CCLP - CSI Compressco: Recovery Should Gain Momentum In The Year Ahead

2023-03-15 12:05:12 ET

Summary

- The last few years have been tough for CSI Compressco but at least there were signs of a recovery back in late 2022.

- Whilst their subsequent cash flow performance during the fourth quarter was not stellar, when digging deeper, it did not derail nor disprove hopes for a recovery.

- More importantly, going forward into 2023 their guidance sees earnings around 12.50% higher year-on-year.

- This means their recovery should gain momentum in the year ahead and thus should help with deleveraging.

- Despite the lack of distribution growth on the horizon, I believe this still makes maintaining my buy rating appropriate.

Introduction

Following several tough years, back in late 2022, it seemed that CSI Compressco ( CCLP ) was possibly leaving the dark days behind because as my previous article discussed, there were signs of a recovery beginning. As we now enter 2023 and can see their new guidance, it seems their recovery should gain momentum in the year ahead with solid results forecast.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

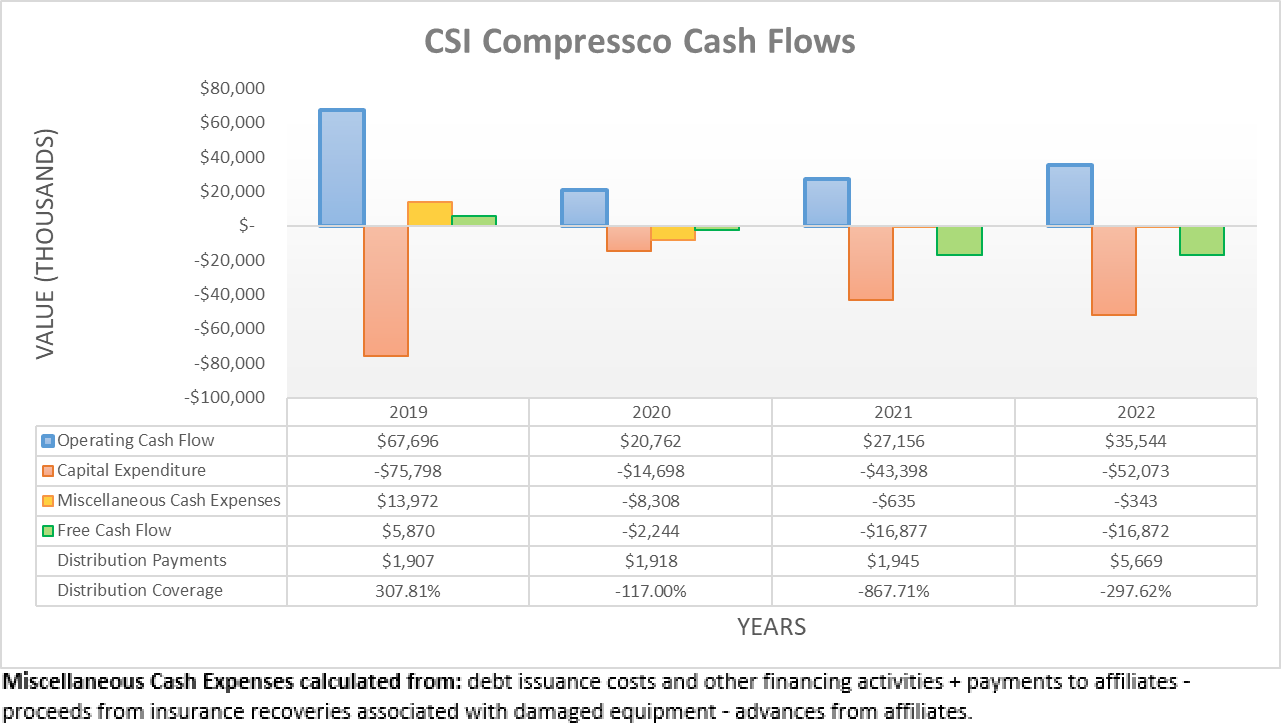

When last reviewing their cash flow performance following the third quarter of 2022, it appeared they were finally seeing the beginning of a recovery, with their operating cash flow increasing materially versus earlier quarters. This raised hopes heading into their fourth-quarter results, but upon opening their report, it was disappointing to see their operating cash flow for the full year actually reversed lower to $35.5m versus the $44m they had already generated during the first nine months. On the surface, this would naturally cast severe doubts over their recovery, but thankfully, if digging deeper, there are still hopes.

{kind=link}

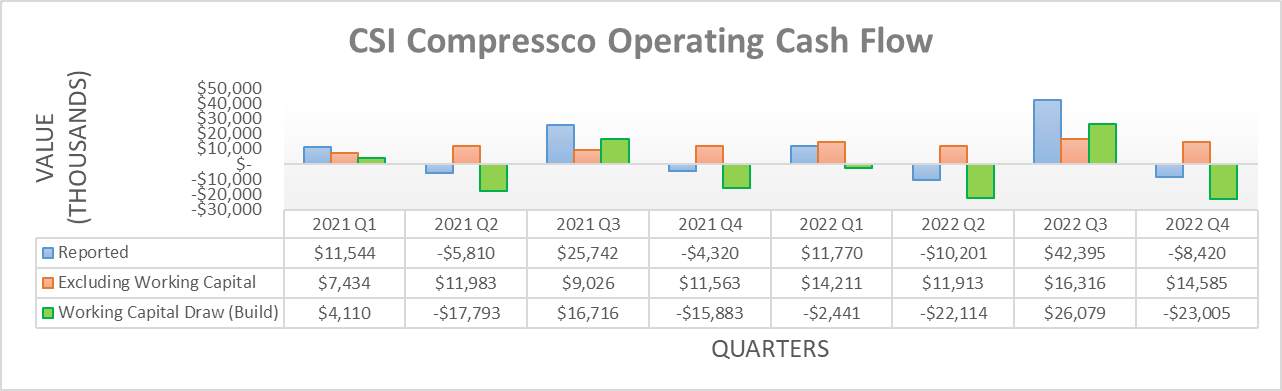

Once switching to a quarterly view of their operating cash flow, it is more easily visible to see their reported results were weighed down by working capital builds in three out of the four quarters during 2022. In particular, the fourth quarter saw a very large build of $23m that effectively wiped out the entirety of their cash generation and thus gave rise to their reported operating cash flow of negative $8.4m that was responsible for their full-year result sliding below that of the first nine months. If this build is excluded, their underlying result of $14.6m during the fourth quarter of 2022 is better. Whilst this is still down versus their previous equivalent result of $16.3m during the third quarter, it remains decent as the second-highest point in recent history since at least the beginning of 2021 and thus, it does not derail nor disprove hopes for a recovery.

When everything is said and done, full-year 2022 saw a net working capital build of $21.4m with their three respective builds of $2.4m, $22.1m, and $23m during the first, second and fourth quarters more than offsetting the draw of $26.1m during the third quarter. Whilst this temporarily skewed the reported results during 2022, at least their guidance for 2023 sees solid results forecast.

CSI Compressco Fourth Quarter Of 2022 Results Announcement

Similar to most companies and partnerships, management does not provide guidance for their operating cash flow, although its relative change can still be inferred given its positive correlations to their adjusted EBITDA. As for the latter, they forecast a result of $130m at the midpoint during 2023 that represents a solid increase of about 12.50% year-on-year against their result of $115.5m during 2022, as per their fourth quarter of 2022 results announcement. In theory, their operating cash flow should see a similar increase when excluding working capital movements and thus, it indicates their recovery should gain momentum in the year ahead. Elsewhere, they forecast capital expenditure of $45.5m at the midpoint, which is modestly lower than the $52.1m they incurred during 2022.

{kind=link}

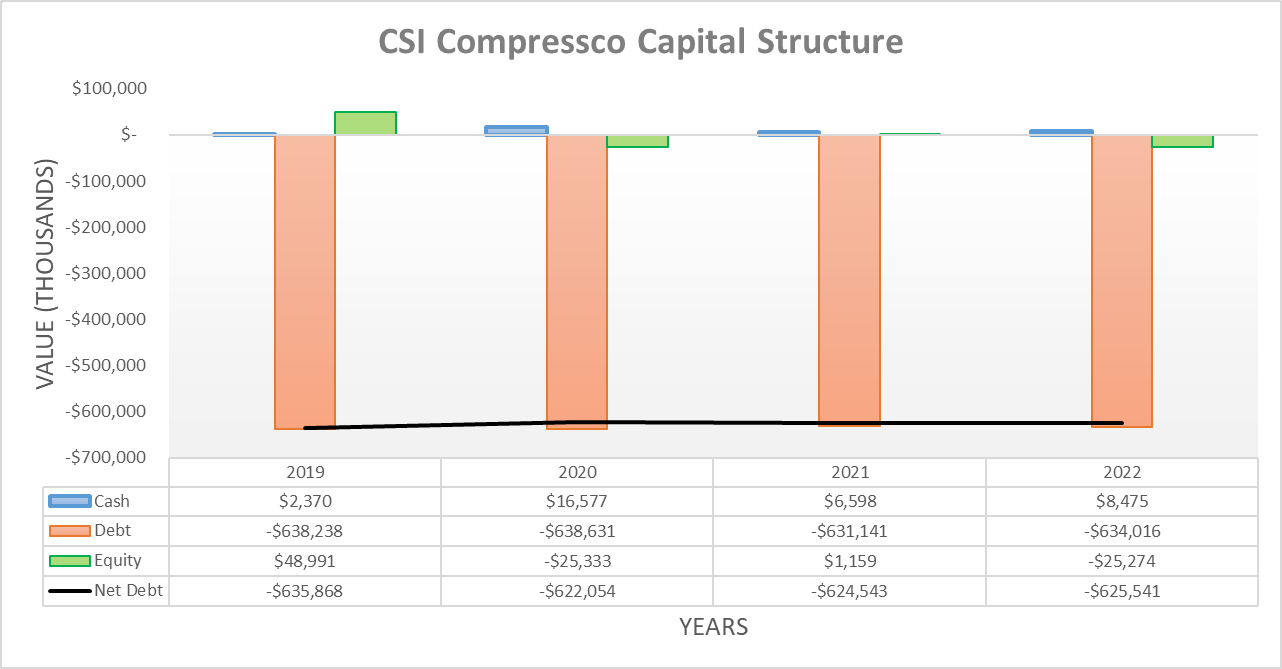

Due to their aforementioned very large working capital build during the fourth quarter of 2022, their net debt reversed its decline from earlier in the year to ultimately end the year at $625.5m. Apart from being slightly higher than their previous result of $608.3m following the third quarter, this is now effectively back to its previous level of $624.5m at the end of 2021.

Whilst a disappointing note, there is nevertheless hope that 2023 should see improvements that hopefully persist. Firstly, their working capital build during 2022 should reverse into a draw and thus, in theory, provide an additional cash infusion on top of what they generate throughout the year. Even if not forthcoming, secondarily they should also benefit from the combination of stronger financial performance and modestly lower capital expenditure, which should translate into higher free cash flow. In light of the only slight changes to their net debt since conducting the previous analysis, it would be redundant to reassess their leverage, debt serviceability, and liquidity in detail, especially as their outlook for 2023 was the primary focus of this follow-up analysis.

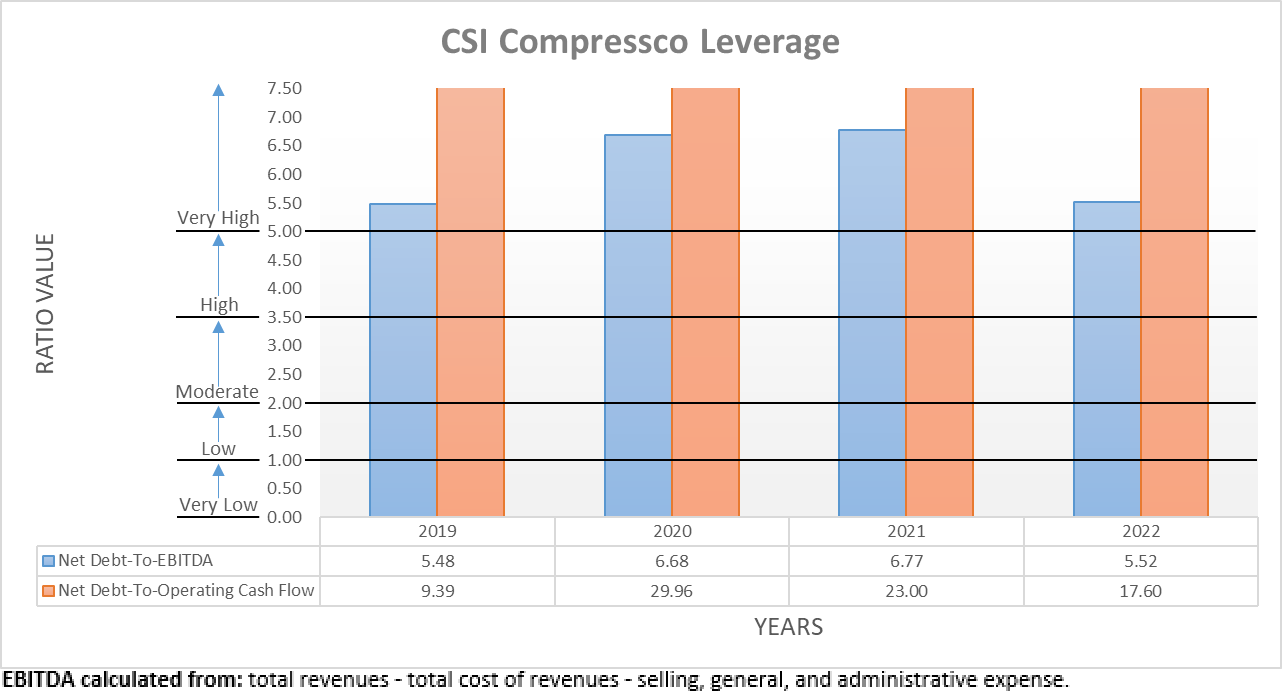

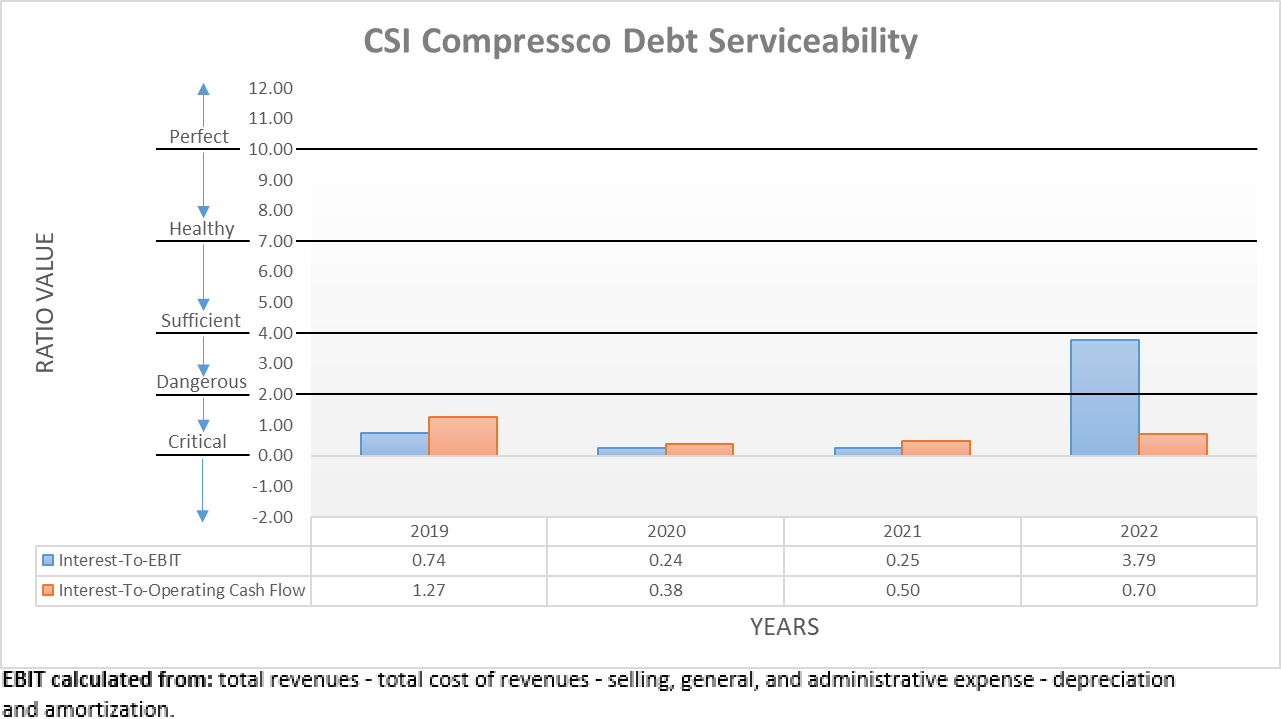

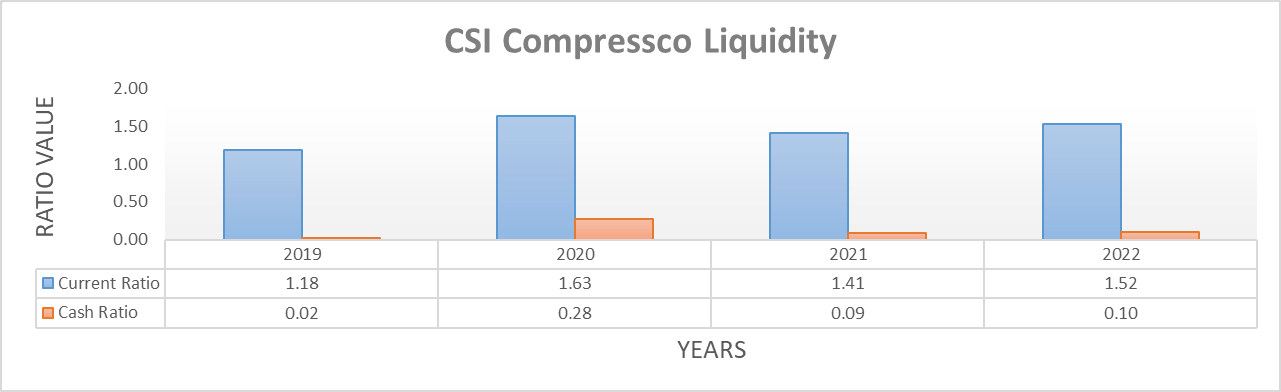

The three relevant graphs are still included below to provide context for any new readers that, quite unsurprisingly, once again show their leverage is very high as easily evident with their net debt-to-EBITDA of 5.52 and net debt-to-operating cash flow of 17.60 both well above the applicable threshold of 5.01. Likewise, it was only natural to see their debt serviceability remaining dangerous with interest coverage of 0.70 when compared against their operating cash flow. Whilst the comparison against their EBIT sees sufficient coverage of 3.79, I prefer to judge on the worst side. At least they retain fiscal stability from their liquidity that remains adequate given their current ratio of 1.52 and their accompanying cash ratio of 0.10. If interested in further details regarding these topics, please refer to my previously linked article.

{kind=link}

{kind=link}

{kind=link}

Conclusion

They are far from a perfect partnership, especially given their overleverage, but at least, there are signs their recovery should gain momentum in the year ahead as 2023 progresses. Even though there are no prospects for higher distributions on the horizon, their beaten-down unit price should still benefit with every dollar of net debt repaid and thus, I believe that maintaining my buy rating is appropriate as we head into 2023.

Notes: Unless specified otherwise, all figures in this article were taken from CSI Compressco's SEC Filings , all calculated figures were performed by the author.

For further details see:

CSI Compressco: Recovery Should Gain Momentum In The Year Ahead