BUDFF - Davide Campari-Milano: Sustainable Grower In The Beverage Sector

2023-11-23 05:54:59 ET

Summary

- Campari has a strong brand portfolio with premium drinks, appealing to the upper middle class and is therefore less sensitive to recessions.

- The company has little exposure to Asia, leaving room for future growth in this massive untapped market.

- Campari has achieved impressive organic growth, with a +40% increase in 2022 compared to pre-pandemic levels, and long-term growth prospects look promising.

- Stock recently made a nice correction after some disappointing news, but this could be an interesting buying opportunity for long-term investors.

Introduction

Davide Campari-Milano N.V. ( DVCMY ) is an international drinks company known for its iconic brands: Campari, Aperol and Sky Vodka. I have been following Campari as an analyst for several years, and it's my favorite in the beverage sector. The company still has a modest market value of 12.14 billion EUR (13.21 billion USD). If you compare this to other beverage makers like Diageo ( DEO ) or AB In B ev ( BUD ) who are worth close to 100 billion USD, you can see that Campari is still a small fish. And that's what I like to invest in. Quality midcaps with the potential for a lot of growth.

{kind=link}

Campari history of brands (Campari annual report 2022)

Campari has been a fantastic success story for investors already. With +240% returns over 10 years and +1000% over 20 years. Today we take a look at why I like the company so much and why this is my preferred defensive investment, with growth, in the beverage space.

Campari: strong brands for long-term success

{kind=link}

Campari global priorities (Campari annual report 2022)

Campari's entire brand portfolio contains more than 50 different brands and has, in my opinion, one of the strongest drinks portfolios on the market. The portfolio contains mostly premium drinks. Some of its biggest brands are: Aperol (aperitif), Campari (aperitif), Sky Vodka (vodka), Wild Turkey (bourbon), Grand Marnier (liqueur), Appleton Estate (rum), Espolon (tequila), Lallier (champagne). In short: a whole spectrum of drinks for a lot of different consumers, to enjoy on a Friday night or in the weekend.

The company is also not depended on just one drink, the revenue diversification is actually well under control. One would think the Campari company is more than 50% dependent on Aperol and Campari, but it's actually only around 30%.

- Aperol is good for 21% of revenue.

- Campari is good for 11% of revenue.

- Wild Turkey is good for 8% of revenue.

- Grand Marnier is good for 6.5% of revenue.

- And other brands represent less than this...

The fact that most of the drinks from Campari aim to higher end consumers, should make the company less sensitive to recessions. As more affluent consumers don't really care about a recession to stop drinking their favorite cocktail. Campari is also playing the ready to drink cocktail market with its pre-packaged and ready to drink Aperol Spritz cocktails, an import growth driver.

So Campari is playing the right consumer trends, and I'm increasingly seeing a shift in society from beer consumption to cocktails. And I think this megatrend will continue. Beer is still a growing market, with an estimated 3% per year. And almost half of that growth will come from Asia. But it has been mostly flat from 2019 to 2021 and beer consumption is almost not growing in the West. But other type of drinks, like apéritifs, are growing much faster.

{kind=link}

Beer market industry analysis (technavio.com website)

Grand View Research (a research organization), assumes that the ready to drink cocktail market (like pre-packaged Aperol Spritz) will grow with a CAGR of 13% per year from 2020 to 2030.

{kind=link}

Ready to Drink cocktails market growth (Grand View Research website)

Finally, it is clear to me that Campari is conquering the West with its Aperol and Campari cocktails. The Aperol Spritz and the Negroni have been in the top 10 list of most popular cocktails worldwide for years, and they are growing in popularity. 46% of turnover comes from North and South America. 47% from wider Europe.

And that brings me to my next point. A positive thing about Campari is that it has little exposure to Asia (7.7% of turnover), especially China. The growth offensive has yet to get underway there. Hundreds of millions of consumers can therefore still be addressed in the coming years.

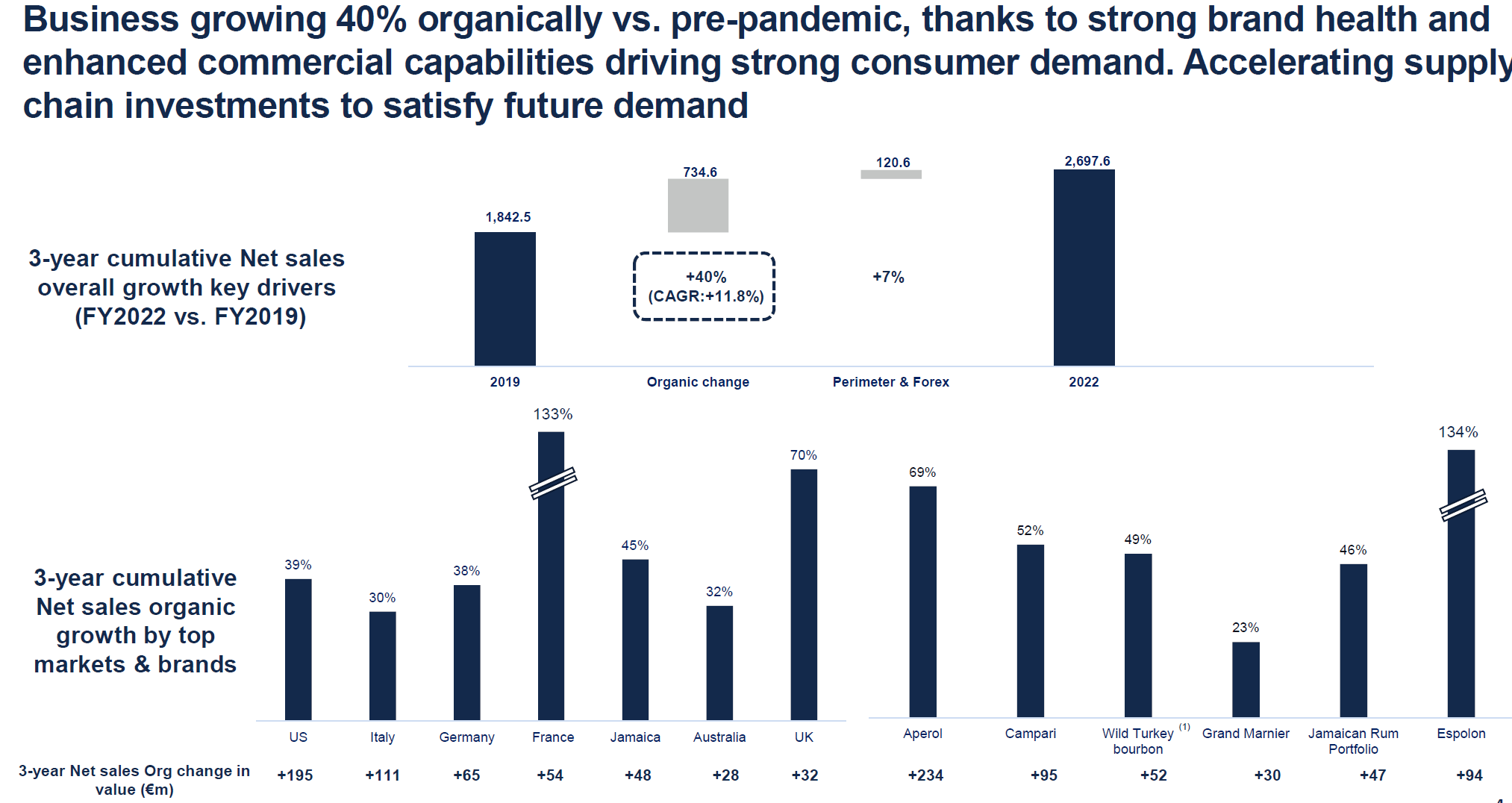

To demonstrate how strong Campari's growth is, consider the 2022 annual report. Campari saw no less than 40% organic growth in 2022 compared to the pre-pandemic year of 2019. That is extremely impressive. And many of its top brands contributed to that strong organic growth.

{kind=link}

Campari business 3-year cumulative growth (Campari annual presentation 2022)

Longer-term growth also looks fantastic. Just look at the photo below of the turnover development.

{kind=link}

Campari revenue overview 2002 - 2023 (Koyfin author subscription)

Since 2002, turnover has increased from 503 million euros to more than 2.7 billion euros today. Good for a x4.36. Very few companies can deliver this kind of growth in a relatively defensive sector (beverage). The company uses a 50% organic growth strategy and 50% acquisitions. This means that opportunistic acquisitions are regularly made, but above all, organic growth is also a priority. And I personally think that organic growth is the most important parameter, as its brands should grow stronger over time.

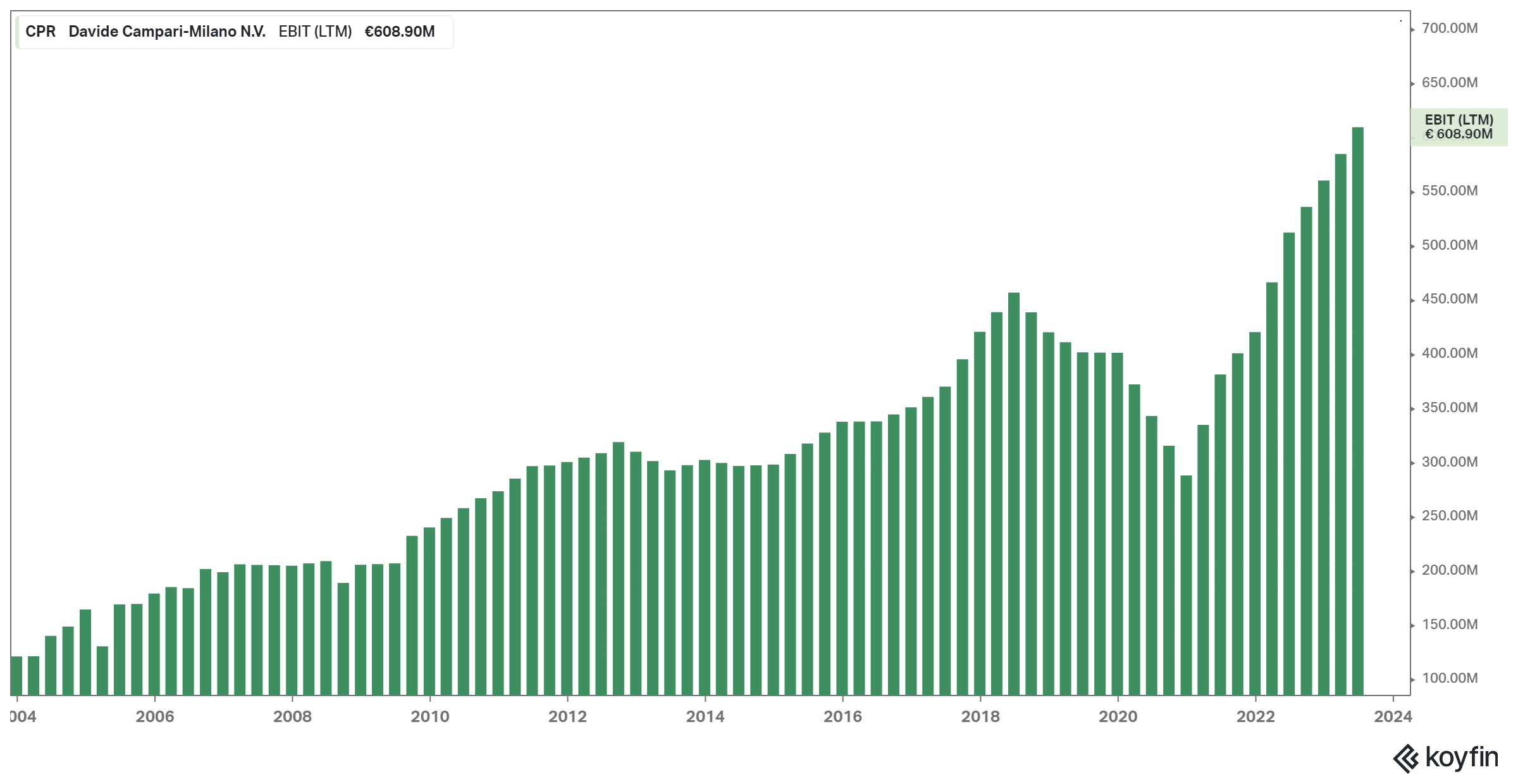

Also the profitability of Campari is going in the right direction. In 2002 the company was barely making 100 million EUR in EBIT. Now it's making more than 600 million EUR per year. So revenue went times 4.36. While profits went times 6. That's what I like to see as an investor.

{kind=link}

Campari EBIT overview 2002 - 2023 (Koyfin author subscription)

Nice detail too: Campari is a family-controlled company. 54% of the shares are still owned by the family. That accounts for 85% of the voting rights. I often have a preference for family businesses, because they are better managed with a view to the longer term and with a focus on value creation for shareholders.

Why is Campari an interesting investment opportunity?

{kind=link}

Negroni campaign Q3 2023 (Campari)

So the story of Campari is very simple for me. I mainly want to focus on safety and growth in my investment decisions. And Campari fits perfectly in that list. It's a company that I know well, of which I am also a customer (Aperol Spritz and Negronis are my favorite cocktails) and with superior growth prospects in an otherwise rather boring beverage sector. Campari doesn't need to reinvent the wheel to do well. It just needs to continue to do, what it's doing. The results speak for themselves. The company now needs to expand further into Asia (only 200 million USD sales right now), and continue to promote its cocktails and gain market share. An annual sales growth rate of around 7% to 10% per year seems very reasonable (based on past performance) and would double sales in 7 to 10 years' time.

The fact that the company still has a relatively low market capitalization, also puts a floor under the price, as I believe that a company like this would become an immediate takeover candidate if price would drop too much. A larger beverage company would love to buy this high quality growth company with intriguing brands at cheap prices.

Recent developments

Unfortunately, the old CEO who headed Campari recently decided to retire. With this, Campari lost a fantastic leader that turned Aperol into a global powerhouse.

As a result, the share has been under some pressure in recent months. But an internal leader was prepared to become the new CEO, Matteo Fantacchiotti. Matteo is currently the managing director of the Asia Pacific region for Campari and will become CEO in April 2024. Fantacchiotti is certainly not a bad leader. He has experience at Nestle ( NSRGY ), Diageo ((DEO)) and Carlsberg ( CABGY ). Three giant consumer companies. I therefore continue to have confidence in the Campari story. Also notice that the Asia leader is now the CEO. Which could increase the focus of the total company on Asia, where the growth is.

Over the first 9 months of 2023, Campari booked 2.2 billion EUR in sales. Which represents 10.5% organic growth. Adjusted EBIT also increased 10.8% to 520 million EUR. This represents a slowdown from the first quarters of 2023, but it's quite normal considering the very strong results Campari reported in 2021 and 2022. So for the next 6 months, especially in the current challenging macro environment, a more stable revenue evolution would make sense. Investors didn't like the news and dumped the stock on the weaker than expected Q3 results, but the stock recovered quickly, which shows how much demand there is for this stock. Every dip is currently being bought up. Also, I still believe Campari will be hurt less than other big beverage companies during a recession, due to its growth profile and its high-end consumer focus. So while a slowdown in the short term is always possible, I believe it will outperform the market in the long term.

At the end of September, Campari had 1.8 billion EUR in net debt. But with a 601 million EUR EBITDA for the first nine months, it's still reasonable (2.6x net debt/EBITDA at full year projection from Campari).

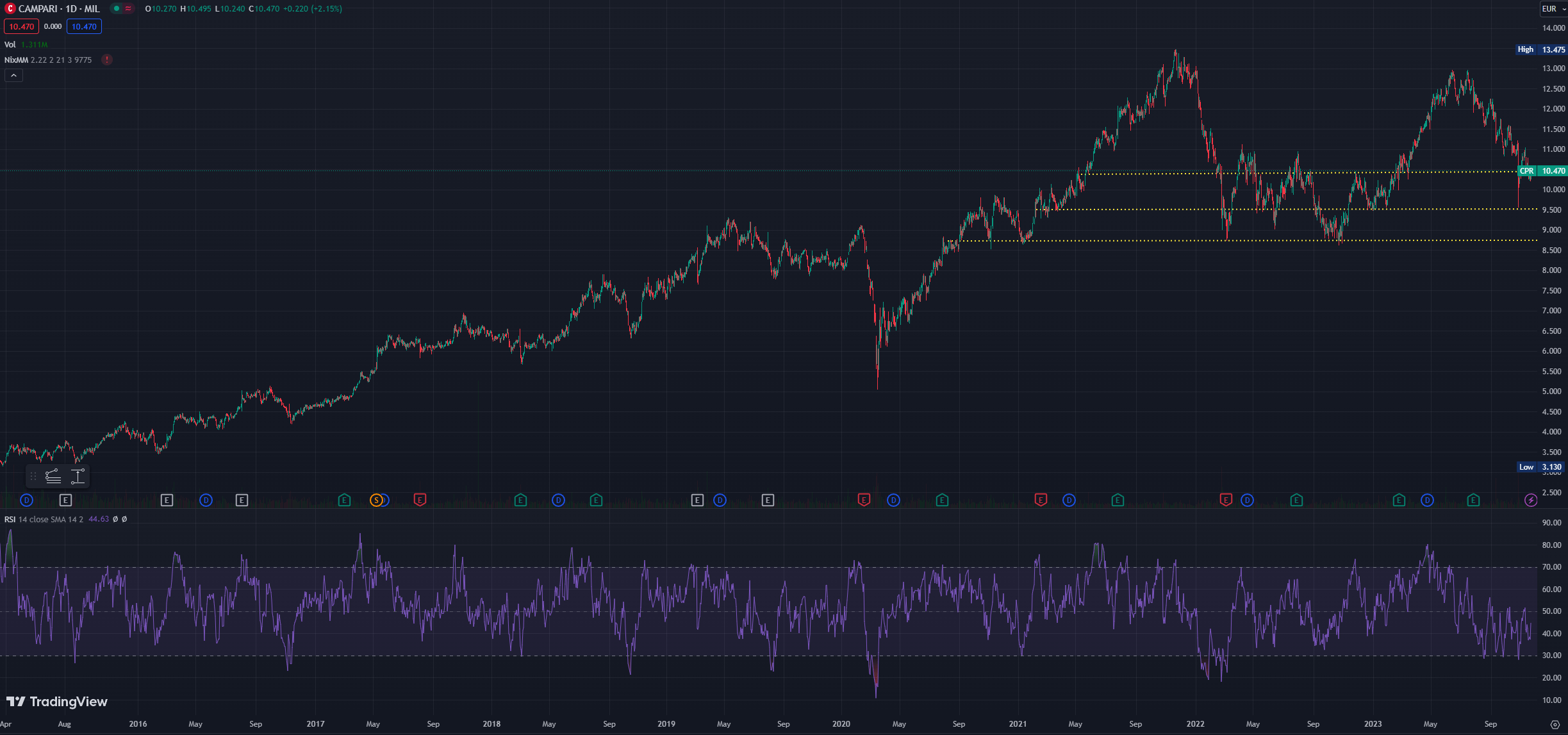

Technical picture

{kind=link}

Campari recently fell from 13 EUR to 10.2 EUR, which now is a support line.

If it went through 10.2 EUR, then the next support is around 9.5 EUR. I consider every dip around 9.5 EUR as a first extra buying opportunity for this long term compounder with strong brands.

Around 8.5 EUR I would double down, if nothing has fundamentally changed.

Everything below this price would concern me, as it would mean something has fundamentally changed in the story. So then we have to reevaluate.

Conclusion

For Campari, you currently pay 13.5 billion EUR in enterprise value. With an expected EBIT of around 1 billion EUR by 2027, you pay around 13.5x the future EV/EBIT. To me, that is a very fair price for a quality company like Campari. And that would be a very low valuation when looking historically. The company has not traded below 14x EV/EBIT since 2014. It mostly trades around 19x EV/EBIT.

Over the next 10 years, I think Campari will continue to grow, organically and through acquisitions. Moreover, it could also become a takeover target for other major beverage companies.

With an enterprise value of 13.5 billion EUR, Campari is a snack for drink giants worth north of 80 billion USD. But of course the controlling family would have to agree to a sale, which probably wouldn't happen anytime soon unless the offer was particularly high.

Anyway, I hope you have enjoyed this article. If you did, feel free to like my work and follow me. I only write about companies I truly believe in and that I understand well.

Disclaimer : always do your own research. Investing is risky. Campari has low volume on the USA markets, but lots of volume in Milano (ticker: CPR) and ISIN-number (NL0015435975). So I recommend buying it there if you're interested in a position.

For further details see:

Davide Campari-Milano: Sustainable Grower In The Beverage Sector