CR - Crane Company: Good Growth Prospects But Valuation Leaves Little Room For The Upside

2023-12-14 11:41:47 ET

Summary

- Crane Company has experienced good core sales growth since its separation from Crane NXT, thanks to healthy demand in its Aerospace and Electronics segment.

- Near-term headwinds in the Process Flow Technologies segment are expected due to project delays in a high-interest rate environment, but a potential interest rates cycle reversal next year could drive growth.

- However, the valuation multiple has already re-rated significantly post the recent run-up, leaving limited upside.

Investment Thesis

Crane Company ( CR ) has experienced a good core sales growth momentum since its separation from Crane NXT, Co. ( CXT ) earlier this year, thanks to healthy end-market demand and higher than normalized backlog levels. Moving forward, I believe the company's revenue should continue to benefit from healthy demand in its Aerospace and Electronics (A&E) segment. In addition, while there are near-term headwinds in the Process Flow Technologies (PFT) segment due to project delays in a high-interest rate environment, a potential interest rates cycle reversal next year should catalyze the growth in this segment adding to overall sales growth. Moreover, the company's growth should also benefit from new product innovations and M&As.

On the margin front, the company should benefit from price increases, productivity and efficiency initiatives, and easing supply chain challenges. In addition, good operating leverage as the sales continue to improve should also benefit margins in the long term.

While I like the growth prospects, the stock has already re-rated and the company's valuation is at a significant premium to its historical averages. This leaves little room for upside. Hence, despite the near-term as well as long-term growth prospects, I prefer to remain on the sidelines and have a neutral rating on the stock due to its premium valuation.

Revenue Analysis and Outlook

Earlier this year, Crane Holdings Co. completed its separation into two independent, publicly traded companies, Crane NXT, Co. and Crane Company. Crane NXT, Co. operates the erstwhile Payment & Merchandising Technologies segment while Crane Company retained its Aerospace and Electronics, Process Flow Technologies, and Engineered Material segments.

While Crane Company's reported sales growth in the first half of this year was impacted by the divestiture of Crane supply business of its Process Flow Technologies segment in May 2022, the core sales growth has seen good momentum since its spin-off, thanks to good demand in the majority of its end markets and a healthy backlog. In the third quarter of 2023, Crane Company continued to see good demand momentum in its end markets. In addition, the company also benefited from price increases, good backlog execution, and volume growth in the Aerospace & Electronics and Process Flow Technologies segments. In addition, favorable foreign exchange also benefited the sales growth in the quarter. This resulted in a 10.4% YoY increase in sales to $530 million. Excluding a 1 percentage point benefit from foreign currency, core sales increased by 9.3% YoY.

On a segment basis, the Aerospace and Electronics segment posted a 23.9% YoY sales growth, as a result of healthy demand from aircraft manufacturers as the industry continues to see a good increase in air traffic. The Process Flow Technologies segment posted 6.7% YoY sales growth and a 4.8% YoY increase in core sales due to higher prices and strength in Industrial markets. This helped the company offset weakness in the Engineered Material segment, where sales declined by 10.5% due to lower demand from recreational vehicle manufacturers and lower production rates.

Crane Company Segment and Total Revenues (Company Data)

Looking forward, the company's growth outlook is encouraging.

In the Aerospace and Electronics segment, the company is seeing healthy demand trends in both commercial aerospace and defense markets. In commercial markets, air traffic has swiftly recovered post-reopening, and global air traffic is approaching pre-pandemic levels. The demand for new aircraft continues to remain high and while OEMs are ramping up their capacity to meet this demand, demand continues to exceed what the OEMs can deliver. This is resulting in low aircraft retirement and an aging fleet that requires more after-market parts and services. So the demand from the commercial end market is strong for both parts and services.

On the defense side, the recent geopolitical developments have increased the need for investment in research and development as well as increased procurement by the government. I expect the demand to remain strong here as well in the coming years.

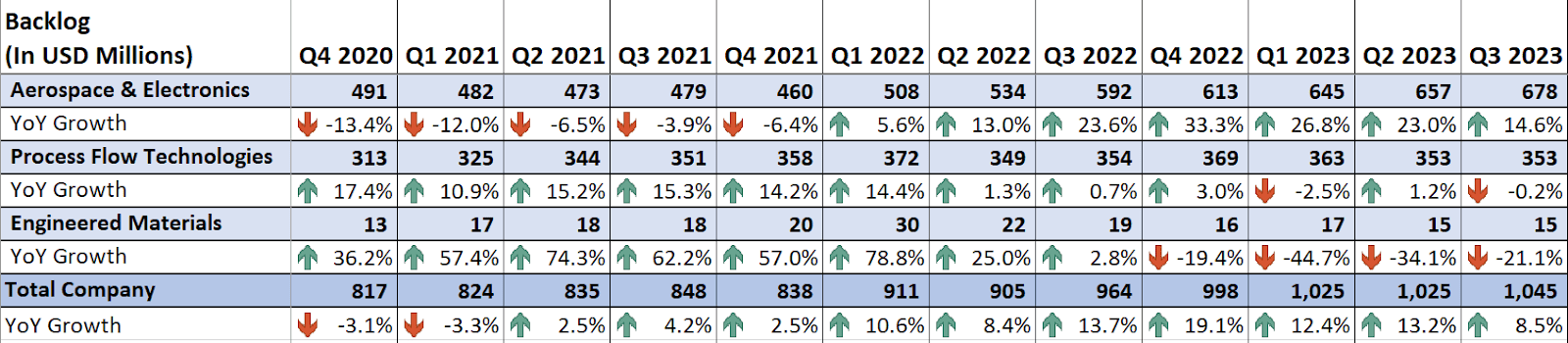

The segment's backlog was up ~14.6% Y/Y at the end of the last quarter which, along with strong end-market demand, sets up the segment for strong growth in the near to medium term.

{kind=link}

In the Process Flow Technologies segment, the end-market demand is not that strong and the clients are delaying projects as the high-interest rate environment is impacting return on investments. However, the company's higher-than-normal backlog has helped it post good revenue growth. The company is also benefiting from innovations and new product launches, which is helping it gain market share. The company has done a good job in terms of new product launches and its product vitality score has risen meaningfully in recent years, which has helped it outperform its end markets.

Crane Co. Product Vitality (Company Presentation)

While I expect flattish to slightly down sales for this segment for the next couple of quarters, I believe a potential reversal in the interest rate cycle by mid-2024 can catalyze a demand recovery in the market which along with good execution and market share gains bodes well for the segment's growth in the late 2024 and beyond.

Long-term management is focusing on high-growth core target markets like industrial automation, water, waste-water, pharmaceuticals, and chemicals which have secular drivers to drive growth, and has plans to increase total revenue derived from these end markets to ~75% from the current ~60% by in the next few years, to improve overall growth profile of the segment.

Crane Co.'s target growth market for PFT segment (Company Presentation)

The company's third segment engineered material is relatively small (comprises ~10% of total revenue and single digit percentage of total segment profit) and while it is facing demand headwinds currently, I don't expect it to have a significant impact on the overall results.

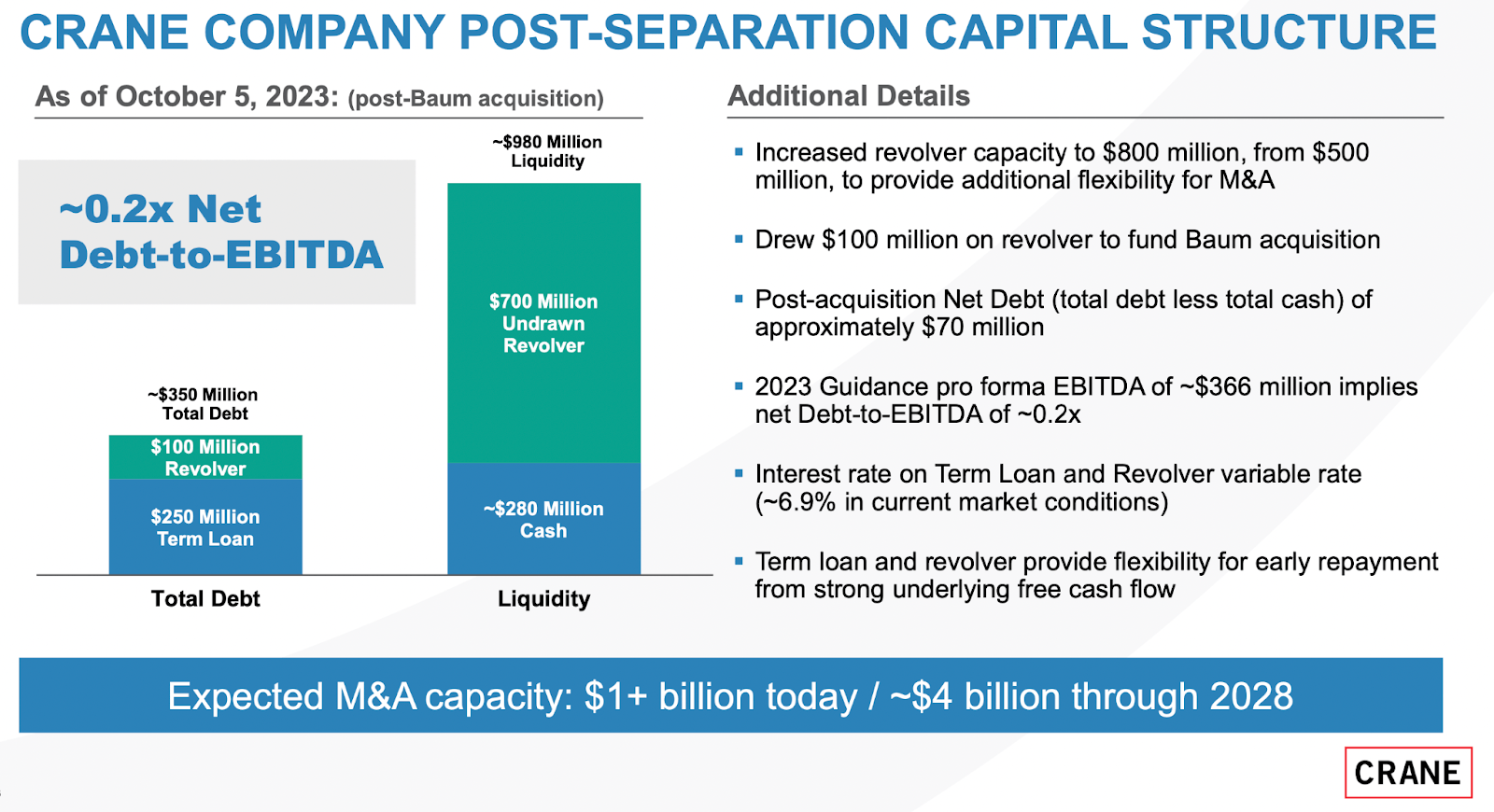

The company also has a healthy balance sheet with a net leverage of only 0.2x and an M&A capacity of ~$1 bn.

Crane Co.'s leverage ratio and liquidity (Company presentation)

{kind=link}

This should enable management to do M&A deals, which should add to the organic growth.

Overall, I am optimistic about the company's near as well as long-term prospects. In the near term, the strong growth in the A&E segment should more than offset a flattish to a slight decline in PFT sales and a slowdown in the engineered material segment. Once the interest rate cycle reverses in the medium term, the PFT segment's sales should return to growth and add to the company's overall growth. In addition, the company's healthy balance sheet should enable it to pursue inorganic growth opportunities.

Margin Analysis and Outlook

Over the past year, the company's margins have seen headwinds from supply chain challenges and inflationary input costs. However, the company has successfully mitigated these headwinds with the help of price increases and productivity gains.

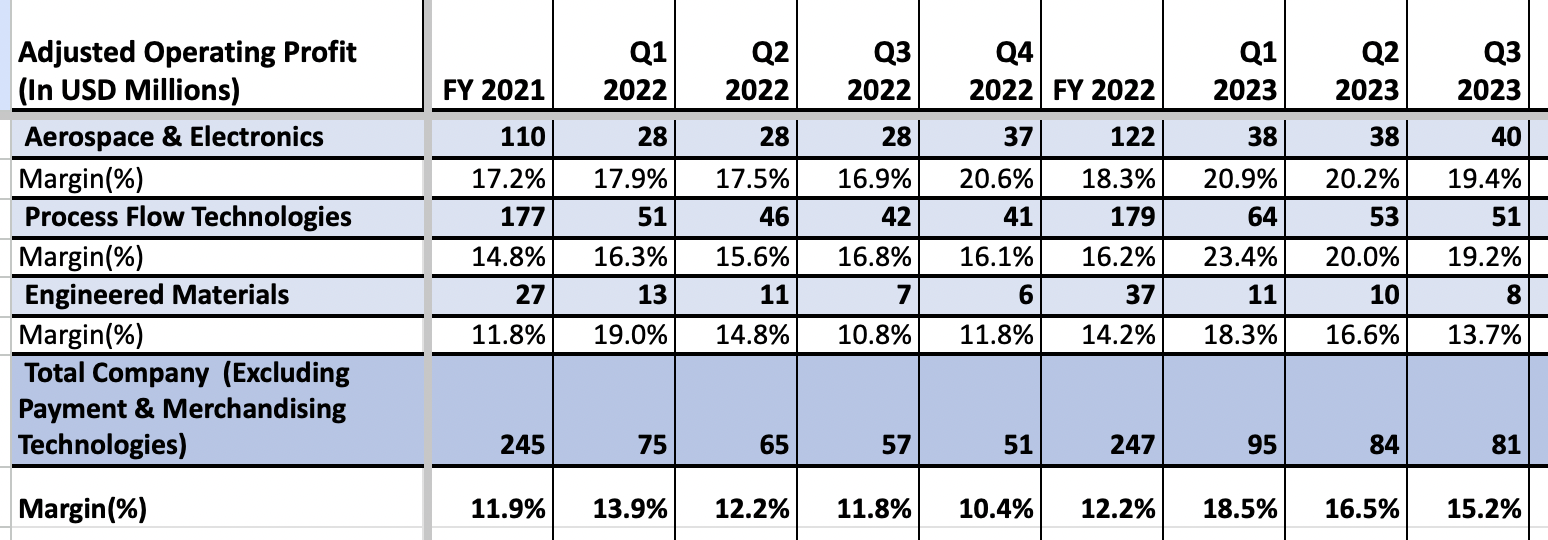

In the third quarter of 2023, the company margins continued to benefit from price increases, volume leverage, and productivity gains, and its adjusted operating margin increased by 340 bps YoY to 15.2%.

{kind=link}

Moving forward, I am optimistic about the company's margin outlook.

In the A&E segment despite the continued supply chain headwind, which adds costs like those related to expediting shipment, the company is expecting ~33% incremental margin in FY23 (as per management guidance) helped by pricing initiatives, productivity improvements, continued investments in technology to improve efficiency, and adjusting staffing levels in factories. The incremental margins next year should be even better, with the supply chain situation expected to improve. So, a good operating leverage from increased sales coupled with cost control, easing supply chain constraints, and productivity improvements bodes well for the company's growth. Prior to the pandemic, this segment used to have an operating margin in the mid-20s, and I see its margins recovering back to those levels in the medium to long term.

The company is also doing a good job in terms of improving margins in its PFT segment through strong execution and pricing increases. In addition, core target markets for this segment, which are growing at a higher rate and where management intends to increase its exposure in the coming years, have higher margins than the segment average, which should help the margin mix moving forward.

PFT segment's higher growth markets have higher margins as well (Company presentation)

For the next year, despite sales-related headwinds, management is targeting flat to modestly up margins for this segment. Once the revenue growth starts improving from FY25 onwards, the segment should see good operating leverage and margin improvements.

Valuation and Conclusion

Crane Company is currently trading at a ~23x FY24 consensus EPS estimate of $4.68. This is at a premium to its 5-year historical average forward P/E of 15.3x. The company has good revenue and margin growth prospects, and there is also a good amount of balance sheet flexibility to drive inorganic growth through bolt-on acquisitions. However, I believe the stock has already seen a good amount of re-rating post separation with Crane NXT (which is trading at a comparatively lower multiple) and there is limited potential for further expansion of the valuation multiple from current levels. One of the company's multi-industry peers, Honeywell ( HON ), which also has a good exposure toward the Aerospace end market and where I have a buy rating , is trading at 20.34x FY24 consensus EPS estimates. Hence, I prefer to remain on the sidelines and wait for a better entry point. For now, I have a neutral rating on the stock.

For further details see:

Crane Company: Good Growth Prospects But Valuation Leaves Little Room For The Upside