilities Incorporated (O&R), and Con Edison Transmission Incorporated ((CET)). Con Edison of New York represents 92.5% of the company's assets; Orange and Rockland is next at 5.6%. Transmission is 0.6%. The company's primary market is the five borough of New York City and it claims its electric system is "the most reliable in the US." According to the Edison Electric Institute annual review, this was the third best performing regulated utility in the US, with a 15.6% rate of return for 2022, after PG&E ( PCG ) and Sempra ( SRE ). The current Fitch credit rating is BBB+ or medium investment grade. ConEdison has a market cap of $31.5 billion making it the ninth largest investor owned electric utility in the US, and shares have a Beta of 0.38, meaning they are considerably less volatile than the market as a whole.

Five Year Share Price (Seeking Alpha Charting)

{kind=link}

According to Forbes, the S&P 500 utilities sector is down 21.0% this year, the largest decline since 2008. That is not true for ConEd, however. Even when the Forbes article was written, the share price was only down 12.4% from its September 2022 peak of $100.85, the highest in the last five years. This is a popular stock, it is a crowded trade. There was, however, a strong buying zone between March 2020 and November 2021, when shares were consistently below $80.00. They bottomed at $65.65 on February 15, 2021. These opportunities do come along every once in a while, investors just have to be patient.

You Are Buying Dividend Certainty

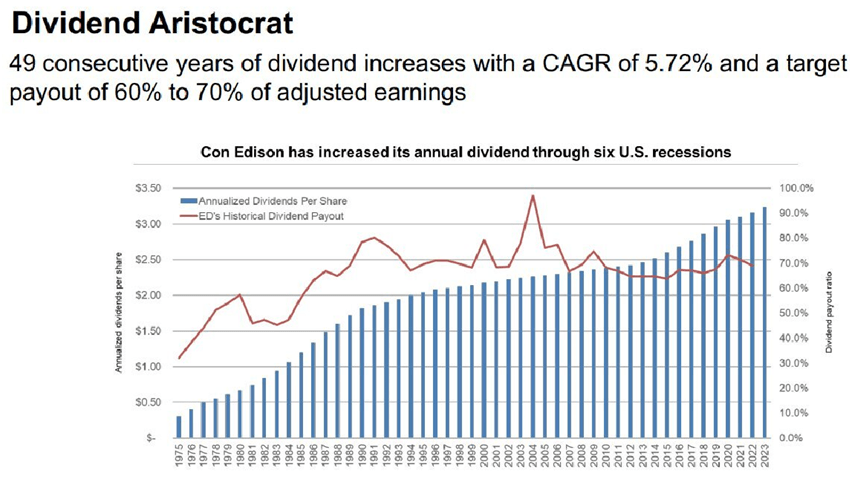

ConEdison is a component of the Standard & Poor's Dividend Aristocrat Index , meaning it has increased its dividend for at least the last 25 consecutive years. According to its Investor Relations ConEd "has increased its dividend for 49 consecutive years," and paid its first dividend in 1962. Atmos Energy ( ATO ) and NextEra Energy ( NEE ) are the only other utilities on the Dividend Aristocrats list. Atmos has increased its dividend for 40 years, while NextEra has increased its dividend for 28 years.

ConEdison's dividend never seems to be as high as investors would like, but it always arrives on time and its increases every year. The current dividend yield is 3.55% and the quarterly dividend was just paid on November 14. The next increase will be in February 2024. Forbes stated that for "the last 15 years, utility yields have been 1.05% higher than the 10-year Treasury yield." That is no longer the case; the average yield in the sector is 4.0% while 10-year Treasuries are at 4.44% and 3-month treasuries are at 5.39%. While ConEd is paying 3.55%, the yield of some of its peers by comparison are Southern Company ( SO ) at 3.98%, Duke Energy ( DUK ) at 4.51%, NextEra ( NEE ) at 3.26%, American Electric Power ( AEP ) at 4.55%, and Sempra ( SRE ) at 3.29%. The dividend history since 1975 is presented below.

Dividend History (2023 Investor Presentation)

{kind=link}

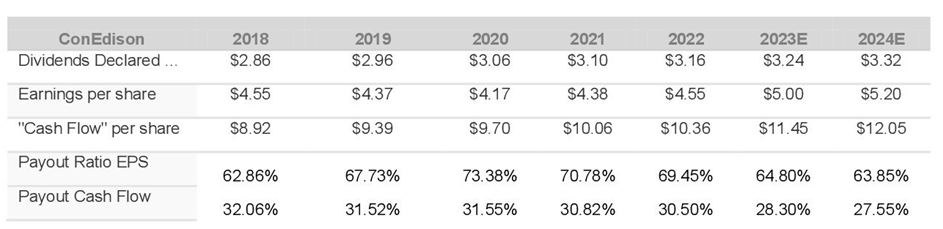

While the long-term compound annual growth rate of the dividend may be 5.72%, I calculate the dividend growth over the last 10-years to be slower at 2.79%. The payout ratio has consistently been within the company's targeted 60.0-70.0% range. There may be some dividend upside now with the recent ConEd New York rate increases, which will take effect in 2024.

Payout Ratio Over Time (Value Line and Author Calculated)

{kind=link}

Shares Are a Buy Below $81.00

The most recent consensus EPS was revised upward to $5.00-$5.10 per share (non-GAAP) in the third quarter , from $4.90 to $5.00 in the prior quarter. Management's annual growth target for earnings is 5.0-7.0% over the long term.

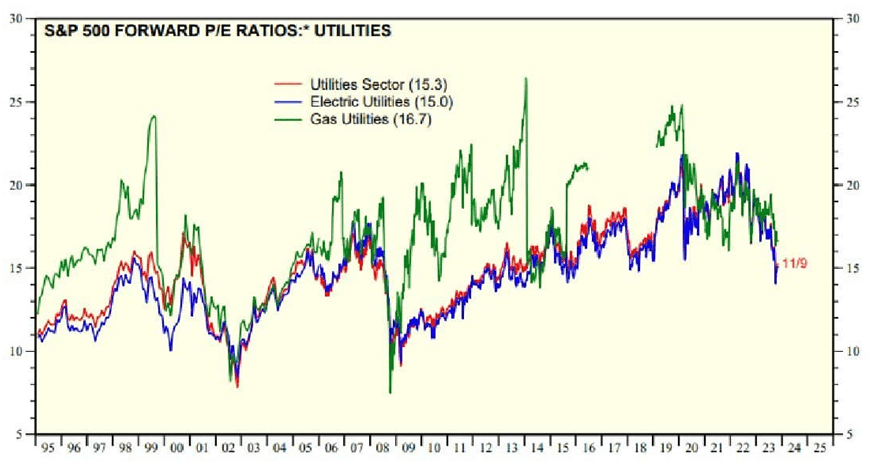

I have used three different approaches to value ConEd's shares: a P/E ratio based on comparable utilities, a discounted cash flow and a dividend discount model ((DDM)). This year has been a tough environment for utilities and it was deemed the "worst performing sector " by Investor's Business Daily. Gabelli Funds compiles a Mid-Year Update for the utilities sector and reported "Electric utility valuation multiples have declined from 23x forward earnings in early 2020 to 17x 2023 and 16x 2024 earnings estimates." Over the last 25 years, the median P/E multiple was reported by Gabelli as 17.1x.

The most recent investor survey is from Yardeni Research and is dated November 16, with data through November 9th. The indicates that P/E multiples are still being compressed and that electric utilities now have an overall multiple of 15.0x, while gas utilities are 16.7x and the overall utility sector is 15.3x earnings. These numbers are all down from last month.

Current Utility Multiples (Yardeni Research)

{kind=link}

Using the 2024 forward non-GAAP earnings per share estimate of $5.20 with the overall utility multiple of 15.3x (ConEd is electric and gas) the calculation is $5.20 x 15.3 = $79.56.

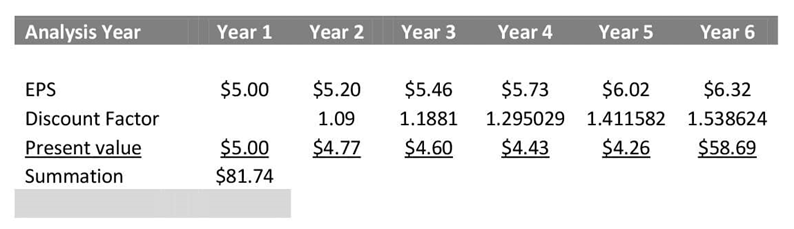

I have also used a discounted cash flow to value shares. The consensus estimates were used for earnings in 2023 and 2024, and then grown at a 5.0% annual rate, in line with management projections. I have used 9.0% for the discount rate, slightly lower than the S&P 500 average return over time, estimated at 9.8% , with a reversion rate of 7.0%; these numbers are based on ConEd's stability and strong balance sheet. Here the value generated was $81.74.

Discounted Cash Flow (Author Calculated)

{kind=link}

I have also used a dividend discount model to value shares (here the Gordon Growth Model ), which needs an estimate for next year's dividend, a future dividend growth rate and a return on equity. Below is a chart of ConEd's return on equity for the last five years, which averaged 7.46%. I am estimating the company's next dividend as $0.83 per quarter as it seems to go up $0.02 per year recently. The calculation now would be ($0.83 x 4)/(0.0746-.035) = $83.84. I have assumed a higher dividend growth rate of 3.5% in the future, given recent favorable regulatory approvals which may be passed on to shareholders.

Discounted Cash Flow (Morningstar)

{kind=link}

The three valuation results are $79.56, $81.74, and $83.34, a spread of 4.8% and an average of $81.55. So let's say shares would be a buy below $81.00. At this price the dividend would be 4.0%.

ConEd Also Sells Steam and Gas

ConEd operates the largest steam system in the world, serving numerous (more than 1,500) buildings in New York. The territory is from the southern end of Manhattan northward to 96th Street. The steam is generated in Manhattan and there are five plants. The steam travels under the city streets to heat and cool properties in the city. Steam operations started in 1882 and they have the advantage of being environmentally friendly. In addition to steam, ConEdison sells natural gas to customers in the five boroughs of Manhattan as well as Orange and Rockland counties. For CECONY gas is about 25.0% of revenues, while steam is 5.0%. For O&R, gas is 30.0% of total revenues. CECONY serves 3.6 million electric customers, and 1.1 million gas customers. O&C serves 300,000 electric customers and 100,000 gas customers.

The Regulatory Environment is Positive, for Now

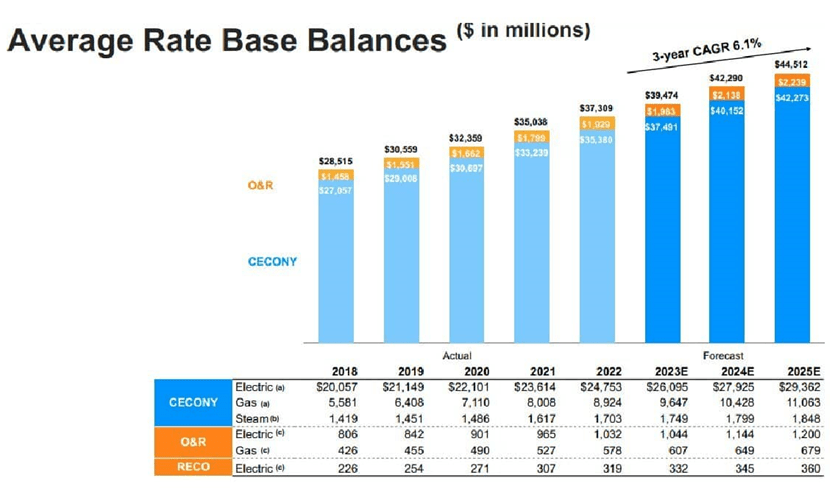

All divisions of ConEdison are regulated by the New York State Public Service Commission ((NYSPC)). There are only a few utilities operating in New York State besides ConEd and they include National Grid ( NGG ), Avangrid a subsidiary of Iberdrola ( IBDSF ), National Fuel Gas ( NFG ) and CH Energy a subsidiary of Fortis ( FTS ). In New York, Rates are "usage decoupled"- so revenue is not affected if delivery volumes go down. Decoupling is a system environmentalists like and it tends to reduce the utility's risk from changing weather or economic conditions, which is favorable for investors. ConEd forecasts the annual rate base growth rate for the next five years as 6.1%, and the rate base has been established through 2025.

Most of the electricity sold to consumers by ConEdison is purchased from New York Independent System Operator ((NYISO)), which administers New York's wholesale energy markets. This year, regulators approved the new Consolidated Edison Company of New York rate base with $11.8 billion of additional capital and a return on equity of 9.25%. The prior allowed return on equity was 8.8%. The company also was granted a steam rate plan with a 9.25% allowed return on equity and a "weather normalization mechanism."

ConEd Rate Base Over Time (2023 investor Presentation)

{kind=link}

Recent Earnings Performance

In 2022, ConEdison had adjusted earnings per share of $4.57, up 4.1% from $4.39 in 2021, which was up 5.0% from 2020. Income for the company was very consistent even though the New York area had one of its warmest winters ever with February temperatures in the 60s. This is one of the benefits of rates being decoupled from usage, and December 2023 is forecast to again be warmer than average . Earnings per share are forecast to grow another 9.0% for 2023, with the most recent consensus EPS revised upward to $5.00-$5.10. In the third quarter 2023, the most recent results reported, non-GAAP earnings were $1.62, down slightly from $1.63 in the prior year. GAAP earnings per share were $1.53, down from $1.73 the prior year.

Shift to Renewables

There are several sets of environmental hurdles set for ConEdison. The first are the goals set by the State of New York Climate Council's Climate Act , approved in 2022. The benchmark here is set at 1990 emissions levels, with reduction targets of 40.0% by 2030 and 85.0% by 2050. The second set of goals was set in the Inflation Reduction Act , which created new emissions levels for utilities, with a benchmark based on 2005 emissions. This legislation called for reduction of greenhouse gasses of 40.0% by 2030 and net zero emissions by 2050. ConEdison has set an aggressive target of 70.0% renewable power by 2030, with a 40.0% reduction in greenhouse gases from 1990 levels, in line with New York requirements.

In the shift toward renewables, ConEdison hopes to have 6.0 gigawatts of solar by 2025. By 2035, it is planning for 9.0 gigawatts of offshore wind. It has a 10-year plan with an overall budget of $72.0 billion to be spent on clean energy and maintenance of existing infrastructure. About $14.6 billion of this will be spent in the next three years. There are currently two wind projects underway, Community Offshore Wind for Brooklyn and Excelsior Wind.

Ironically, at the beginning of 2023, the company sold its wholly owned subsidiary, ConEdison Clean Energy Businesses for $6.8 billion. This part of the utility was not regulated and ConEdison used the proceeds to pay down debt, so the parent holding company no longer has any long-term debt. After tax, the company earned about $2.24 per share on this transaction.

Near Term Capital Expenditures (Q3 Report)

Long-Term Debt

Long-term debt as of the end of 2022 was $20.15 billion or 29.2% of total assets, and as of year-end 2021, it was $22.60 billion or 32.6% of total assets. In 2020, long-term debt was $20.38 billion and 32.4% of total assets, while in 2019 it was $18.52 billion or 31.9% of total assets. So over time, long-term debt has held steady or declined slightly. ConEdison's levels of debt are considered reasonable and manageable.

Risks to Outlook

The risk that most utilities have faced over at least the last two years is warmer weather, which means lower revenues. However with a usage decoupled rate structure, this is not an issue of concern for ConEdison. Regulatory risks seem to be limited these days and ConEd appears to operate in a utility-friendly environment. However it is always possible that this could change. Another risk would be the possibility of more rate hikes from the Federal Reserve, as interest carrying costs do reduce the company's net income.

Conclusion

Consolidated Edison is the electric and gas utility of New York City, the largest US Metropolitan area. It has no real competition in the markets it serves. It is one of three utilities on the Dividend Aristocrats list, but it is the one that has by far the longest track record of increasing its dividend - 49 years. If you are a dividend investor you are attracted to this stock for the continuity of its dividend payout and the prospect of some future dividend growth. Over the long-term the compound annual growth of the dividend has been 5.72%, generally exceeding the rate of inflation. For the last 10 years, I estimate that it has been closer to a 2.79% per year dividend increase, below the rate of inflation. But inflation has cooled to just over 3.0% this October, making the disparity a bit less. ConEd is a great long-term buy for dividend investors and it has a place in most portfolios. You just need to find the right entry point and right now that is a price below $81.00, which was available in February 2020 through November 2021, and before that in January of 2018 through February of 2019, both long stretches of time. Right now the share price is above $91.00. As Warren Buffett has said: "The stock market is a device to transfer money from the impatient to the patient." You just have to be patient for ConEd to enter buy territory.

For further details see:

Consolidated Edison: Dividend Certainty Comes At A Premium, Wait For A Lower Entry Point