CCRD - CoreCard: Potential Buyout

Summary

- Potential acquisition in the fintech space.

- Late last year, media reports appeared that Goldman Sachs has expressed interest in acquiring credit card issuance software provider CoreCard.

- Goldman Sachs, which manages Apple Card, has been CoreCard’s largest customer, accounting for over 70% of the company’s revenues.

- A buyout might be likely given CoreCard’s relative cheapness amid a substantial growth runway and GS’ continuing focus on card partnerships.

- Meanwhile, CoreCard’s CEO/founder might be a willing seller here given his large ownership stake.

CoreCard ( CCRD ) is a $279m market cap company providing software, consulting and processing services to credit card issuers. In 2018, the company struck a deal to license its software to Goldman Sachs ( GS ) which manages the Apple Card. GS has been CCRD’s major customer since then, accounting for over 70% of revenues. In November ’22, WSJ reported that GS expressed interest in acquiring CCRD, among a couple of other fintech software companies. I subsequently highlighted the idea to Special Situation Investing members, noting that an acquisition might be likely. CCRD's share price has jumped 14% since, however, I think the situation is still interesting. Aside from the already existing tight cooperation between GS and CCRD, there are a number of aspects suggesting both sides might potentially come to terms on an acquisition:

- CCRD seems to be cheap trading at 10x EBITDA. While this is quite a sizable multiple, the company’s current EBITDA is likely significantly below the company’s true earnings power in the long-term. CCRD is a fast-growing company which has compounded its topline at 34% CAGR since 2018 driven by an increase in the number of Apple Card users from 3.3m in 2020 to 6.7m as of early 2022. An increasing growth contribution has come from CCRD’s other partnerships, including the agreement with Cardless to launch a co-branded card with American Express and another partnership to process American Express’ Kabbage loans. It seems, however, that there is substantial further growth runway ahead. CCRD’s management has projected a 20-25% growth rate going forward. This estimate seems reasonable, if not conservative, given several points:

-

Penetration of the Apple Card is still low. For reference, largest credit card provider Chase recorded 149m holders in 2021. The Apple Card - which is currently limited to the US - likely has a TAM north of 50m individuals.

-

The management expects to land 1-2 large customers by the end of 2023 and 3-4 by late 2024. The new customers are expected to come either through Goldman or new partnerships which are apparently already in discussion stages.

-

The American Express partnership will give CCRD direct connection to the American Express network (in addition to Visa and Mastercard). This means that CCRD will be able to process other customers using the American Express network.

Likewise, the company does not seem expensive on a relative valuation basis. CCRD currently trades at 3.7x TTM revenues. In comparison, peer Galileo Financial Technologies was acquired by SoFi in 2020 at a 6x revenue multiple. The only publicly-listed competitor Marqeta ( MQ ) is currently valued at 2.7x TTM revenue. Both companies seem somewhat comparable - not unlike CCRD, MQ has a high customer concentration risk, with 70% of revenues coming from Square. It is worth highlighting, however, that MQ primarily operates in the debit card issuing space as opposed to credit card issuing which is CCRD’s focus. As noted by CCRD’s founder/CEO, credit card issuing is much more sophisticated and less commoditized given tougher regulatory scrutiny and the need for a ledger to keep up with interest charges - CCRD’s CEO during the investor conference in August ’22:

I think credit is probably, oh, exponentially 20 times, 30 times more difficult than credit. When you go to the issuing space, you really can talk about three things. You talk about stored value; that's a prepaid card. It can have all kinds of names. It can be a gift card. It can be all sorts of things. But it means the money's in the bank somewhere. And we're simply using a card to allocate the money that's in the bank in some way.

[…]

The interest complexity and the regulatory make it just totally different. It is easy. It's relatively easy to build a software platform that can process stored value or that can process debit. I mean, debit is probably the simplest of all. I think the big difference that we see and the CoreCard takes advantage of is that credit is where people make money. Debit and stored value, you pay money to somebody to keep up with that credit. You've got interest being earned. So therefore, you have a source of funds to pay for the complexity of credit, as opposed to just kind of keeping up with a very simple ledger.

Worth noting that MQ has recently entered into the credit card issuing space, however, as noted by CCRD’s CEO, given the complexity inherent in credit card issuance MQ might very well need a number of years to provide offerings on par with those of CCRD. Given CCRD’s highly sophisticated service offering in a market with relatively few suppliers, the business might warrant a significant premium versus the competitor MQ. Aside from MQ and Galileo, the other competitor in the space is i2c.

-

A potential acquisition would fit into Goldman Sachs’ increasing focus on card partnership (such as the one with Apple). While the company recently scaled back its plans to expand the broader consumer banking business, card partnerships have remained among the company’s priorities. This is also shown by Apple and GS recently extending their Apple Card partnership through the end of the decade. Moreover, in 2021 rumors appeared that GS was in talks with JetBlue ( JBLU ) to take over its credit-card program. JBLU’s current issuer is Barclays, however, the contract between the two sides reportedly ends in 2024. GS has generally been an active acquirer in the payment space - the bank acquired credit card start-up Final in 2018, BNPL lender GreenSky in 2022 as well as GM’s credit card unit for $2.5bn in 2020 (before launching the GM card in early 2022). Potential acquisition of CCRD would allow GS to scoop up the target’s technology before rolling out more credit card partnerships going forward.

-

CCRD had previously been approached by the above-mentioned SoFi before it decided to buy Galileo Financial Technologies. This VIC author suggests that the key hurdle during the due diligence process was CCRD’s lack of capacity to undertake new projects after agreeing to the Goldman Sachs-Apple partnership. Since then, however, CCRD has substantially expanded its workforce - from 530 as of Mar’20 to over 1100 currently. This suggests this time the company might potentially be a more attractive acquisition target now that it is able to onboard new large customers.

-

CCRD is led by the founder and CEO Leland Strange (owns an 18% stake). The founder might potentially consider a company sale given his age (81) and sizable ownership stake. Strange’s salary has stood at $700k-$750k in recent years - immaterial compared to the value of his ownership stake of $50m at current prices.

CoreCard

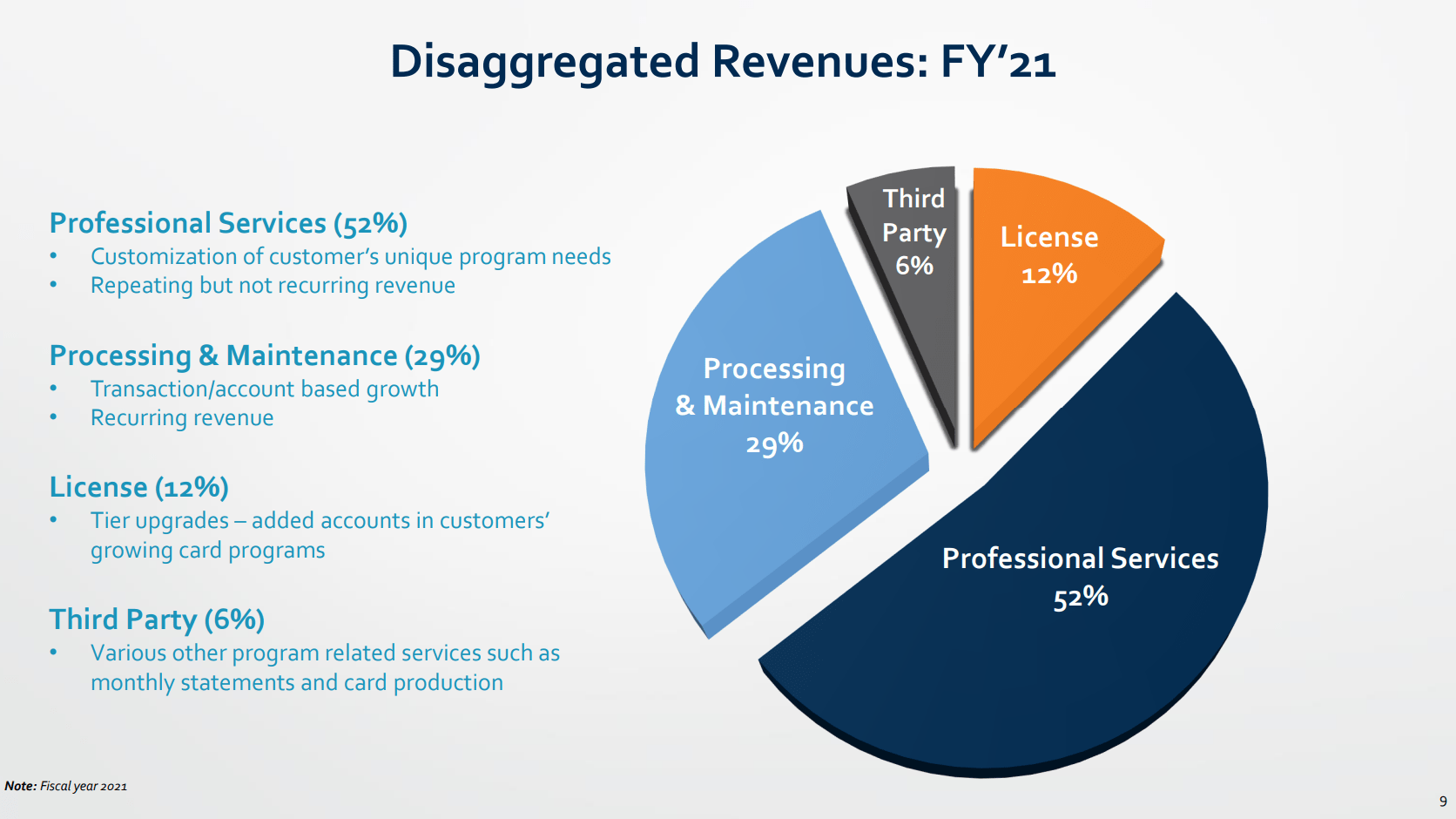

CCRD provides software, consulting and processing services, with a focus on credit card issuance. The company's revenues come from licensing (Goldman Sachs largely licenses CCRD’s software), processing services (whereby customers outsource their card processing requirements) as well as consulting (BPO business where consumers are charged to customize, maintain and modify software). The company has put increasing focus on the processing and BPO services while de-emphasizing licensing revenues given their lumpiness. As noted by the CEO :

Well, currently, we have potential partners that may license or may want to be processed. If they license, we get more upfront. If they choose processing, we have more upfront expense and infrastructure and the monthly numbers just add up over time.

{kind=link}

CoreCard Investor Presentation, September 2022

Worth noting that despite high multi-year growth CCRD’s margins have been suppressed over the recent quarters. The company recorded 21% EBITDA margins in Q3’22 - compared to 33% in Q3’21. This has been driven by continuous hiring of new personnel (primarily in India) for the BPO business. This, nevertheless, is an important component of the company’s strategy given that the personnel needs extensive training - ranging up to three years - before the staff is sufficiently competent to provide services to a new customer. From the CEO:

You've heard me in the past talk about how long it takes to train to be able to offer our customers and partners the quality, high-end expertise that differentiates us from others. For some specialties, 18 months of training suffices. But for others, it will be a 3-year process.

For further details see:

CoreCard: Potential Buyout