ROAD - Construction Partners: Infrastructure Funding And Acquisitions Driving Growth

2023-03-28 11:36:49 ET

Summary

- Construction Partners should benefit from the infrastructure funding in the United States and acquisitions.

- The company’s profitability should improve in 2H FY23 and beyond.

- Based on favorable growth prospects and attractive valuation metrics, I have assigned a "buy" rating.

Investment Thesis

Construction Partners, Inc. ( ROAD ) appears to be well-positioned to take advantage of the robust demand in both the public and private sectors. In the public sector, the recent Infrastructure Investment and Jobs Act (IIJA) has started to allocate funds for highway programs throughout the United States. Meanwhile, the company's presence in states experiencing migration gains has led to increased demand for both residential and non-residential construction in the private sector. Additionally, the company's revenue stream is expected to receive a boost from recent acquisitions of hot-mix asphalt plants, which has enabled ROAD to expand its geographic footprint and increase vertical integration at its facilities. On the margins front, the completion of lower margin projects and improvement in supply chain and labor should bring the margins to historical levels. Overall, I am optimistic about the company's growth prospects.

Infrastructure funding

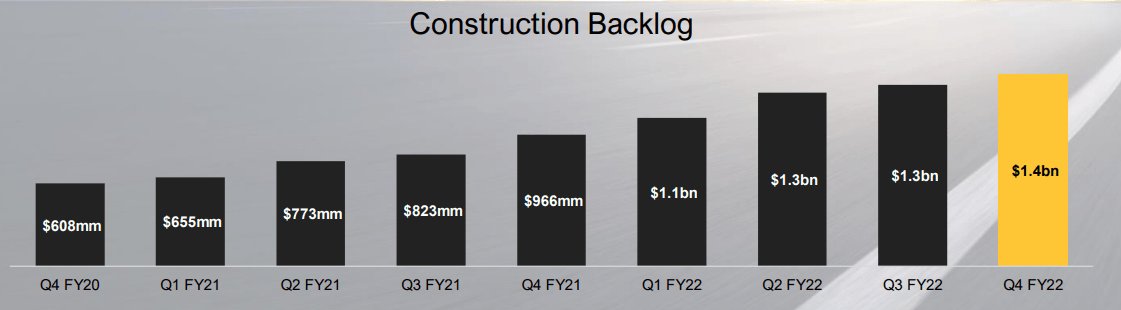

ROAD's backlog order (Created by DzD Analysis using data from ROAD's investor presentation)

{kind=link}

Construction Partners had a healthy start to its first quarter of FY23. The revenue in the quarter grew 20% Y/Y with 8.7% organic growth and 11.3% from acquisitions. At the end of the quarter, the backlog stood at $1.47 billion, driven by the robust demand environment in both the public and private sectors. In the public sector, demand remains strong due to the Infrastructure Investment and Jobs Act (IIJA). The IIJA-funded projects have begun to flow throughout the United States, including Alabama, Florida, Georgia, North Carolina, South Carolina, and Tennessee, where ROAD has a strong presence. The IIJA funding should create ample growth opportunities for the company, with approximately $350 billion allocated to highway programs over the next few years until 2026, of which approximately $47 billion is assigned to states where ROAD operates.

Over the past two years, Construction Partners has been focused on improving its workforce and organization to capitalize on this infrastructure investment opportunity over the next five to six years. The company has acquired several hot-mix asphalt ((HMA)) plants, added equipment and workforce, and positioned itself well for projects related to infrastructure funding.

Apart from the public sector, the company has also witnessed healthy demand in the private sector, benefiting its order backlog. Looking ahead, the company sees better opportunities in both residential and non-residential spaces, given the increased migration of new residents to the Southeast region. The National Association of Realtors measured net migration gains in the United States in 2022, with ROAD being present in five out of the top six states, including North Carolina, South Carolina, Florida, Tennessee, and Georgia. The increase in migration gains was due to outmigration from cities such as New York, California, and Illinois due to rising affordability issues. Despite the decline in residential markets, developers in the Southeast regions are continuing to build their projects due to migration trends but building fewer lots compared to prior years.

Acquisitions

ROAD's expansion strategy involves adding strategic assets, workforce, and equipment, and increasing the vertical integration of HMA plants and construction services through acquisitions. Since 2018, the company has acquired 21 companies and added 65 hot-mix asphalt plants through bolt-ons and three platform acquisitions, consolidating the highly fragmented HMA industry. The company's ideal acquisition target has revenues in the range of $20mn to $40mn with 1-3 HMA plants and a purchase price of 4.5 to 6.0x EBITDA.

In Q1 FY23, ROAD carried out two strategic acquisitions, a bolt-on acquisition in Nashville, Tennessee, and a new platform company (Ferebee Corporation) in Charlotte, North Carolina. With these acquisitions, the company added six HMA plants to its portfolio and a backlog of approximately $70 billion.

Looking ahead, the company plans to continue its acquisition strategy, with a focus on expanding in the Southeast region. With a debt-to-TTM EBITDA ratio of 2.96x at the end of Q1 FY23, ROAD has the financial flexibility to pursue potential acquisitions in the near term. The company has generated strong cash flow from operations over the years and has been using its cash reserves to fund its expansion strategy. The company's acquisition spree over the past two years has been aimed at better utilizing its cash reserves for growth opportunities.

Profitability

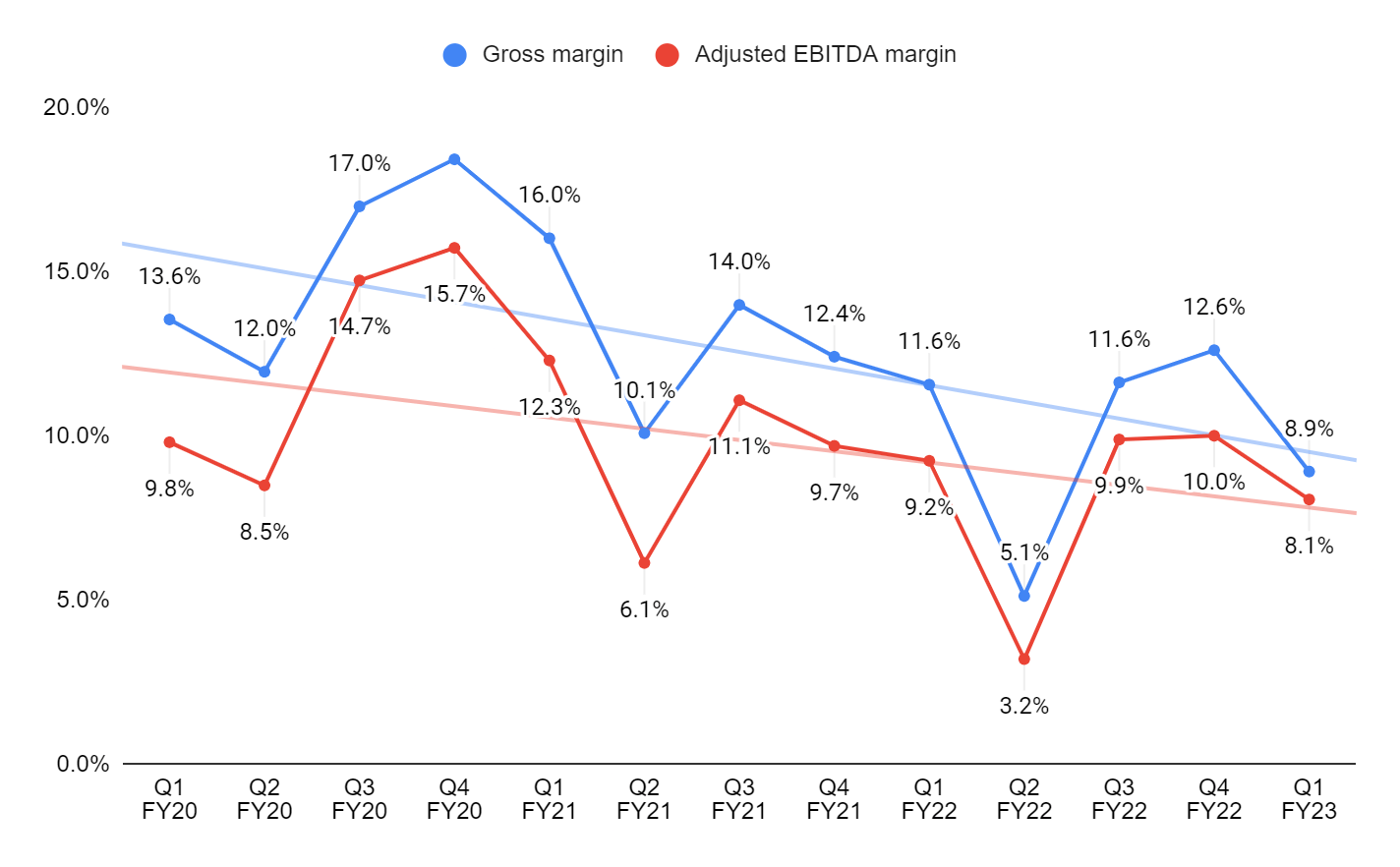

Gross margin and adjusted EBITDA margin (Created by DzD Analysis by taking data from ROAD's press release)

{kind=link}

The main factors responsible for this are the rising costs of commodities, supply chain issues, and labor shortages. In the first quarter of FY23, the gross margin fell by 260 basis points Y/Y to 8.9%, while the adjusted EBITDA margin decreased by 120 basis points Y/Y to 8.1%. The above-mentioned headwinds and the lower number of working days due to above-average precipitation in November and December contributed to this decline. As a result, there was a $4 million impact on EBITDA due to the under-absorption of fixed costs at the company's asphalt plants and equipment use.

However, looking forward, I am confident that the company's margins will improve in the second half of FY23. This is because the lower gross margin projects that were bid before October 2021 are almost complete now. The completion of these projects, along with the higher-margin projects that the company booked over the last few quarters, should bring the margins back to their historical levels. Additionally, the supply chain constraints and labor shortages that have been impacting the company have begun to ease, which will act as a tailwind for the company's margins in the near to medium term.

In conclusion, while there have been some challenges faced by the company in terms of declining margins, I am optimistic about the future. With the completion of lower-margin projects and improvements in the supply chain and labor market, the company's margins should begin to improve in the coming months.

Valuation

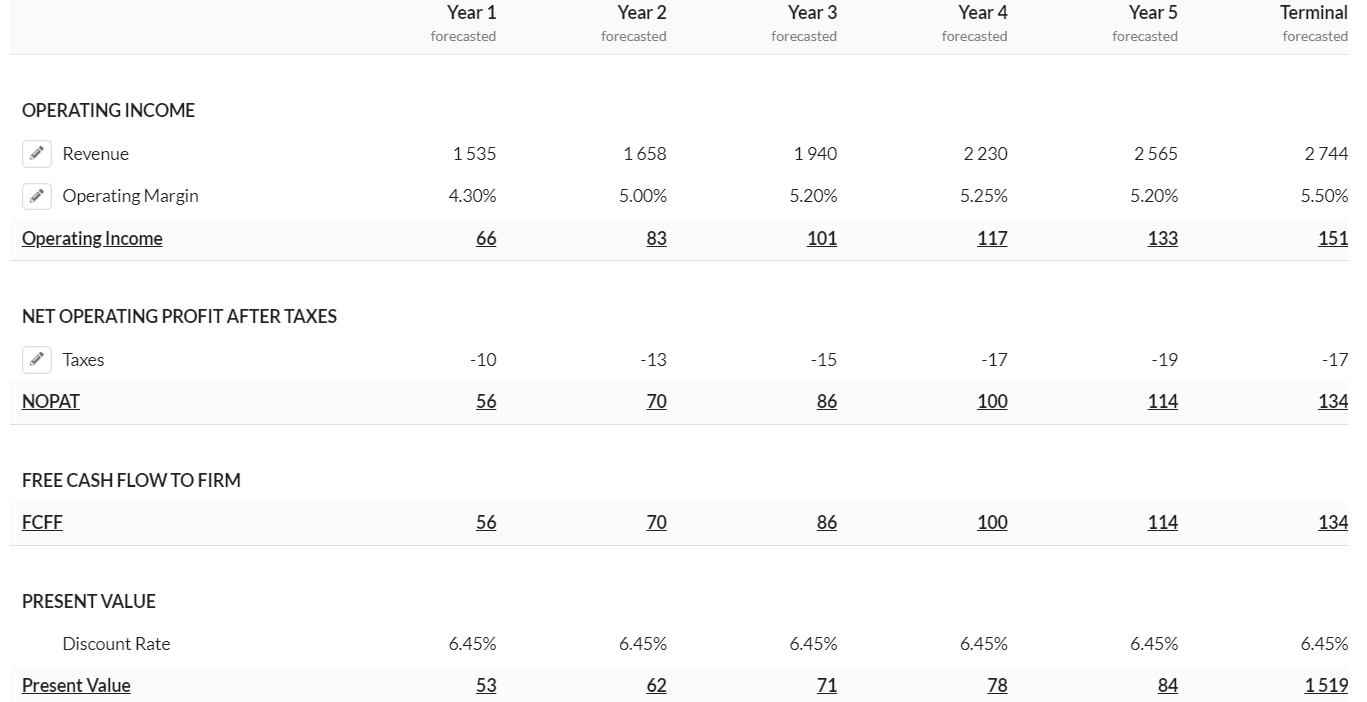

DCF Valuation (Created by DzD Analysis by using Alpha Spread)

{kind=link}

In my DCF calculations, I am assuming revenue growth to be in the high teens in 2023, given the healthy order backlog, acquisitions, and infrastructure funding in the United States. Beyond 2023, I have assumed growth to be in the mid-teens, with a terminal growth rate in the high single digits given the strong infrastructure funding environment in the United States. I have assumed the operating margins will improve in FY23 and beyond. I used a discount rate of 6.45% by using the cost of equity of 7.67% and a cost of debt of 2.30%, which is below the industry level , and arrived at a fair value of $28.51 for ROAD.

Conclusion

Overall, Construction Partners had a solid start to its first quarter of FY23, with a 20% YoY revenue growth, driven by strong demand in both the public and private sectors and strategic acquisitions. The company has been positioning itself well to capitalize on the infrastructure investment opportunities created by the IIJA. Despite some challenges faced by the company, such as declining margins due to rising costs and supply chain issues, the completion of lower-margin projects, and improvements in the supply chain and labor market should bring margins back to their historical levels in the coming months. Looking ahead, with a healthy order backlog and continued expansion plans through acquisitions, Construction Partners is well-positioned for future growth.

For further details see:

Construction Partners: Infrastructure Funding And Acquisitions Driving Growth