CRCT - Cricut: Potential Is There But Significant Pain Is Ahead

2023-11-02 08:29:18 ET

Summary

- Cricut’s revenue has grown impressively at a +22% rate, while EBITDA has lagged behind at +15%. The business has executed a strong go-to-market strategy, underpinned by a compelling suite of.

- Management has done a fantastic job of monetizing its product offering, launching a Subscription service that has positive uptake. Although we are skeptical of its long-term story, its ecosystem will.

- Cricut is experiencing a significant decline in revenue due to macroeconomic conditions, with the discretionary nature of its products weighing heavily. We expect continued pain.

- Cricut is facing numerous material risks. Its margin development has been underwhelming, its FCF generation is volatile, and its growth rate in the medium-term is uncertain as interest in its products wane currently.

- Cricut’s valuation implies further downside in our view, given the share price decline has not deviated sufficiently from its decline in profitability.

Investment thesis

Our current investment thesis is:

- Cricut's business model is quite compelling, underpinned by a fantastic range of products. Having built a ringfenced eco-system that is sufficiently filled with value for consumers, the business is capturing a large share of the growing interest in the technology-driven arts and crafts segment. From this, we believe Cricut is positioned to achieve long-term success, although it is difficult to assess how this will materialize financially.

- With Cricut facing near-term headwinds and operating a highly discretionary set of products, we see pain ahead. This will only worsen the uncertainty associated with this company, making it incredibly difficult to assess the normalized long-term trajectory of this company.

Company description

Cricut, Inc. (CRCT) is a pioneering technology company in the creative arts industry. Its innovative products, including smart cutting machines and design software, empower millions of users globally to create personalized and professional-quality crafts. With a user-friendly approach, Cricut has become a household name among DIY enthusiasts, artists, and small businesses alike.

Share price

Cricut's share price has collapsed in recent quarters, with a ~50% decline since 2021. This is partially a reflection of the wider market, which has struggled to remain positive during this period. This said, Cricut has also struggled financially, compounding its negative fortunes.

Financial analysis

Cricut financials (Capital IQ)

Presented above are Cricut's financial results.

Revenue & Commercial Factors

Cricut's revenue has grown well during the last 5 years, with a CAGR of +22% into the LTM period. EBITDA has lagged behind, with a CAGR of +15%.

Business Model

{kind=link}

Cricut designs cutting machines equipped with advanced technology. These machines can cut a variety of materials, from paper and fabric to leather and wood. Its focus on developing cutting-edge, user-friendly technology has set it apart in the crafting industry and allowed for a market-leading position within this new segment of the arts and crafts market.

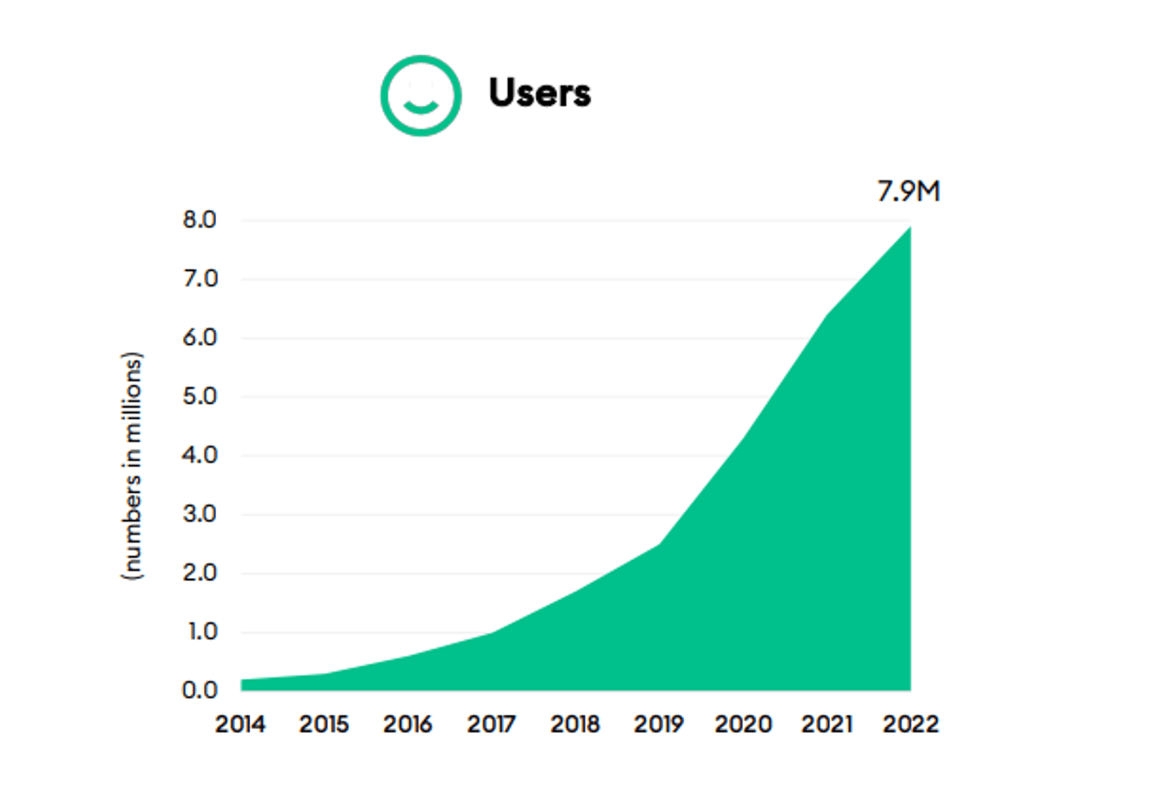

Cricut offers a subscription-based service called Cricut Access, where users pay a monthly fee for access to a vast library of images, fonts, and projects. The successful implementation of this subscription model has been impressive, allowing for consistent revenue. Of the company's >8m users, ~3m are paid subscribers.

{kind=link}

Cricut provides an ecosystem that includes not only cutting machines but also design software (Cricut Design Space), a cloud-based offering, AI capabilities, and a wide range of materials and accessories. We are extremely impressed by Management's ability to take what is an innovative manufacturing business and upscale it to be far more lucrative. Unlike many businesses, we do not see this as faux services but as a genuine value-add for consumers. This is illustrated in its strong subscription growth, with this representing ~70% of GP.

{kind=link}

The active and supportive community around Cricut has strongly fostered brand loyalty and increased usage of its product. Users share their creations, tips, and ideas, creating a positive cycle where existing users inspire and welcome new ones. This is critical to its "proof of concept" to society as a whole. We genuinely believe this is working, evidenced by ~40%of new users heard of Cricut through friends and family.

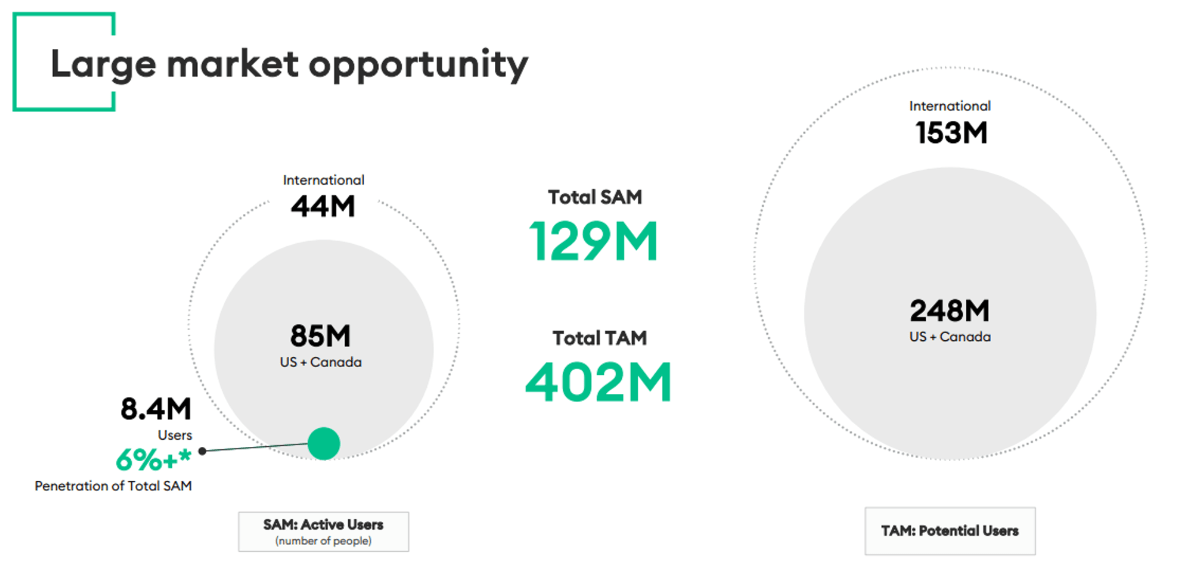

Management estimates its total international SAM to be 44m users and its TAM to be 153m, suggesting a significant runway for long-term growth. We believe these are fairly optimistic but possible. It is heavily predicated on investing in new technologies and improving the quality and depth of its output. In conjunction with this, it is critical that society continues to learn of its products and the value offered.

{kind=link}

Margins

{kind=link}

Cricut's margins, outside of the post-pandemic bump, have experienced margin erosion as it has scaled. We attribute this to an aggressive customer-acquisition strategy post-IPO, as Management seeks to maintain its growth momentum to scale the business. GPM has increased 7ppts since FY18 from the benefits of economies of scale while S&A spending as a % of revenue has increased by 10ppts, illustrating this.

We suspect the business will continue to face downward margin pressures as macroeconomic conditions weigh heavy, resulting in greater discounting. Offsetting this will be further growth in subscription revenue, for which the marginal cost is low.

Quarterly results

Cricut's recent performance has materially declined relative to its prior trajectory. Its top-line revenue growth was (31.9)%, (27.6)%, (26.0)%, and (3.3)% in its last four quarters, which is part of a broader period of 6 successive quarters of decline. In conjunction with this, margins have declined, although we do see stabilization in its last two quarters.

The slowdown experienced is a reflection of the wider macroeconomic environment in our view. With heightened inflation and interest rates, consumers are experiencing soaring living costs, which wage inflation is barely offsetting. As a result of this, consumers are reducing discretionary purchases as they move defensive with finances. Cricut's products are highly discretionary in nature and are more expensive than other creative products. This does not position the business well.

Looking ahead, we expect conditions to worsen before improving, with a significant degree of evidence to suggest a difficult quarter or two ahead. There is renewed uncertainty in the market, with a particular focus on whether consumers can truly withstand the pressures of the current conditions. The only positive for investors is that following such a substantial decline in recent quarters, the business is likely nearing its "bottom".

Key takeaways from its most recent quarter are:

- Despite the decline in revenue growth, its subscriptions revenue and machines revenue streams both remained positive, up 13% and 5% respectively.

- Further, international growth was positive, with 34% YoY growth as the business continued its marketing push overseas following the consolidation of its trajectory in the US.

- The company successfully launched Cricut Venture, the largest and fastest connected cutting machine on the Cricut Platform.

Balance sheet & Cash Flows

Cricut is conservatively financed, with a negative net debt balance. This has been facilitated by its cash-generative business model, with an impressive FCF conversion. This said, we note that FCFs have been fairly volatile, contributing to significant uncertainty as to their normalized level.

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a significant decline in its growth rate, with a CAGR of +5% into FY24F. In conjunction with this, margins are expected to sequentially improve.

We broadly consider these assumptions reasonable. Economic pressures are not subsiding and the knock-on effect will likely last into FY25 and potentially FY26, contributing to difficulty in achieving double-digit growth at its current scale.

Further, margin improvement is likely to be driven by a transition to higher-value products and subscription sales, with analysts expecting this to offset any weakness that will come from slower growth.

Industry analysis

Household Appliances Stocks (Seeking Alpha)

{kind=link}

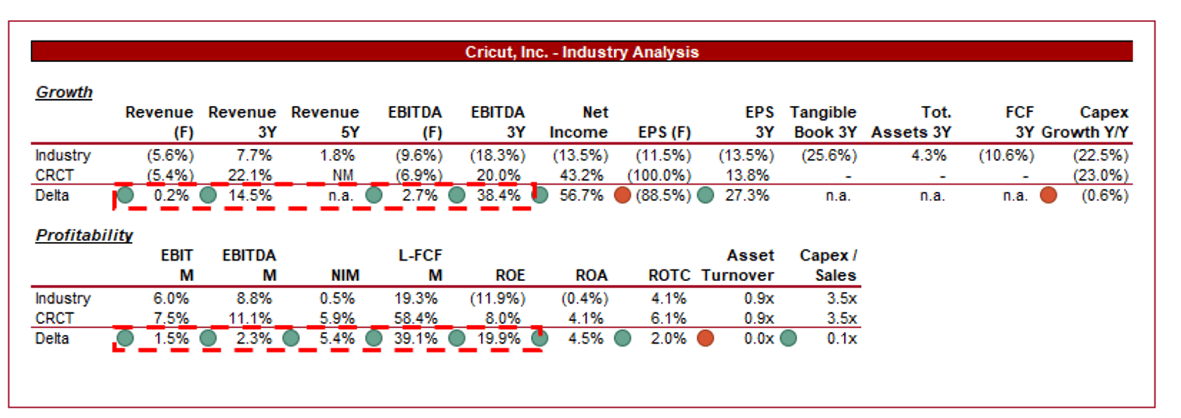

Presented above is a comparison of Cricut's growth and profitability to the average of its industry, as defined by Seeking Alpha (4 companies).

Cricut performs well relative to its peers, with superior growth and margins. The company's growth is a reflection of its innovative product and exploitation of a gap in the market, allowing for rapid scale. The margin strength is attributable to Management's ability to pivot its business model to maximize returns through monetizing its customer base.

Valuation

{kind=link}

Cricut is currently trading at 16x LTM EBITDA and 13x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, owing to the company's derailed growth story, with significant uncertainty as to how this will return. Further, margin improvement has not been consistent, further increasing the risk of where it will normalize.

Further, Cricut is trading at a premium to its peer group, which is reasonable as it reflects the company's superior financial performance thus far. This said, we are unconvinced by a significant premium, again due to the uncertain outlook and whether this outperformance is unsustainable.

Our view is that Cricut is likely overvalued currently. There is material uncertainty as to the future outlook and development of the company, with the risk that the current macroeconomic environment restricts the ability to capture new customers as interest softens.

Its highly discretionary nature is limiting to any near-term upside.

Valuation evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Strong growth in the international user base

- Successful product diversification

- Strategic partnerships with leading brands.

Final thoughts

Cricut is a fantastic case study on innovation. The company's products are quite impressive and Management's ability to develop its business model is equally so. We do not think this is a company that will disappear or fade to irrelevance but does face an uphill battle to justify bullish financial development.

We struggle to see what its medium-term revenue growth rate will be, where its margins can normalize, or where its FCF conversion should be. The company is incredibly volatile and still being weighed down by its discretionary nature.

With the near-term appearing difficult and its valuation not materially declining relative to recent quarters, we see more downside ahead.

For further details see:

Cricut: Potential Is There But Significant Pain Is Ahead