PLAT - Coursera: Avoid This Stock For Now

- Coursera’s recent second quarter earnings missed expectations. Management cut their revenue growth guidance by almost a quarter.

- After hours, shares cratered by as much as 40%.

- Enterprise growth is still solid, but the company has struggled to add new clients.

- I think Coursera is a high quality company, but their valuation and continued dilution add a lot of risk.

Investment thesis

Coursera, Inc. ( COUR ) is a best-in-class online learning company. However, their valuation is based on a growth story that is experiencing some headwinds. Shares cratered by as much as 40% after a poor second quarter result.

I like the company and its story. However, the fundamentals concern me. The company is still unprofitable and diluting shareholders. I'm adding this stock to my watchlist, but I think avoiding the stock is the safest option for now.

Revenue growth is slowing down

Coursera's second quarter results were not good. The company missed top line and bottom line expectations and cut guidance for the full year. Management announced that they're reducing their rate of growth and investment for the year.

Coursera reported $124.8 million in revenue, which missed the company's first quarter guidance range of $128 to $132 million. The company slashed its 2022 revenue guidance from a midpoint of $542 to $511 million. This reduces their projected annual growth rate by almost a quarter. To partially offset this, management reduced their adjusted EBITDA loss guidance by 6%.

The major headwind facing the company is the business's top line growth rate. The core platform is still performing well. The company added five million new learners in the quarter. This is in line with Coursera's historical user growth rate.

Weakness in individual customers

Coursera reports its results in three segments. These are their consumer, enterprise, and degree businesses. Both their consumer segment and degree programs deal with individual customers. These were the weakest performers this quarter and saw the largest cuts in guidance. On their earnings call , management admitted that results in these segments were "lower than anticipated."

Coursera Q2 2022 Earnings Presentation

{kind=link}

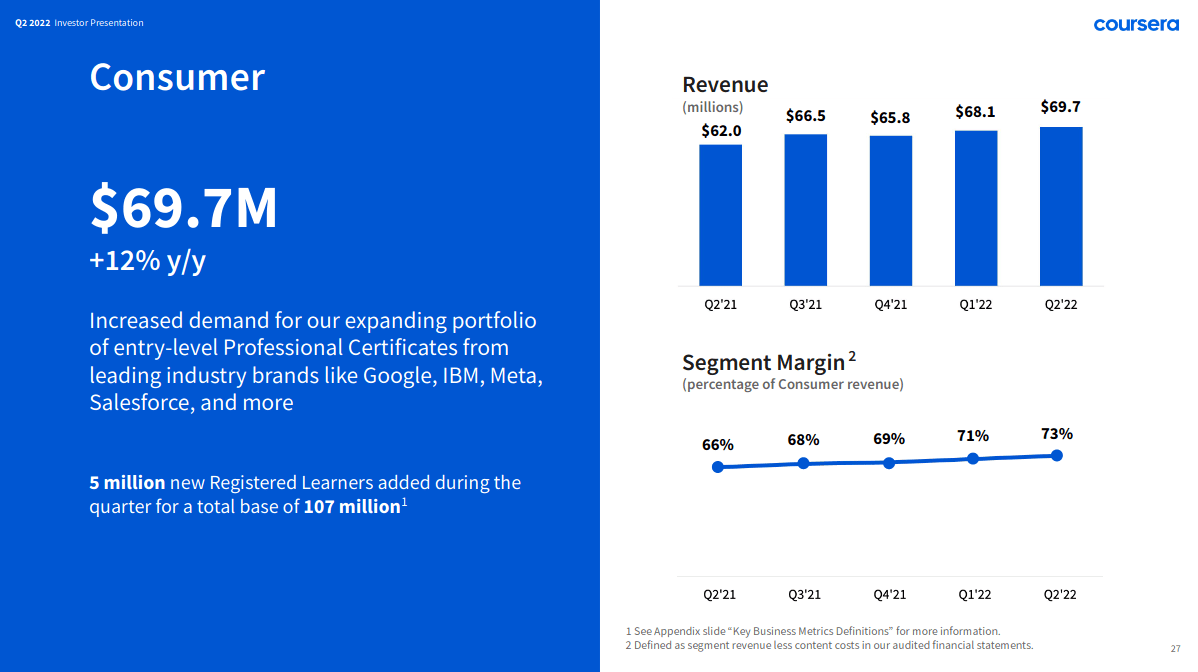

The consumer business generates the majority of Coursera's revenue and profit. The segment grew its revenues by only 12% year over year. The company reported weaker conversion rates in several markets, especially EMEA.

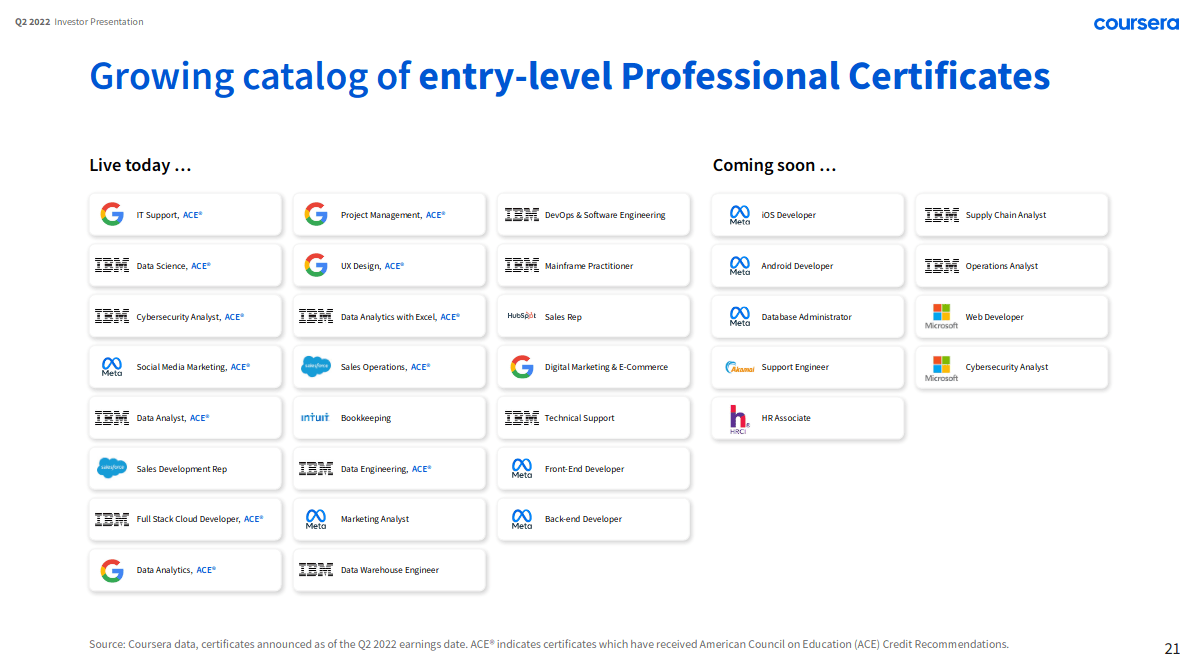

There are some interesting trends in this segment. On their earnings call, management reported increasing consumption of industry partner content. This content is generated by businesses rather than universities. The main products are entry level professional certificates .

Coursera Q2 2022 Earnings Presentation

{kind=link}

These trends started showing up early last year, and have only grown since. It looks like a lot of new customers are using Coursera's platform to completely change careers. This is a shift away from a lot of Coursera's university-produced content. A lot of that content is aimed at professionals learning new skills for their existing careers.

One side effect of this trend is an improvement in the segment's profitability. Consumer gross margins have increased by 7 percentage points year over year. This is because industry partner certificates have lower content costs than Coursera's other offerings.

Coursera Q2 2022 Earnings Presentation

{kind=link}

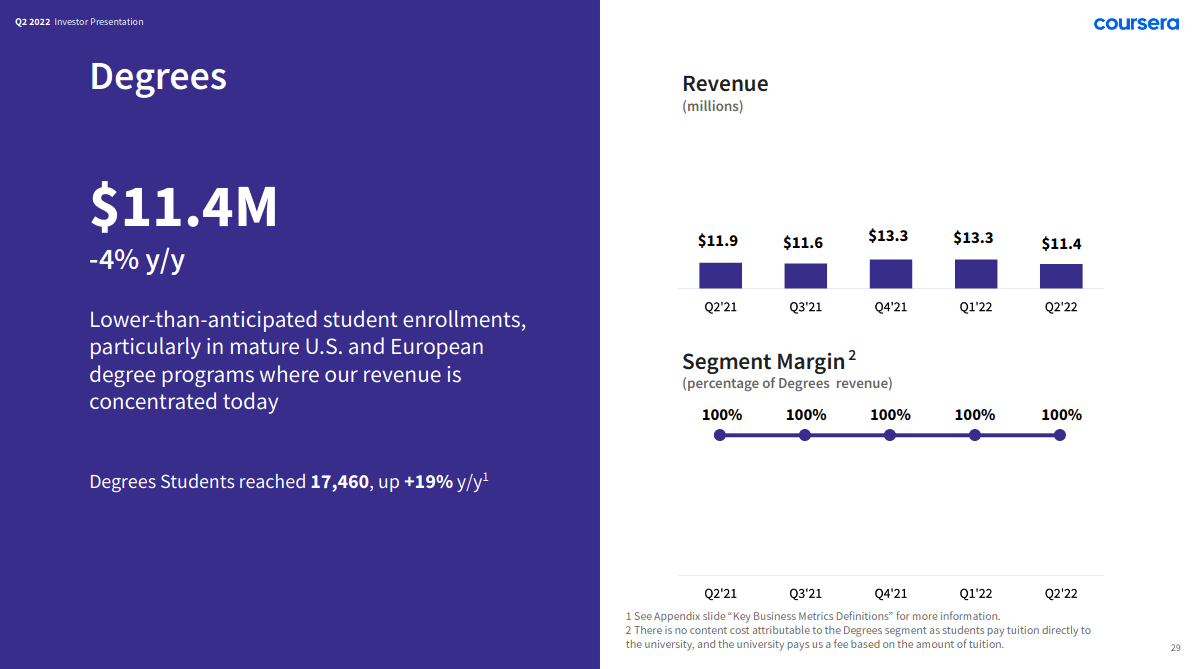

Coursera's degree programs also reported disappointing results. The number of students increased by almost 20% year over year, but revenue was down by 4%. This is because Coursera charges by the credit hour. Even though there are more students, these students are taking fewer courses on average. This segment is still in its early stages, but I find the enrollment trends promising.

Continued growth in enterprise revenue

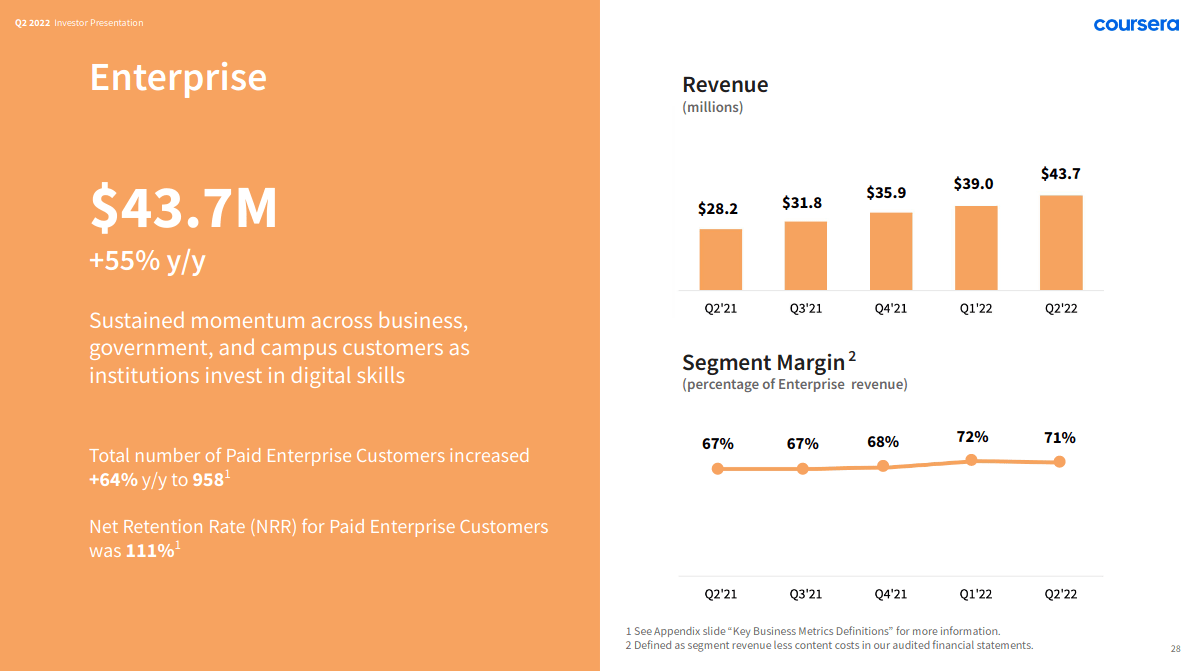

The standout growth driver has been Coursera's enterprise segment . This segment grew revenues at an impressive 55% year over year. Solid growth in this division helped offset the mediocre results from other segments. However, Coursera still reduced enterprise growth guidance from 50% to the mid-40% range.

Coursera Q2 2022 Earnings Presentation

{kind=link}

The results in this segment are remarkable, but I see some headwinds to this growth. While top line growth was strong, the segment added fewer new clients than it has historically. The company only added 41 paid enterprise customers during the quarter. This is the lowest number since the worst of the pandemic.

Management indicated that they're seeing a delay in purchases. This is due to economic headwinds, particularly in Europe. I think that these trends could get worse. The technology industry is seeing a pullback in growth as well as hiring freezes . If this continues, I think the pace of enterprise sales may suffer. This is an important risk since the high growth in this segment is important to the business's valuation.

How is Coursera positioned?

Coursera is positioned as an industry leader in online learning. The platform has partnerships with many top universities and leaders in the tech industry. Their library has a lot of high-quality content.

This creates a strong competitive advantage. Coursera's relationships with major institutions set the company apart from its competitors. Other online learning platforms have content from independent creators. The quality can vary wildly. This is the most important for enterprise customers and professional development programs. These clients want to make sure they're getting useful content.

I think Coursera is well-positioned for long-term growth as online learning grows in popularity.

Stock-based compensation makes the valuation risky

Coursera's shares plunged after hours, reaching lows below $10. The company has about $5.41 per share in cash and equivalents. At the opening price of about $12.30, this gives shares a cash adjusted value of about $6.89.

Shares are trading at about 2 times EV/Sales multiple. Revenues are only projected to grow at 23% this year. This is higher than what I'd be willing to pay for a company with solid negative EBITDA.

Another concern I have is Coursera's stock-based compensation. The company is paying out 20% of its operating costs in shares. The company has a very low cash burn rate, so there's little risk of running out of money. But sustained dilution is a concern. Coursera has increased its shares outstanding by 5% year-over-year. I want more clarity on how the business plans to mitigate dilution.

Final verdict

I believe that Coursera's core platform is strong. However, the business is unprofitable and their valuation is based on high top-line growth. A lot of the company's expansion depends on very high growth in their enterprise segment. I think headwinds in the technology sector make this too risky.

I don't see enough of a margin of safety to recommend buying or holding shares. But I believe that Coursera has a high quality platform and the potential for long term outperformance. I think that growth investors should keep an eye on this company.

For further details see:

Coursera: Avoid This Stock For Now