OUT - Cove Street Capital Q4 2023 Letter To Shareholders

2024-01-10 08:07:00 ET

Summary

- Cove Street Capital manages assets for a global mix of institutions, foundations, family offices, and high net worth individuals on a separate account, mutual fund, and sub-advisory basis, utilizing a research-intensive, concentrated value-based strategy.

- With respect to Cove Street Capital, we had an excellent year in performance. We admit to being truly amazed by the last 3 months of market activity as our “relative” performance fell back as the broader market ran ahead fearlessly.

- Our value-add is in the bottom-up work we do on individual companies, valuation and an assessment of management.

Greetings Fellow Shareholder:

What a wonderful year 2023 was… and now the traditional idiocy of making any attempt at predictions for 2024. Or frankly any year to come. Not that that proof statement will stop anyone. But it will mostly stop us.

Instead of looking forward, let us look back at 2023, and Mark Twain comes to mind, after all “truth is stranger than fiction”:

- A bank collapse of 3...and then nothing.

- A credit collapse? Nope.

- Inflation and interest rates going to the moon? Nope.

- Real estate dying as an asset class under higher rates? Nope.

- Ukraine/Russia and then the Israel Oct. 7th disaster destroying global order and pushing oil to $150? Nope.

- A Biden/Trump rematch obviously the high probability event in 2024?

- Large Cap / Tech / Growth finishes its second year of lagging value in general and Small Cap in particular? Nope.

With respect to Cove Street Capital, we had an excellent year in performance. We admit to being truly amazed by the last 3 months of market activity as our “relative” performance fell back as the broader market ran ahead fearlessly. As noted, ours is a curated and concentrated portfolio of securities and not the world’s best beta bet. So when the Russell 2000 ® gains 24% approximately 50 days after sinking to a fresh one-year nadir in October, we huff and puff behind it. We would also note the big fat rally in banks specifically and financials in general, sectors which dominate the Russell 2000 ® Value index. But “relative performance” is the meal ticket for the manager, not for you the client. Let’s move on to detractors and contributors in the portfolio.

Lifecore Biomedical ( LFCR ), via our holding of the Convertible Preferred, remains our “on again, off again” performer. This was an “off” quarter, but it is important to understand the big picture here: the company is for sale as stated publicly by the company. It is correct to note that this is not a great time for the doing deals in general and healthcare services world in particular, but this is a process with an end, preferably within our lifetime. To reiterate, we utterly nailed the intrinsic value of the company’s strategic position and utterly missed the ineptitude of management, which to this writing plagues us. We materially reduced positions at higher levels than the current share price to recognize the likelihood that time hasn’t been our friend in a final value. We hate to ever be “hopeful” in our investment process, but we will attribute the word toward a guess at timing...soon.

{kind=link}

Performance shown for the period through January 20, 2012 reflects performance for CSC Small Cap Value Fund, a series of CNI Charter Funds, the predecessor to Cove Street Capital Small Cap Value Fund (“The Fund”). The Fund has the same portfolio manager and substantially similar investment strategies to the predecessor fund. The Institutional Class commenced operations on October 3, 2001. The performance results for the Institutional Class reflect the performance of the Investor Class shares from December 31, 1998 through October 2, 2001. The Investor Class subsequently closed, effective November 25, 2015.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-866-497-0097.

The gross expense ratio as per the Prospectus is 1.33%. The Fund imposes a 2.00% redemption fee on shares sold within 60 days of purchase. Performance data does not reflect the redemption fee. If it had, return would be reduced.

Hallador Energy (HNRG) is one of three energy-related stocks in the portfolio and was our biggest contributor through the third quarter. Like all energy stocks, internal competence gets trumped by the price of the commodity, and warmer weather plus the lack of global disasters in Ukraine and the Middle East put the hurt on pricing. We again took some profits at materially higher levels than current prices. We continue to advocate cautiously that demand for carbon energy is a lot stickier than many would like, and a sufficient and steady supply of alternatives is a lot harder to produce than many would like. We think this produces a higher and steadier set of profit fundamentals for Hallador via its coal mining and power production, for CNX Resources ( CNX ) via its natural gas resources and Vitesse Energy ( VTS ) via its predominantly oil resources. All of these are domestic sources of energy.

Corus Entertainment ( CJREF ) started as a small position, and we reduced the position as we began to recognize the probability of a mistake. Ultimately, we did not completely relieve ourselves of the position. We like to buy what we determine are “cyclical problems” and we think “advertising” in general fits that bill. What we under-appreciated is the “stickiness” of Canadian regulation in regard to broadcasting and media. We thought we saw movement for legitimate change in the ability of the industry to meaningfully participate in consolidation and partnership in a way that could benefit shareholders. Wrong. Our remainder is tiny and will be exited in 2024.

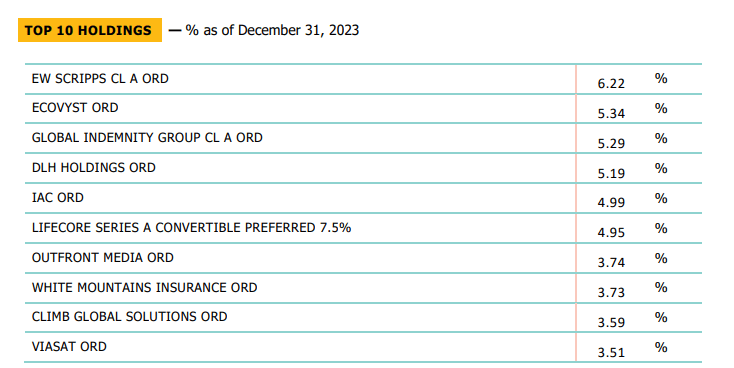

Our largest contributor in the quarter was E.W. Scripps ( SSP ), which benefited from the alleviation (slightly) of concerns about the general economy and ad market. It helped that the world of labor strikes – affecting the desire of auto companies to advertise and the ability to produce scripted television and movies – slowed down too. We added aggressively to our stake to make this a Top 5 position as recently as October, when these issues were top of mind, and we have been quickly rewarded. Scripps has done a very nice job of positioning itself to capitalize on the evolution of the media industry. We think “legacy” TV has a much longer life to it than “fancy talk” suggests, and despite obvious exposure to the cyclicality of the advertising business at large, Scripps is a cash gusher that is rapidly paying down debt from a series of acquisitions that were enabled under the prior administration. Pick your favorite math, but ours suggests that free cashflow to pay down debt is creating 20% annualized increases in equity value at current levels.

Liberty TripAdvisor Holdings Inc. ( LTRPA ) has made it a habit in 2023 of appearing in our contributor/detractor section. We are happy to say that the Q4 edition finds them in the former category as one of our top performers. The volatility in LTRPA stems from the investment community’s tennis-rally-esque focus, alternating between the two biggest holdings: TripAdvisor, a slowly declining (though highly profitable) legacy metasearch business and secondly Viator, a market-leading experiences online travel agency (OTA), that is growing 40% and nearing breakeven profitability. Lately, attention has been paid to the latter part of the business, as smaller experience OTA competitors like GetYourGuide and Klook raised $194m and $210m in private markets. It’s not just the dollars raised, but the valuations; GetYourGuide raised that capital at a $2B valuation. Our exposure to TripAdvisor comes through Liberty’s tracking stock, which provides 3:1 leverage to the TRIP share price. With Viator turning the corner to breakeven and setting its sights on “hotel OTA” margins, we continue to view LTRPA as highly attractive at these levels.

DLH Holdings Corp. ( DLHC ) is a consultant that provides a wide range of services to various Federal health agencies such as the Veterans Administration and Centers for Disease Control. It offers public health and life sciences services and has added high margin cybersecurity capabilities via its acquisition of Grove Resources late in 2022. This is an asset-lite, high free cash flowing business with generally sticky 3 to 5 year contracts. This company trades at a discount to its peers—despite having best in class margins—largely due to an overhang from a high revenue but low margin incumbent contract that the government continues to drag its feet on re-awarding. Our research indicates stock continues to be priced for a “worst case” scenario with respect to this renewal, and other likely outcomes present a high-upside case. Furthermore, management has been astutely using cash to acquire smaller players in adjacent capabilities—such as Grove—to diversify revenue across more contracts. CEO Zach Parker came in seven years ago when the company was doing $2m in EBITDA; we expect them to deliver ~$45m in EBITDA in FY24. DLHC was a top performer for us in the fourth quarter as the management team continues to execute on its strategy and positions the company to be sold to a larger player.

Outfront Media ( OUT ) was a new position for CSC and it brings a smile to our faces here at Cove Street when a new position shows up as a top contributor because the two are often uncorrelated. Outfront is one of the Big 3 billboard companies, mostly in the US. It is mostly structured as Real Estate Investment Trust (“REIT”). Properly run, the Billboard segment is a “great one” - very high returns on tangible capital, limited and highly coveted real estate, great free cash flow and a secular profitability uptick from a conversion from wood to digital. A few unfunny things happened on the way to the bank, which lead to a decline from the mid $20’s to our entry point (~$10). You might recognize from these themes from the discussion of SSP: a general advertising slowdown, a particular slowdown from the auto and the movie industry strikes, and yes, Covid…again. Outfront has 20-ish percent of its revenue from public transport venues and you might have read people are resisting coming back to work in major cities. Our research suggests that most of this was cyclical rather than permanent. The company had multiple avenues for improving the balance sheet, like selling their Canadian business for almost 2x the trading multiple of the entire company shortly after purchase. Arguably, the stock was selling for half our estimate of value in a reasonable environment. So far so good.

Viasat ( VSAT ) simply rebounded from “stupidly cheap” levels. There has been an interesting change at the company, after the “how can two new world class satellites get malfunction within 60 days of each other.” The company has taken their foot off the CapEx pedal and appears to be focused on near-term cashflow rather than the pursuit of global technical dominance. New investors, and perhaps long-term holders as well, recognize and appreciate this new sense of balance and moderation.

We initiated a position in American Vanguard ( AVD ), a manufacturer, developer, and marketer of crop and plant protection chemicals. American Vanguard is a smaller player in the Agricultural Chemical space that has succeeded in picking off under-loved and sun-setting product lines from the giants of the industry and applying the focus and resources necessary to extract value that was simply “not worth it” for its former owners. We have bought and sold AVD at various points throughout the last decade, but this iteration presents a unique confluence of factors we view as highly favorable.

For starters, the Ag Chem industry is going through the trough of an inventory de-stocking cycle last seen in 2015…except this time around the magnitude is more extreme and the effects are global. The ag value chain includes manufacturers like AVD, who sell to distributors, who then sell to retailers, who then sell to the ultimate growers. During Covid, supply chains were such a mess that the intermediate players in the value chain – distributors and retailers – loaded up on inventory to ensure they could meet grower demand. Once interest rates rose, the cost of carrying all this inventory became a massive drag, and so these intermediate players sold out of the inventory they had but stopped buying from Ag Chem manufacturers like AVD. We are in the part of the cycle where a “new-normal” of inventory levels being established, and at a level far below what we saw in 2020-2022. Ag Chem sales in 2023 got crushed across the board, even as crop-protection end-demand has remained stable.

Compounding this issue, AVD engaged in its own self-immolation in not being able to produce two of its leading products in Aztec and Dacthal for the 2023 growing season due to avoidable supply chain and regulatory snags, causing a loss of $50-60m of revenue. AVD has responded in-kind by refreshing its board, bringing in outsiders to improve operations, and creating a transformation plan to improve working capital management and factory efficiency. We expect much of this lost revenue to return simply by basic execution as well as a meaningful working capital swing following the bottom of this inventory destocking that should free up cash flow and allow AVD to reduce debt. We see meaningful upside should this business return to its historically steady 11% EBITDA margins and 11x EV/EBITDA multiple.

Going forward, we will note how incredibly sensitive “we” are to perception in the future direction of interest rates, as if 2023 didn’t raise that flag to the sky. Will Federal Chairman Powell be the Arthur Burns of our generation - selling out to political pressure, which arguably created the great legs of 1970’s inflation? Or will he be our Paul Volcker figure who crushed inflation in 1982?

This is series of statements by “noted” (and we use that term lightly) economist Larry Summers, who can now proudly say that he was run out of Harvard. I think it’s a decent summary for 2024.

I think it’s premature to judge that we have landed softly, because I think that if you look at underlying inflation rates, depending upon your measures, some of them are still running well above 2 per cent. If inflation is currently at 2 per cent, it’s not clear that it won’t go back up again. And it isn’t clear that the landing has been soft in the sense that there are a variety of problems — declining flows of credit, inverted yield curves, aspects of consumer behavior, rising evidence of credit strains — that raise the possibility that the landing won’t be soft, if there is one. So at this point, we may soft land on the aircraft carrier, but the landing may be hard, and we may overfly.

That said, if by a soft landing one means a period when you have inflation above 4 per cent and unemployment below 4 per cent, and you extricate from that situation without a recession — that’s something that’s never happened before in the United States and for which there’s very little precedent in the industrial world.

We will close with our inscrutable face. Our value-add is in the bottom-up work we do on individual companies, valuation and an assessment of management. If we get most of that right, we can ignore most of the fun around predicting macroeconomic events, as we have risk protection in the nature of our ownership and the prices we pay. There is still precious little capital going into our space and there is simply a long and inverse correlation between lack of capital entering a sector and future performance.

Best Regards,

Jeffrey Bronchick, CFA | Principal, Portfolio Manager

Shareholder, Cove Street Capital Small Cap Value Fund

The information provided herein represents the opinions of Cove Street Capital LLC and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Opinions expressed are subject to change at any time.

The fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The statutory prospectus and summary prospectus contain this and other important information about the investment company, and they may be obtained by calling 1-866-497-0097 or visiting www.covestreetfunds.com. Read it carefully before investing.

{kind=link}

Fund holdings are subject to change and should not be considered a recommendation to buy or sell any security. Current and future portfolio holdings are subject to risk.

Mutual fund investing involves risk. Principal loss is possible. There is no assurance that the investment process will consistently lead to successful results. Value investing involves risks and uncertainties and does not guarantee better performance or lower costs than other investment methodologies. Investments in smaller companies involve additional risks such as limited liquidity and greater volatility. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. Concentration of assets in a single or small number of issuers, may reduce diversification and result in increased volatility.

The Russell 2000® Index measures the performance of the small cap segment of the U.S. equity universe, representing approximately 10% of the total market capitalization of the Russell 3000® Index, and the Russell 2000® Value Index includes those Russell 2000® Index companies with lower price to book ratios and lower forecasted growth values. One cannot invest directly in an index.

Cashflow is the net balance of cash moving in and out of a business over a specific period of time.

EBITDA stands for earnings before interest, taxes, depreciation, and amortization, and its margins reflect a firm's short-term operational efficiency.

EV/EBITDA is a ratio that compares a company's Enterprise Value ((EV)) to its Earnings Before Interest, Taxes, Depreciation & Amortization (EBITDA).

The Cove Street Small Cap Value Fund is distributed by Quasar Distributors, LLC.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Cove Street Capital Q4 2023 Letter To Shareholders