ROAD - Construction Partners: A Road To Profits

2023-08-24 09:21:35 ET

Summary

- Construction Partners is a growth company in the construction industry, specializing in roadways and infrastructure.

- The company has achieved attractive revenue growth through acquisitions and growth in organic demand for its products and services.

- Despite some volatility in profitability and costs, the company's long-term growth prospects and government funding support make it a favorable investment.

I don't know about you, but when I think of the concept of a growth company, usually my mind goes to many of the technology companies that are out there today. However, some of the most interesting growth prospects on the market involve companies that operate in less exciting industries. One great example that I could point to is a firm called Construction Partners ( ROAD ). In recent years, management has achieved attractive growth, both through organic means and by completing multiple acquisitions. Shares are not exactly the cheapest. But on the whole, the company does look decently priced and growth looks set to continue. Given these facts, I would argue that the firm represents a soft 'buy' prospect that investors who like some growth should be aware of.

An interesting road to travel

If you haven't guessed it by now after looking at the ticker symbol for Construction Partners, the company's primary operations center around the construction and maintenance of roadways in the states in which it operates. As of the end of its 2022 fiscal year, the company had a physical presence in Alabama, Florida, Georgia, North Carolina, and South Carolina. In these states, the business provides products and services to both public and private customers, with the primary emphasis on highways, roads, bridges, airports, and both residential and commercial property developments. In addition to constructing the roads, the company also produces the hot mix asphalt, as well as other products, that are involved with said construction. Its work touches on things like the installation of utility and drainage systems, the act of providing mining aggregates like sand and gravel, and more.

{kind=link}

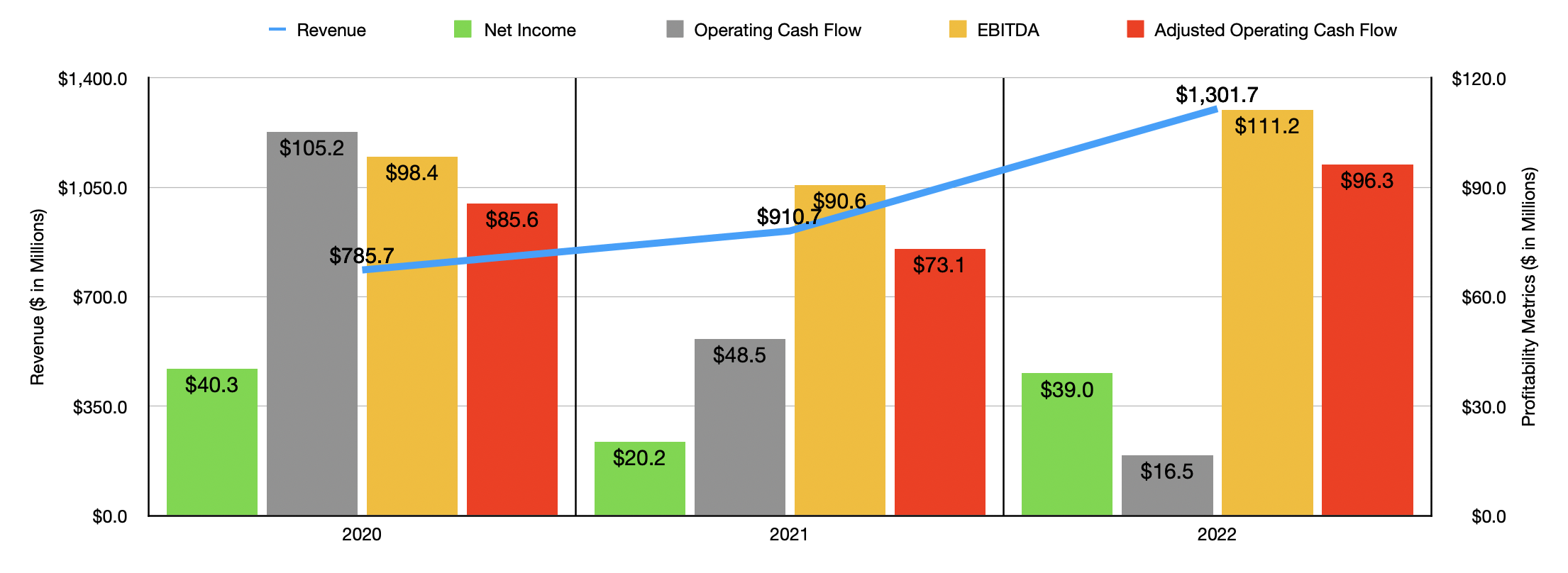

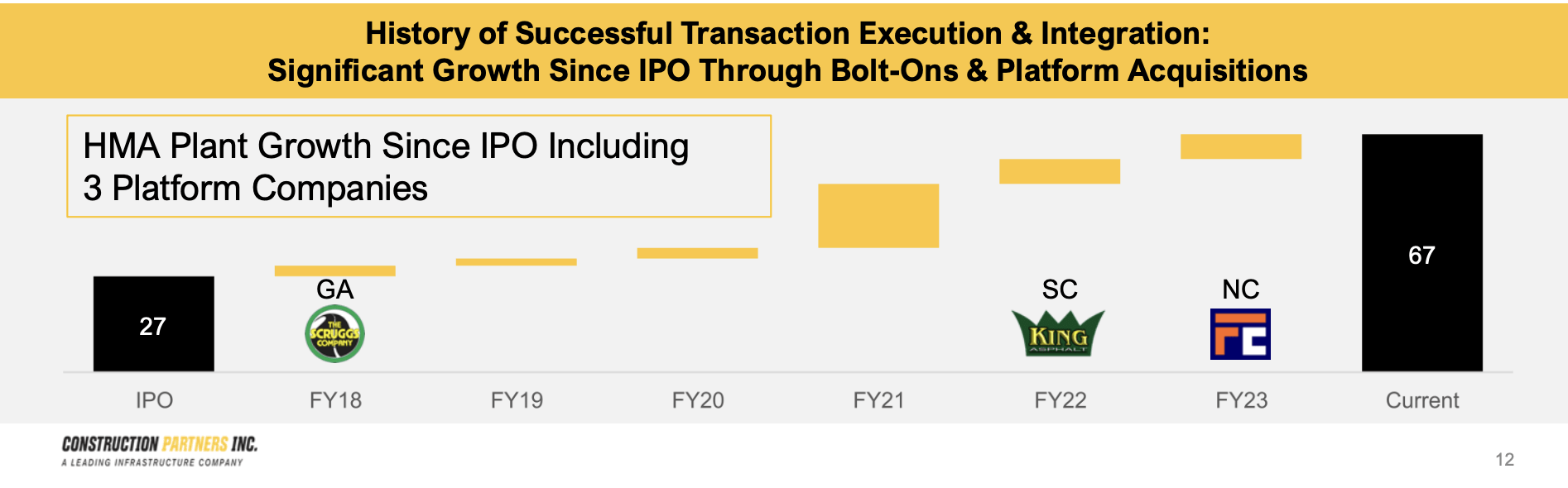

Over the past three completed fiscal years , revenue for the company has shot up. Sales went from $785.7 million in 2020 to $1.30 billion in 2022. This corresponded with a surge in backlog from $608.1 million to $1.41 billion. According to management, the increase in revenue was driven by a couple of factors. Let's look, for instance, at the picture between 2021 and 2022. During that year, overall revenue jumped $391 million, or 42.9%. $170.4 million of this revenue was driven by acquisitions completed during or subsequent to the 2021 fiscal year. However, the largest share of the revenue growth, the remaining $220.6 million, was driven by more contract work and sales of products like hot mix asphalt and aggregates that it made available to third parties. Speaking of acquisitions, the company does have a history of growing by means of purchasing other properties. In fact, since going public in 2018, the company has completed 24 different acquisitions as of the end of the most recent quarter. That has allowed it to grow to 67 asphalt plants compared to the 27 that it had when it first went public.

{kind=link}

Even though you would think that bottom line results improved significantly during this time, that's not exactly what transpired. Net income dropped from $40.3 million in 2020 to $20.2 million in 2021. In 2022, it rebounded mostly, coming in at $39 million. Higher interest expense has been partially responsible for this. But what has been even more problematic has been the rising costs that the company has had to deal with. Even though profits rebounded in 2022, the firm's overall gross profit margin shrank from 13.2% to 10.7%. That was driven by higher raw material costs, fuel, labor, trucking, and other items. Other profitability metrics have been rather volatile as well. Fortunately, the overall trend for adjusted operating cash flow and EBITDA has been positive. But it certainly has not kept up with the growth in sales.

{kind=link}

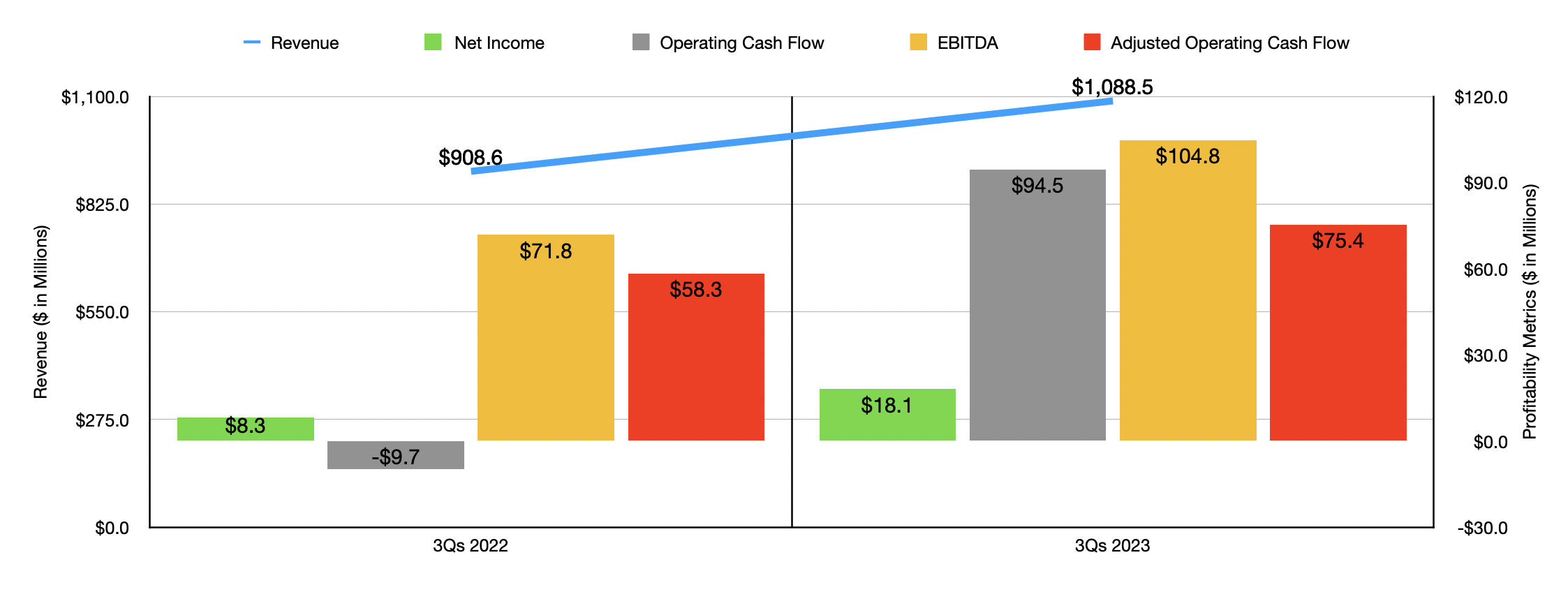

For the current fiscal year, management has demonstrated continued growth. Revenue of $1.09 billion in the first nine months of the 2023 fiscal year was 19.8% above the $908.6 million the company reported one year earlier. $91 million, or 50.6%, of this growth was driven by acquisitions. Meanwhile, $88.9 million of the growth was driven by organic means because of greater contract work and higher sales of hot mixed asphalt and aggregates to third parties. As you can see in the chart above, profitability has improved significantly year over year. The completion of a new backlog that brought with it more favorable margins, as well as optimization initiatives implemented by management, coalesced to push margins up. Net income more than doubled from $8.3 million to $18.1 million. And the other profitability metrics for the company also improved nicely.

{kind=link}

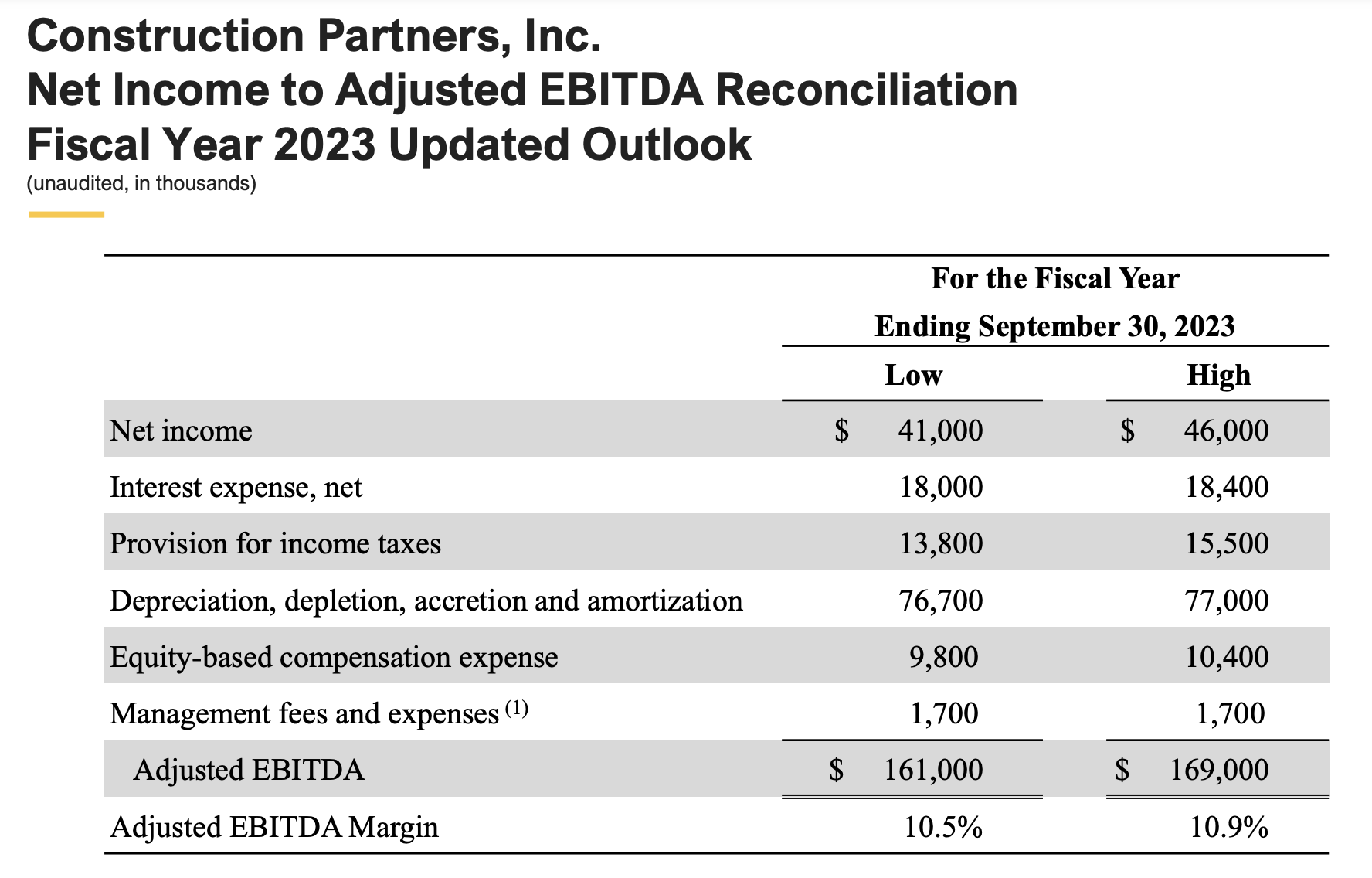

When it comes to the near-term outlook, the picture for the company is definitely positive. Management is forecasting revenue for 2023 of between $1.535 billion and $1.555 billion. At the midpoint, this would be 18.7% above the $1.30 billion reported for 2022. Net income is supposed to come in slightly higher than it was last year between $41 million and $46 million, while EBITDA should be between $161 million and $165 million. No guidance was given when it came to operating cash flow. But if we work backward with the guidance management did give, using the midpoint for EBITDA to start with, we should end up with a reading of roughly $130.5 million.

{kind=link}

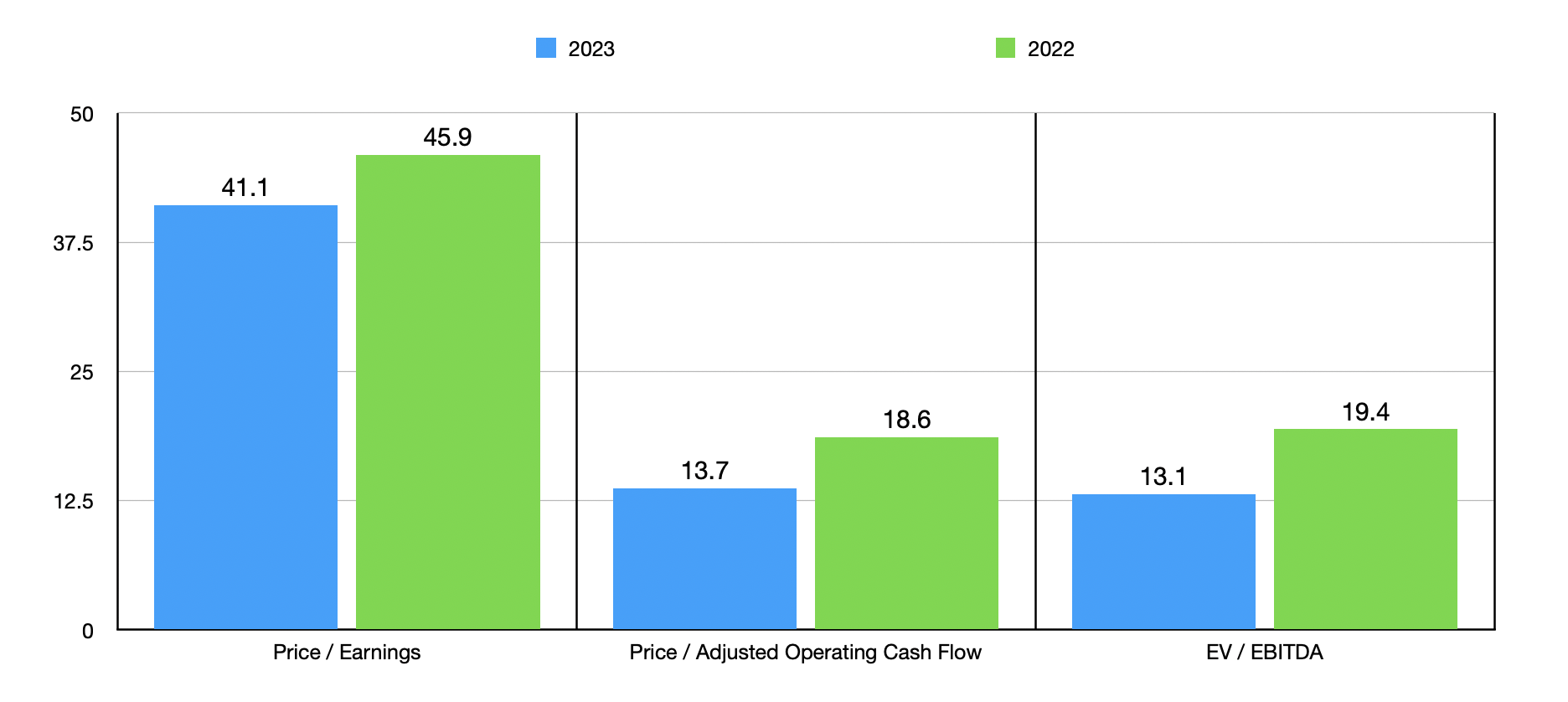

In the chart above, you can see how shares are priced both on a forward basis and using data from 2022. On a forward basis, shares of the company do look quite affordable from a cash flow perspective but. Though it is true that, from an earnings perspective, the stock looks very expensive. In the table below, meanwhile, you can see how shares are priced compared to similar firms. On a price to earnings basis, four of the five companies I looked at were more expensive than it. This drops to one of the companies if we rely on the price to operating cash flow basis, while the EV to EBITDA multiple results in three of the five companies being cheaper.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Construction Partners |

| 41.1 |

| 13.7 |

| 13.1 |

| Granite Construction ( GVA ) |

| 40.9 |

| 47.8 |

| 13.9 |

| Primoris Services Corp. ( PRIM ) |

| 14.9 |

| 19.8 |

| 8.5 |

| MYR Group ( MYRG ) |

| 27.0 |

| 19.4 |

| 13.0 |

| Sterling Infrastructure ( STRL ) |

| 19.9 |

| 6.7 |

| 10.3 |

| Ameresco ( AMRC ) |

| 45.7 |

| N/A |

| 24.4 |

Even though shares of the company are not as cheap as I would like them to be, the firm does seem to have significant potential in the long run. For starters, in the markets in which the company operates, score very poorly in terms of their current quality. And the great thing is that 94% of them are paved with asphalt, so the business does have some nice growth prospects here. In addition to this, they also have fuel to capture some of this potential. I say this because existing state and federal funding aimed at supporting this kind of work over the next five years totals $47 billion across the six states the company has a presence in.

Construction Partners

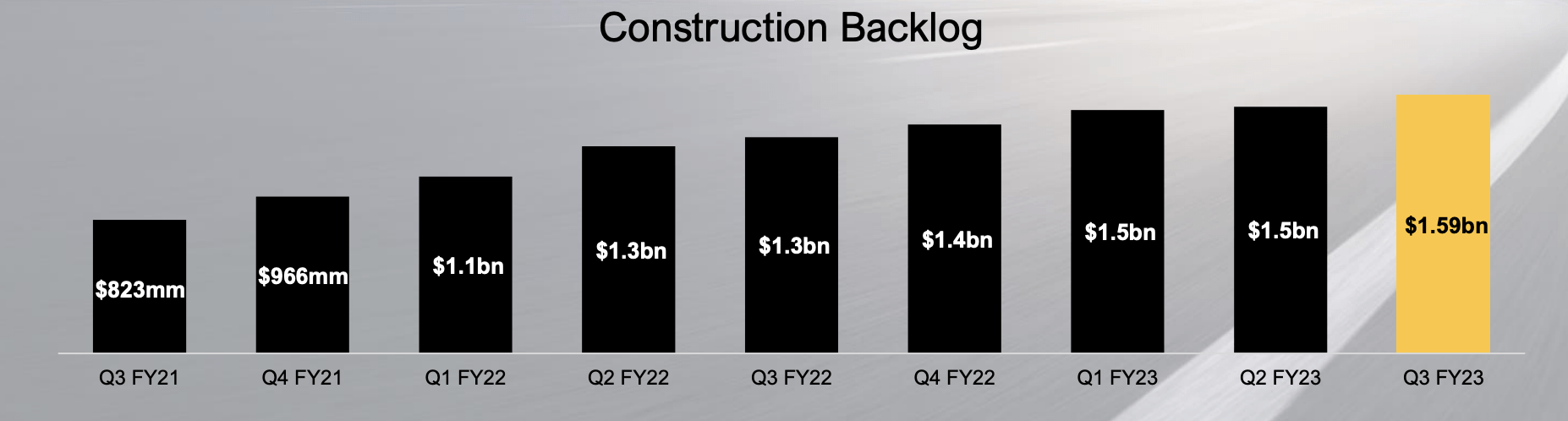

And over the next five years, the population in those states is expected to grow by about 6% compared to the paltry 2% forecasted for all other states combined. The really exciting thing about this is that the growth prospects continue to show up in the form of increasing backlog for the company. As of the end of the most recent quarter, the backlog was $1.59 billion. That is up from the $1.52 billion reported one quarter earlier, and it is 19.5% above the $1.33 billion the company reported in the third quarter of 2022.

Construction Partners Construction Partners

{kind=link}

Takeaway

Truth be told, there's not a lot about Construction Partners that I dislike. I don't like how volatile profitability and cash flows have been in recent years, and I would prefer that the stock was cheaper than it currently is. But outside of that, I like a lot of what I have seen. Growing revenue, continued growth in backlog, and government funding that should result in further growth for the company, give me plenty of reasons to like the business. Given this combination of factors, I have decided to rate the firm a soft 'buy' at this time.

For further details see:

Construction Partners: A Road To Profits