CYRX - Cryoport: Great Potential That Management Continues To Fail To Actualize

2023-10-03 09:39:55 ET

Summary

- Cryoport has experienced a decline in revenue and worsening bottom line results over the past year.

- The company's stock has fallen 30.6% since May and 64.2% since July 2022.

- Despite potential in the life sciences market, Cryoport needs to show progress in sales growth or bottom line improvements to be taken seriously.

I don't believe that I have ever found a company that I have wanted to see fail. In an ideal world, every company would be a tremendous success. But sadly, that's not how the world works. Some firms, perhaps the most firms, will eventually fail. Although it hasn't failed yet, one company that has done quite poorly over the past year or so is Cryoport ( CYRX ), an enterprise that offers specialized supply chain solutions for companies in the life sciences space. Examples of their work include controlled temperature storage, specialized packaging, product labeling, regulatory services, drug return handling and destruction services, and more.

I have been bearish on the business for well over a year now. But when I first became bearish, I never thought that the picture would get this bad. Although revenue has been mixed, profits and cash flows look largely worse year over year. And even if the company were to stabilize at the levels of profitability and experienced in 2022, shares would look very pricey. So even though the stock has fallen mightily over the past year or so, I would still argue that further downside is likely on the table.

A rough time

The most recent article that I published about Cryoport came out at the end of May of this year. At that time, I lauded the company for its ability to continue growing its top line. However, its bottom line results were worsening and showing no signs of stopping. Shares also looked pricey under the scenario that the company wouldn't see any material improvement on its bottom line for the foreseeable future.

At the end of the day, this led me to conclude that the decline for the company's share price was not over yet. And that gave me the push I needed to reiterate the 'sell' rating I had on the stock. Since then, shares have continued to fall. In fact, they are down 30.6% since the time that article was published. That's at a time when the S&P 500 is up 1.5%. And since I first rated the company a 'sell' back in July of last year, shares are down a whopping 64.2% while the S&P 500 is up 4.3%.

{kind=link}

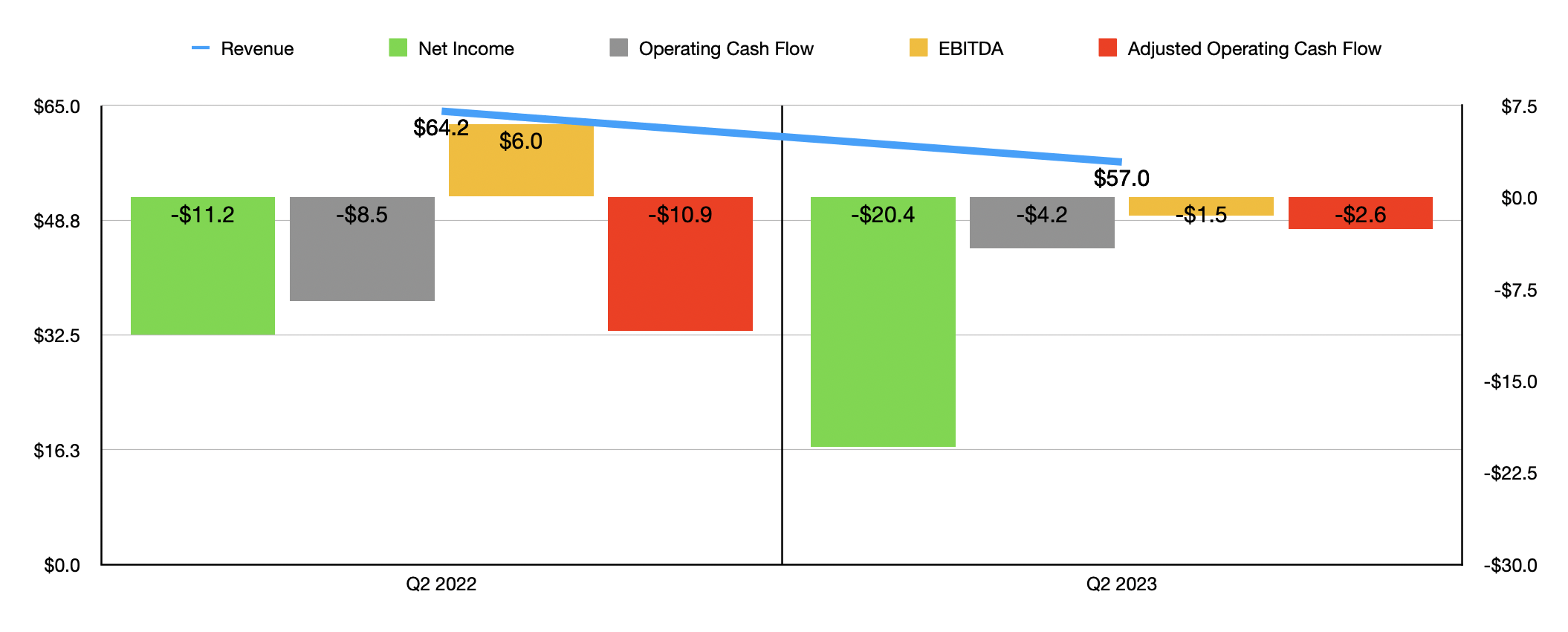

Only one additional quarter worth of data has come out since the publication of my last article. So it might be a wise idea to focus on that quarter for the purpose of this article. During that time, revenue for the company actually fell , dropping from $64.2 million to $57 million. That's a year-over-year decline of 11.2%. Service revenue for the company actually inched up 1.8% from $34.6 million to $35.2 million during this window of time. And that was thanks to growth in bioservices and revenue from the support of commercial cell and gene therapies. The weakness, then, came from a 26.2% plunge in product revenue from $29.6 million to $21.8 million. This, management said, was due to a reduction in demand for cryogenic systems, largely in China.

On the bottom line, the picture worsened as well. Net income dropped from negative $11.2 million to negative $20.4 million. The decline in revenue was partially responsible for this. However, the company also suffered from a 27% surge in selling, general, and administrative costs, and a 21.1% increase in engineering and development costs. I consider the latter to be an investment in the company's future. So I would encourage investors not to be too harsh on that. The increase in selling, general, and administrative costs, meanwhile, ended up stemming from investments that the company was making in order to more appropriately scale the business and meet future demand for its offerings. Integration and acquisition costs, for instance, grew by $3.8 million year over year, mostly because management has been actively exploring a strategic business opportunity that has not been revealed to shareholders publicly.

{kind=link}

Other profitability metrics have been rather mixed. For instance, it is true that operating cash flow improved from negative $8.5 million to negative $4.2 million. On top of this, if we adjust for changes in working capital, we get an improvement from negative $10.9 million to negative $2.6 million. On the other hand, EBITDA for the company worsened from $6 million to negative $1.5 million.

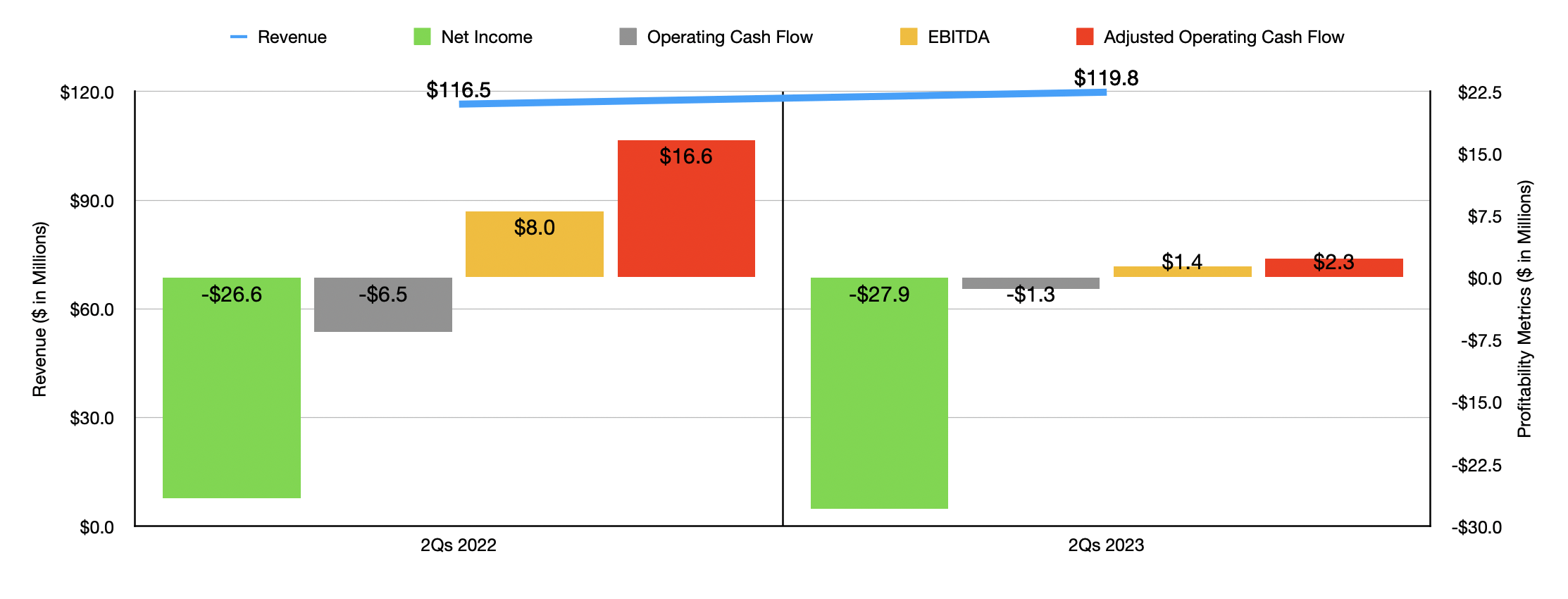

As you can see in the chart above, the first half of this year was not great. Despite the weakness in revenue in the second quarter, revenue for the first half of the year as a whole is still up. However, net profits, adjusted operating cash flow, and EBITDA have all worsened year over year.

This is not to say that everything about the company is bad. Most of its debt is convertible. But even if we factor it in as debt instead of the stock it can become, the company still enjoys cash in excess of that debt totaling $96.7 million. This creates a tremendous amount of runway for the enterprise at this time. The company also benefits from playing in a market that should do well in the long run.

I recently wrote an article about a REIT called Alexandria Real Estate Equities ( ARE ) that focuses on owning and leasing out real estate to life sciences companies and other similar firms. In that article, I talked about how the industry for life sciences is growing rapidly. Considering that the global market is $2.83 trillion already, the growth that should come on in future years will likely prove bullish for companies like Cryoport.

{kind=link}

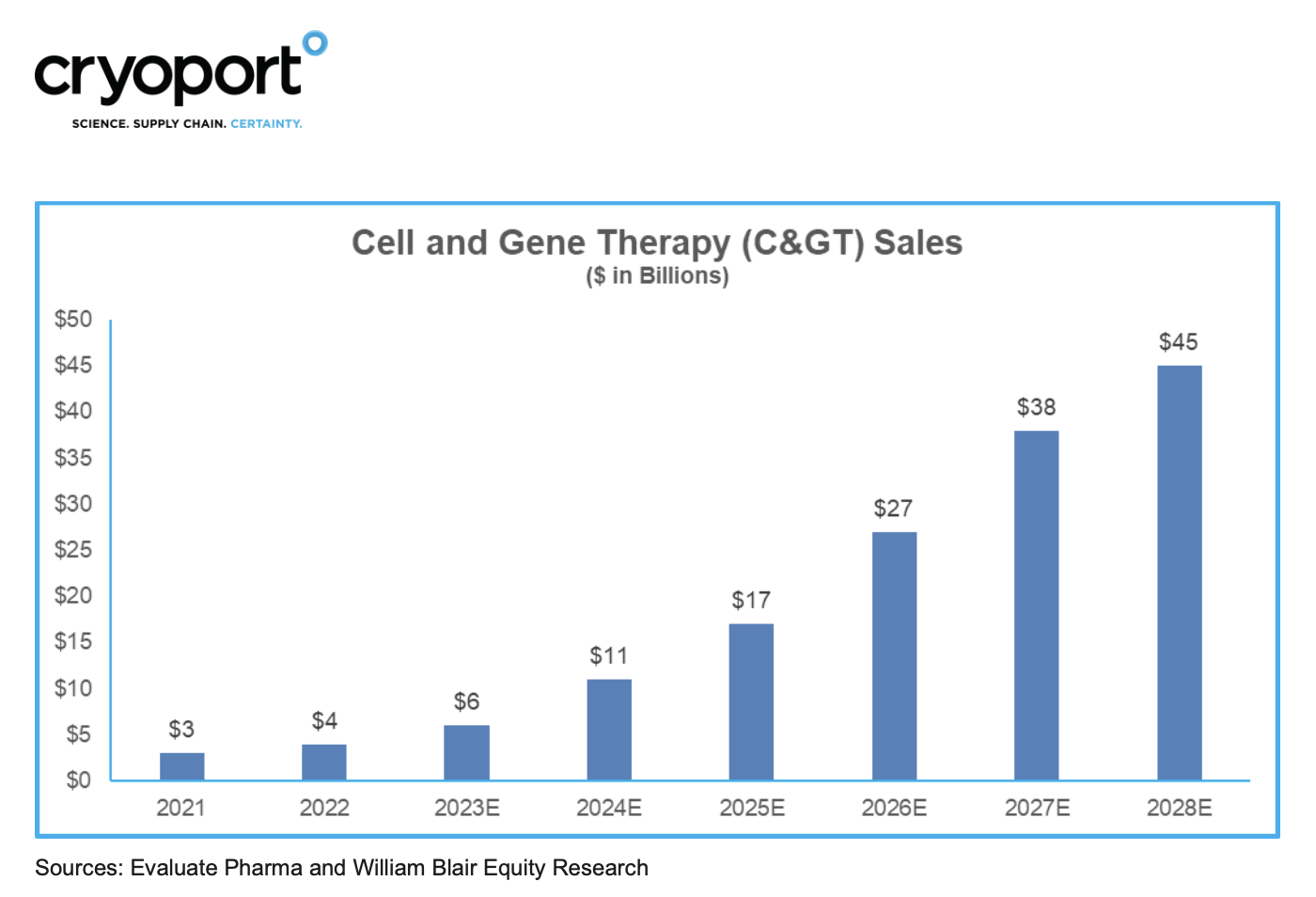

The management team at Cryoport has its own assessment of different market opportunities. For instance, they benefit tremendously from the expansion of the cell and gene therapy market. This year, that market is estimated to be worth $6 billion. It's expected to nearly double to $11 billion in next year before eventually climbing to $45 billion in 2028. And with 48 facilities spread across 17 different countries and over 3,000 active global clients, Cryoport does stand to benefit from this growth.

Management is using this opportunity to also invest in other new services and products. One example would be the Cryoportal 2 Logistics Management Platform. This is the second generation of the company's current supply chain information system. In addition to making vast improvements on its UX/UI, and also has added new security and compliance features, including a new audit logging system that captures all changes made within the database. There is also the Cryoport ELITE line of shipping containers that are custom built for keeping high value gene therapies at -80 degrees Celsius. These investments, and more, should help the company in the long run.

{kind=link}

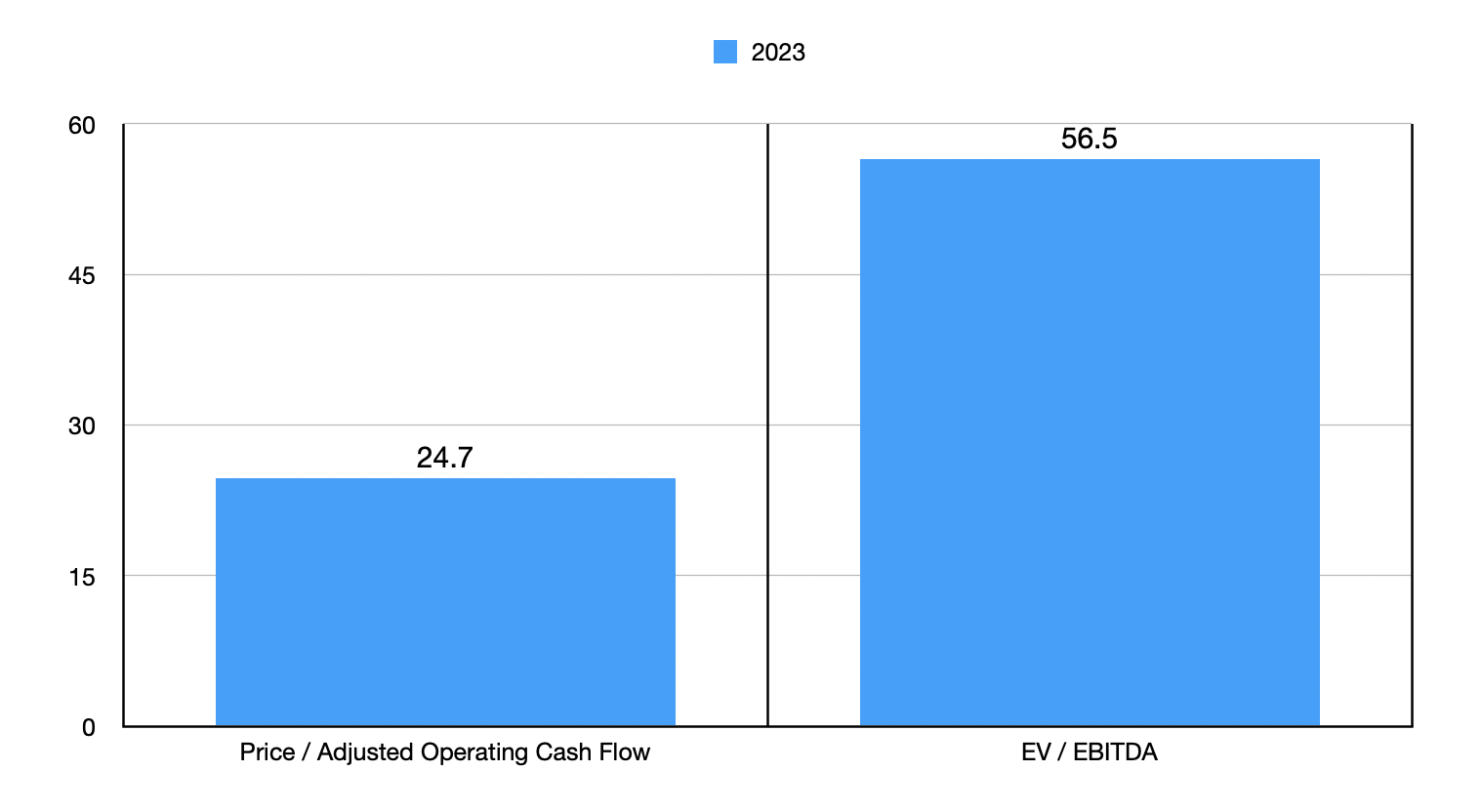

But in order for the company to be taken seriously, we have to see some progress, either in the form of rapid sales growth or in the form of bottom line improvements. As I showed already, the bottom line for the company has worsened from a net profit and EBITDA perspective. For the year-to-date period, operating cash flow has also worsened on an adjusted basis. And sadly, with revenue expected to be between $233 million and $243 million, we aren't really looking at any material change compared to the $237.3 million the company reported last year. Even if profitability were to stabilize at what the company experienced in 2022, shares would be trading at a price to adjusted operating cash flow multiple of 24.7 and at an EV to EBITDA multiple of 56.5. Both of those are astronomical for a company that's not living up to the hype.

Takeaway

All things considered, Cryoport is an interesting company. It's a company that I would love to see succeed and, if the fundamentals warranted it, I would likely invest in it. The firm does seem to have potential based on the market it operates in. But until we see some real improvement, either on the top line or, preferably, on the bottom line, there is no reason to be anything other than pessimistic. Because of this, I've decided to keep the company rated a 'sell' for now.

For further details see:

Cryoport: Great Potential That Management Continues To Fail To Actualize