STVN - Cryoport's Tumble Isn't Over Yet

2023-05-29 04:56:42 ET

Summary

- Cryoport continues to grow its top line, while bottom line results are improving.

- The picture isn't as positive as it initially appears, but progress is still very much welcomed.

- Even so, the firm still has problems and shares look far too pricey to make sense right now.

It takes a great deal for me to become incredibly bearish on a company. In general, I believe that, if a firm is well run, the long-term outlook will at least not be bad. It may not be great, but the company should grow or at least stay the same, while improving bottom line results. I am especially cautious when it comes to taking a bearish stance on companies that are demonstrating attractive top line growth. But when I see a firm that struggles to generate profits year after year, even as revenue grows, I start to worry about that firm's future. When you add on top of this shares that are very expensive from a cash flow perspective, I rarely have any problem anymore rating the company a 'sell' or a 'strong sell'.

One example of a company that I have been quite bearish on recently is Cryoport ( CYRX ). For those who don't know, the business provides special supply chain solutions to companies in the life sciences space. Examples include controlled temperature storage of life science products, packaging and labeling of said products, regulatory services involving them, drug return handling and destruction services, and more. In recent months, shares of the company have plunged. This comes even at a time that revenue growth continues to impress. But even with this decline, I believe that shares of the business are too pricey at this moment relative to the risk that investors assume. So even though the stock has taken a beating, I would make the case that further downside is probably warranted.

More pain incoming

The last article I wrote about Cryoport was published in early February of this year. In that article, I acknowledged that the company was in a pretty good position from a cash perspective. It boasted a tremendous amount of cash on its balance sheet, which made the near-term risk for shareholders of a permanent loss of capital quite small. On the other hand, shares looked very expensive and the company continued to struggle when it came to profitability. These facts convinced me to keep the company rated a 'sell', reflecting my belief at the time that the market would likely outperform the stock for the foreseeable future. Since then, this call has played out quite nicely. While the S&P 500 is down 0.7% since the publication of that article, shares of Cryoport have dropped 15.5%. And since I initially rated the company a 'sell' back in July of last year, shares are down a whopping 47.4% compared to the 0.1% increase experienced by the S&P 500.

{kind=link}

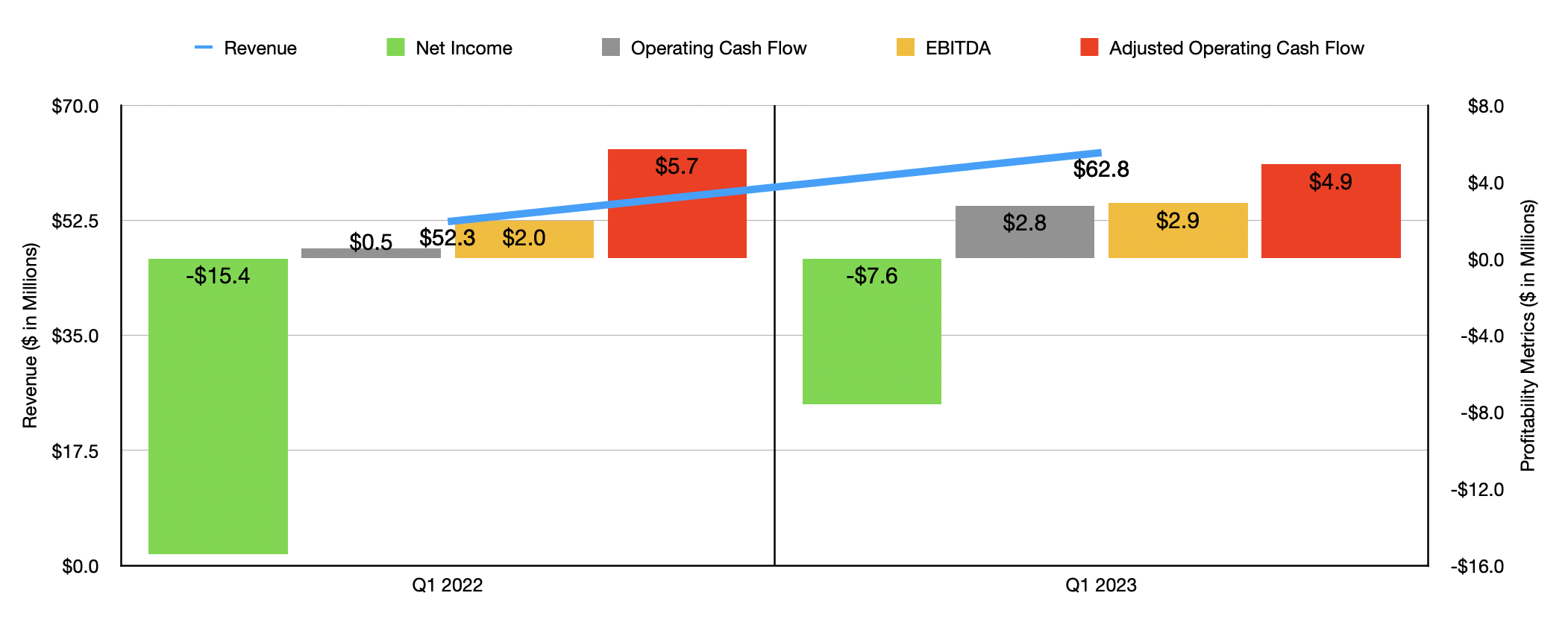

Given the massive downside that the stock has seen, you might think that I would become more neutral on the business. I have, but not so much that an upgrade is warranted. Consider how the company performed during the most recent quarter. This is the first quarter of the company's 2023 fiscal year. During that time, revenue came in at $62.8 million. This represented a 20.1% increase over the $52.3 million the business reported one year earlier. Actual service revenue for the company grew a very modest 8.9% from $32.9 million to $35.8 million. This increase, according to management, was driven by strong customer demand for its supply chain solutions. Product revenue, on the other hand, shot up 39.1%, surging from $19.4 million to nearly $27 million. This move higher, according to management, was driven largely by the firm's recovery from the New Prague Fire that the company experienced last year that ended up resulting in $9.4 million in reduced product sales.

This leads us into the first problem that bothers me about the business. Although the firm has a history of attractive growth, when we adjust for the lost revenue associated with the fire, sales growth year over year in the first quarter was only about 1.8%. That shows a tremendous deceleration in revenue. Having a company that generates net losses can be fine if growth is high enough to convince the market the profits will eventually be large. But a 1.8% growth rate in revenue is not confidence inspiring.

On the bottom line, at least the company did post some improvements. The company went from a net loss of $15.4 million in the first quarter of 2022 to a net loss of $7.6 million in the first quarter of this year. Other profitability metrics did show some improvement as well. Operating cash flow, for instance, went from $524,000 to $2.8 million. If we adjust for changes in working capital, however, we would have seen it drop from $5.7 million to $4.9 million. Meanwhile, EBITDA for the company popped up from just under $2 million to roughly $2.9 million.

{kind=link}

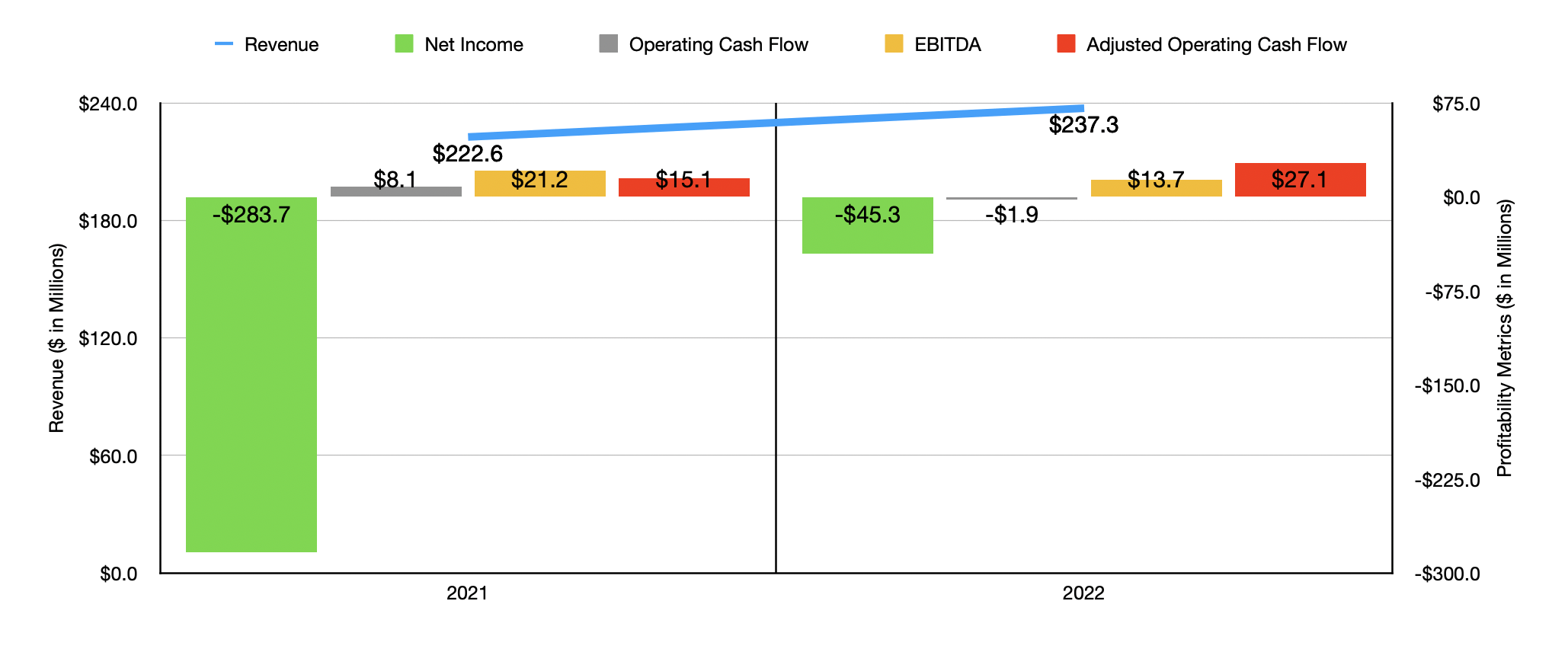

When it comes to the 2023 fiscal year in its entirety, the only real guidance that management provided involved revenue. They currently think that sales will come in at between $270 million and $290 million. This would compare nicely to the $237.3 million in revenue the company generated in 2022 and the $222.6 million generated in 2021. As you can see in the chart above, financial results on the bottom line were mixed in both of those fiscal years. But we do notice that both adjusted operating cash flow and EBITDA were positive. If we assume that the margins associated with these cash flow figures will be reflective of the margins the company should experience this year, then we would anticipate adjusted operating cash flow of $32 million and EBITDA of $16.2 million.

{kind=link}

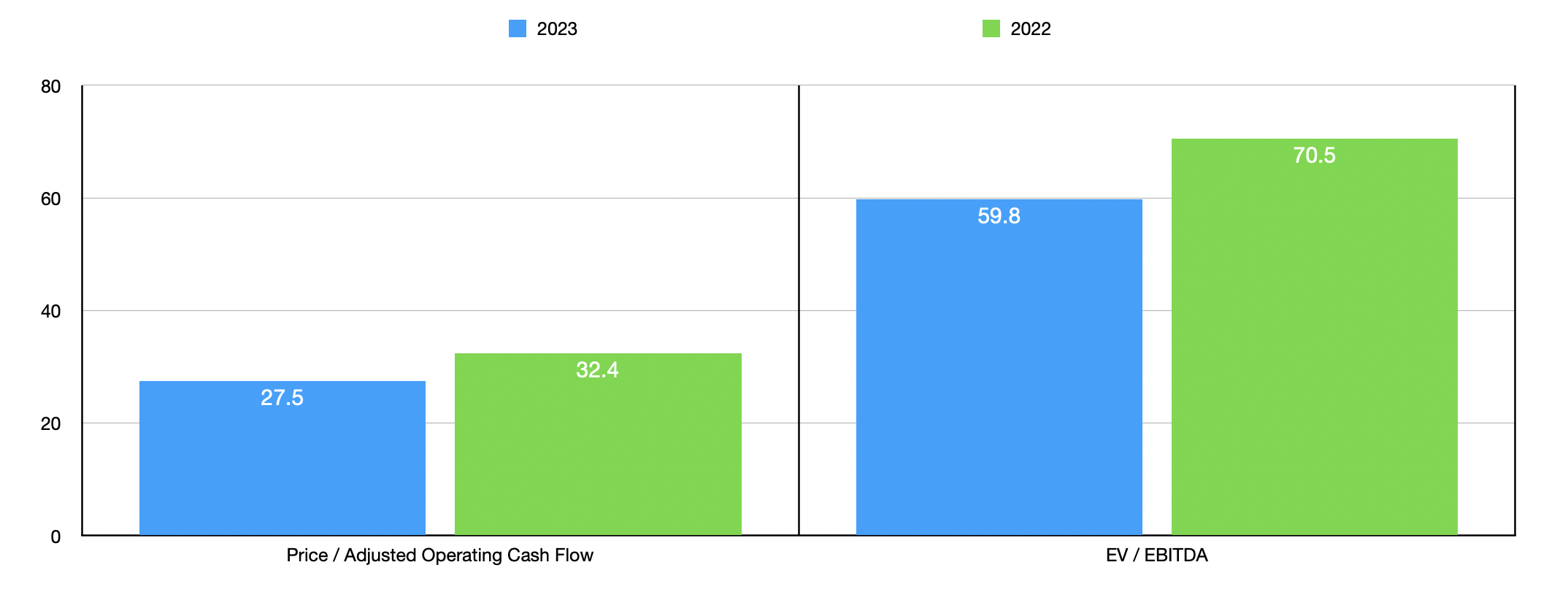

Based on these figures, we can easily value the company. In the chart above, you can see how the company is priced using data from 2022 and using estimates for 2023. As part of my analysis, I also compared the company to five similar firms. In the table below, you can see that, on a price to operating cash flow basis, Cryoport is cheaper than the four firms that had positive multiples. But when it comes to the EV to EBITDA multiple, it ended up being the most expensive of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Cryoport |

| 27.5 |

| 59.8 |

| Nevro ( NVRO ) |

| 40.8 |

| 39.5 |

| Stevanato Group ( STVN ) |

| 49.9 |

| 27.2 |

| AtriCure ( ATRC ) |

| N/A |

| 25.5 |

| Mesa Laboratories ( MLAB ) |

| 31.1 |

| 25.7 |

| LeMaitre Vascular ( LMAT ) |

| 58.2 |

| 34.3 |

Takeaway

Recent months have been very difficult for shareholders of Cryoport. Although the company continues to grow its top line, that growth is now fairly slow when we adjust for the aforementioned fire that it dealt with last year. Profitability remains an issue and cash flows are so low that shares of the business look very expensive on an absolute basis. Relative to similar firms, the picture is definitely mixed. But that doesn't bring me much confidence when we consider all the other problems the company is contending with. Given these factors, I do still think some additional downside is still on the table. I would argue that the amount of additional downside is probably not terribly significant. But it is enough to warrant a soft 'sell' rating in my book.

For further details see:

Cryoport's Tumble Isn't Over Yet