CCLP - CSI Compressco Balances Growth With Cash Flow As Refinancing Awaits

2023-12-04 18:09:29 ET

Summary

- CSI Compressco LP reported a 5.1% YoY revenue growth and increased fleet utilization in its Q3 2023 financial results.

- The company provides natural gas compression and processing services and targets customers in the energy supply chain.

- The global market for natural gas processing is expected to reach nearly $302 billion by 2030, driving the growth of CSI Compressco.

- With the potential for reduced interest costs as the firm nears refinancing combined with growth and cash flow generation, my outlook on CSI Compressco stock is a Buy at around $2.00 per share.

A Quick Take On CSI Compressco

CSI Compressco LP ( CCLP ) reported its Q3 2023 financial results on November 2, 2023, reporting revenue growth of 5.1% year-over-year and increasing fleet utilization.

The firm provides a range of natural gas compression and processing services.

The potential for reduced interest costs, while management balances growth and expense discipline means my outlook on CCLP is a Buy at around $2.00 per share.

CSI Compressco Overview And Market

The Woodlands, Texas-based CSI Compressco was founded in 2008 and provides natural compression fleet rentals and related services in the U.S. and internationally.

The firm is headed by Chief Executive Officer John Jackson, who founded Spartan Energy Partners in 2010. Previously, he was Chairman and CEO of Price Gregory Services, an energy pipeline construction service provider.

The company’s primary offerings include the following:

-

Compression and services

-

Treating and cooling (Spartan Energy).

CCLP acquires customers through its direct business development efforts and targets E&P, midstream, and transmission/storage companies in the energy supply chain.

According to a 2023 market research report by Virtue Market Research, the global market for natural gas processing was estimated at $201 billion in 2020 and is forecast to reach nearly $302 billion by the end of 2030.

This represents a forecast CAGR (Compound Annual Growth Rate) of 5.2% from 2023 to 2030.

The main driver for this expected growth is the continued growth in demand for natural gas in pure form for saleable use by consumers.

Also, technological advancements have resulted in lower operational costs, enabling operators ‘to extract higher-quality gas while minimizing emissions.’

The International Energy Agency forecasts that the global capacity for gas processing will reach 15.0 billion meters per day by 2030, "due to rising demand for gas in countries like China, India and the United States."

Major competitive or other industry participants include:

-

PetroChina

-

China National Petroleum

-

PJSC Gazprom

-

ConocoPhillips

-

BP Plc

-

Royal Dutch Shell

-

TotalEnergies SE

-

Statoil

-

Exxon Mobil

-

Saudi Arabian Oil Co.

-

Chevron.

CSI Compressco’s Recent Financial Trends

Total revenue by quarter (blue columns) has continued to grow year-over-year; Operating income by quarter (red line) has also trended higher in recent quarters:

Seeking Alpha

Gross profit margin by quarter (green line) has been trending higher in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have trended slightly lower more recently:

Seeking Alpha

Earnings per share (Diluted) have remained negative but have made slow progress toward breakeven:

Seeking Alpha

(All data in the above charts is GAAP.)

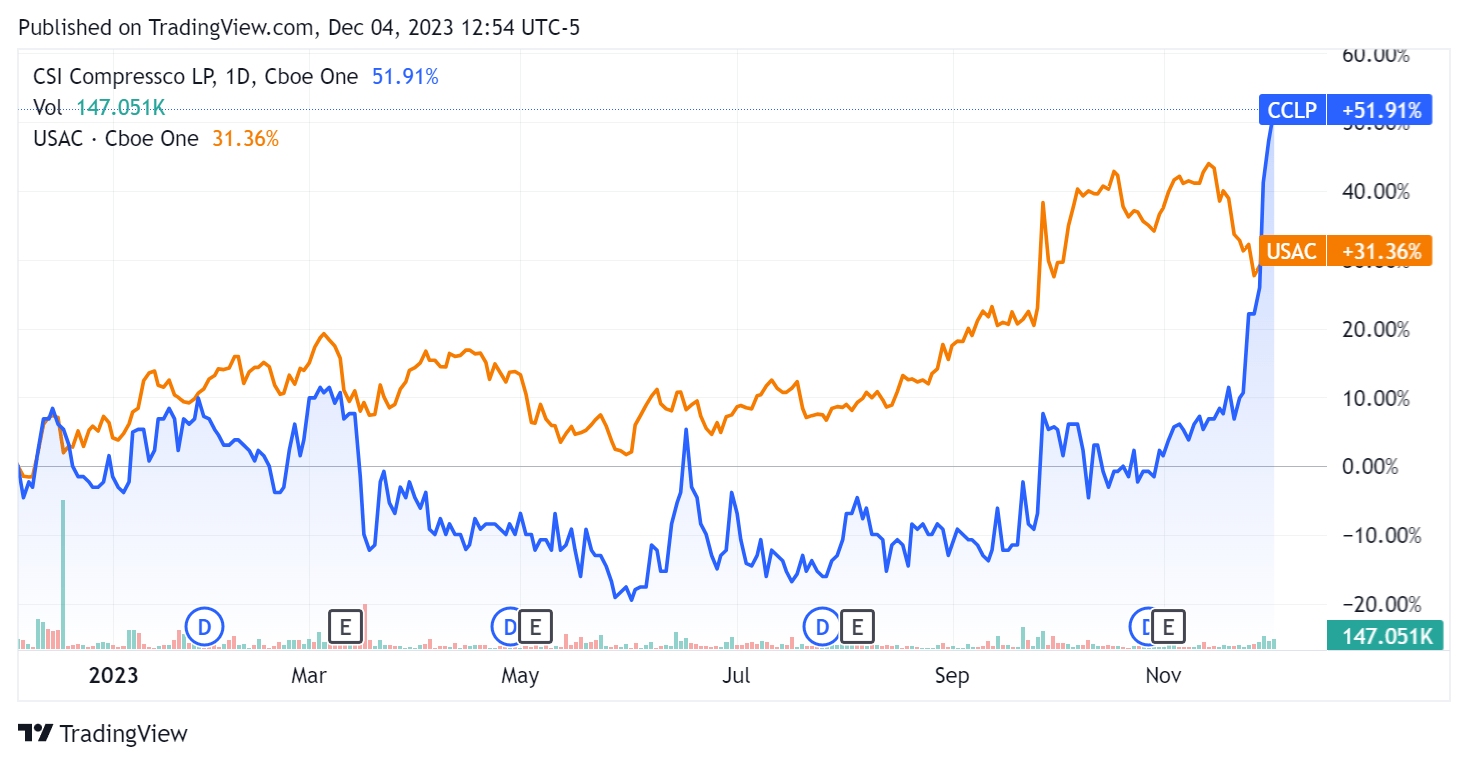

In the past 12 months, CCLP’s stock price has gained 51.91% vs. that of USA Compression Partners, LP's (USAC) rise of 31.36%:

{kind=link}

For balance sheet results, the firm ended the quarter with $15.5 million in cash and equivalents and $634.2 million in total debt, of which $7.3 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash used was ($1.0 million), during which capital expenditures were $52.4 million. The company paid only $1.4 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For CSI Compressco

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 2.4 |

| Enterprise Value / EBITDA |

| 7.3 |

| Price / Sales |

| 0.7 |

| Revenue Growth Rate |

| 12.4% |

| Net Income Margin |

| -2.7% |

| EBITDA % |

| 32.6% |

| Market Capitalization |

| $274,050,000 |

| Enterprise Value |

| $907,600,000 |

| Operating Cash Flow |

| $51,370,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.08 |

| Free Cash Flow Per Share |

| -$0.01 |

| SA Quant Score |

| Hold 3.42 |

(Source - Seeking Alpha.)

As a reference, a relevant partial public comparable would be USA Compression Partners:

| Metric (Trailing Twelve Months) |

| USA Compression |

| CSI Compressco |

| Variance |

| Enterprise Value / Sales |

| 6.3 |

| 2.4 |

| -62.1% |

| Enterprise Value / EBITDA |

| 11.1 |

| 7.3 |

| -33.9% |

| Revenue Growth Rate |

| 20.3% |

| 12.4% |

| -38.7% |

| Net Income Margin |

| 7.9% |

| -2.7% |

| --% |

| Operating Cash Flow |

| $262,380,000 |

| $51,370,000 |

| -80.4% |

(Source - Seeking Alpha.)

Commentary On CSI Compressco

In its last earnings call (Source - Seeking Alpha ), covering Q3 2023’s results, management’s prepared remarks highlighted the company's revenue growth as being driven by increasing utilization and stronger pricing.

Distributable cash flow was $14 million, up notably from $11.1 million in the same quarter in 2022.

The company's net leverage rate dropped to 4.8x, the lowest since the first quarter of 2016 as management continues to focus on ‘returns and deleveraging’ over growth at all costs.

In the earnings call, I tracked the frequency of a variety of keywords and terms mentioned by management and analysts:

Seeking Alpha

Analysts asked management about its pricing dynamics, organic growth expectations and debt refinancing.

Management said that pricing for its larger compressor equipment was up significantly, as high as 60% more than 1 - 2 years ago. Smaller compressors are higher, but only by about 15%.

Growth expectations are for high single-digit to low double-digit organically.

Leadership believes the firm could grow faster but is constrained by capital availability. The firm has plans to reevaluate options after concluding the refinancing of existing debt.

For that debt refinancing, management forecasts interest costs to increase by 1% to 2% and is currently seeing a wide range of pricing.

For the quarter’s results, total revenue for Q3 2023 rose by 5.1% YoY while gross profit margin increased by 1.9%.

Selling and G&A expenses as a percentage of revenue grew by 0.5%, and operating income produced strong growth of 33.3%.

The company's financial position is moderate, with enough liquidity from cash-on-hand and available credit.

Looking ahead, management is seeking to continue to transition its fleet composition to higher rate-producing compressors under contract terms of increasing duration and CPI price escalators.

With the potential for lower interest rates just as the company needs to refinance its significant debt load, CCLP may be in a position to improve its capital structure and costs.

As the stock price has been up sharply in recent weeks, the prospect of reduced interest costs while management balances growth and expense discipline leads me to be Bullish [Buy] on CSI Compressco LP stock at around $2.00 per share.

For further details see:

CSI Compressco Balances Growth With Cash Flow As Refinancing Awaits