BNCZF - Credit Agricole: Already Looking Ahead

- Beat to consensus on revenue growth and lower cost of risk.

- Strong performance in its home market but also in Italy.

- Supportive valuation based on its TBV. Already ahead of its internal forecast estimates.

Our readers know that we intensively follow the European bank environments. Looking at the French financials, we already presented SocGen and BNP Paribas Q2 results. Yesterday, it was showtime for Crédit Agricole ( CRARF ) which reported strong financial performance. Indeed, the stock price was up by more than 4%.

Our buy case recap is based on the following:

- Acceleration of Crédit Agricole 'Ambitions 2025 Plan'. The French bank " plans to raise the integrated bank-insurance-asset management business model ". The strategic plan also includes more details, so we recommend that our readers check up on this publication so that they are well acquainted with the story;

- New inorganic growth, especially in the Italian market - ( we also commented about the latest M&A )

- Strong Q1 results and a low impact from Russian activities.

Half-year Results With a Focus on Italy

Starting with the CASA numbers and looking at the bottom line, the group's net income stood at €1.97 billion against the consensus expectation that was forecasting €1.17 billion. This was driven by revenue growth and lower provision. In particular, the French bank emphasized a very good performance in gross clientele capture, in numbers, customers increased by more than 450k (the best-performing markets were France, Poland and Italy). Regarding the cost of risk, Crédit Agricole was well below Wall Street analyst numbers - the company reported a CoR of minus €203 million against a consensus that was forecasting a minus €590 million. Moreover, and in line with our estimates, the Russian exposure declined by almost €400 million in the quarter.

Crédit Agricole CoR Evolution (Crédit Agricole Q2 Results)

Looking at the division, the group overperformance was achieved by the following segment:

- The large customers division achieved strong growth thanks to CIB results and the financing sub-division;

- The insurance division - this was very similar to AXA's Q2 performance ;

- The international retail division was led by Crédit Agricole Italy's three-month account.

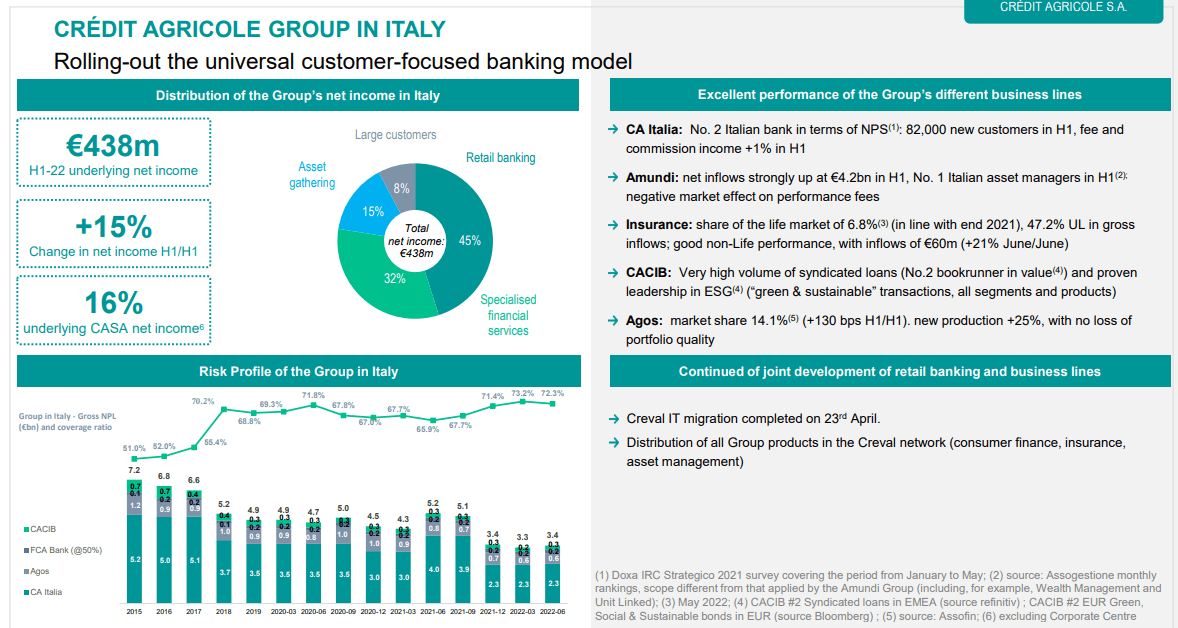

Looking specifically at Italy, in the first half of the year, all activities recorded an aggregate underlying net income of €438 million signings a plus 12%. In detail, the Italian arm reported a turnover of €1.27 billion (stable year-on-year) and operating costs down by 3.6% to €792 million with a cost/income ratio again down at 59.6%. Crédit Agricole Italy once again demonstrates better profitability and resiliency across the cycle.

Another important consideration is related to Banco BPM in which Crédit Agricole S.A. acquired a 9.18% equity stake. For the first time in 11 years, the ECB raised interest rates by 50 basis points. According to our calculation, on average, European banks' EPS will rise by 8% for each rate increase of 50 basis points. However, Italian banks are above average, in particular, Banco BPM in which we expect a rise of almost 30%. This is very supportive of Crédit Agricole's future accounts.

Crédit Agricole Italy (Crédit Agricole Q2 Results)

{kind=link}

Conclusion and Valuation

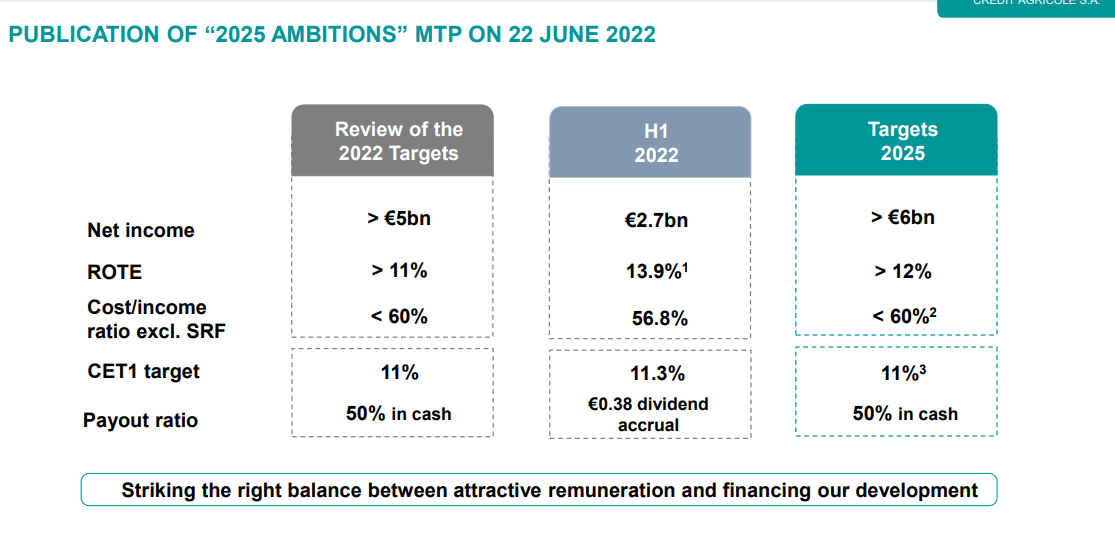

Last time, we really deep-dived into the valuation. We knew that we were above Wall Street analysts' future estimates. Thanks to Crédit Agricole S.A.'s Ambitions 2025 Plan, we were forecasting a turnover " increase by an average 2021-25 CAGR of 3.5% versus a consensus estimate of 2.6%. The company plans a cost/income ratio capped at 60%, and consequently a profit CAGR of +3% over the same horizon. Even if costs are not disclosed, IFRS17 expenditure is forecasted to be neutral on capital by 2025". During the quarter, the Crédit Agricole CET1 ratio was up by 0.3%. Here below, we can see that the company is already ahead of its Ambitions Plan. Thus, we continue to have full support for our premium valuation, indeed, we derive a €13 stock price versus the current €9.68 per share. (We also have support for its TBV discounted compared to peers (ex-SocGen) by almost 20% and its dividend yield).

Higher Guidance (Crédit Agricole Q2 Results)

{kind=link}

For further details see:

Credit Agricole: Already Looking Ahead