DBL - DBL: This Is A Decent Bond Fund But Not When It Is At A Premium

2023-12-20 04:44:22 ET

Summary

- Doubleline Opportunistic Credit Fund is a debt fund that aims to provide income-focused investors with current income and potential capital appreciation.

- The fund's manager has a strong reputation as a quality debt house, but its current yield of 8.57% is lower than other fixed-income funds.

- Over the past three years, DBL has delivered a 3.26% gain to investors, offsetting the decline in share price.

- The fund failed to cover its distribution in the most recent fiscal year and is relying on selling new shares to fund the shareholder payouts.

- The fund is quite expensive right now, especially considering that it is unable to cover its distribution.

The DoubleLine Opportunistic Credit Fund ( DBL ) is a closed-end fund that provides income-focused investors an attractive way to achieve their goals and potentially retain more upside potential than simply putting their money into an ordinary leveraged fixed-income fund. The fund's description on the webpage is a bit misleading though, as this fund is a debt fund and not a blended fund that invests in both debt and equity securities. We will discuss this in more detail later in this article. The fund also does not have as high a yield as most fixed-income funds today, as its 8.57% current yield pales in comparison to the double-digit yields available from other options. DoubleLine has earned a very strong reputation for being a quality debt fund manager though, so the fund does have that going for it. After all, as we have seen in a few previous articles, some investors are willing to pay a premium valuation to purchase shares from certain managers. For example, PIMCO funds tend to trade at enormous premiums for precisely this reason.

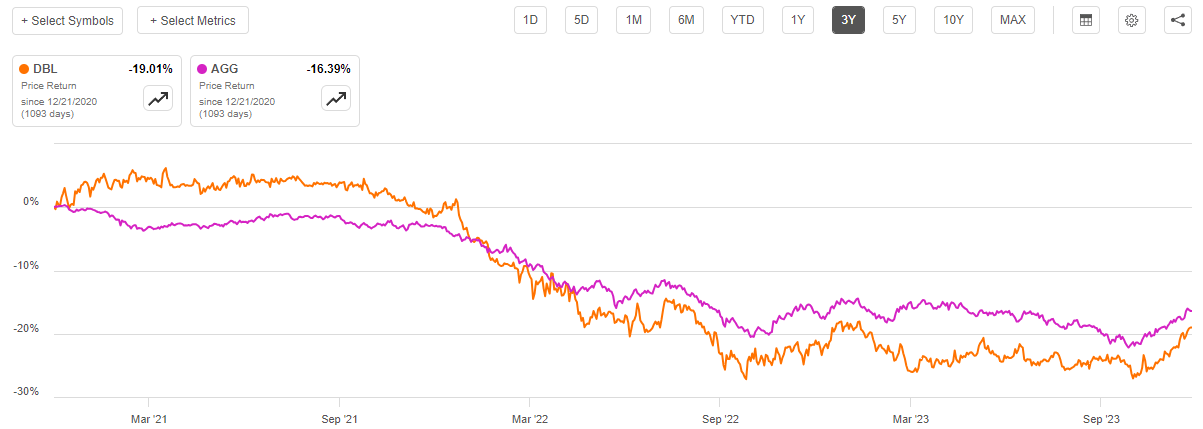

As everyone reading this is no doubt well aware, the past few years have been very difficult for fixed-income funds. With the notable exception of those funds that managed to invest their assets into floating-rate securities, pretty much every fund that invests in this sector took fairly large losses when interest rates increased. The DoubleLine Opportunistic Credit Fund was certainly no exception to this, as shares of the fund are down 19.01% over the past three years. This is significantly worse than the 16.39% decline in the iShares Core U.S. Aggregate Bond ETF ( AGG ):

{kind=link}

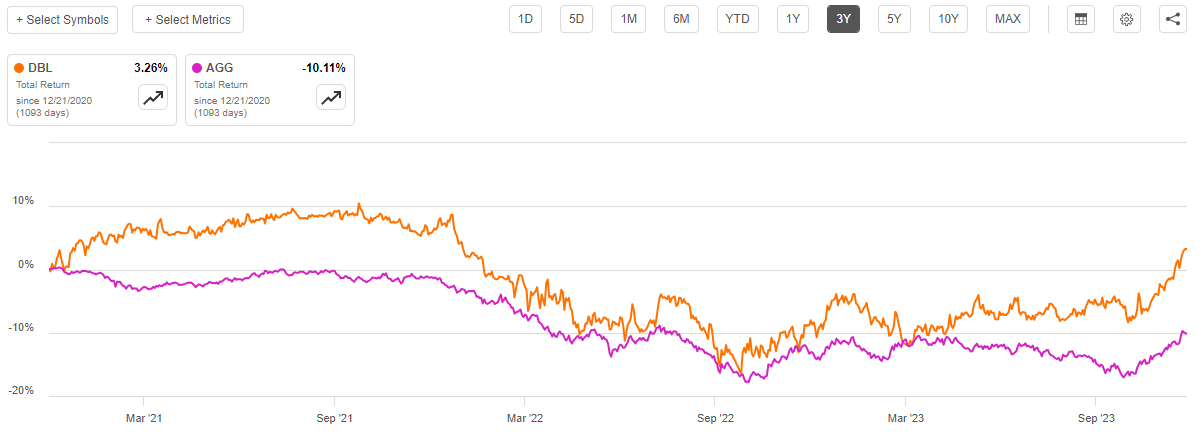

However, as I have pointed out in numerous previous articles, closed-end funds tend to pay out most to all of their investment profits to their investors. This is even true when a fund's share price declines as a bond fund like this one will still collect interest payments from the assets in its portfolio. The fund still pays this money out to the shareholders despite its assets declining in price, and these payments have the effect of offsetting some of the share price declines. As such, we should always look at the total return when evaluating the performance of a fund as opposed to simply the share price fluctuations. When we do this, the DoubleLine Opportunistic Credit Fund looks much more attractive. Over the past three years, investors in this fund have actually earned a 3.26% gain, which does not seem that attractive at first but it is still much better than the Bloomberg U.S. Aggregate Bond Index managed to deliver over the period:

{kind=link}

Thus, investors in this fund managed to earn enough in distributions to completely offset all of the impact of the declining share price. Admittedly, this is not ideal, but it should still at least somewhat increase the fund's appeal in the eyes of those investors who are highly risk-averse and do not want to lose money. For example, many retirees might be in this category.

Over the past few weeks, long-term interest rates have begun to decline, and this has caused bond prices to rise fairly aggressively. We can see this in the chart above. This could have investors beginning to wonder if now may be a good time to purchase this fund. Let us investigate and attempt to answer this question.

About The Fund

According to the fund's website , the DoubleLine Opportunistic Credit Fund has the primary objective of providing its investors with a very high level of current income along with the potential for capital appreciation. That is not an atypical objective for a bond fund due to the simple fact that bonds are by their nature income vehicles. An investor purchases a bond at face value, collects a regular stream of income via the bond coupons, and then receives the face value back when the bond matures. As such there are no net capital gains over a bond's lifetime. In addition, a bond has very limited potential for long-term capital appreciation for reasons that I explained in a previous article .

Nevertheless, the DoubleLine Opportunistic Credit Fund's objectives and strategy specifically claim that this fund is seeking a combination of current income and capital appreciation. Per the website:

The Fund will seek to achieve its investment objective by selecting investments for their potential to provide high current income, growth of capital, or both. The Fund may invest in debt securities and income-producing investments of any kind, including mortgage-backed securities (residential and commercial), asset-backed securities, U.S. Government securities, corporate debt, international sovereign debt, and short-term investments.

It is hard to see how any of these securities can provide growth of capital. After all, the only way to get bond prices to go up is by lowering interest rates, and there is a limit to how low-interest rates can go. It might be that the fund will attempt to purchase bonds when interest rates are high and then hold them while interest rates decline, but otherwise, it is very difficult to see how it can possibly achieve its goal of purchasing investments with the potential to provide growth of capital unless it includes common equities or convertible securities in its portfolio.

The above description implies that this fund invests solely in different types of bonds and debt securities, however. CEF Connect states the same thing, as its asset allocation chart for this fund states that the DoubleLine Opportunistic Credit Fund's assets consist of 97.19% bonds alongside a very small allocation to cash:

CEF Connect

We do see an exceptionally small 0.06% allocation to common stock, but that is such a small allocation that it is hardly worth discussing. Thus, this is clearly a bond fund as the description above suggests. This is not really a surprise considering that this is a DoubleLine fund. However, it is very difficult to understand why this fund is mentioning its efforts to invest in securities with the potential capital growth if it is a bond fund.

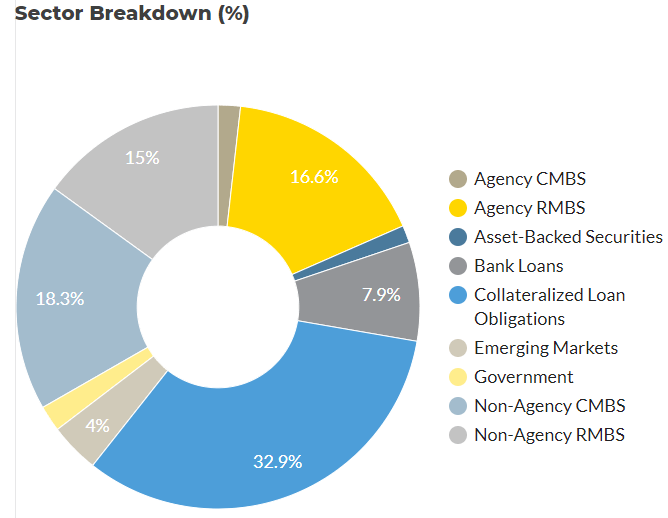

The DoubleLine Opportunistic Credit Fund is very well-diversified in terms of the types of bonds that it invests in. We can see this here:

{kind=link}

One very interesting thing to note here is that the fund has a 32.9% allocation to collateralized loan obligations. In addition, we see a 7.9% allocation to bank loans. Unlike most traditional bond issues, these securities are very frequently floating-rate bonds. There are some advantages to floating-rate securities in today's market, such as the fact that they are quite resistant to changes in interest rates.

As we saw in the introduction to this article, the Bloomberg U.S. Aggregate Bond Index was devastated over the past three years as rising interest rates burst a bubble that was created by the "free money" policies of the pandemic era. These policies had been keeping bond yields at some of the lowest levels that we have seen in history, and by extension keeping prices high. That index consists of traditional fixed-rate bonds. In contrast, floating-rate securities were basically unaffected by the reversal of the zero-interest rate policy. As we can see here, the iShares Floating Rate Bond ETF ( FLOT ) has been almost perfectly flat in comparison to the Bloomberg U.S. Aggregate Bond Index:

{kind=link}

The DoubleLine Opportunistic Credit Fund undoubtedly benefited from this as well, as the presence of these securities in its portfolio should have protected the fund from the worst of the effects of the bursting of the bond bubble. After all, if part of its portfolio maintains stable prices regardless of interest-rate movements, then the fund's losses as bond prices fell would not be as high as they would have been if the fund were fully invested in traditional fixed-rate bonds. The reverse is also true, however, as the fund will probably not benefit as much as it would if it had a standard bond portfolio during periods of falling interest rates. This is something that could be very important over the coming year as the Federal Reserve is widely expected to reduce interest rates over the course of 2024. The fact that 40.8% of the fund's portfolio is invested in securities that are almost certainly floating rate could hold back its potential performance.

As regular readers are no doubt aware though, I believe that the market is far too optimistic about the near-term trajectory of interest rates. This suggests that traditional fixed-coupon bonds are currently overpriced and that a mixture of both floating-rate and fixed-rate securities is appropriate for today's markets.

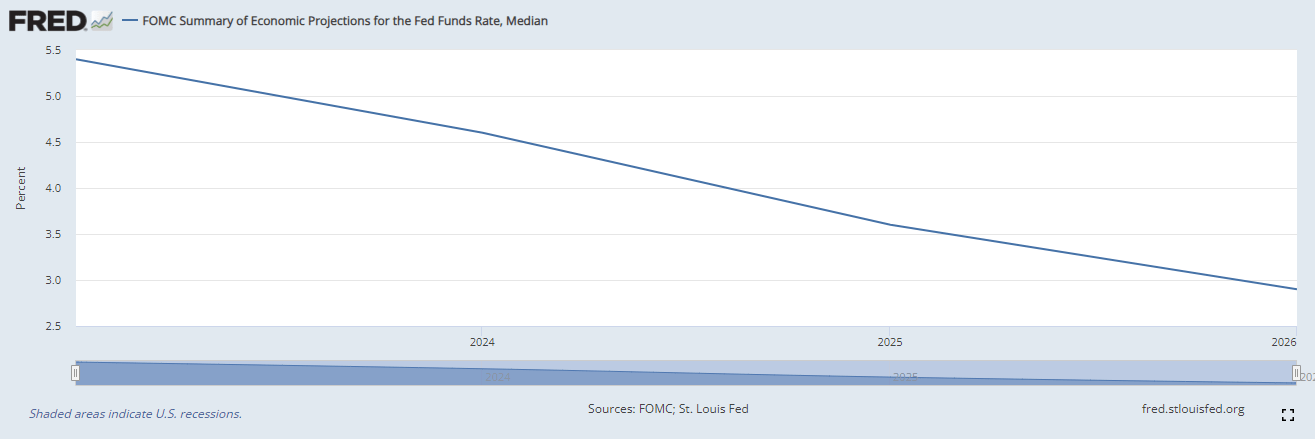

First, we need to consider that the market is currently projecting six interest rate cuts of 25 basis points each by the end of next year. This means that the market is expecting that the federal funds rate will be at 4% at the end of 2024 and is pricing bonds accordingly. That is a much lower federal funds rate than the members of the Federal Open Market Committee, which sets the federal funds rate, expect. As we can see here, the members of this committee expect either two or three 25-basis point cuts next year, which puts the federal funds rate median expectation of 4.6% at the end of 2024:

{kind=link}

If the projections by the Federal Reserve itself prove to be more accurate than those of the market, the price of fixed-coupon bonds will fall from today's levels. That will result in losses for anyone who is purchasing bonds today. This could actually happen by March, as the market is expecting that the first rate cut will occur at the March meeting. There could be some reasons to believe that there will not be a cut in interest rates that early in the year, considering that the core consumer price index is still at 4%. If there is no cut to the federal funds rate at that meeting, then there will almost certainly be a correction in bonds within the next three months.

Floating-rate securities should be relatively unaffected by such a situation though, due to the fact that these securities always deliver a yield that is competitive with the market interest rate and newly-issued securities. As such, it may be a good idea to hold some of these securities as a form of protection against an overly optimistic market. The DoubleLine Opportunistic Credit Fund thus looks reasonably well-positioned regardless of what the Federal Reserve does next year. This is a much better position to be in than trying to gamble on central bank policy and ending up on the wrong side of the trade.

Leverage

As is the case with most closed-end funds, the DoubleLine Opportunistic Credit Fund employs leverage as a means of boosting the effective yield and total return from its portfolio. I have explained how this works in a number of previous articles. To paraphrase myself:

In short, the fund borrows money and then uses that borrowed money to purchase bonds and other income-producing assets. As long as the yield that the fund receives from the purchased assets is higher than the interest rate that it needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will normally be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that a fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like a fund's leverage to exceed a third as a percentage of its assets for this reason.

As of the time of writing, the DoubleLine Opportunistic Credit Fund has leveraged assets comprising 16.85% of its portfolio. That is an incredibly low level of leverage for a fixed-income fund, and this is likely the reason why this fund's distribution yield is a bit lower than some other funds that employ a similar strategy. In other words, the fund could probably increase its leverage in order to control more assets and boost the effective yield while still being well within the safe range. That would make the fund a bit more volatile though, which may be problematic if bond prices decline next year.

Overall, investors should not have to worry about the fund's leverage today. In fact, even highly risk-averse investors should be quite comfortable.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the DoubleLine Opportunistic Credit Fund is to provide its investors with a very high level of current income. In pursuance of this objective, the fund purchases a variety of bonds and debt securities that primarily deliver their returns through direct payments to their investors. In this case, it is the fund that is collecting those payments. The fund pools all of the money that it collects from these bonds and combines it with any profits that it manages to make by trading securities as their prices change in the market. The fund then pays all of this money out to its investors, net of its own expenses. When we consider that bonds have very respectable yields in today's monetary environment and that the fund is adding trading profits on top of this, we can assume that this strategy would allow this fund to pay out a very attractive yield.

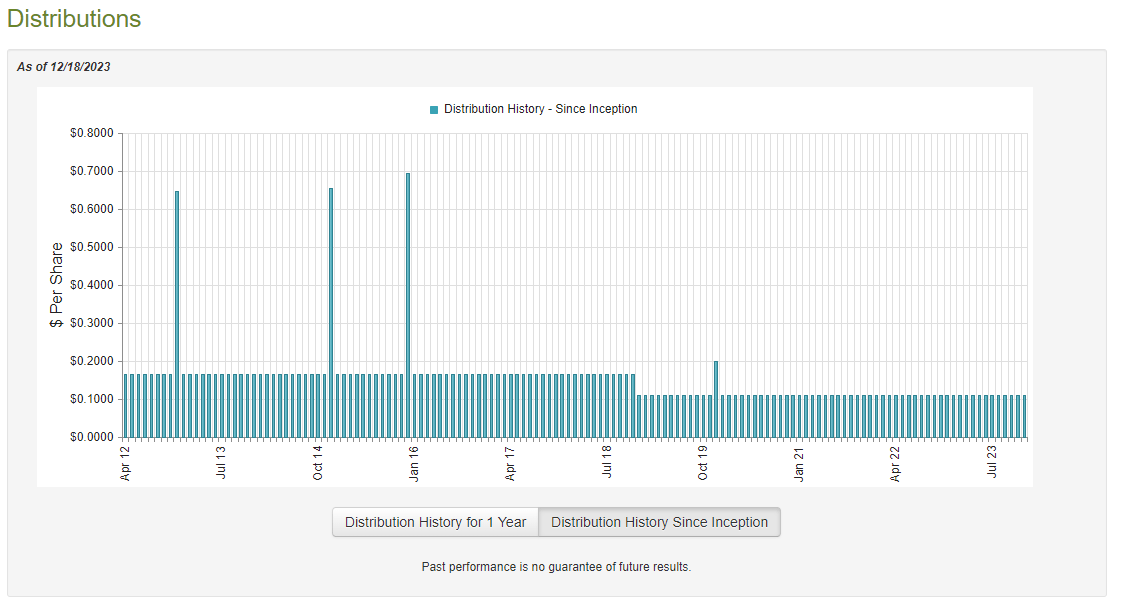

This is indeed the case, as the DoubleLine Opportunistic Credit Fund pays a monthly distribution of $0.11 per share ($1.32 per share annually), which gives it an 8.57% yield at the current price. This is nowhere near as attractive as the yield possessed by some other fixed-income funds, but it is still well above the current rate of inflation and can still provide a respectable level of income when compared to common stocks or U.S. Treasuries. Unfortunately, the fund's distribution history has not been as attractive as we might like to see:

{kind=link}

As we can quickly see, the fund had to cut its distribution a few years ago, but it has otherwise been remarkably consistent. This is one of the few fixed-income funds that did not have to cut its distribution in response to the rout in bond prices back in 2022, which is curious. We should investigate this situation as it seems strange that this fund was able to accomplish a task that its peers were unable to pull off. Then again, the fact that this fund changes its portfolio between fixed-rate bonds and floating-rate securities gives it an advantage that some funds lack.

Naturally, though, the most important thing for our purposes today is how well the fund can sustain its current distribution. After all, anyone purchasing the fund today will receive the current distribution at the current yield and will not be affected by events that occurred in the past. Therefore, let us have a look at the fund's current finances and see how well it is covering its distribution.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on September 30, 2023. This is one of the newest financial reports that we have available to us from any closed-end fund, and it covers a period of time that should give us an idea of how well the fund handles both good and bad markets. After all, both the latter few months of 2022 and the summer of 2023 were bear markets for fixed-income assets. During each of these two periods, bond prices were declining, and interest rates were rising. That may have handled the fund some unrealized losses. However, the first half of 2023 was quite strong as investors were front-running an expected Federal Reserve pivot, just as they are now. During that period, bond prices were rising, and this may have given the fund the opportunity to earn some short-term profits by selling bonds as their price rose. This report should give us a good idea of how well the fund handled each of these different environments.

During the full-year period, the DoubleLine Opportunistic Credit Fund received $11,117,145 in interest and $237 in dividends from the assets in its portfolio. This gives the fund a total investment income of $11,117,382 during the period. The fund paid its expenses out of this amount, which left it with $4,826,622 available for shareholders. As might be expected, that was nowhere close to enough to cover the fund's distributions, as the fund distributed a total of $21,477,585 over the full-year period. At first glance, this is almost certainly going to be very concerning, as we would generally like to see any debt-focused closed-end fund cover its distributions out of net investment income.

However, the fund does have other methods through which it can obtain the necessary money to cover its distributions. For example, it might have been able to exploit fluctuations in bond prices to earn some short-term trading profits. Realized capital gains such as these are not considered to be investment income for accounting or tax purposes, but they obviously do represent money coming into the fund that can be distributed to the fund's shareholders. This fund managed to have a considerable amount of success at this task during the period, as it reported net realized losses of $3,776,695 but this was offset by $13,859,226 net unrealized gains. Ultimately though, the fund still failed to cover its distribution solely out of investment profits, as its net investment profits totaled $14,909,153 over the full-year period:

Fund Annual Report

That was not enough to cover $21,477,585 in distributions. However, the fund's net assets did still increase during the period because the fund conducted a capital raise that brought in $11,667,601 of new money. It used that new money to partially fund the distribution. Overall, the fund's net assets only increased by $5,419,896 after accounting for all inflows and outflows during the period.

It is not sustainable long-term to be paying a fund's distribution out of new investment capital. We should keep an eye on this situation, as we will want the fund to correct it and fully cover the payout from its own investment capital. After all, eventually, new investors will stop funding a distribution that relies on new capital always being available.

Valuation

As of December 18, 2023 (the most recent date for which data is currently available), the DoubleLine Opportunistic Credit Fund has a net asset value of $14.79 per share but shares currently trade for $15.37 each. This gives the fund's shares a 3.92% premium on net asset value. This is a lot higher than the 1.65% premium that the shares have averaged over the past month. It also explains why the fund's yield is a bit lower than some of its peers, as the premium results in a lower yield given a similar portfolio performance.

Overall, the current price seems very high. As regular readers are certainly well aware, I generally dislike ever paying a premium to obtain a fund. The fact that this one is higher than normal reduces its appeal further.

Conclusion

In conclusion, the DoubleLine Opportunistic Credit Fund looks like a pretty solid debt fund. The fund has relatively low leverage, which should reduce its volatility compared to peers, and the fact that just under half of the portfolio is invested in floating-rate securities should improve its safety even more. There is a very real risk that fixed-rate securities are overpriced right now, so this fund's allocation to floating-rate bonds should partially offset that risk. The distribution looks challenged though, as the fund did fail to cover it with investment profits and had to resort to selling new shares over the past year. When we combine that with the fact that this fund is selling at a premium, there are some real concerns here. The fund does appear to be very well-managed, though, and it might be worth buying at a discount if it can improve the distribution coverage issue.

For further details see:

DBL: This Is A Decent Bond Fund, But Not When It Is At A Premium