CRARF - Credit Agricole - Why This French Bank Is A 'Buy' (Rating Upgrade)

2023-06-23 12:41:43 ET

Summary

- I retain a small position in the French bank Credit Agricole. I've held it for many years, missed some opportunities to sell, and am now looking at late 2023.

- Fundamentals for this bank are rock-solid - it's time to look at what we can expect, and whether the company's growth estimates fulfill my minimum target of a conservative upside.

- I'm switching my target to €11/share, with an overall "BUY".

Dear readers/followers,

You may not consider Crédit Agricole ( CRARF ) one of the best banks in the world - but I would argue that if you consider this a poor investment, you're most definitely missing the mark here. In this article, I'll show you why this bank, with its A+ rating and its yield of around 9.7% for the 2022A dividend, is one of the better banks you could invest in Europe at this time.

Let's review recent results and see what we have. Oh, also - just so you know. I've been positive about Crédit Agricole for some time - just not in my last article. I went "HOLD" at the time, and I consider myself knowledgeable in the question of when exactly to invest in this bank.

This is how my stance on the bank has turned out since then.

Seeking Alpha Credit Agricole RoR (Seeking Alpha)

Because of the dividend, you're in the positive on this investment. Overall, however, you're still below the S&P500 in the same timeframe.

Let's update the thesis and let me show you why I'm a bit more positive at this time around.

Crédit Agricole - A lot to like, but valuation is absolutely crucial here

La Banque Verte is one of the best banks in France. Why?

Because it's one of the nation's oldest with ties to one of the lifeblood sectors of France - farming. It's the world's largest cooperative institution - which might be unfamiliar to those outside of Europe, but it's also the second-largest French bank after Paribas (BNPQF), as well as the third-largest in all of Europe, much larger than some of the Scandinavian bank. It didn't survive GFC scot-free, being forced to liquidate significant holdings as well as organize some very large rights issues and disposal programs due to the at-the-time newly instituted Basel requirements.

But it survived - and more than that, it was one of the first banks to recover, and I personally know shareholders who made 40% returns in 2009 due to investing in Crédit Agricole.

The company employs a universal banking model that has delivered very strong results over time - the same thing is true for the results we've seen in 1Q23, which is the latest quarter we have for this bank.

What has Agricole managed?

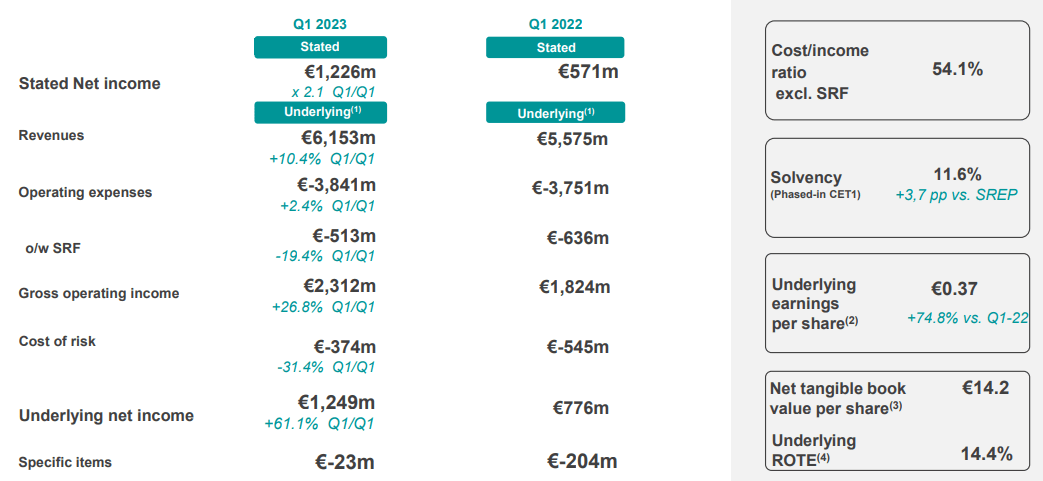

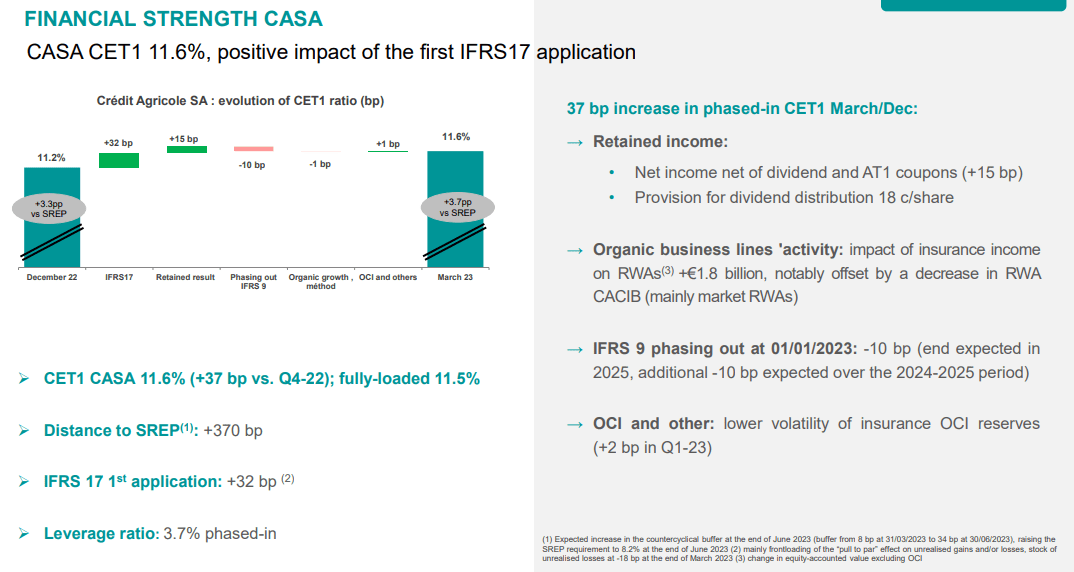

Well, 10.4% revenue growth for one, with a 61.1% improvement in net income for the group, as well as a solid 54.1% cost/income ratio. It's not the best in the business - quite a bit from it in fact, but it's absolutely solid. What's more, the company managed 17.6% phased CET-1, which makes it one of the best-prepared banks in France for any type of financial distress, not to mention nearly half a trillion euros of liquidity reserves.

Crédit Agricole isn't going anywhere - and I expect significant positives from this company going forward. Take a look at some of these trends (pro-forma IFRS 17).

Credit Agricole IR (Credit Agricole IR)

{kind=link}

Not bad, for sure. Buying this company cheap is not always possible - and it might even be considered not that cheaply now. But there are good trends to consider here, and why some of the valuation trends are justified.

The company managed to add over 550,000 customers in half a year alone. Crédit Agricole also had record results for its insurance sector with good mix in P&C as well as the automobile channel, seeing over 38% YoY growth here.

Retail banking saw good trends - with a slight growth in deposits, while loans managed to sustain some growth, with 4.7% YoY growth to professionals. The company is active in geographies like France and Italy - seeing far more resilience than you might expect in a bearish market.

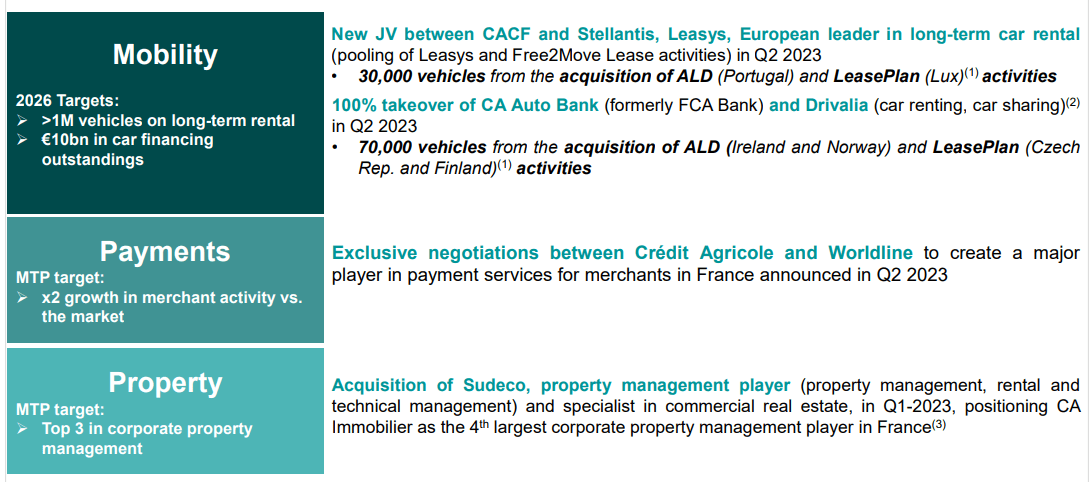

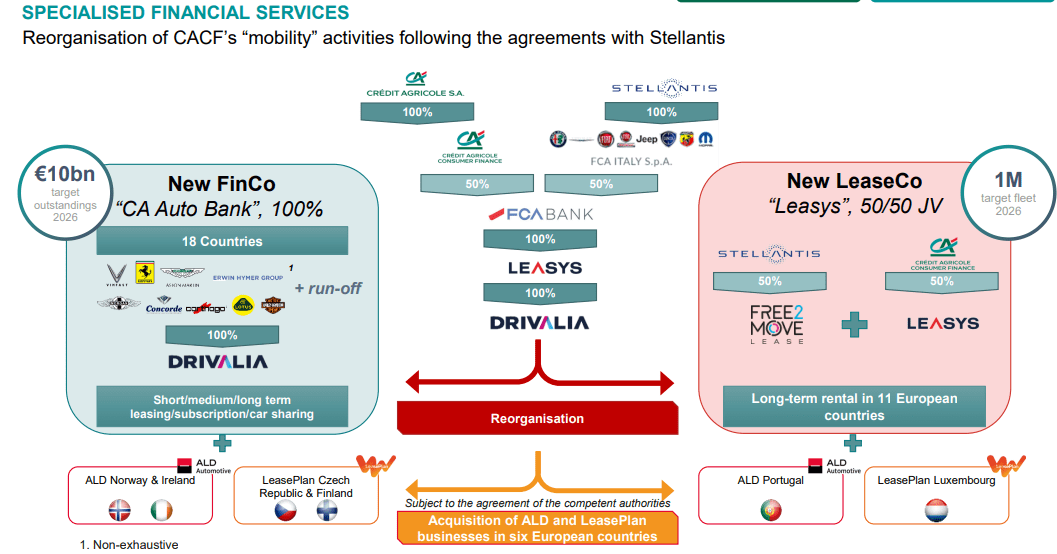

Agricole has a mobility segment - and with a new JV between some major players in the market, CA is destined to see further growth not only in automotive, but payments and property management as well.

Credit Agricole IR (Credit Agricole IR)

{kind=link}

So, the bank is active in a multitude of fields, and with underlying businesses growing solidly across several fields, including but not limited to asset gathering, large customers, retail banking and somewhat flat results in SFS.

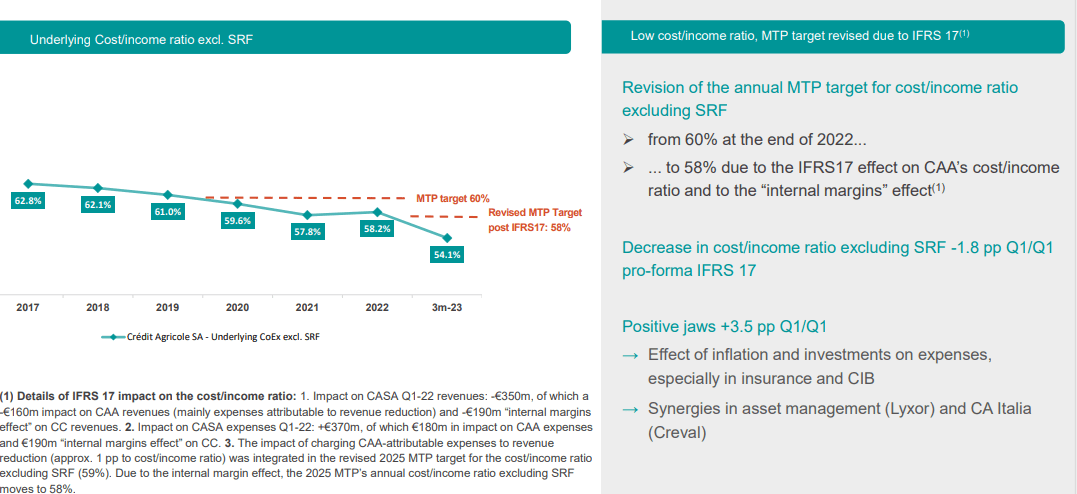

Expense management is decent. They're up, but much of it is IT, payroll and some variable comp, which has seen some positive trends, up around 2.4% YoY. Underlying C/I is seeing very good trends, especially over time with a decline from 62.8% in 2017, to below 55% in this quarter.

Credit Agricole IR (Credit Agricole IR)

{kind=link}

The increased interest rates has done their share in lowering the bank's cost of risk and hedging, and the financial strength of the company puts it in the best capital safety position in Europe, with an SREP distance of 870 bps.

Aside from some Scandinavian banks, there is none better here.

Credit Agricole IR (Credit Agricole IR)

{kind=link}

The one thing that can be said for Crédit Agricole that differs it somewhat from peers is the sort of specialized financial services it offers. This can be thought of either as a boon or a drawback, depending on how you want to invest. It involves things like the new FinCo Credit Agricole Auto Bank, as well as the Leasys JV. CA will own 100% of the FinCo and 50% of the LeaseCo JV.

Credit Agricole IR (Credit Agricole IR)

{kind=link}

This will be one of the more significant JVs and specialized segments in Europe for all things automotive and leasing.

All in all, I don't see much potential downside for the company in the longer term - but nor do I see any massive upside given the company's costs. This is probably why most analysts following the company don't expect massive, double-digit growth from the company here either.

The focus remains on company cost control. Positives have been the so-called "jaws" performance. This is also where the bank has probably the most potential to save more money, and as such, improve its performance further. For the time being though, with the C/I now below 55%, I believe that the company, given its somewhat more complex operating structure, will have difficulties actually getting below this.

What I like about Agricole is the bank sticking to that 50% payout on a very consistent basis. If the company has a €1-€2 EPS, you can expect a €0.5-€1/share dividend for that year. This puts the company dividend at around 7-9% for the next few years, which even considering inflation is very good.

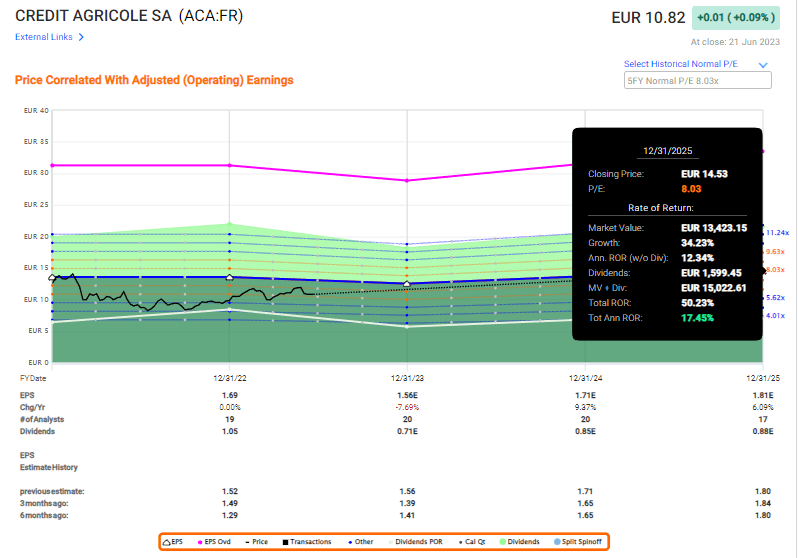

We could go ahead and discuss the growth potential in individual markets - but I still think what's more relevant is the bank's high-level performance and targets. I expect EPS to improve slightly over the coming few years after 2023, with a decline this year. I believe a company EPS between a €1.5 trough level and a €1.7-€1.8/share level is something we really can expect from the bank, and that would make a share price target between €9-€11/share valid based on an 8-10x P/E. The 8x-10x P/E might seem small, but let me clarify this somewhat in the valuation section.

Crédit Agricole - The valuation is attractive enough here if you're willing to view it as a "bond"

This company has an almost bond-type level of long-term safety. That's long-term safety, not short-term. If you "BUY" the company at the right price, you can expect a solid yield coupled with a good upside. At today's valuation that is technically possible, though you would have had a better potential during last fall, when the company traded at single-digit share price levels. The upside to a longer-term 8x P/E here is still over 15% annually though.

FAST Graphs CA Upside (FAST Graphs)

{kind=link}

And I consider this to be likely enough for an investment. In my last article, I called for an €11/share PT - that's still my target now, and at a €10.82/share native share price, that makes the company a "BUY".

Plenty of finance companies and banks are currently on sale - Crédit Agricole is certainly not the only undervalued financial company. It also doesn't have the most solid analyst accuracy - though I hasten to add that most of that lack of accuracy was over 8 years ago - the bank has grown far better and safer over the past 6 years.

Overall, I don't see many arguments against owning Crédit Agricole long-term. With the company's share price below €11/share, I believe you can buy it, and in the longer term, you'll get out on top. You have one of the largest banks in France as your safety - something very serious would have to happen for this to destabilize - and after what happened to Credit Suisse, I doubt many banks in Europe are up for taking the riskier road.

Agricole trades at a peer group that includes several banks and financial companies, and it is neither particularly overvalued compared to peers like the National Bank of Canada, Canadian Imperial ( CM ), Truist ( TFC ), and others. It is also not, however, particularly cheap. There is not much to like here from a peer perspective in terms of undervaluation. I own several of these banks, with large positions in companies like Truist as well as Scotiabank (BNS) and Toronto-Dominion (TD). if you follow my writing, you should in fact know that I have a high exposure to financials, and insurance and banks chief among them.

Crédit Agricole is both - and that makes it very attractive indeed.

I now consider the company to be cheap enough, coupled with its recent results, to warrant a "BUY". The downside is possible, and there are alternatives to CA, but I still believe it to be a 6-9% solid yield - and that is worth highlighting.

Because of that, here is my current thesis for the company.

Thesis

- Credit Agricole is a great bank, with solid fundamentals and good long-term growth prospects. It's one of Europe's leading banks, and it's also the largest cooperative financial institution on earth. It has a great yield and an A rating in terms of credit. At the right valuation, this company becomes a definite "BUY".

- I believe the recent 6 months in this company have pushed the valuation lower, and the company's forecasts higher to a level where I consider the company buyable.

- Because of that, I now consider Crédit Agricole a "BUY" at my price target of €11/share.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I say this company currently fulfills 4 out of 5 criteria, which means I'm at a "BUY" here, a change from my previous stance.

For further details see:

Credit Agricole - Why This French Bank Is A 'Buy' (Rating Upgrade)