LEVI - Crafting Excellence: Ermenegildo Zegna's Journey Towards A Luxury Brand Empire

2023-11-09 17:05:54 ET

Summary

- Zegna Group aims to become a beacon of luxury brands through its vertically integrated structure and network of benefits to each brand under its umbrella.

- The company is expanding its Italian manufacturing footprint and workforce, and has opened seven new stores in strategic locations.

- Modelling a bull and bear scenario for this company provides interesting insights relative to the risk/reward profile of this company.

Zegna Group ( ZGN ) is a supplier of fine tailoring, with its expertise spanning the Zegna, Thom Browne, and TOM FORD labels. The company is a bastion of in-house luxury textile and knitwear production, offering an array of high-end menswear, shoes, leather goods, and accessories that cater to the discerning gentleman.

With a keen eye on the full spectrum of its trade, from the initial sketches to the final stitch, Zegna Group maintains a tight ship over its operations. The company reaches its clientele through a blend of direct-to-consumer storefronts and a network of wholesale partners. Its wares populate the shelves of select franchisees, upscale department stores, specialty boutiques, and are also available on premium online platforms.

Made in Italy Luxury Laboratory Platform

Zegna appears to be charting a course similar to that of some renowned conglomerates, aiming to become a beacon of luxury brands. The strategy hinges on its vertically integrated structure, which is poised to offer synergistic advantages and a network of benefits to each brand under its umbrella.

The company's prowess in vertical integration is not new; it's rooted in its historic Lanificio Zegna. This foundation has fostered innovation in textiles, manufacturing efficiency, and adaptability. Zegna's expertise, coupled with a robust supply chain, positions it as a desirable collaborator within the luxury domain. A testament to this is the growth of Thom Browne, which saw its revenue swell from €117 million in 2018 to €264 million in 2021 post-acquisition.

On the production side, Zegna is bolstering its Italian manufacturing footprint, expanding its capabilities in both footwear and apparel, and is on track to enhance its workforce with 300 new roles in Italy. The establishment of the Accademia dei Mestieri is a cornerstone of this expansion, reflecting a commitment to sustainable growth and the preservation of artisanal expertise.

In recent years, Zegna has been streamlining its operations, optimizing its retail footprint through strategic rightsizing. Emerging from this period of consolidation, the brand is now broadening its retail horizons, inaugurating seven new stores in prominent and strategic locales, including the esteemed Saks New York . Store productivity has been a major engine of Zegna's growth.

The latest addition to the portfolio, TOM FORD FASHION, is gearing up for a significant reveal at Milan Fashion Week with a collection from new creative director Peter Hawkins. The impending appointment of Lelio Gavazza as CEO heralds a new chapter for TOM FORD FASHION, underscoring the anticipation for its journey with the Zegna Group.

Pursuing the LVMH playbook

In the realm of luxury goods, a strategy akin to that employed by some of the industry's titans involves a steadfast commitment to domestic manufacturing, a firm grip on retail operations, and a shrewd use of the existing retail and manufacturing networks to ensure that new acquisitions swiftly amplify their market presence. Zegna, with its vertical integration, is well-positioned to emulate this approach, though it currently operates on a smaller retail scale compared to some of its peers. Yet, it boasts a strong manufacturing foundation that capitalizes on the "Made in Italy" cachet, with esteemed brands and an expanding distribution network.

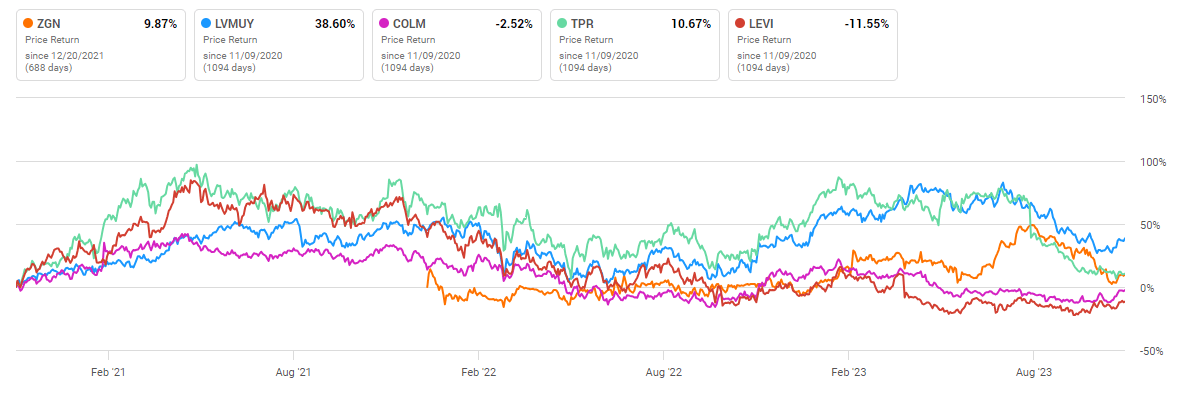

In a previous analysis , I've highlighted key indicators for companies pursuing growth through acquisition in this sector. Applying this framework to Zegna, and juxtaposing it with other entities like Louis Vuitton ( LVMUY ), Levi Strauss ( LEVI ), Tapestry ( TPR ), and Columbia Sportswear ( COLM ), offers an insightful comparison. Note that not all of them pursue acquisitions, but they offer good contrast in other dimensions to our analysis.

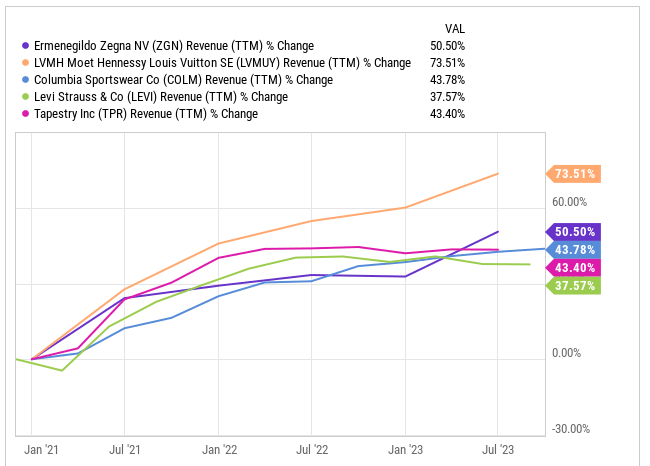

A critical factor for these brands is the ability to drive revenue growth. While all the brands in question meet this criterion, LVMH is particularly notable, with Zegna not far behind.

{kind=link}

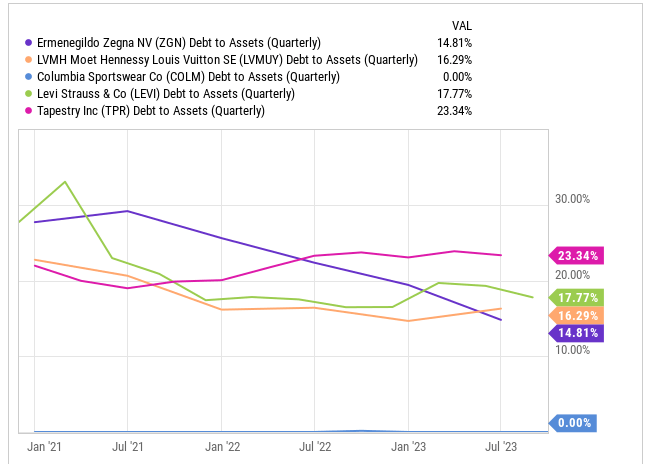

However, revenue growth can sometimes be artificially inflated through aggressive acquisition strategies or discounting practices. To assess the sustainability of growth, one should consider the company's debt levels.

{kind=link}

Zegna has commendably managed to reduce its debt-to-assets ratio while expanding its brand portfolio. In contrast, Tapestry's higher debt levels may indicate challenges in integrating acquisitions effectively.

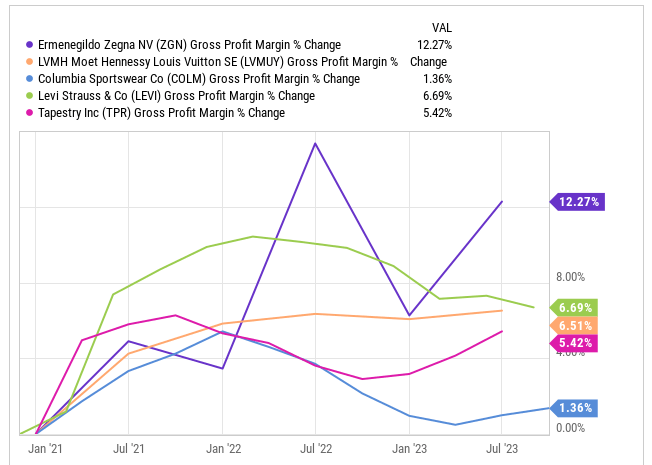

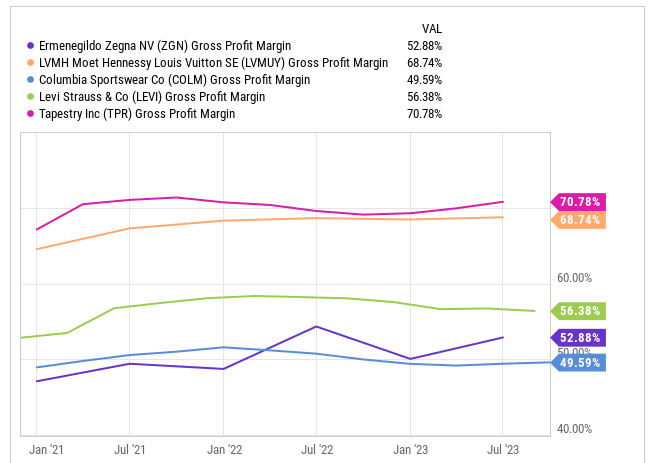

Next, we turn to gross margins as a measure of profitable growth.

{kind=link}

{kind=link}

Zegna has shown the quickest improvement in gross margins among its peers, although it still has room to grow to match the leaders in this area. This suggests that while Zegna's pricing power may be increasing, there's still potential for further refinement. It's crucial to discern whether these margins are a result of manufacturing relocations.

{kind=link}

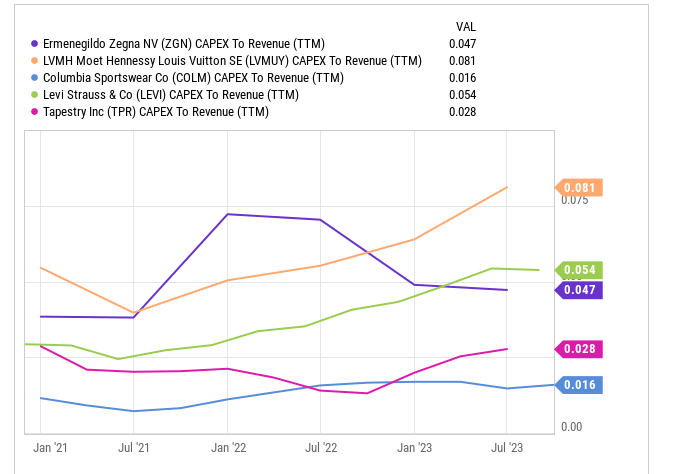

For LVMH, robust gross margins are paired with significant CapEx, indicative of heavy investment in their manufacturing stronghold. Tapestry's lower CapEx, conversely, suggests a shift in production to lower-cost regions like China. Levi's appears to be channeling more into CapEx, raising questions about their strategic intent.

Zegna strikes a balance, with a healthy level of CapEx that underpins its commitment to Italian manufacturing excellence.

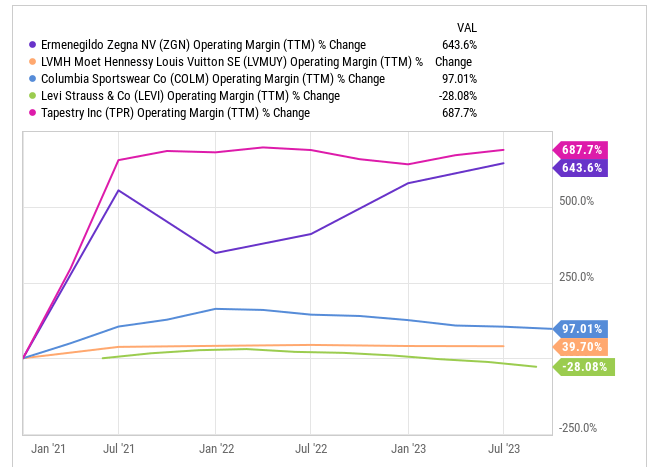

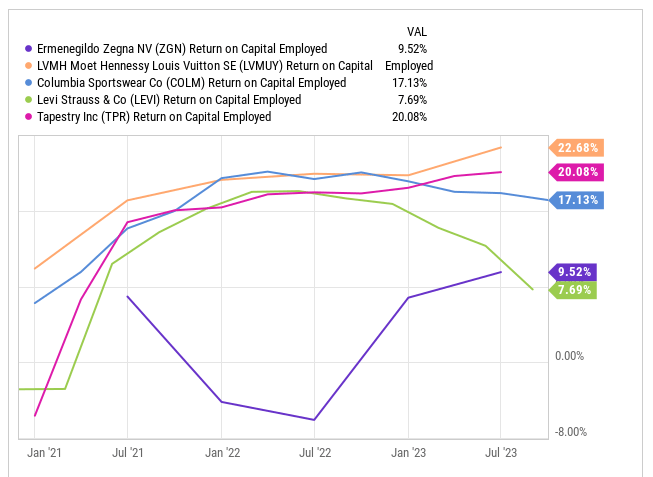

Lastly, we must consider the impact on operating profits. Both Zegna and Tapestry have shown rapid growth in operating earnings. However, Zegna still has progress to make to achieve margins comparable to the industry leaders. This journey towards optimizing profitability is one that Zegna appears to be navigating with a clear vision and strategic investments.

{kind=link}

{kind=link}

Valuation & Risks

The firm has demonstrated a commendable trajectory of revenue growth and has made notable strides in enhancing profitability. A substantial uptick in gross profit and margin is a testament to a series of strategic moves: a refined pricing strategy, a deliberate reduction in end-of-season markdowns, a focus on essential products with longer shelf lives, and more effective absorption of fixed industrial costs.

Concurrently, there's been an uptick in marketing expenditures and SG&A costs, in part due to the integration of TOM FORD and broader business expansion efforts.

Zegna's current performance trajectory bears similarities to that of Tapestry.

{kind=link}

This similarity underscores a pivotal challenge for the company: it must evolve its market perception. To ascend to a stature reminiscent of LVMH, the company must bolster its pricing power, thereby enhancing gross and operating margins to levels more aligned with the French luxury conglomerate. Achieving this could be the difference between commanding a sales multiple akin to LVMH's or being perceived in line with Tapestry, with a notably lower multiple.

{kind=link}

To quantify these trajectories, we can envisage two scenarios: a bullish and a bearish one. In the bullish scenario, we anticipate revenue to climb by 15% annually until 2028, with gross margins reaching 65% and EBIT margins advancing to 15%. Those would be numbers closer to what is accomplished by leaders like Louis Vuitton. This could merit a lofty price-to-sales (P/S) multiple of around 4. Conversely, the bearish scenario projects a modest 5% revenue growth, with gross margins and EBIT margins lingering at 52% and 10%, respectively, which might lead the market to assign a P/S multiple of 0.6. These figures are compatible with a stagnation of the recent evolution and the P/S multiple would reflect that.

Author's computations

The analysis reveals an intriguing asymmetry in risk/reward favoring the upside. Should the company successfully navigate this path, the prospects are indeed promising.

Yet, the risks are palpable. The bullish scenario hinges on flawless execution, emulating the Louis Vuitton model of cultivating a portfolio of brands that yield significant synergies with each acquisition. Presently, Zegna is some distance from this benchmark, and sculpting a conglomerate akin to LVMH is an endeavor that spans decades. To garner a lofty sales multiple, the company must hone its acquisition strategy, manufacturing prowess, and pricing power to a pinnacle of excellence. Falling short in any of these areas could preclude reaching the esteemed valuation multiples of an LVMH.

Given these considerations, it's not surprising that the bullish scenario is deemed a one-in-ten probability in our model. The undertaking is formidable. Nonetheless, the initial steps have been astutely taken: the company wields the cachet of Italian manufacturing, and in time, it could well realize both the profound network effects and the pricing power that accompany esteemed brands. The potential rewards are enticing, particularly when the downside appears contained.

For further details see:

Crafting Excellence: Ermenegildo Zegna's Journey Towards A Luxury Brand Empire