CRARF - Credit Agricole: Earnings Growth Momentum With Attractive Acquisitions

2023-09-06 06:03:39 ET

Summary

- French banks are not facing regulatory risk on windfall tax as is happening in other EU countries.

- Crédit Agricole is a buy thanks to its ability to maintain deposits and achieve cost target initiatives. This is also coupled with M&A optionality to supper earnings growth.

- Despite a positive net profit trajectory, the bank trades at a lower tangible book value. Our buy rating is then confirmed.

Following our recent update on Société Générale , today we are back to comment on the French banks. While the Italian government remains open to a review of the banking extra profit tax, we are not forecasting this risk in France. Why? To date, new taxes on banks have been invoked not only in Italy but also in Spain , Hungary , and the Czech Republic . Here at the Lab, we question the logic behind these populist measures. There is a risk of discouraging banks from lending money to businesses and personal clientele, especially if the levy is calculated as a function of interest margin growth and if it drives up their cost of capital. Furthermore, if a government intends to tax the banks when rates go up, the question arises whether they will be willing to support them when rates start going down again, and we very much doubt that. The UK moved in the opposite direction, while the finance minister ruled out the possibility of a banking tax in France. We should also note that it is reasonable to expect a rate normalization, and the ECB's recent monetary policy will not necessarily result in increased profitability, as it should be offset by higher cost of funding, higher provisioning, and higher default rates for some corporations.

Therefore, we prefer banks less susceptible to domestic political risk, able to maintain deposits without pricing pressure, and also able to support cost savings initiatives and capital reallocation. With this characteristic, Crédit Agricole stands out (CRARF).

Why are we still supportive?

- Following the ' Ambitions 2025 ' strategic plan and post-Q2 results, we believe that the bank will achieve its cost targets thanks to recent acquisitions with a lower cost of risk. Here at the Lab, we anticipate that a cost/income ratio below 58% is within reach;

- Crédit Agricole improved its capital generation and remained committed to a 50% payout ratio. Although the CET1 ratio was 11.6%, and we projected a 2024/2025 ratio above 11%, the dividend payout is unlikely to increase (Fig 1). This follows the management's comment on M&A optionality;

- Indeed, the company's recent acquisitions fuel the net profit. In numbers, the RBC Securities deal is guided to generate an additional income of more than €100 million by 2026, while the Degroof Petercam acquisition is expected to achieve a pre-synergy net profit of €80 million per year starting from 2024;

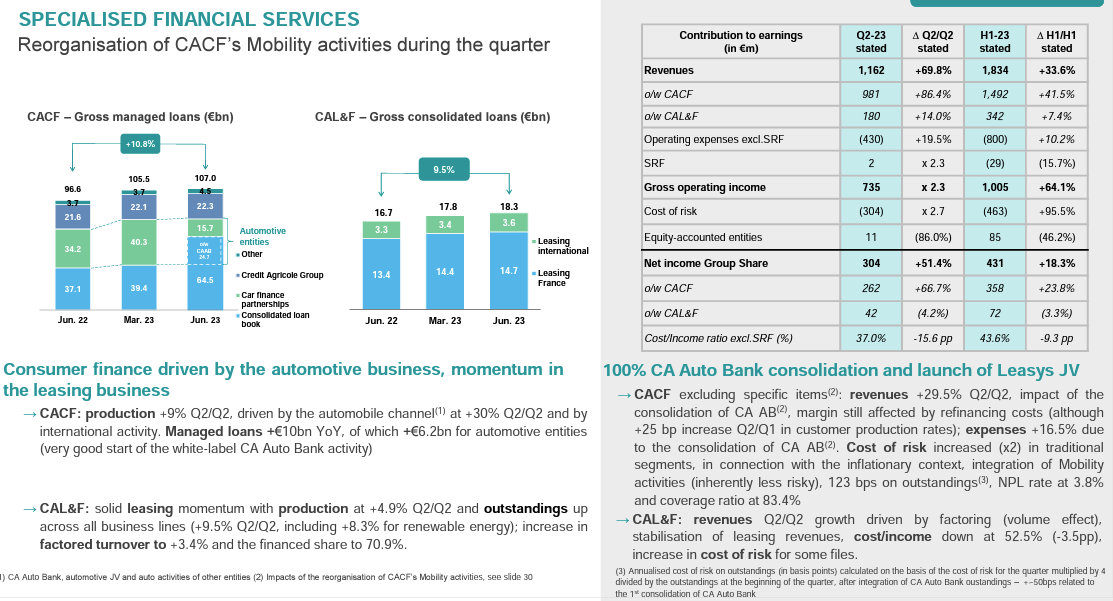

- Still related to point 3), it is vital to emphasize the CA Auto Bank's current opportunity (Fig 2). The heir of FCA Bank passed to Credit Agricole is untied from Stellantis. The company is expanding with new partnerships and recently signed a new deal with Tesla and Lucid . As of June-end, the company had approximately €24.7 billion in loans, with Stellantis's portfolio reduced to €10 billion. The half-year financial statement is positive, with a net result of around €270 million. Indeed, CA Auto Bank has launched new partnerships and has already developed new agreements to operate in nine new countries by year-end. CA Auto Bank is also expanding its financial services in short-medium-long term rental, subscription, and car sharing. A major industrial renewal is underway, supported by a new electric mobility era. Here at the Lab, thanks to our supportive coverage, we suggest our readers check on our previous ALD ( SocGen ) and Arval ( BNP Paribas ) coverage. According to the bank, CA Auto Bank will have a positive €62 million net profit impact in Q3 and a significant positive upside in the future, given that new business is picking up faster than expected. We believe that earnings optionality will partially offset the headwinds on the higher cost of risk;

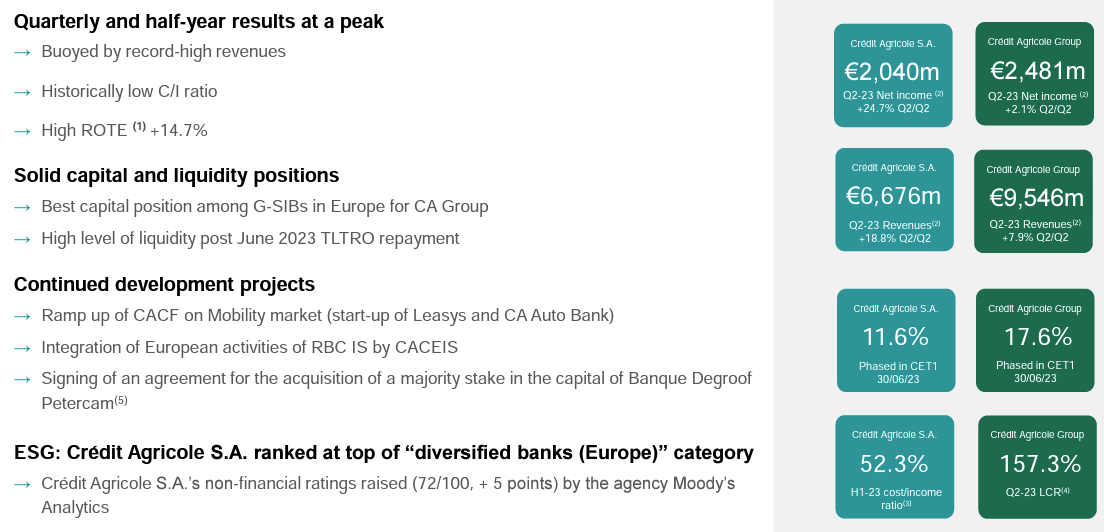

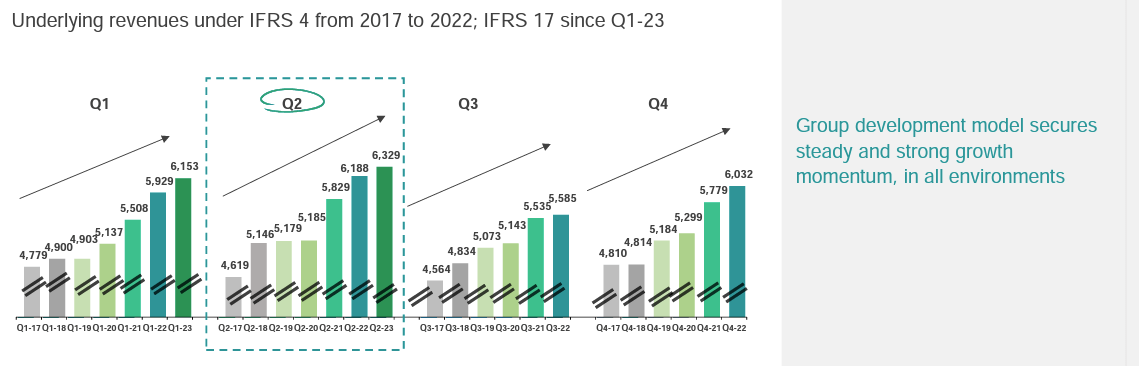

- Post Q2 results, very briefly, it is vital to report that the company has a solid liquidity cover ratio of 157.3% with €334 billion in liquidity reserves. Despite a favorable interest rate evolution, expenses are well under control, and looking at the record, Crédit Agricole managed to secure steady earnings growth (Fig 3);

- Here at the Lab, we are also forecasting a higher cost of risk for the next visible period in the 35 basis points area vs. the 29 basis points recorded in Q2 (Fig 4). This is for prudency reasons, and to support Crédit Agricole's investment thesis, we should report that the bank has loan loss reserves of €20.6 billion. This was an increase of €3.3 billion from Q4 2019, and the company has one of the best coverage ratios for doubtful loans among the EU's largest banks (83.6% at June end).

Crédit Agricole Q2 Financials in a Snap

{kind=link}

Fig 1

Crédit Agricole Q2 CA Auto Bank

{kind=link}

Fig 2

Crédit Agricole Earnings Growth Story

{kind=link}

Fig 3

Crédit Agricole COR

Fig 4

Conclusion and valuation

The company's defensive position might address future deteriorating assets and a safer shareholder remuneration. Even if, despite a higher EPS, we left unchanged our DPS forecast, Crédit Agricole is now yielding 7.5% and 8% in 2024 and 2025, respectively. The group's capital position is reassuring, even if capital buffers are lower than other international competitors. We supported the strategic plan, and the company already achieved a better-than-expected ROTE (target at >12% with Q2 results of 14.7%). Crédit Agricole reached a net tangible book value per share of €14.9; in our estimates, we have adjusted net income from €4.8 in 2022 to €5.28 in 2024, thanks to recent acquisitions and higher rates. For this reason, we increased our tangible book value to €16.39 per share, and with a target TBV of 0.8x, we slightly increased our buy rating from €13 to €13.1 per share. We should recall that the bank offers a lower yield vs. comps ( UniCredit , ISP , and BNP Paribas ) and still has crucial Russian exposure ( €6.7 billion ).

For further details see:

Credit Agricole: Earnings Growth Momentum With Attractive Acquisitions