CCRN - Cross Country Healthcare: Is It Creating Shareholder Value Or Not?

2023-11-27 21:10:17 ET

Summary

- Cross Country Healthcare's stock performance suggests investors expect a challenging period for the company.

- Long-term tailwinds include high capital turnover, compounding earnings, compressed valuations, and technical support.

- The rate at which CCRN compounds earnings on investor equity is a standout in the investment debate, supporting value creation even without growth.

Investment Brief

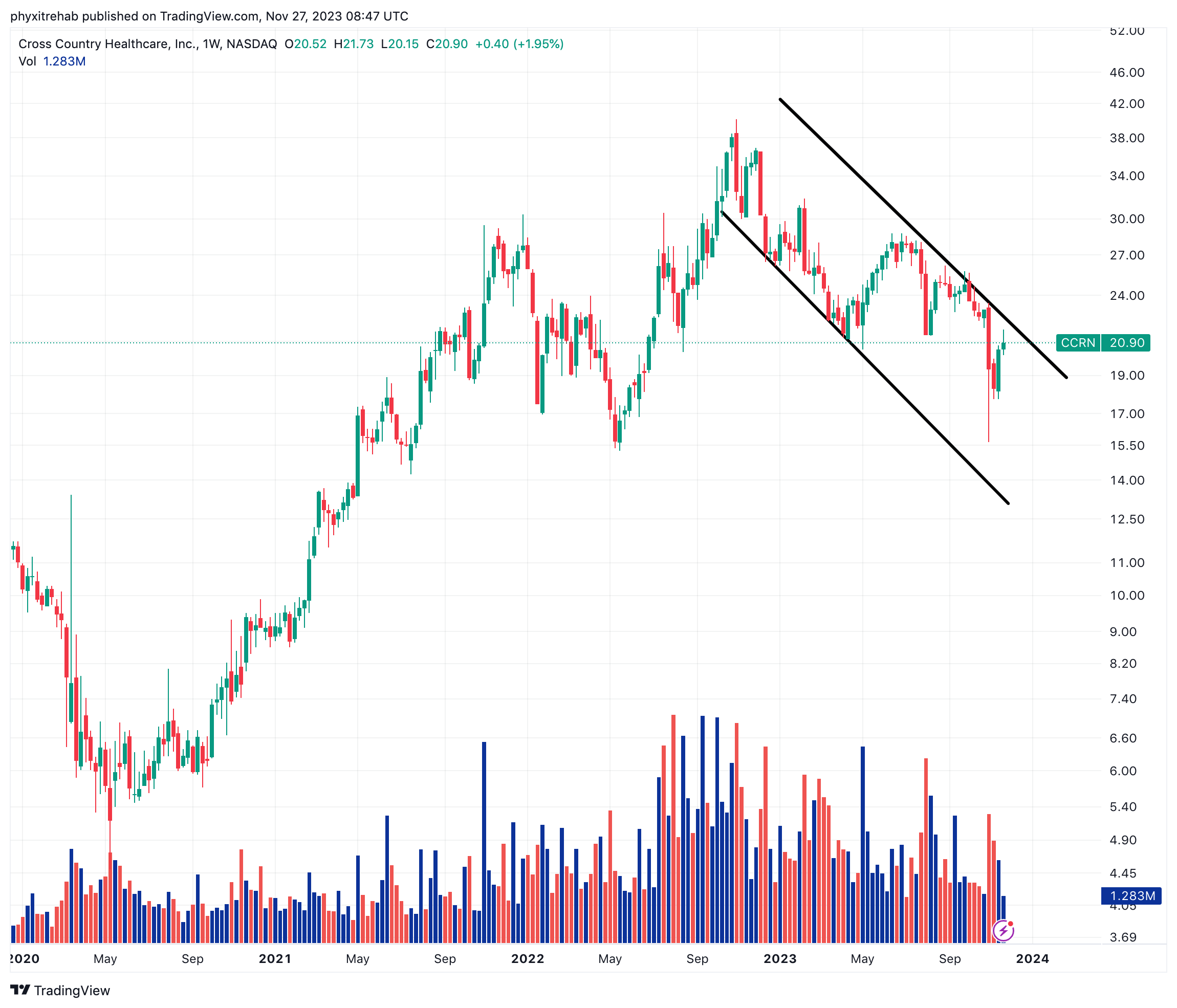

The H2 FY'23 market performance of Cross Country Healthcare, Inc.'s ( CCRN ) common stock suggests investors expect a period of more challenging business for the company in 2024–'25 (Figure 1).

My last CCRN analysis revealed numerous long-term tailwinds. One, CCRN is rotating back $0.90 in gross profit per $1 of assets employed on the balance sheet. Two, it is compounding post-tax earnings at a rate of 25–30% relative to capital required to run the business. Three, valuations were (and still are) compressed below 10x earnings and 2x book value. Four, there was building technical support at the time.

Since that publication, the stock is down a further 20%, leading to a much-needed reappraisal of the thesis. In that vein, the critical issues that need tackling include the following:

- Growth rate— sales + earnings, 1 to 3 years out, inc. recent history,

- Business returns— capital intensity, profits relative to capital required to run,

- Shareholder returns— Rate of earnings relative to shareholder equity, growth relative to ROE, FCF per share,

- Valuations— Based on cash flow, earnings power + asset factors.

The central theme is to know precisely what we're paying and precisely what we're getting for it. Based on an objective view of the facts, my estimation there is potential for CCRN to unlock risk capital for investors holding longer than 12–18 months. This report will dissect the investment reasoning. Net-net, I reiterate CCRN as a buy for the reasons outlined here.

Figure 1.

{kind=link}

Figure 2.

{kind=link}

Critical investment facts supporting buy thesis

1. Growth outlook (1–3 years)

Being CCRN is such a high capital turnover business (discussed later), the market looks to sales as much as earnings in valuing the company.

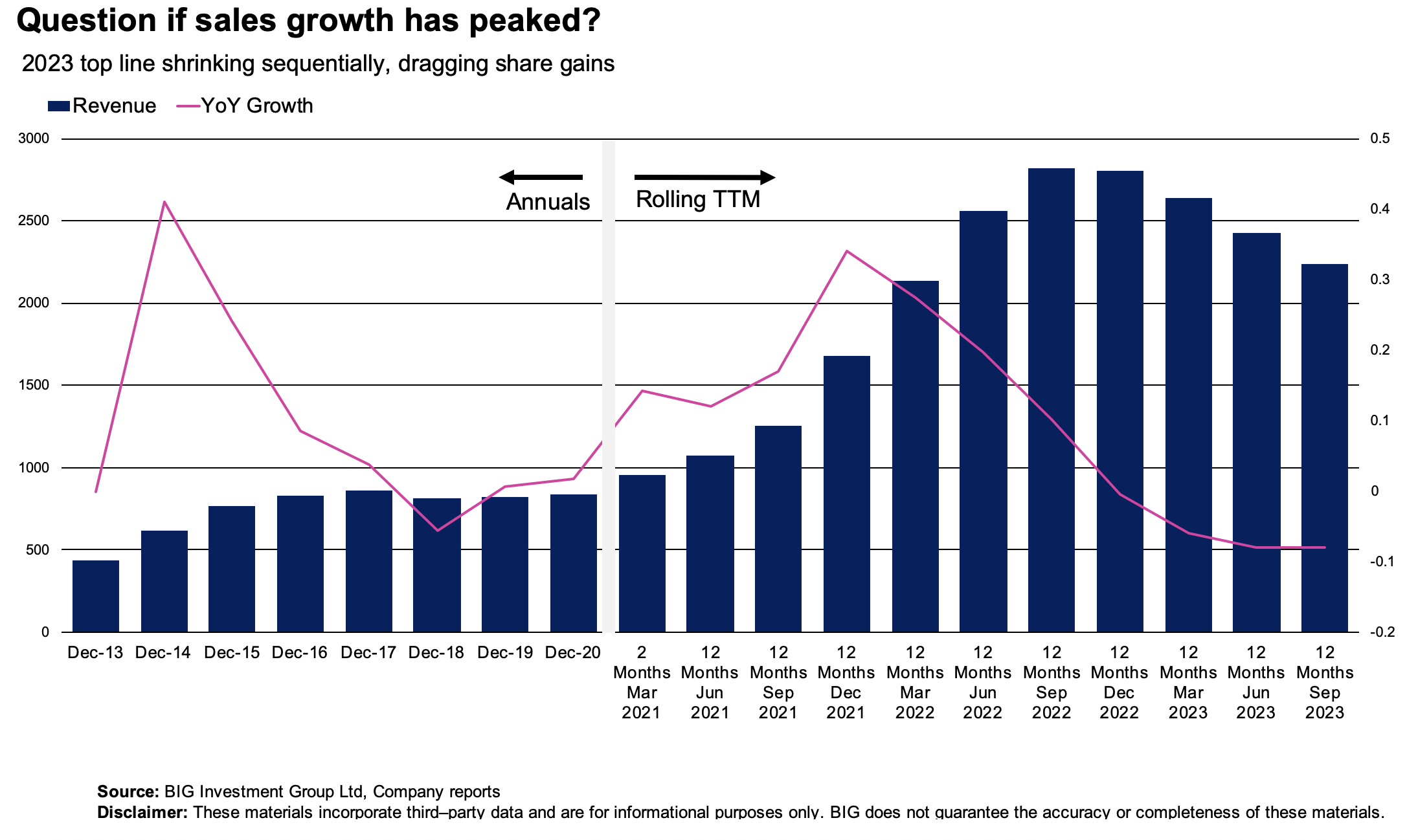

The firm posted quarterly numbers earlier this month. It put up Q3 revenues of $442.3mm, down 30% YoY, and a 18% sequential decline. This continues a trend seen firmly in place across 2023 (Figure 3). The question is, have sales peaked for CCRN for now? I am not so sure. As to the segments:

- Nurse and Allied Staffing ("NAS")—

Revenues booked were $396.6mm, down by 35% YoY and 20% sequentially. Contribution income decreased to $39.2mm from $77.8mm YoY last year, mirroring the revenue clip.

Drivers to the revenue downside include— (i) Average field contract personnel on an FTE basis were 9,849; this is down from 12,524 YoY and 11,385 sequentially, and (ii) revenue per full-time equivalent ("FTE") per day was $434 compared to $526 YoY and $474 sequentially.

- Physician Staffing ("PS")—

The PS segment did $45.7mm of business, growing 92% YoY. Excluding all acquisition impacts, revenues were up 21%. Contribution income rose to $2.6mm from $0.8mm YoY. Unlike in NAS, total days filled were 23,004, up 74% YoY from 13,219 YoY. Finally, revenue per day filled was $1,986, compared to $1,803 YoY, driven by higher volumes.

Figure 3.

{kind=link}

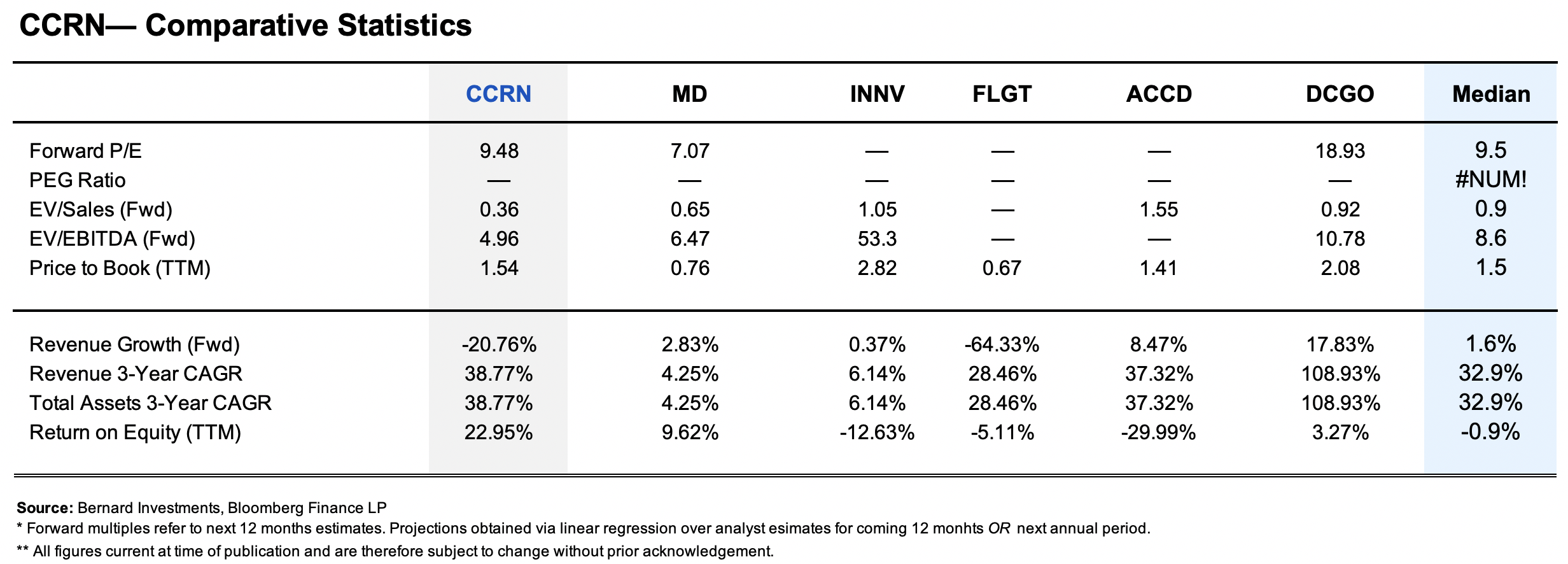

Consensus estimates project a softer period of business for CCRN going forward. Sales are forecast to decrease 19% in 2024 and earnings 30% in the same year. Management on the other hand is constructive , looking to FY'23 adj. EBITDA of nearly $150mm. It did mention, however, it "will continue to balance investments with cost savings to preserve profitability while ensuring we maintain sufficient capacity to fuel long-term growth ".

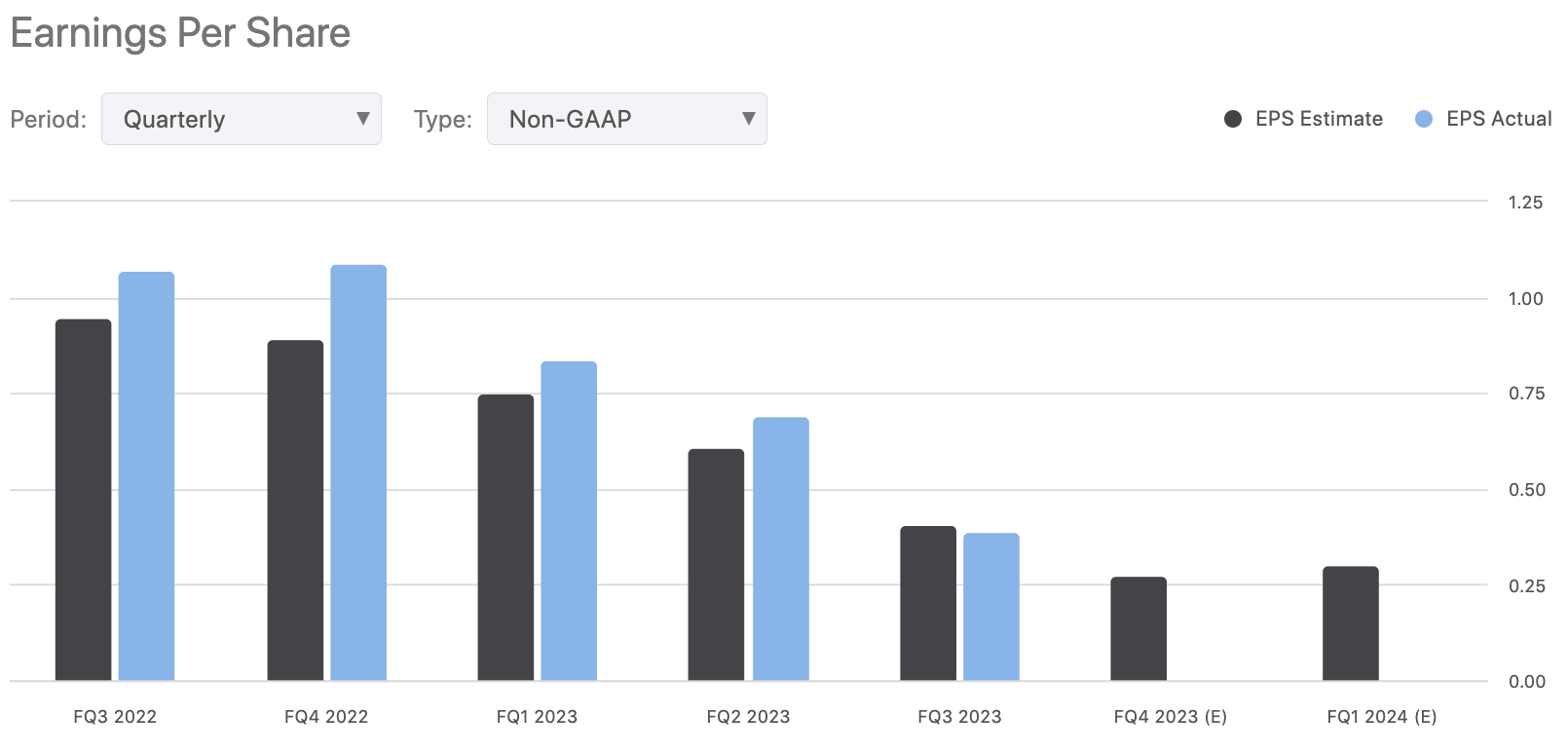

You can see the consensus projections below. The recent earnings trend is down as you can plainly see. As for the outlook 1–3 years from now, this weakens the case severely in my view. Stock returns over this duration are highly sensitive to sales + earnings growth. With the numbers tightening up, will the capital appreciation too? If this continues, it is very difficult to foresee a large re-rating 1–3 years out. CCRN is a firm that has terrific economics, that balance this debate (below).

Figure 4.

{kind=link}

2. Economics of shareholder value

CCRN is historically a highly profitable enterprise that makes good use of business capital and compounds shareholder equity. What is attractive in the debate, is (i) the rate of earnings relative to shareholder equity, and (ii) growth relative to ROE and FCF per share.

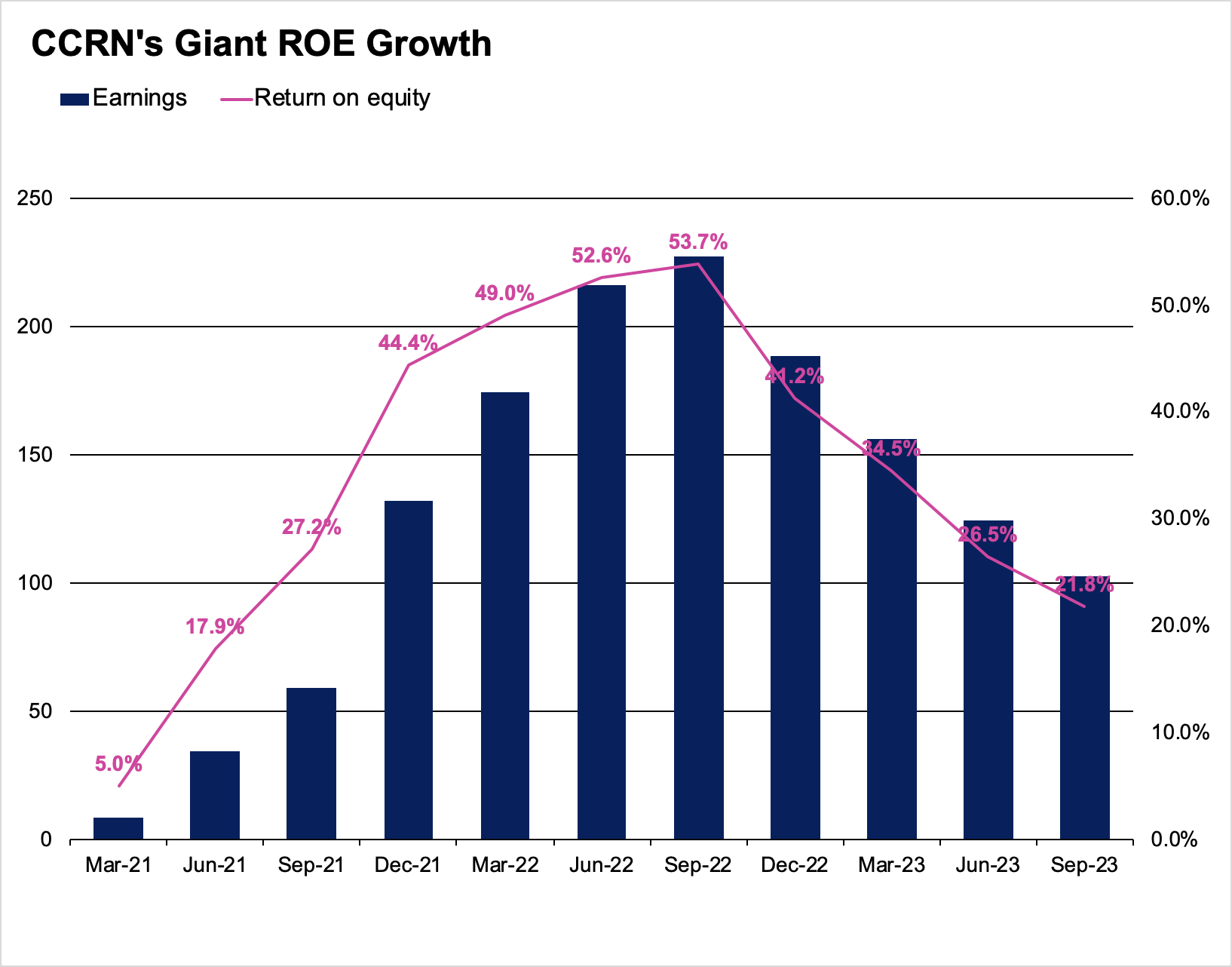

From 2021, the company's gargantuan earnings growth was well supported by the rate at which it compounded returns on equity capital (Figure 5). After Q3 earnings, the return on equity summoned to 23% in the TTM, rolling off highs of ~53% a year ago, but in multiples of the 5% in 2021.

Figure 5.

{kind=link}

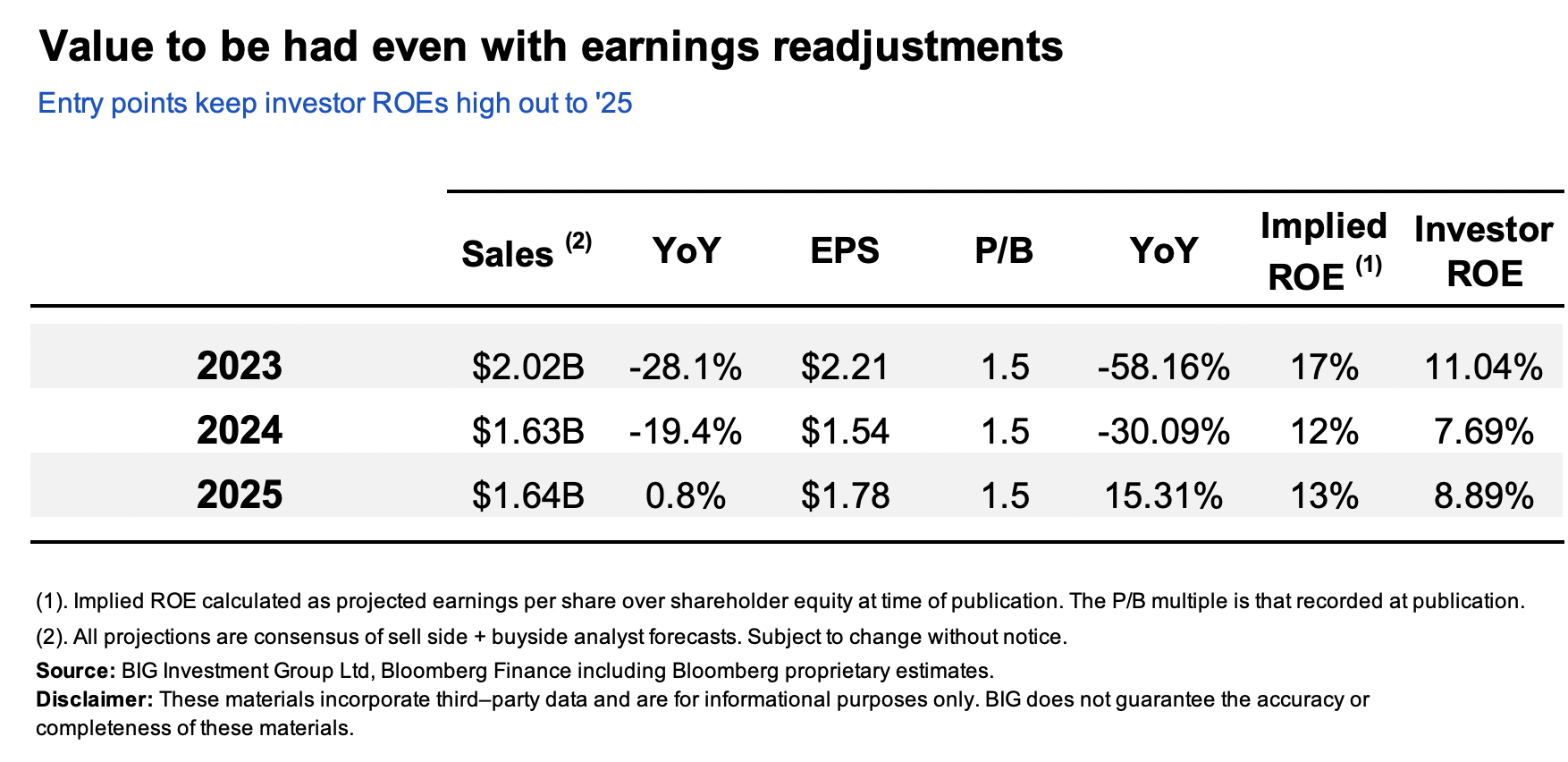

The questions are what is on offer, and for what price. Linear regression on analyst estimates fits 58% earnings decline in 2023 and 30% in 2024, before a growth recovery in '25 (Figure 6).

Again, further context is needed on growth vs. shareholder equity:

- Despite the pullbacks, at today's book value per share, CCRN would still produce 17% return on shareholder equity this year, 12% the next.

- The company is also priced at 1.5x book value (1.5 x 470 = ~730). The investors' ROE of 17% is therefore 11% if paying this multiple ($102.4/730 = 11%).

The critical fact is you are paying a fair price for the company's net assets and receiving a high rate of return for today's price. Moreover, despite the pullback in growth, CCRN looks set to still create value for its shareholders.

Figure 6.

{kind=link}

The company produces a similar rate of return from profits on its business capital. This too has doubled from 12% in 2020 to 24% in the last 12 months, producing $3.30 in NOPAT/share. The high rate of business returns—similar to that of shareholder equity—makes the earnings economically valuable. Here, we have considered anything above a 12% ROIC to add economic value, which came to $58mm or 2.6% of sales last period. The drivers of such exceptional returns are:

(1). Capital turnover of >4.5x,

(2). Single-digit margins (Figure 7),

(3). Positive returns on new capital deployed

CCRN's capital intensity is balanced, and the ratio of sales to capital invested is tremendously high, indicating its efficiency. Again these are bullish features.

Figure 7.

{kind=link}

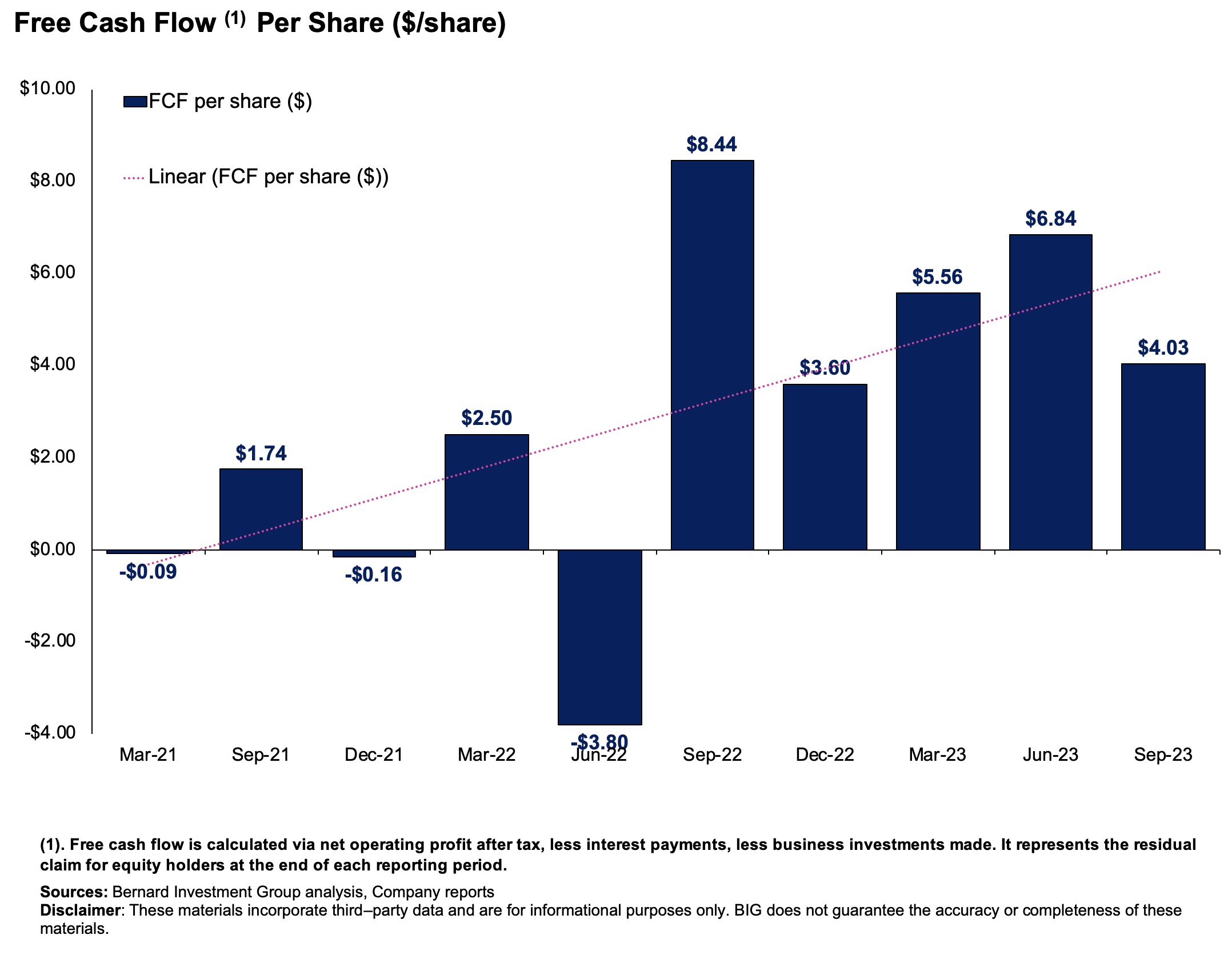

The final piece of the puzzle is the cash CCRN is throwing off for its shareholders. Such exemplary returns on shareholder equity and business capital support CCRN in producing plenty of cash moving forward:

- The profits earned on capital/equity ensure these are reinvested at rates that don't jeopardise FCF to shareholders (vice versa).

- It has thrown off $28.6/share in FCF to its owners since 2021, whereas its share price has levelled just $8.00 higher (after consolidation)—potential value gap. Picture a similar scenario moving forward, which isn't unlikely in my opinion, a tidy value proposition.

The point is that a company spinning away so much cash is being heavily punished at 1.5x book value and 9.5x earnings, and a 33% cash flow yield. There is scope for a reversal in these multiples, with the catalyst fundamentally based.

Figure 8.

{kind=link}

Valuation and conclusion

The stock sells at 9.5x forward earnings, 1.5x book value, and a 33% cash flow yield as mentioned earlier. Therein lies the critical issue once again— what do we get for what we pay.

This is summarized by the following data points:

(i). For 1.5x book value, you get a 22% trailing ROE, potential 17% fwd ROE,

(ii). Paying 9.5x earnings buys you a company producing >20% rate of earnings on the capital required to run,

(iii). Both get you a company spinning off $4–$6 in FCF per share fairly convincingly, a 20% FCF yield.

At the price of 9.5x earnings and the est. ROE of 17%, my judgement is the firm is worth $1.138Bn (9.5 x (102 x 1.17) = 1,138) or 55% upside potential as I write.

This is a company normalizing earnings growth but still doing high rates of business on its equity capital + business capital. Such firms can continue producing FCF to either reinvest or return to shareholders. The data says that it can unlock value given the right flock of buyers.

In summary, my rating on CCRN remains a buy. There is too much objective value to be overlooked in this name, which boils back to 1) Return on investor equity, 2) FCF per share, 3) compounding intrinsic value. My judgement is the company can trade fairly at a market value of $1.14Bn or $32 per share. Net-net, reiterate contrarian buy.

Key risks to the thesis include:

- Further selloff of 20% below price at publication would hinder upsides,

- CCRN produces weaker than expected ROE in 2023, reducing the profit factor,

- Sales + earnings growth completely disappoint, worse than what's baked in,

- Continued macro pressures cannot be ignored.

Investors must recognize these risks in full before proceeding further.

For further details see:

Cross Country Healthcare: Is It Creating Shareholder Value Or Not?