WEX - Crane NXT: Still A Bit More Upside In This Currency Play

2023-09-05 10:00:00 ET

Summary

- Crane NXT is a company that focuses on technology solutions for payment transactions and the creation of banknotes.

- The company's revenue increased by 2.2% in the first half of the 2023 fiscal year, with strong performance in the Crane Payment Innovations segment leading the way.

- Net income and profitability metrics for the company worsened year over year, but management has provided positive guidance for the future and shares look attractive enough to warrant some upside.

One of the most interesting companies to come across my radar this year has been Crane NXT ( CXT ). Originally spun off from its parent company, Crane Company ( CR ) earlier this year, the business focuses on a couple of primary sets of operations. About 65% of its revenue comes from Crane Payment Innovations, which provides technology solutions that help in the detecting and authenticating of payment transactions.

The second unit is called Crane Currency. For those who don't know, it focuses mostly on the creation of technology involved in securing and authenticating banknotes. In fact, it has served as the only supplier of US currency paper since 1879. In recent months, shares of the business have roared higher, with shareholders being rewarded for their vote of confidence in the company. Financial performance has been admittedly mixed. But management has increased guidance and shares are not unrealistically priced. All combined, this makes for a solid prospect that investors should consider for their portfolios.

Checking in on recent performance

The first thing that attracted me to Crane NXT was the company's interesting business model. I have a soft spot for firms that have unique operations. So the thought of a firm that supplies currency paper to the government and that also focuses on technology that aids the monetary system of this nation made it right up my alley. What made the picture even better was the fact that shares were trading on the cheap, and the company had some attractive growth potential bottled up in the form of catalysts that could propel shares even higher in the years to come. This combination of factors led me to even rate the company a 'strong buy', a rating that reflects my view that shares should significantly outperform the broader market for the foreseeable future. Since the publication of that article back in early April of this year, the S&P 500 has jumped 10.1%. While impressive, the increase pales in comparison to the 35.6% rise enjoyed by shareholders of Crane NXT.

{kind=link}

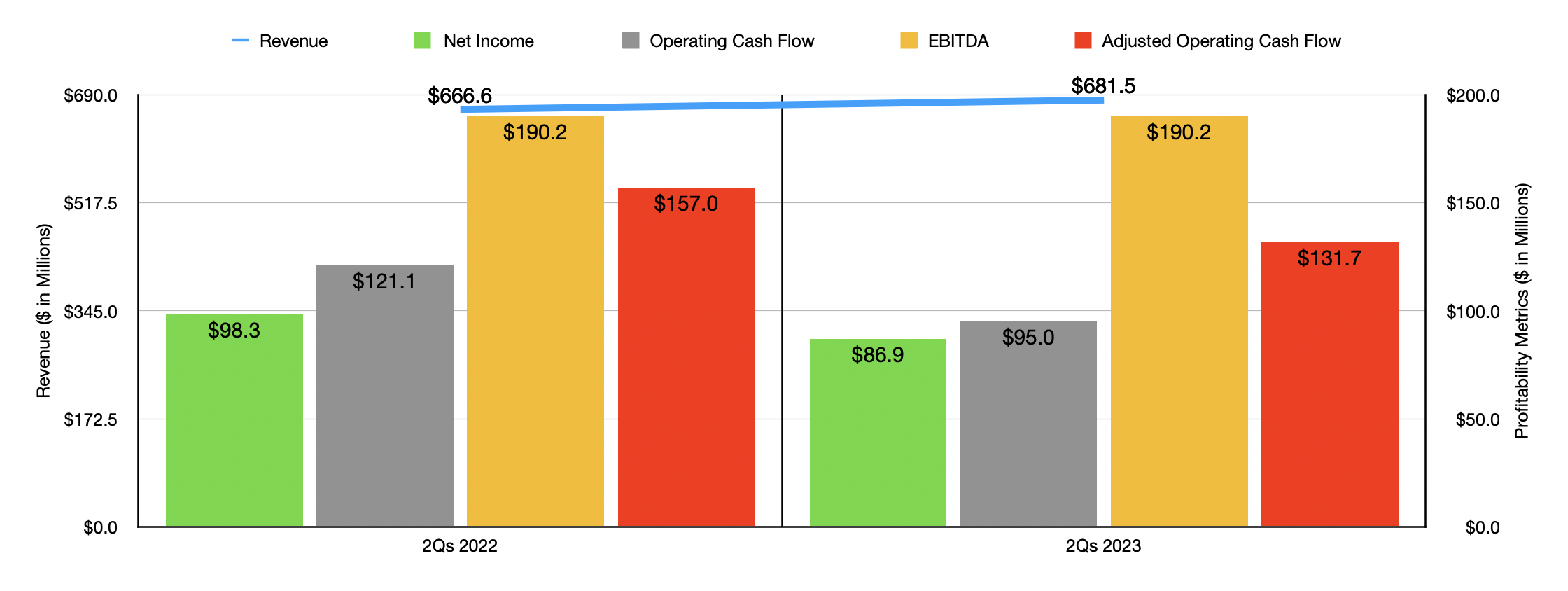

Even though share price performance suggests that overall fundamental performance for the company has been robust, the picture is more complicated than that. Let's start, though, with the good news. During the first two quarters of the 2023 fiscal year, revenue for the enterprise came in at $681.5 million. That's 2.2% above the $666.6 million reported one year earlier. Management attributed this mostly to higher pricing for its offerings. Interestingly, revenue would have been even higher had it not been for foreign currency fluctuations. These impacted sales negatively to the tune of $15.4 million.

It is important to point out that not every part of the company performed well. There was a strong side for the first half of this year and a weak side. The strong side involved the Crane Payment Innovations segment. Revenue jumped 6.5% from $422.4 million to $449.7 million. Stronger demand for things like its payment acceptance and dispensing products, as well as for various services associated with a growth in contract sales, combined with higher pricing to push revenue higher. On the other hand, Crane Currency faced some difficulties, with revenue dropping 5.1% from $244.2 million to $231.8 million. This was driven by a $12.4 million decline associated with banknote and security product sales. Lower volumes and foreign currency fluctuations played a role in this, hitting the company by $4.1 million. The other $8.4 million came from lower core sales reported by management.

All combined, it was great to see revenue increase, even if this sales growth was not terribly large. On the other hand, performance on the bottom line was largely negative. Net income, for instance, shrank from $98.3 million to $86.9 million. A decline in the gross profit margin for Crane Currency from 41.4% to 39.9% occurred because of foreign currency fluctuations and lower volumes that were only partially offset by productivity gains and an unfavorable product mix. Selling, general, and administrative costs rose from 14.9% of sales to 17.4%. Management chalked this up mostly to higher selling and engineering costs. After all, this is a technology company. So the engineering side of the equation makes sense. Fortunately, Crane Payment Innovations came to the rescue, with an increase in overall operating margin from 23.7% to 28.2% being driven by higher pricing and a greater volume of service contract sales.

Other profitability metrics for the company also worsened year over year. Operating cash flow, for instance, went from $121.1 million to $95 million. If we adjust for changes in working capital, we would get a drop from $157 million to $131.7 million. When it comes to EBITDA, there is something that I need to discuss. Management gives a reading of $192.2 million for the first half of 2023. However, they don't give a calculation for the same time last year. This is actually a problem when you look at some of the financial results covering just the second quarter of the year relative to the same time last year as well. This is because of how management continued financial reporting after the spinoff of this enterprise from the rest of the firm. I calculated my own version, then, of EBITDA for both this year and last year. And this version came out to $190.2 million for each time. That's not far off, and it shows a leveling off of cash flow from that perspective.

Even though management has not been as detailed as I would normally like, they have provided guidance for the 2023 fiscal year in its entirety. They expect core sales, for instance, to grow by between 3% and 5% year over year. They are also forecasting earnings per share of between $3.85 and $4.15. This is actually $0.10 per share higher on both the low end of the range and the high end compared to initial guidance that was released earlier this year. Taking the midpoint of guidance, we would get net profits of $229.2 million for the year. Following the same approach that I followed in my first article on the company, this would imply an operating cash flow of roughly $276.5 million and an EBITDA of around $382.7 million.

{kind=link}

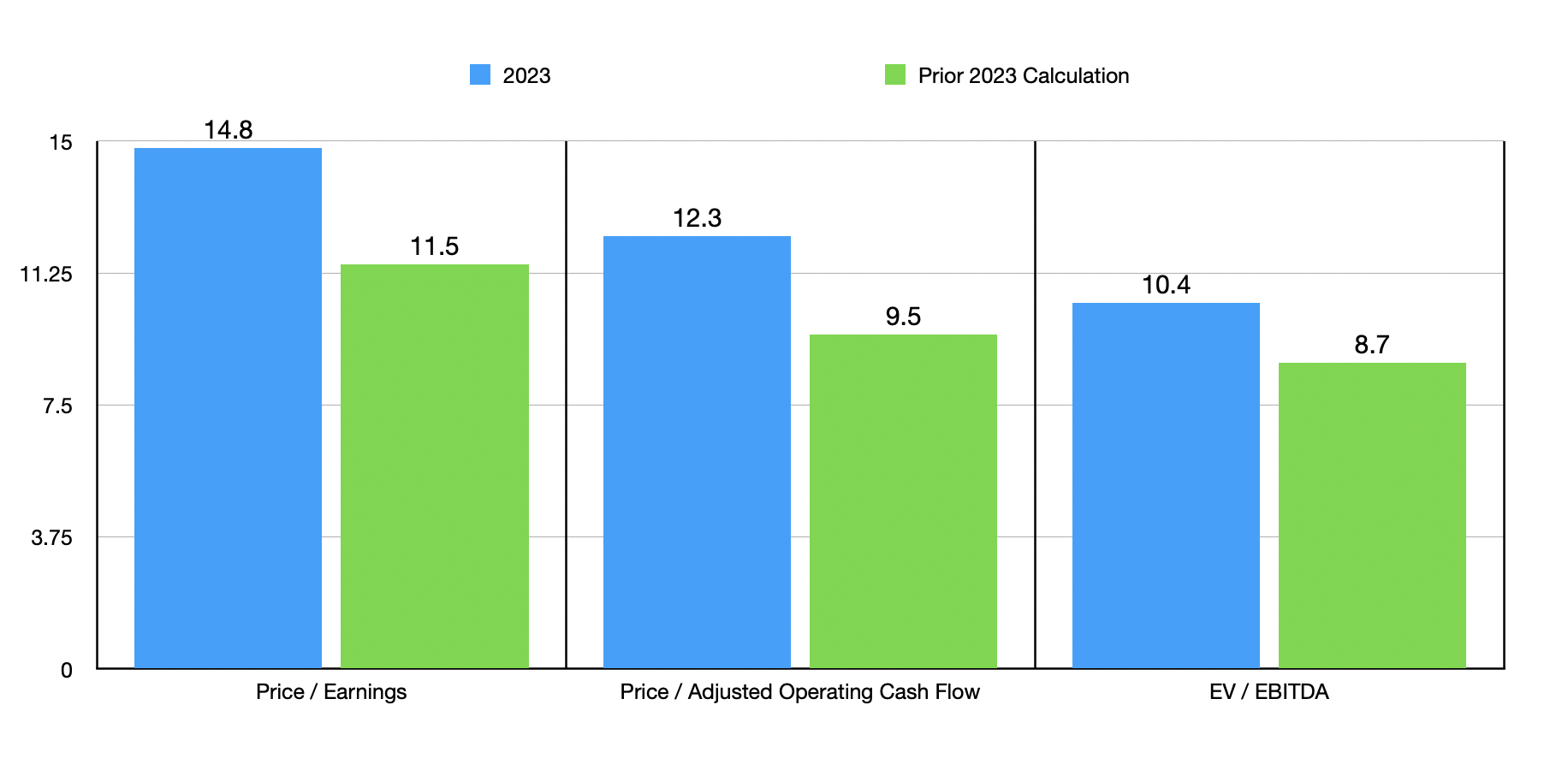

In the chart above, you can see how shares are priced using these metrics. The chart also shows how shares were priced when I last wrote about the company. Clearly, the stock is not as cheap as it was. But I wouldn't go so far as to say that upside is non-existent. In the table below, I compared the firm to five similar enterprises. On both a price to earnings basis and an EV to EBITDA basis, it ended up being the cheapest of the group. And when it comes to the price to operating cash flow approach, two of the five companies ended up being cheaper than it.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Crane NXT |

| 14.8 |

| 12.3 |

| 10.4 |

| Global Payments ( GPN ) |

| 41.6 |

| 15.1 |

| 15.3 |

| WEX Inc. ( WEX ) |

| 40.5 |

| 7.7 |

| 11.1 |

| Fidelity National Information Services ( FIS ) |

| 44.4 |

| 8.9 |

| 10.5 |

| Jack Henry & Associates ( JKHY ) |

| 31.4 |

| 30.2 |

| 17.4 |

| Payoneer Global ( PAYO ) |

| 200.8 |

| 19.4 |

| 114.2 |

Takeaway

This year is proving to be a bit lumpy for Crane NXT and its investors. However, the market has realized just how cheap shares are and has rewarded shareholders handsomely. If management can come through on their guidance for the current fiscal year, the stock looks reasonably priced. It definitely does not have the kind of upside that it did previously. But I do think it is worthy of at least a soft 'buy' rating at this time, especially when stacked up against other companies that have similarities to it.

For further details see:

Crane NXT: Still A Bit More Upside In This Currency Play