ROAD - Construction Partners: Building Future Wealth With Robust Growth And Strategic Vision

2023-12-25 04:46:45 ET

Summary

- Construction Partners is a civil infrastructure company that offers comprehensive solutions in the southeastern United States.

- I rate shares as "Buy" with a fair value of $53.26/share.

- In my opinion, the positive factors outweigh the challenges, and I hold a high degree of optimism regarding the management's execution capabilities.

Company Description

Construction Partners ( ROAD ) - Industrials - Construction and Engineering

Established in 2007, Construction Partners (“the company”) is a civil infrastructure company that offers a comprehensive, vertically integrated solution. This solution encompasses activities ranging from manufacturing and distributing HMA to paving and site development, including the installation of utility and drainage systems. The company's solutions cater to public (?63% of 2023 sales) and private (?37% of 2023 sales) sectors, primarily focusing on operations in the southeastern United States.

At the core of Construction Partners' mission is the commitment to building and maintaining transportation infrastructure that not only fosters connectivity but also enhances communities.

Management

The management team appears well-suited for Construction Partners, bringing a mix of leadership, financial expertise, industry experience, and a commitment to industry associations. Their diverse backgrounds and track records suggest a strong foundation for the company's success in the construction sector.

1. Jule Smith – CEO:

- Chief Executive Officer, since March 31, 2021.

- Former President at Fred Smith Company.

- Extensive career in highway construction.

- U.S. Navy veteran, active in NC Chamber.

2. Greg Hoffman – CFO:

- Experienced CFO since April 2023.

- Previous roles include SVP, and CFO at Wiregrass Construction Company.

- Background in heavy civil infrastructure and auditing.

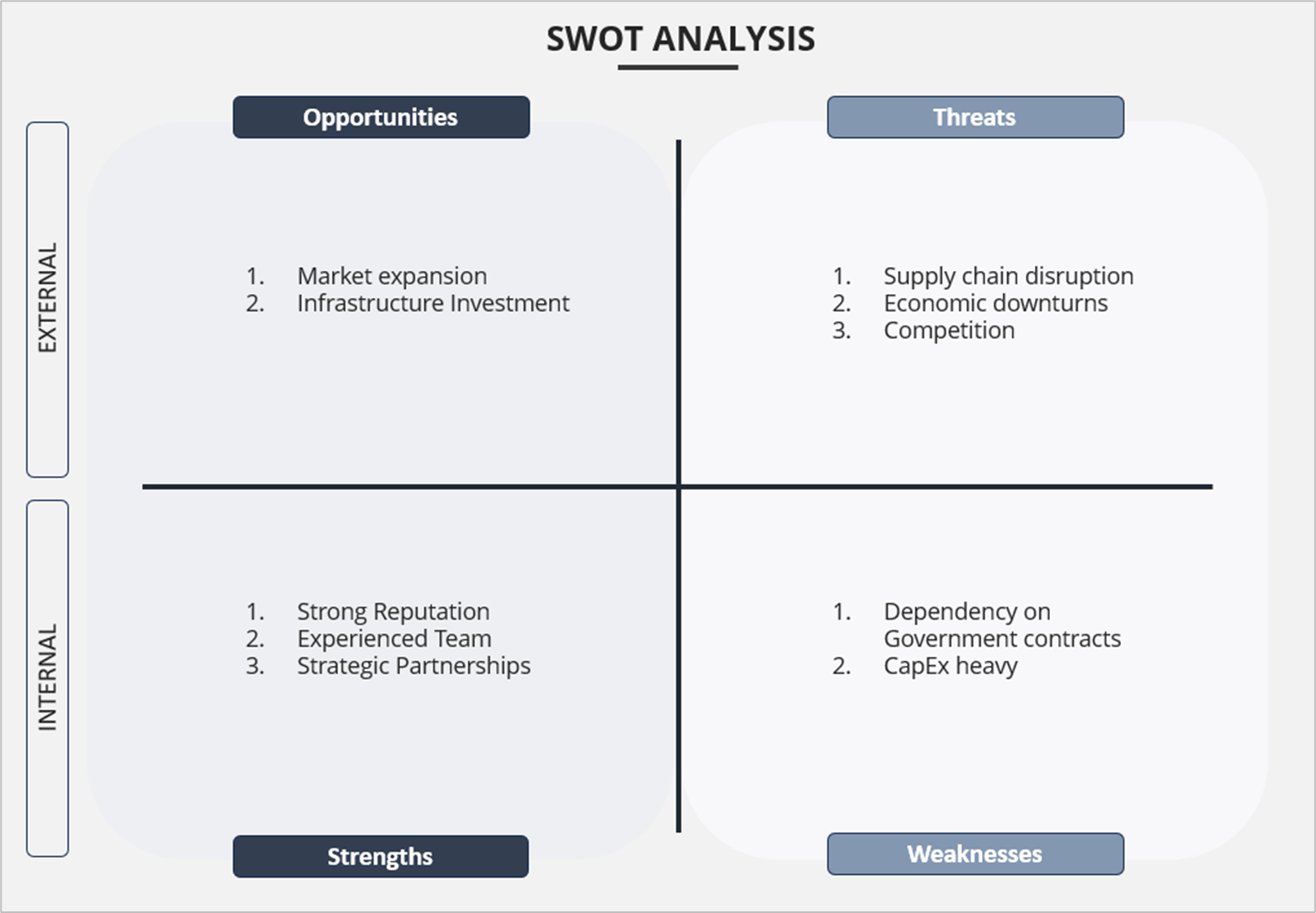

Swot Analysis

Here is a breakdown of SWOT analysis:

{kind=link}

Author's Estimates

Business Performance

Classification - High Growth (i.e., Peter Lynch classification)

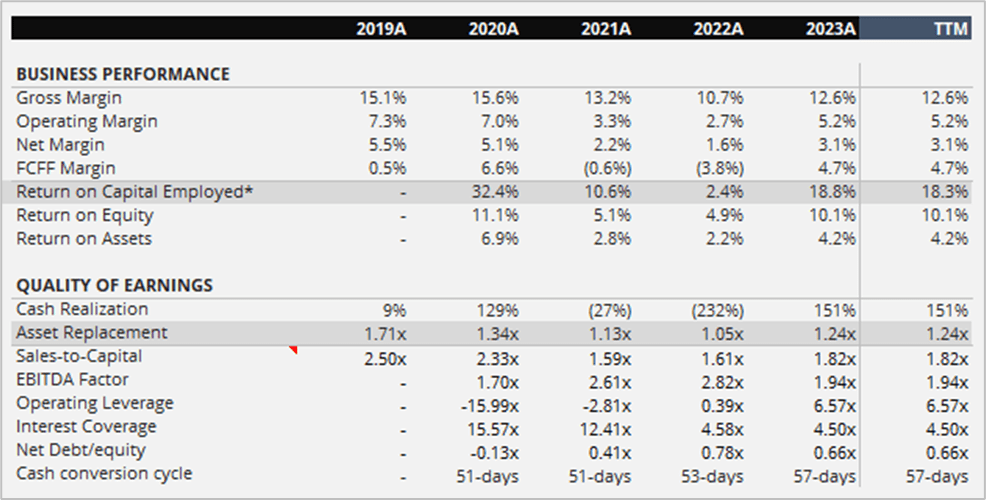

Construction Partners is a capital-heavy (i.e., EBITDA factor of 1.94x TTM) business that, over the last four years, delivered an average ROCE of 16.1% and an average ROE of 7.8% primarily driven by financial leverage expansion.

{kind=link}

Author's Estimates

Income Statement

From 2019 to 2023, the top-line grew at a CAGR of 18.9% driven by both organic and acquisitions growth. The latter, in particular, represents one of the key growth levers for Construction Partners. The company aims to consolidate the highly fragmented asphalt paving materials and services segment, characterized by thousands of local operators.

{kind=link}

Author's Estimates

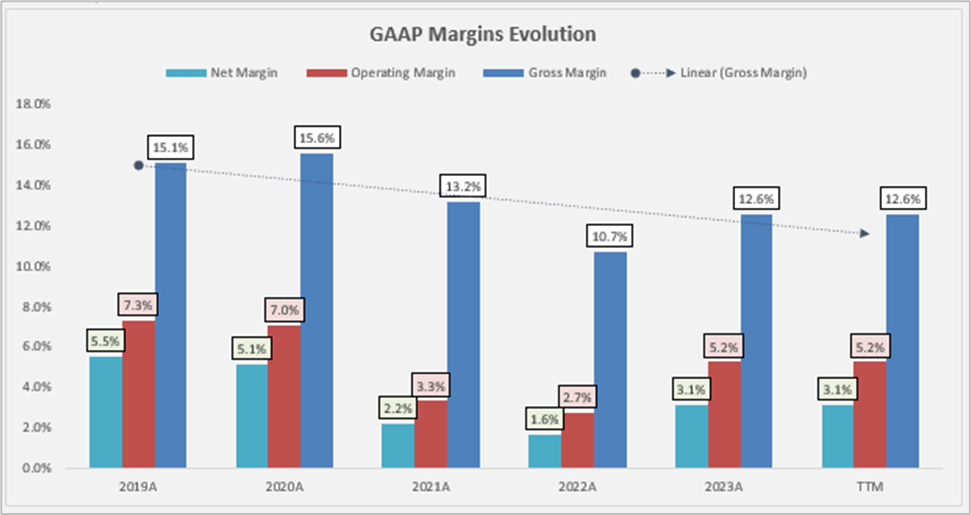

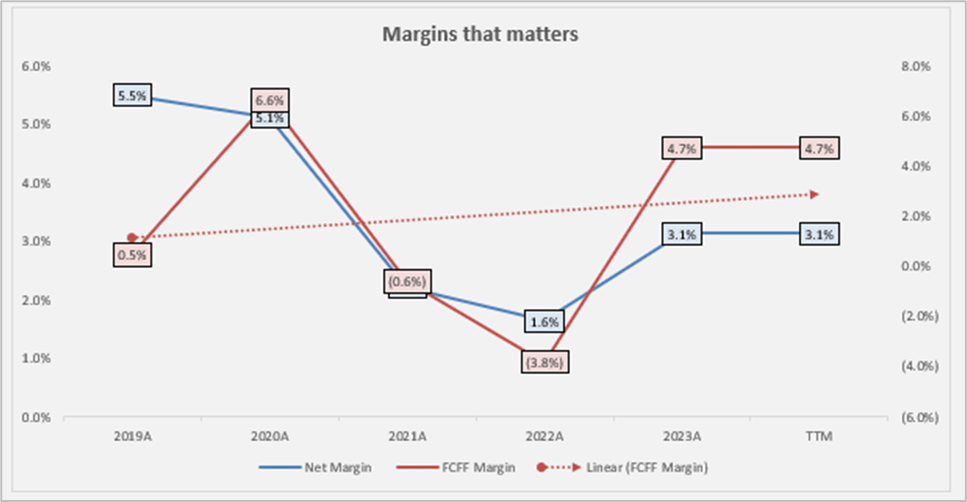

As evident from the chart above, margins, especially in the period of 2021A to 2022A, have faced significant pressure. This was primarily due to a combination of factors, including increased energy costs, inflation (leading to lower profit margins on the pre-inflationary backlog), and challenges on the labor front.

Balance Sheet

The balance sheet is solid with an Interest Coverage ratio of 4.50x TTM. The cash conversion cycle stands at 57 days TTM (above the historical 3-year average of 51 days), driven by lower turnover in A/R standing at 73 days (up from the historical 3-year average of 66 days) suggesting weakness on the demand side (in my opinion, likely on the private projects side); partially offset by lower turnover in A/P and an in-line inventory turnover currently standing at 21 days (vs historical 3-year average of 20 days).

{kind=link}

Author's Estimates

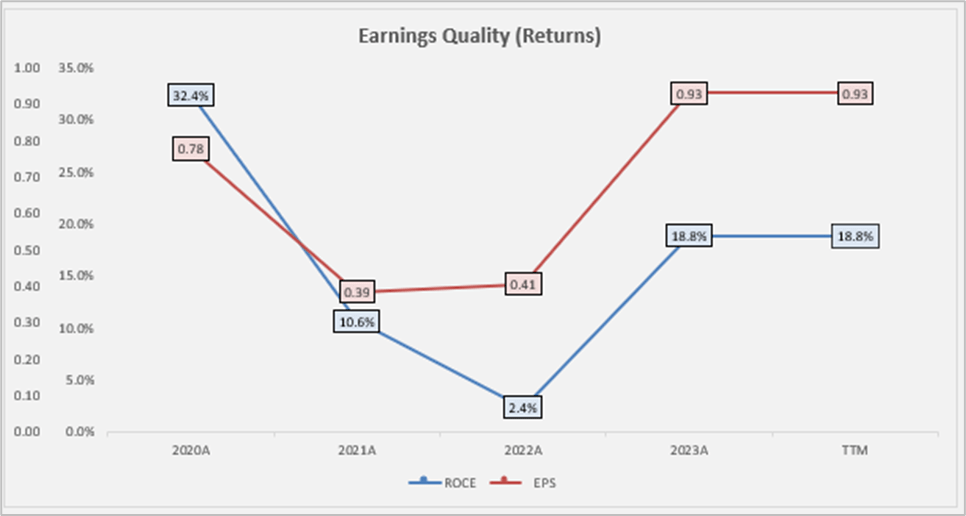

On the performance side, both ROA and ROE are normalizing toward the historical norm and are currently standing at ?4.2% and ?10.1% (above the cost of equity of ?10.7%) respectively. In particular, ROE is driven by higher financial leverage and total asset turnover, partially offset by lower net margins. A ROE driven by higher financial leverage is not inherently unfavorable unless the company is making investments with an ROE lower than the cost of equity. Fortunately, this is not the case for Construction Partners. Additionally, to mitigate unnecessary risks, Construction Partners has entered into an interest rate swap, set to expire on June 30, 2027. This swap has secured a fixed interest rate of 3.1%, which is well below the prevailing market interest rate.

Cash Flow Statement

The business is capital-heavy, with maintenance CapEx averaging ?3.25% of sales per annum and total CapEx averaging ?5.0% over the last 5 years. Here, some might contend that, given Construction Partners' highly acquisitive nature, business acquisition costs should be treated as capital expenditures (CapEx). While I acknowledge this viewpoint, I still lean towards maintaining a clear distinction between the two.

{kind=link}

Author's Estimates

On the cash flow generation side, the performance is quite volatile due to working capital items, in particular changes in A/R. Nonetheless, the cash conversion stands at ?151.4%, CFO-to-Net-Income at 3.21x (vs 4-year average of 1.77x), and FCFF margin at ?4.7% TTM. Overall, it is a cash-generative business. In relative terms, when comparing the FFCF trends of Construction Partners with those of its peers, it paints a more favorable picture compared to similarly sized players like Granite Construction ( GVA ). However, it lags behind larger players such as Sterling Infrastructure ( STRL ). In my perspective, the company is poised to enhance its margins in the future, owing to a strategic blend of vertical integration and economies of scale.

Valuation

Construction Partners trades at a discount to its intrinsic value, both on an adjusted and unadjusted basis.

{kind=link}

Author's Estimates

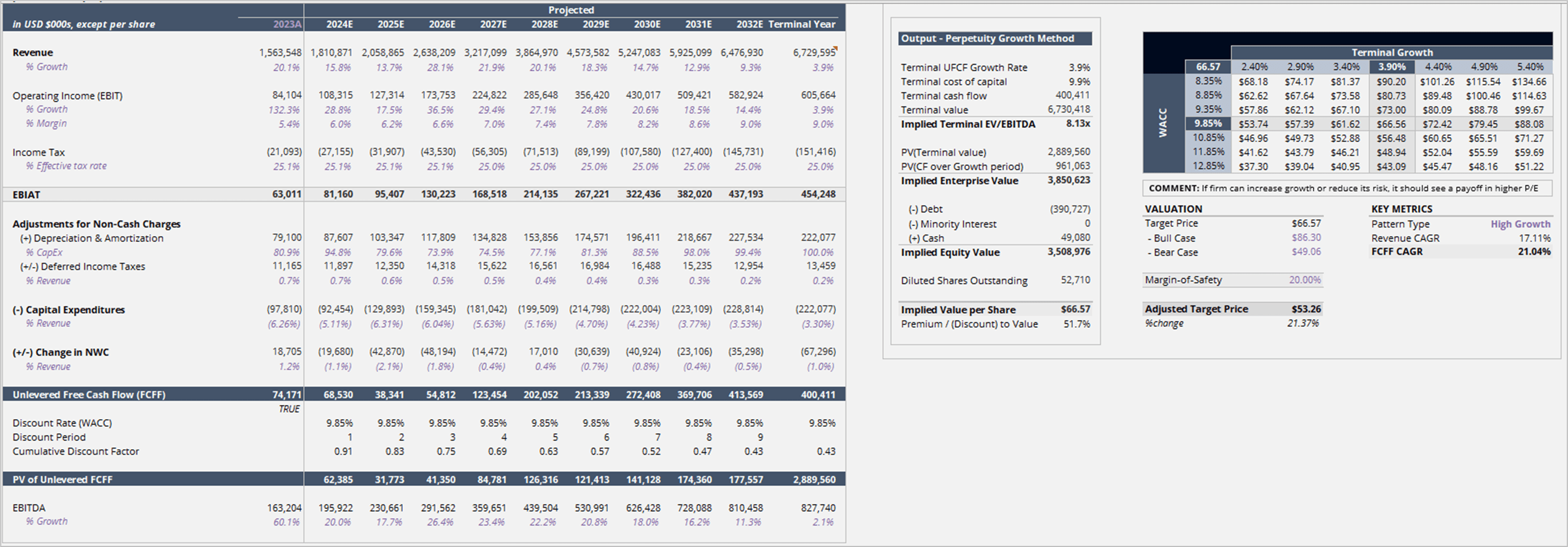

Under my conservative scenario, and incorporating a margin of safety of 20%, it suggests a target price of $53.26/share or a discount of 21.36% vs. the current price of $ 43.88/share.

Over the next 10 years, I assume sales will grow at a CAGR of ~17.11%, which is below the historical CAGR of ~25.78% over the last 4 years. I anticipate that sales will be predominantly influenced by volume. Regarding profitability, I expect margins to expand by an average of approximately 0.40% per annum. This growth will be fueled by a blend of factors, including vertical integration—illustrated by the recent completion of a new liquid asphalt terminal in North Alabama—and operating leverage.

Catalysts

In my opinion, the following should represent a potential tailwind:

- Infrastructure Investment and Jobs Act (IIJA) - represents a multi-year tailwind for companies involved in construction, engineering, and related industries.

- Strategic Acquisitions and Expansion of Services in existing markets - which would strengthen the company's market position, enhance competitiveness, and capitalize on existing customer relationships to boost organic growth.

- Quantitative Easing - lower interest rates would enable the company to leverage cheap capital for expansion and growth opportunities.

- Better than expected weather conditions.

Risks

There are a significant number of headwinds with the stock. In particular, issues by segment are:

- Inflationary trends - upward pressure on wages and in the cost of raw materials used to produce HMA, such as liquid asphalt and aggregate materials may negatively affect profit due to a limited company’s ability to pass through increased costs for projects already in its backlog.

- Worse than expected weather conditions – as the activities are conducted outdoors, the operations can be negatively impacted by adverse weather conditions, including prolonged snow, rain, or cold weather.

- High dependence on publicly funded projects - changes in government spending priorities, budget cuts, or delays in project approvals can negatively impact the business.

- Lack of workforce in the construction industry.

Final Remarks

In my opinion, Construction Partners represent an attractive investment, providing a sufficient margin of safety on both an adjusted and unadjusted basis.

Long-term analysis indicates that the company is well-poised for strong performance. In my opinion, the positive factors outweigh the challenges, and I hold a high degree of optimism regarding the management's execution capabilities. I anticipate sustained growth in both top-line and bottom-line results through a strategic blend of organic expansion and well-executed acquisition strategies, positioning the company to capture additional market share.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Construction Partners: Building Future Wealth With Robust Growth And Strategic Vision