CEQP - Crestwood Equity Partners Preferreds: 9% Yield Strong Investor Protection

2023-06-16 09:15:00 ET

Summary

- The Crestwood Equity Partners LP preferred shares yield 9.24% and have stronger investor protections than most preferreds.

- Adjusted EBITDA rose 11%, and net income surged 87% in Q1 2023.

- Management expects even higher Free Cash Flow in the 2nd half of 2023, which will be allocated to further debt paydown and leverage reduction.

Are you an income investor, looking for attractive dividends with good coverage?

If you don't own any preferred stocks, it makes sense for you to check them out - preferred stocks usually have better dividend coverage than common stocks.

Why? Because preferred dividends are deducted from profits before Net Income available for common dividends is calculated.

Company Profile:

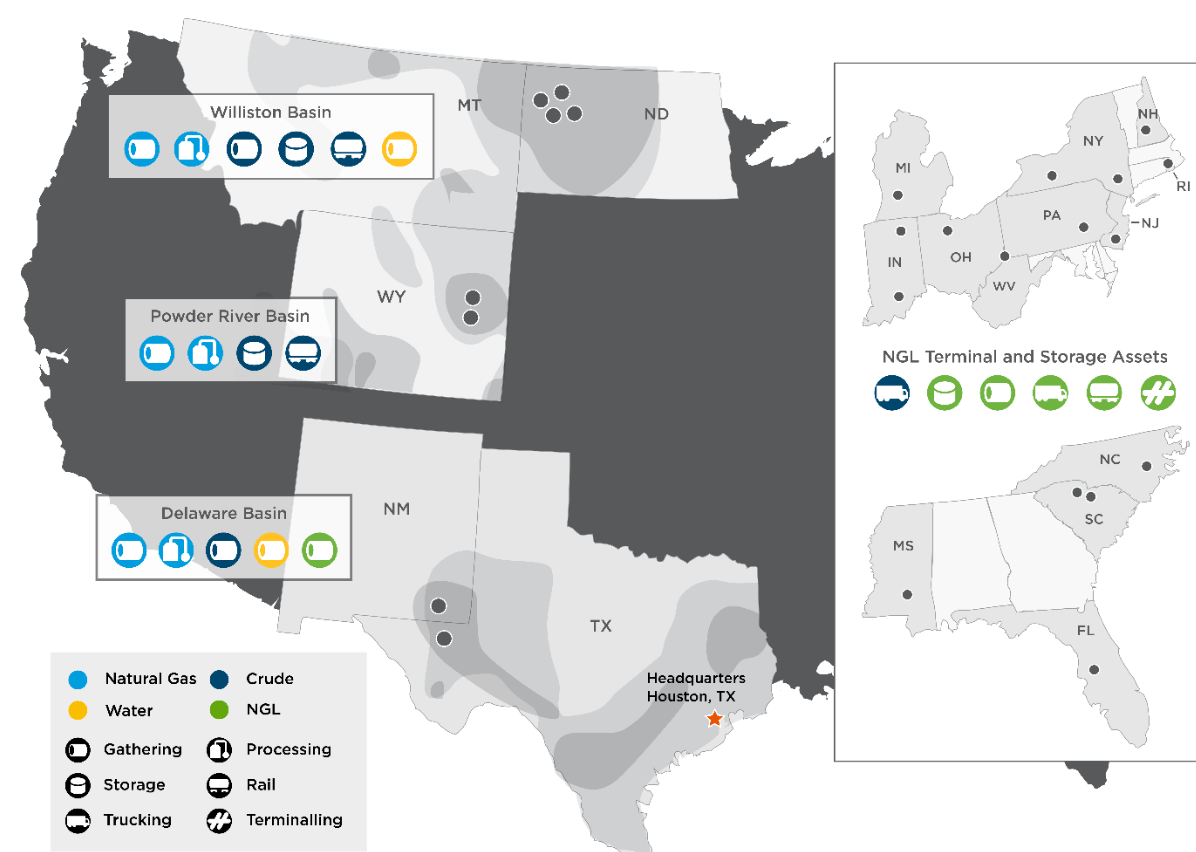

Crestwood Equity Partners LP ( CEQP ) is a master limited partnership ("MLP") that owns and operates midstream assets located primarily in the Williston Basin, Delaware Basin, Powder River Basin and Marcellus Shale.

Its operations and financial results are divided into 3 segments that include Gathering & Processing North, Gathering & Processing South and Storage & Logistics.

Across its 3 segments, CEQP is engaged in the gathering, processing, treating, compression, storage and transportation of natural gas; storage, transportation, terminaling and marketing of NGLs; gathering, storage, transportation, terminaling and marketing of crude oil; and gathering and disposal of produced water. ( CEQP site ).

{kind=link}

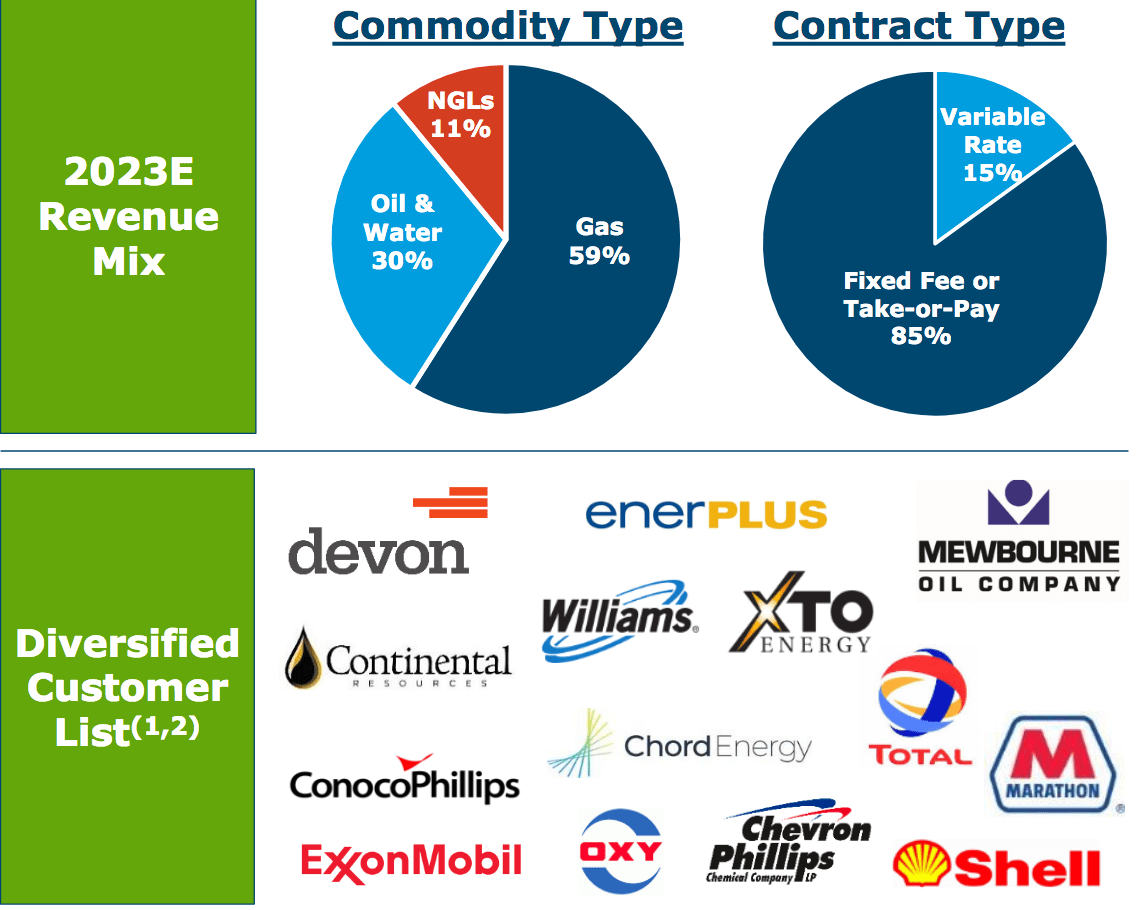

CEQP's business model relies mainly on fixed fee/take or pay contracts, with only 15% of its contracts having variable rates. 59% of Crestwood's revenue is generated by gas, with oil & water producing 30%, and NGL's contributing 11%.

CEQP works on long term contracts with its customers, which include many well-known names in the energy patch. Its Williston and Delaware Basins operations have an average contract tenor of ~9 years, and its Powder River operations have an average of ~13 years.

{kind=link}

Preferred Units Profile:

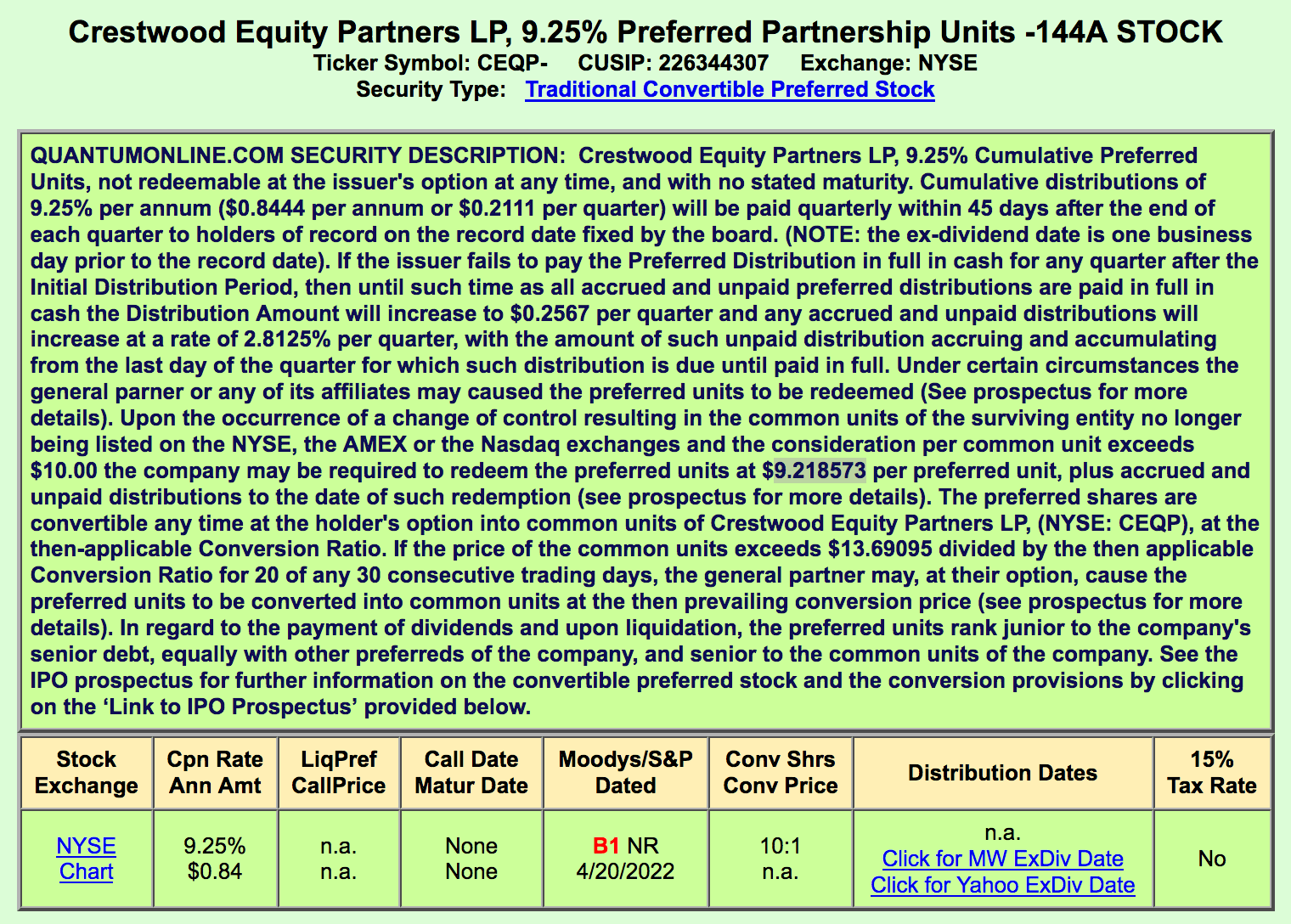

The Crestwood Equity Partners LP - Unit - Pfd Unit 9.25% (CEQP.P) units have more investor protections than most preferred shares, having been part of a Crestwood merger deal back in 2015. The preferred units are entitled to a cumulative distribution of $0.2111/quarter.

However:

"if Crestwood fails to pay the Preferred Distribution in full in cash, then until such time as all accrued and unpaid Preferred Distributions are paid in full in cash, the Distribution Amount will increase to $0.2567 per quarter; Crestwood won't be permitted to declare or make any distributions in respect of any Junior Securities (including the common units) and; ((B)) subject to certain exceptions, certain preferred unitholders shall receive the board designation rights.

If a Change of Control occurs, then each preferred unitholder shall, at its sole discretion:(i) convert its preferred units into common units, at the then applicable Conversion Ratio, subject to the payment of any accrued but unpaid distributions to the date of conversion;

(II) if (1) either ((X)) we are not the surviving entity or (Y) we are the surviving entity but the common units are no longer listed on the New York Stock Exchange or another national securities exchange and (2) the consideration per common unit exceeds $10.00, require us to use our best efforts to deliver to such preferred unitholders a mirror security to the preferred units in the surviving entity ((III)) if we are the surviving entity and the consideration per common unit exceeds $10.00, continue to hold its preferred units; or (iv) require us to redeem its preferred units at a price of $9.218573 per preferred unit, plus accrued and unpaid distributions to the date of such redemption (which redemption may be paid, in the sole discretion of the general partner, in cash or in common units, in accordance with the terms of the Partnership Agreement Amendment)." (CEQP site)

There's also a conversion feature, which allows preferred unitholders to convert all or any portion of their preferred units to into common units, at the then applicable Conversion Ratio. The preferred units have the same voting rights as the common units.

{kind=link}

Preferred Dividends:

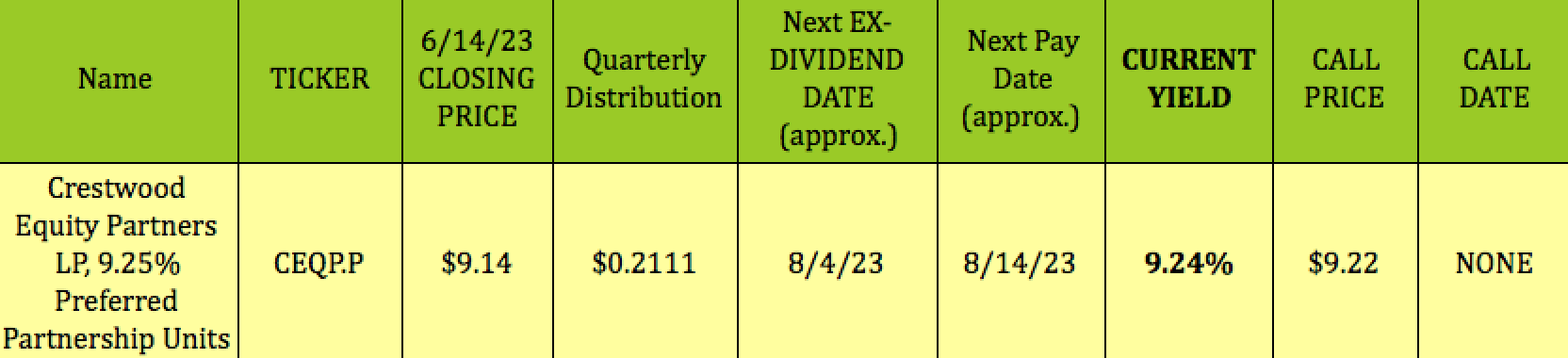

The Crestwood Equity Partners LP, 9.25% Preferred Partnership Units closed at $9.14 on June 14, 2023, giving them a 9.24% dividend yield.

The next ex-dividend date is ~8/4/23, with an ~8/14/23 pay date. There is no call date for these units, which eliminates the situation in which investors have their preferred shares redeemed, forcing them to find a new investment.

{kind=link}

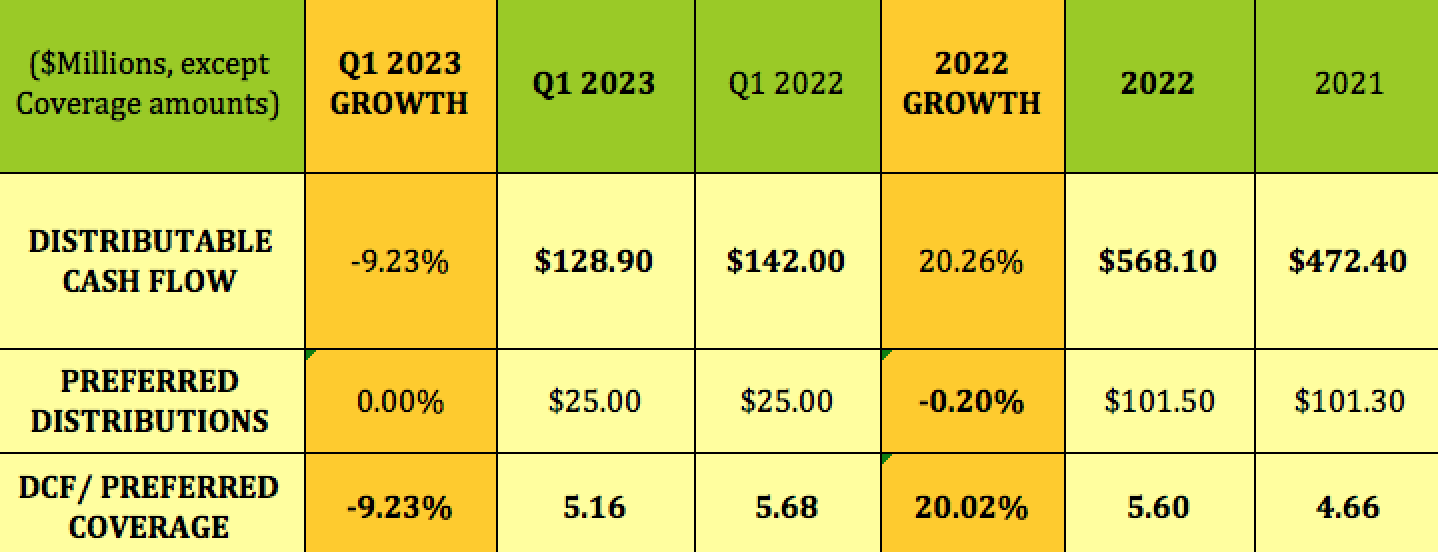

Using Distributable Cash Flow, or DCF, which accounts for taxes and Capex, these units had a 5.16X coverage factor in Q1 '23, down from 5.68X in Q1 '23, but still quite strong. Full year 2022 coverage rose to 5.60X, vs. 4.66X in 2021.

There are $15M/quarter in CEQP.P preferred distributions - the other $10M/quarter is paid to Niobrara, as part of Crestwood's acquisition of a 50% interest in Jackalope Gas Gathering Services LLC.

{kind=link}

Taxes:

Unitholders receive a K-1 report at tax time.

Earnings:

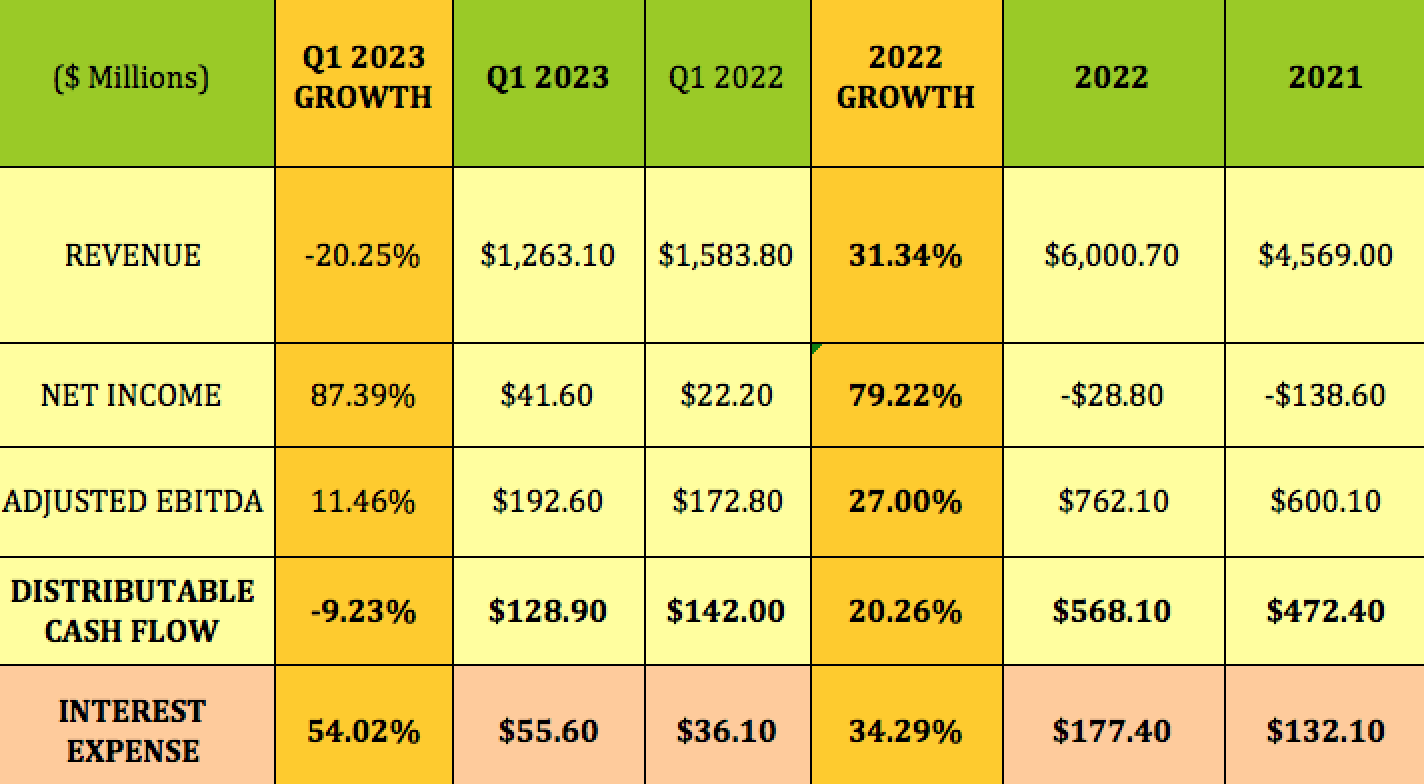

Q1 '23 revenues were down 20%, mainly due to lower revenues in the Storage & Logistics segment; while Adjusted EBITDA rose 11.5%, and DCF fell 9%. Net Income rose 87%, due to a larger asset base, in spite of 54% rise in Interest expense.

2022 was a good year for CEQP, with revenues up 31%, Net Income up 79%, EBITDA up 27%, and DCF up 20%, fueled by its the Oasis Midstream merger, which doubling CEQP's size in the Williston Basin.

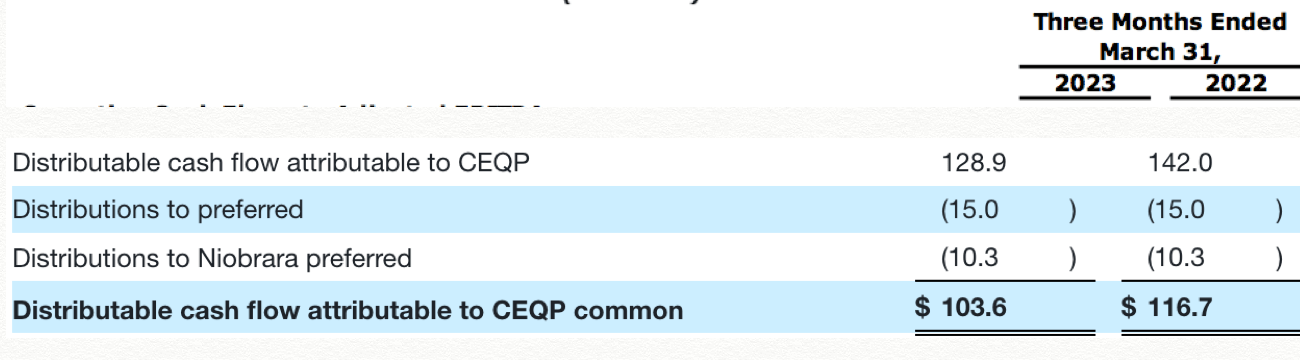

NOTE: The DCF amounts listed below are before preferred distributions to CEQP.P unit holders, and to Niobrara preferred unit holders.

The net amounts post-preferred payments were $103.6M in Q1 '23, and $116.7M in Q1 '22; and $466.6M and $377.1M in 2022 and 2021, respectively.

CEQP site Hidden Dividend Stocks Plus

{kind=link}

{kind=link}

Segments:

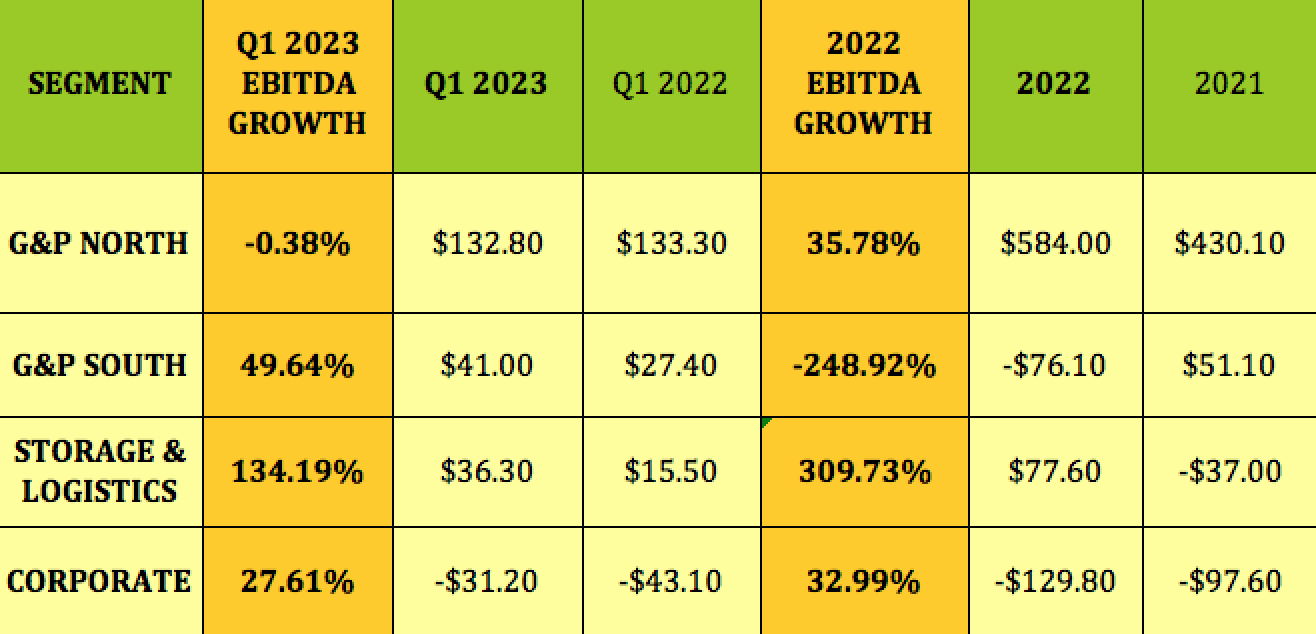

Digger deeper, Gathering % Processing North, CEQP's biggest segment, had flat EBITDA in Q1 '23, vs. a 36% jump in full year 2022. G&P South's EBITDA rose 49.6% in Q1 '23, after posting a loss in full year '22. Storage & Logistics' EBITDA rose 134% in Q1 '23, and 310% in 2022:

{kind=link}

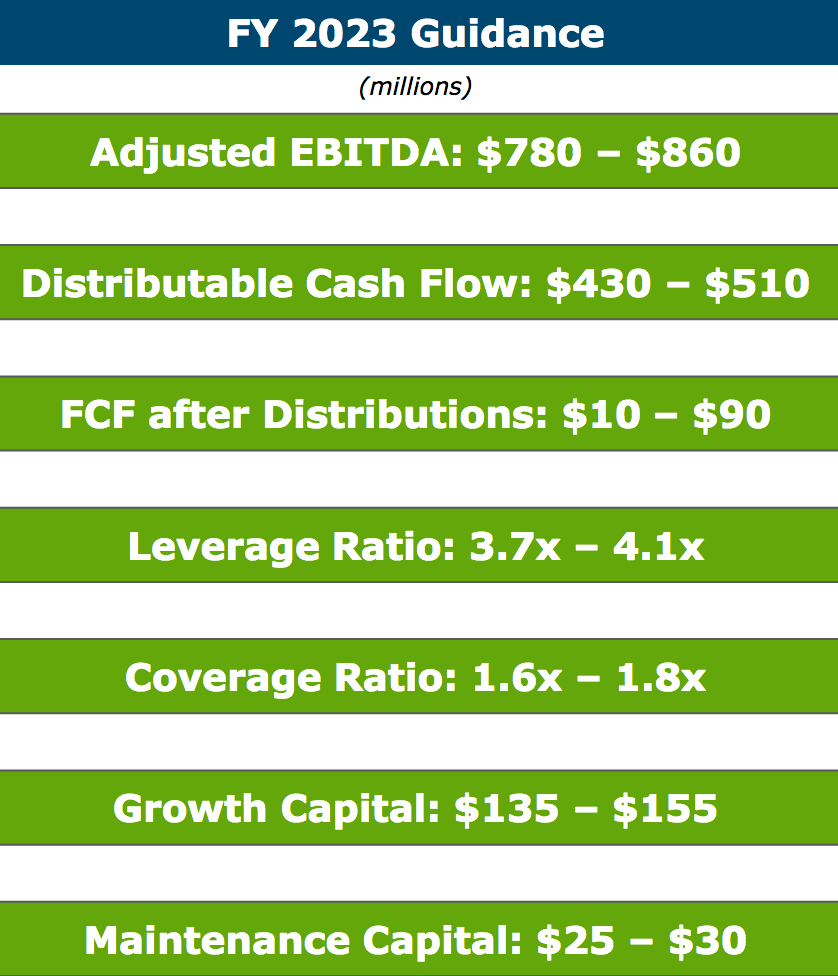

2023 Guidance:

Management gave midpoint Adjusted EBITDA guidance of $820M for 2023, up 7.6%; and midpoint DCF of $470M, up slightly vs. 2022. Free Cash Flow after Distributions will be in a wide range of $10 - $80M.

In April 2023, Crestwood and its JV partner Brookfield Infrastructure (BIP) closed the sale of their Tres Palacios Gas Storage facility for $335M. Management intends to use the proceeds to pay down more debt, and is targeting a 3.7 - 4.1X leverage ratio in 2023.

{kind=link}

2023 Capex:

Management estimates ~$135 - $140M in 2023 Capex in these asset areas:

Williston Basin: $75M-$85M for a build-out of three-product gathering systems at Rough Rider.

Delaware Basin: $50M-$60M for compression expansions in New Mexico and well connects across gathering systems.

Powder River Basin: Less than $5 MM for well connects.

CEQP site

Profitability & Leverage:

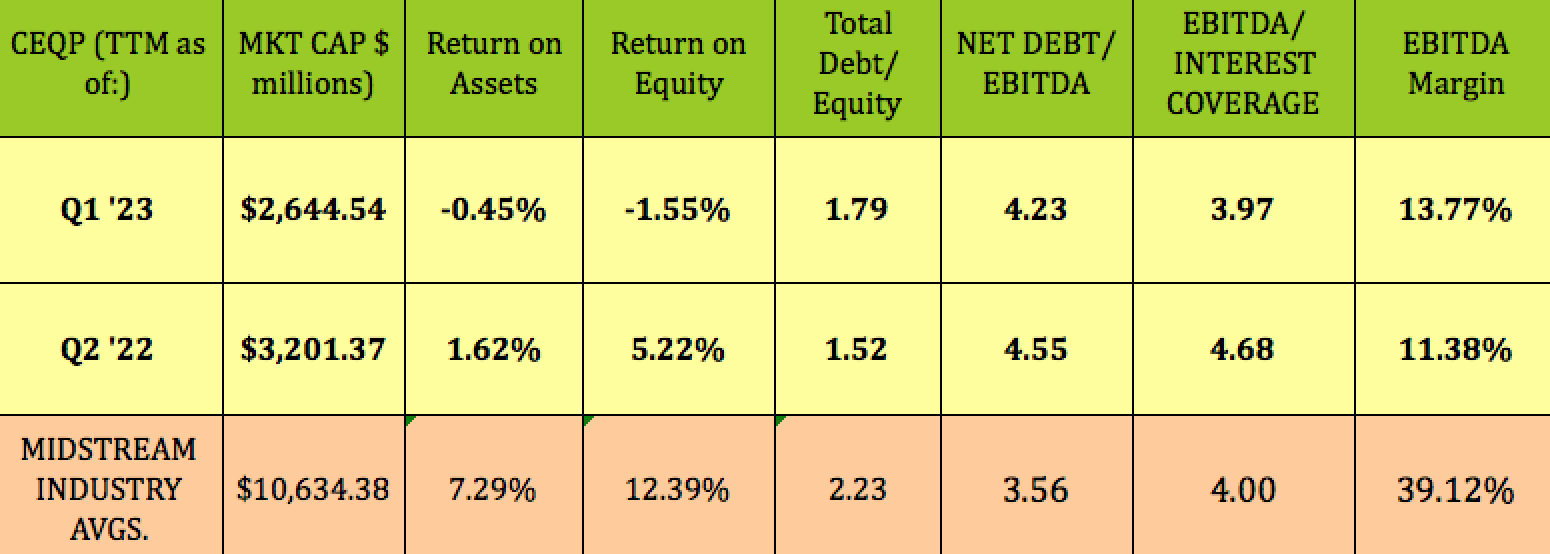

The negative net income in '22 pushed ROA and ROE into the red, but those metrics should improve in Q2 '23. Total Debt/Equity was up a bit in Q1 '23, while Net Debt/EBITDA improved to 4.23X. Interest coverage was lower, at 3.97X, but still in line with the industry average.

Management expects "significant free cash flow generation beginning in the second half of 2023, which will be allocated to debt paydown and leverage reduction." (CEQP site.)

{kind=link}

Debt & Liquidity:

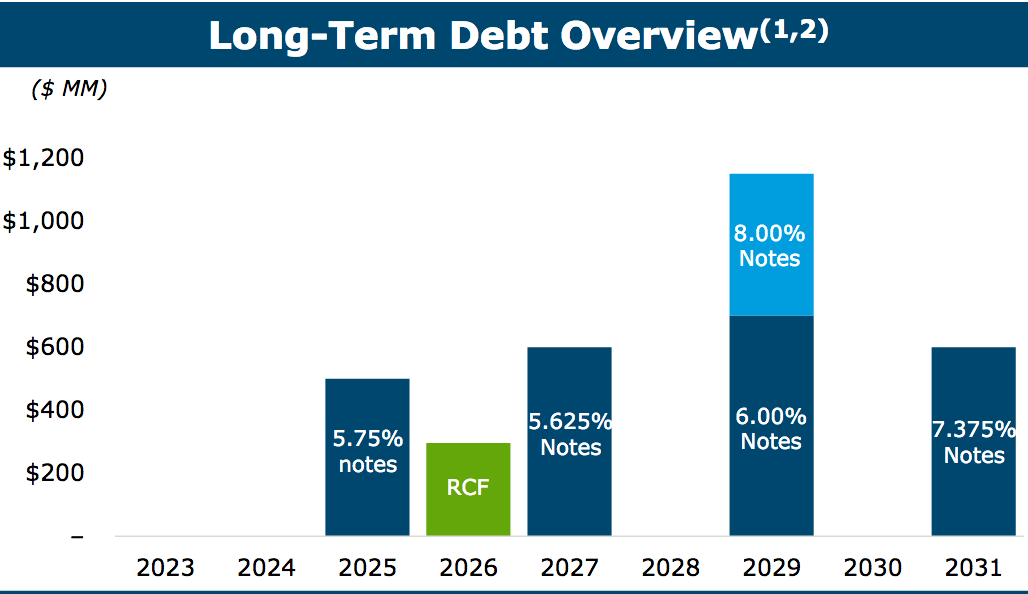

In January 2023, Crestwood Midstream Partners LP, a wholly owned subsidiary of Crestwood, issued $600M of 7.375% senior unsecured notes due 2031. Crestwood used the proceeds of the issuance to repay borrowings on the corporate revolving credit facility and to repay and terminate the Crestwood Permian Basin Holdings revolving credit facility.

As of March 31, 2023, Crestwood had $1.2 billion available capacity on its revolving credit facility, and a lower 4.2X Debt leverage ratio. CEQP has no debt maturities until 2025, when its 5.75% Notes come due.

{kind=link}

Parting Thoughts:

If you're looking for a solid high yield income vehicle, take a closer look at CEQP.P. We rate these preferred units a long-term BUY, based upon their strong preferred distribution coverage, Crestwood Equity Partners LP's continuing growth, and their stronger investor protections.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

For further details see:

Crestwood Equity Partners Preferreds: 9% Yield, Strong Investor Protection