KMLM - DBMF And KMLM: 2 Alternative ETFs We Simply Can't Dislike

Summary

- Alternative investments are supplemental, usually more sophisticated, investing strategies to traditional long-only positions in stocks, bonds, and cash.

- Alternative investments include investments in five main categories: hedge funds, private capital, natural resources, real estate, and infrastructure.

- Most retail investors face all sorts of issues/restrictions that prevent them from investing in hedge funds. The stock market offers a couple of by-passes through unique ETFs.

- While the track record of these hedge-fund-like ETFs is fairly short, it does look as if they're successful in mitigating risks while enhancing returns.

- There's a thin line between offering a valuable alternative investment strategy to turning this very same investment strategy into a too aggressive, potentially wild, approach that may outweigh its benefits.

Background

During the long Labor Day weekend, one of our subscribers has asked us about iM DBi Managed Futures Strategy ETF ( DBMF ), and I must admit that until then I had never heard of this security before.

As it turned out, there are less than a handful of exchange-traded funds ("ETFs") that are offering what DBMF does, and the closest one we found is KFA Mount Lucas Strategy ETF ( KMLM ).

If you look at the performance of DBMF and KMLM this year and compare it to the performance of the overall market ( SPY ), it looks as if these ETFs are some kind of magic.

- How these ETFs are operating and what exactly do they invest in?

- How do they manage to outperform the market by that much?

- Do they come with a much higher risk than the overall market?

- Is it safe to allocate a large portion of your portfolio into such ETFs?

These are some of the questions that are likely going through your mind right now.

In this article we explain what these ETFs are doing, compare the two ETFs, and explain what are the advantages and disadvantages of investing in such instruments.

Overview

Let's start with understanding an important term - "Commodity Trading Advisor" ("CTA"):

A commodity trading advisor ("CTA") is an individual or firm that provides personalized advice regarding the buying and selling of futures contracts, options on futures, and retail off-exchange forex contracts or swaps.

Advisors who give such advice are required to be registered as a CTA by the National Futures Association ("NFA"), the self-regulatory organization for the derivatives industry. [ Source ]

Based on DBMF most recent factsheet :

The SG CTA Index is an index published by Société Générale that is designed to reflect the performance of a pool of Commodity Trading Advisor ("CTAs") selected from larger managers that employ systematic managed futures strategies. The index is reconstituted annually.

The SG CTA Index is designed to track the largest 20 (by AUM) CTAs and be representative of the managed futures space. Managers must meet the following criteria: Must be open to new investment, Must report returns on a daily basis. The CTA Index is equally weighted, and rebalanced and reconstituted annually [ Source ]

- The iMGP DBi Managed Futures Strategy ETF seeks long-term capital appreciation.

- Targets pre-fee returns of the largest Commodity Trading Advisor Hedge Funds by assets

- A strategy designed to seek to perform regardless of the direction of equity markets

- Exposure built through some of the most liquid US-based futures contracts

- Optimized portfolio turnover through weekly rebalancing frequency and low transaction costs

Based on KMLM's most recent fact sheet :

KMLM is benchmarked to the KFA MLM Index, which consists of a portfolio of twenty two liquid futures contracts traded on U.S. and foreign exchanges. The Index includes futures contracts on 11 commodities, 6 currencies, and 5 global bond markets. These three baskets are weighted by their relative historical volatility, and within each basket, the constituent markets are equal dollar weighted.

The KFA MLM Index ETF seeks to provide investment results that, before fees and expenses, track the price and yield performance of the MLM Index EV. The Index is a modified version of the MLM Index, which is an index constructed of a portfolio of commodity, currency, and global fixed income futures contracts traded on U.S. and foreign exchanges using trend following methodology.

KMLM Features:

- Access to managed futures through a liquid and low-cost ETF structure

- Managed futures are considered alternative investments and may provide additional diversification and decrease volatility when included within traditional equity/bond portfolios

- A potential hedge on equity, bond, and commodity risk

After all of these complicated words, allow us to put this in very simple words: These ETFs are basically tracking the positioning of some of the most sophisticated hedge funds out there, while using instruments (derivatives, options, futures) that are either not accessible nor being used by the average retail investor.

Under normal market conditions, the Sub-Advisor will seek to achieve Fund volatility of 8-10% on an annual basis , which refers to the approximate maximum amount of expected gains or losses during a given year expressed as a percentage of value.

Investment Strategies

This is coming straight from DBMF's Prospectus (emphases ours):

The Fund is a non-diversified, actively-managed exchange-traded fund ("ETF") that seeks to achieve its objective by: (i) investing its assets pursuant to a managed futures strategy (described below); (ii) allocating up to 20% of its total assets in its wholly-owned subsidiary (the "Subsidiary"), which is organized under the laws of the Cayman Islands , is advised by the Sub-Advisor (as defined herein), and will comply with the Fund's investment objective and investment policies; and (iii) investing directly in select debt instruments for cash management and other purposes.

The Fund's managed futures strategy employs long and short positions in derivatives, primarily futures contracts and forward contracts, across the broad asset classes of equities, fixed income, currencies and, through the Subsidiary, commodities .

Fund positions in those contracts are determined based on a proprietary, quantitative model - the Dynamic Beta Engine - that seeks to identify the main drivers of performance by approximating the current asset allocation of a selected pool of the largest commodity trading advisor hedge funds ("CTA hedge funds"), which are hedge funds that use futures or forward contracts to achieve their investment objectives. The Dynamic Beta Engine analyzes recent (i.e., trailing 60-day) performance of CTA hedge funds in order to identify a portfolio of liquid financial instruments that closely reflects the estimated current asset allocation of the selected pool of CTA hedge funds, with the goal of simulating the performance, but not the underlying positions, of those funds. Based on this analysis, the Fund will invest in an optimized portfolio of long and short positions in domestically-traded, liquid derivative contracts.

The Dynamic Beta Engine uses data sourced from (1) publicly available U.S. futures market data obtained and cross-checked through multiple common subscription pricing sources, and (2) public CTA hedge fund indexes obtained through common subscription services and cross-checked with publicly available index information. The Sub-Advisor relies exclusively on the Dynamic Beta Engine and does not have discretion to override the model-determined asset allocation or portfolio weights . The Sub-Advisor will periodically review whether instruments should be added to or removed from the model in order to improve the model's efficiency. The model's asset allocation is limited to asset classes that are traded on U.S.-based exchanges . Based on this analysis, the Fund will invest in an optimized portfolio of long and short positions in domestically-traded, liquid derivative contracts selected from a pool of the most liquid derivative contracts, as determined by the Sub-Advisor.

This is coming straight from KMLM's Summary Prospectus (emphases ours):

The Fund seeks to achieve its goal by investing in commodity, currency, and global fixed income futures contracts traded on U.S. and foreign exchanges that are the same as or similar to those included in the Index.

The Index is a modified version of the MLM Index, which is an index that measures the performance of a portfolio of commodity, currency, and global fixed income futures contracts traded on U.S. and foreign exchanges using a trend following methodology. The Index determines weightings of these three types of futures contracts by the relative historical volatility of each type of futures contract as determined by the MLM Index Committee . Within each type of futures contract, the underlying constituent markets are equal dollar weighted.

The Index will roll futures contracts forward on a market by market basis as each constituent market nears expiration. The selection of the constituent markets occurs annually. The constituent markets of the futures contracts for the Index currently consist of the following commodities (corn, crude oil, copper, gold, heating oil, cattle, natural gas, soybeans, sugar, wheat and gasoline), currencies (British pound, Canadian dollar, Australian dollar, Euro, Japanese Yen, and Swiss francs), and global bond markets (Canadian government bond, Euro bund, Japanese government bond, Long gilt and Ten-year Treasuries) . Constituent markets are traded both long and short based on each market's trading signals.

The Index evaluates market trading signals on a daily basis and rebalances on the first day of the month. In addition, the Index has a target average annualized volatility of 15% over time .

The Fund will invest in futures contracts on commodities, currencies and global bond markets. The Fund will utilize a subsidiary (the "Subsidiary") for purposes of investing in futures contracts on commodities. The Subsidiary is a corporation operating under Cayman Islands law that is wholly-owned and controlled by the Fund . The Subsidiary is advised by the Fund's investment adviser, Krane Funds Advisors, LLC ("Krane" or "Adviser") and is sub-advised by Mount Lucas Index Advisers LLC, the Fund's sub-adviser ("MLIA" or "Sub-Adviser"). The Fund's investment in the Subsidiary may not exceed 25% of the value of its total assets (ignoring any subsequent market appreciation in the Subsidiary's value), which limitation is imposed by the Internal Revenue Code of 1986, as amended, and is measured at the end of the quarter.

Once again, to make things simple (and ignoring immaterial differences in the exact figures): Both funds are investing in all asset-classes (buy Crypto), both funds trade long and short, both funds are aiming for fairly-low annualized volatility, and both funds are using a subsidiary in Grand Cayman for some (up to 1/4) of the activity.

The main differences are the different benchmarks (although it's safe to assume that they both call for quite similar positioning, at least directionally), and the use of different models (though with a similar "follow the herd" mentality).

Nonetheless, as you may well understand, these are fairly similar concepts.

Fees & Risks

The similarity continues here too.

When it comes to fees, the all-in annual cost associated with holding any of the two ETFs is almost the same.

| DBMF |

| KMLM |

| Management Fees |

| 0.85% |

| 0.89% |

| Distribution and/or Service (12b-1) Fees |

| 0.00% |

| 0.00% |

| Interest and Dividend Expenses |

| 0.10% |

| 0.00% |

| Acquired Fund Fees and Expenses |

| 0.00% |

| 0.03% |

| Total Annual Fund Operating Expenses |

| 0.95% |

| 0.92% |

Same goes for the risks associated with holding DBMF and/or KMLM.

As is the case with most funds, both DBMF and KMLM are covering any potential risk that may arise while holding any type of fund.

Most of these risks aren't unique to DBMF or KMLM and we see no reason to state the obvious.

Nonetheless, here are a few types of risks that investors in these ETFs should be minded of:

- Commodity and Commodity-Linked Derivatives Risks. Since a relatively large part of the investments involves commodities, and since this asset-class is more volatile than other asset-classes, investors should take the extra volatility/risk into consideration.

- Currency Risk. This is true to any pool that has a non-USD exposure, but DBMF and KMLM are way more active in currencies than the average fund, making the currency risk greater than it may normally be.

- Subsidiary Investment Risk. While the use of a tax-haven jurisdictions is a common practice among hedge funds/proprietary trading platforms, and although we don't view this as something that should be a deal-breaker, whenever there a more complicated legal structure that involves entities incorporated outside of the main country/jurisdiction of activity - (at least) a bit of an extra risk is being added to the mix.

- Derivatives Risk. Goes without saying in the case of a fund that its entire activity involves derivatives and leverage.

- Liquidity Risk. That goes to both the instruments used by the fund (for trading) as well as for the ease of going in and out of the fund. In case of a major distress in the markets, funds usually have the option to suspend redemptions and the smaller the fund - the higher the risk of this potentially happening (even if the risk, for itself, is quite remote).

- High Portfolio Turnover Risk. Trading costs aren't part of the official fees and so the higher the turnover - the more significant the trading costs become.

5 Main Advantages

1) A non-correlated strategy to the main asset classes.

This is especially beneficial in a year like 2022, which is on pace to become the worst year for traditional portfolios (i.e. 40%-60% stocks, 40%-60% bonds) on record.

B.I.G

2) Playing both Long and Short sides.

Many people fear short selling, but we (as occasional short sellers ourselves) believe that shorting is a great way to mitigate risk of a portfolio, and it doesn't mean that you're "going wild" (as many people wrongly assume).

There's no guarantee that short selling would be profitable, but think of it this way: Had I offered you a car that can only move forward vs a car that can also move backwards (reverse), which car would you choose to buy?

3) Personally, whenever there's (out of the box) thinking and (investing) creativity - I tend to think that better things may happen compared to when the investment strategy is 100% long only, 100% of time, with no flexibility to reduce/increase risk based on the macro landscape/market outlook.

4) Principally, these are hedge funds wearing a costume of ETFs. If you don't like hedge funds - there's no reason for you to like these ETFs. However, if you like hedge funds (at least conceptually, i.e. adopting a more dynamic and sophisticated investment strategy) but you have no access to those (mostly due to the high minimum amount that they usually require as an initial investment) and/or you don't want to pay the high fees that are usually associated with hedge funds - these ETFs are making hedge funds accessible to you.

5) It's hard to argue with success.

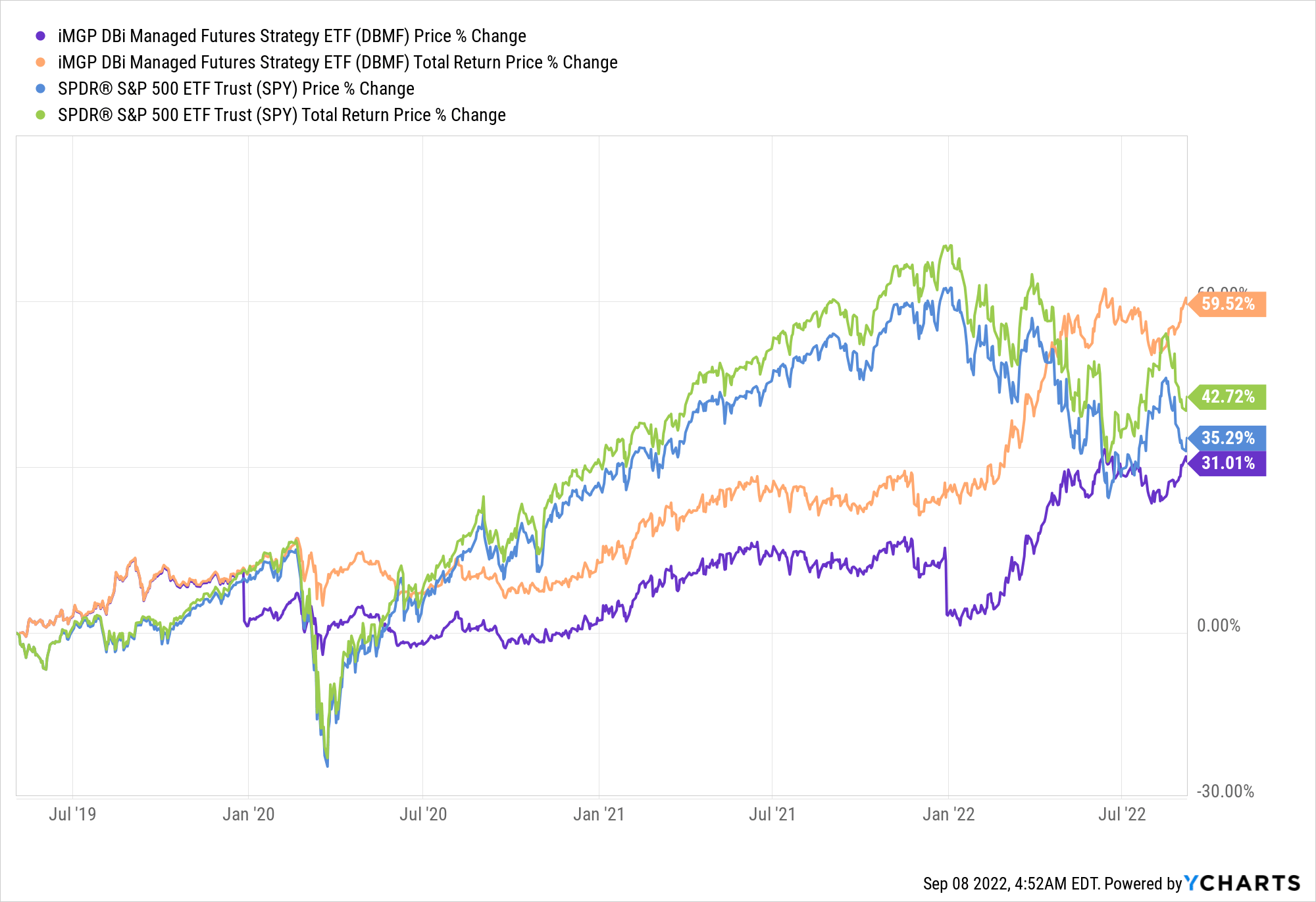

DBMF since inception (May 7, 2019) compared to SPY: Higher return, lower volatility/risk.

{kind=link}

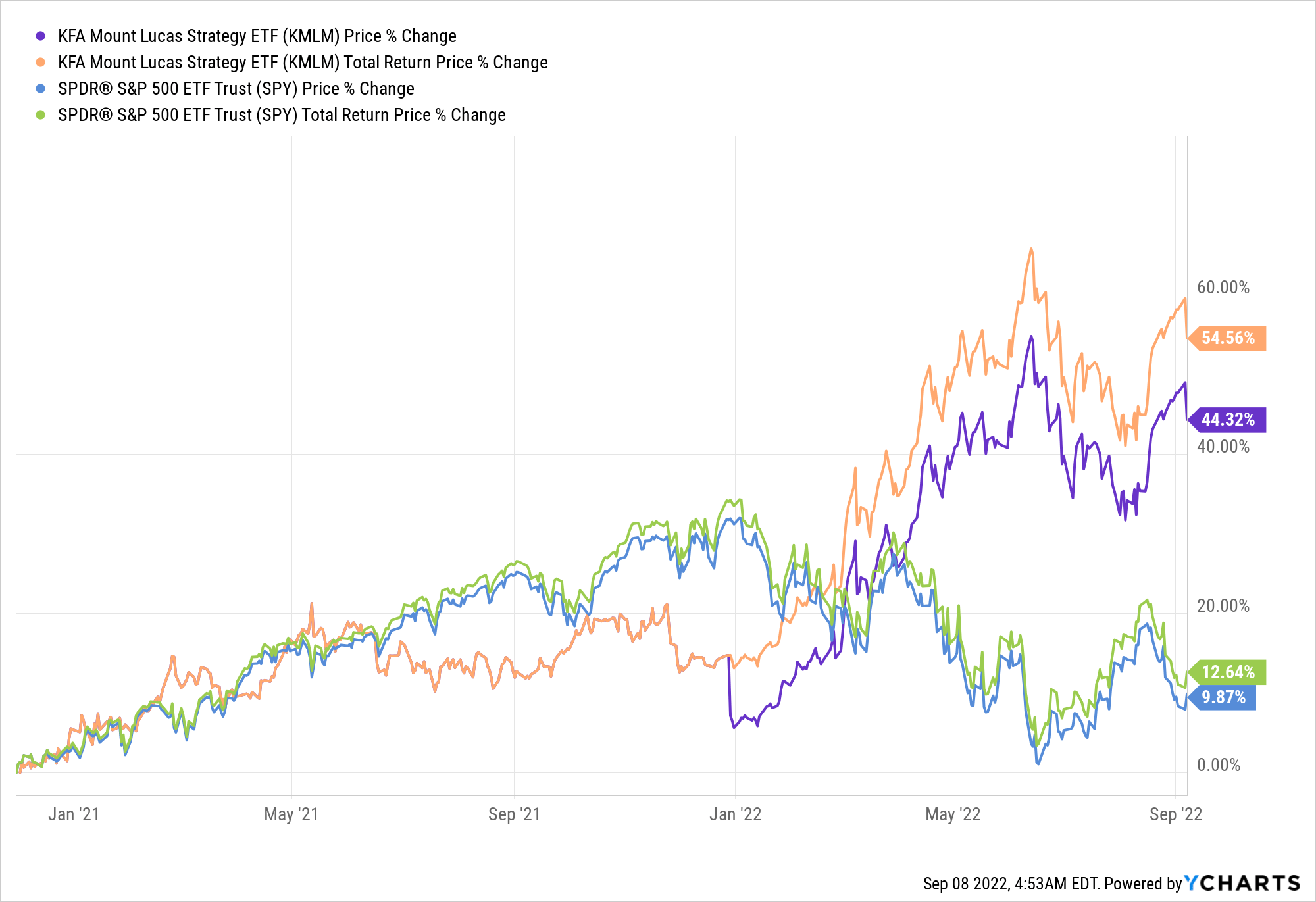

KMLM since inception (Dec. 2, 2020) compared to SPY: Higher return, lower volatility/risk.

{kind=link}

DBMF vs KMLM

1) Both ETFs are fairly young, however DBMF is trading publicly about twice as long as KMLM is.

2) DBMF is 3x as big as KMLM is. Size matters because size translates into better liquidity, potential better trading terms, and (general) lower costs.

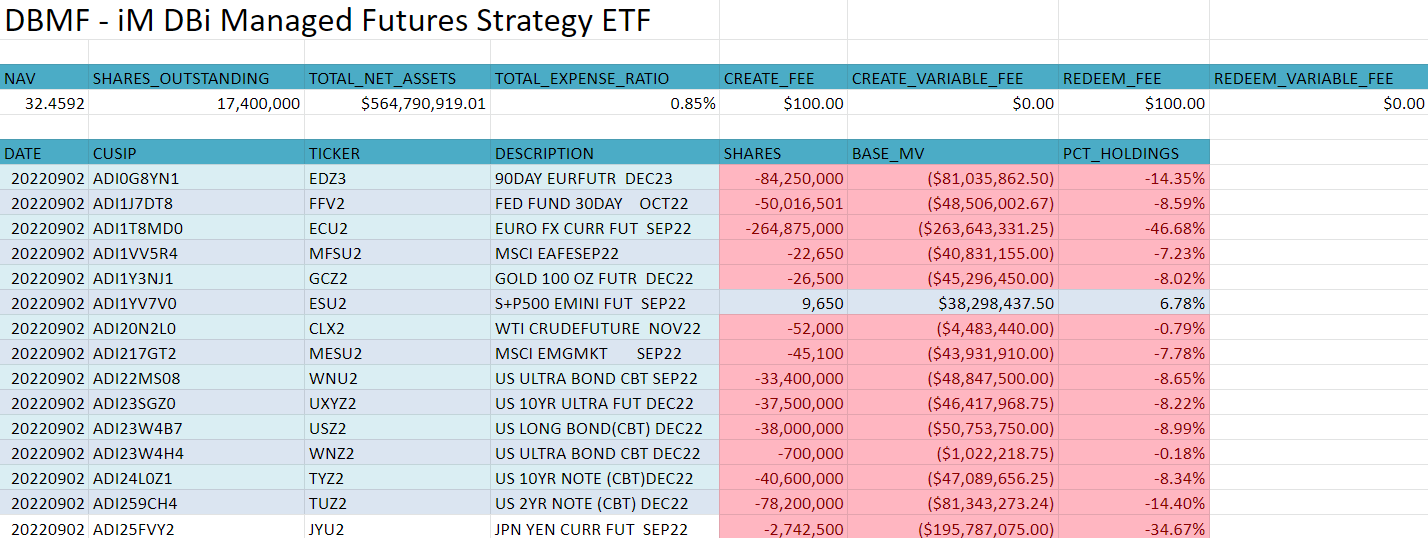

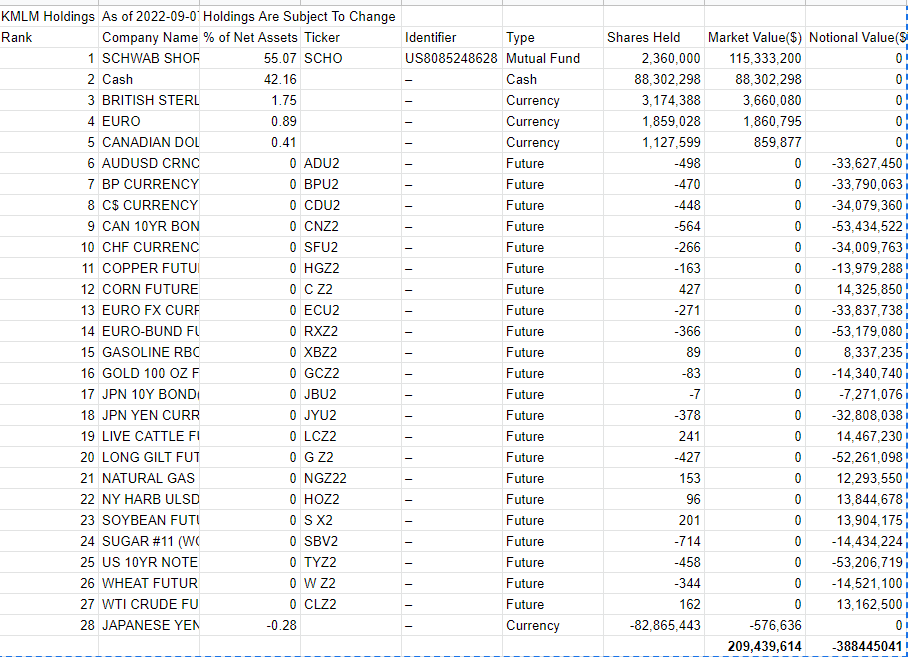

3) It may not be easy to see but based on us checking both funds' holdings we can say that both are running a similar leverage and they also take more or less the same positioning.

They keep their assets in cash and cash equivalents as collaterals and they are almost entirely short in a size of about 180% of their respective NAV.

The main differences are the weightings (used for each holding) and what they choose to be long.

DBMF is currently only long e-mini futures on the S&P 500.

{kind=link}

KMLM, on the other hand, is long some types of agriculture (e.g. corn, live cattle, soybean) and energy (gasoline, natural gas, WTI crude oil).

{kind=link}

KMLM might seem like it's more long than DBMF, however in terms of leverage and net short it's about the same as DBMF.

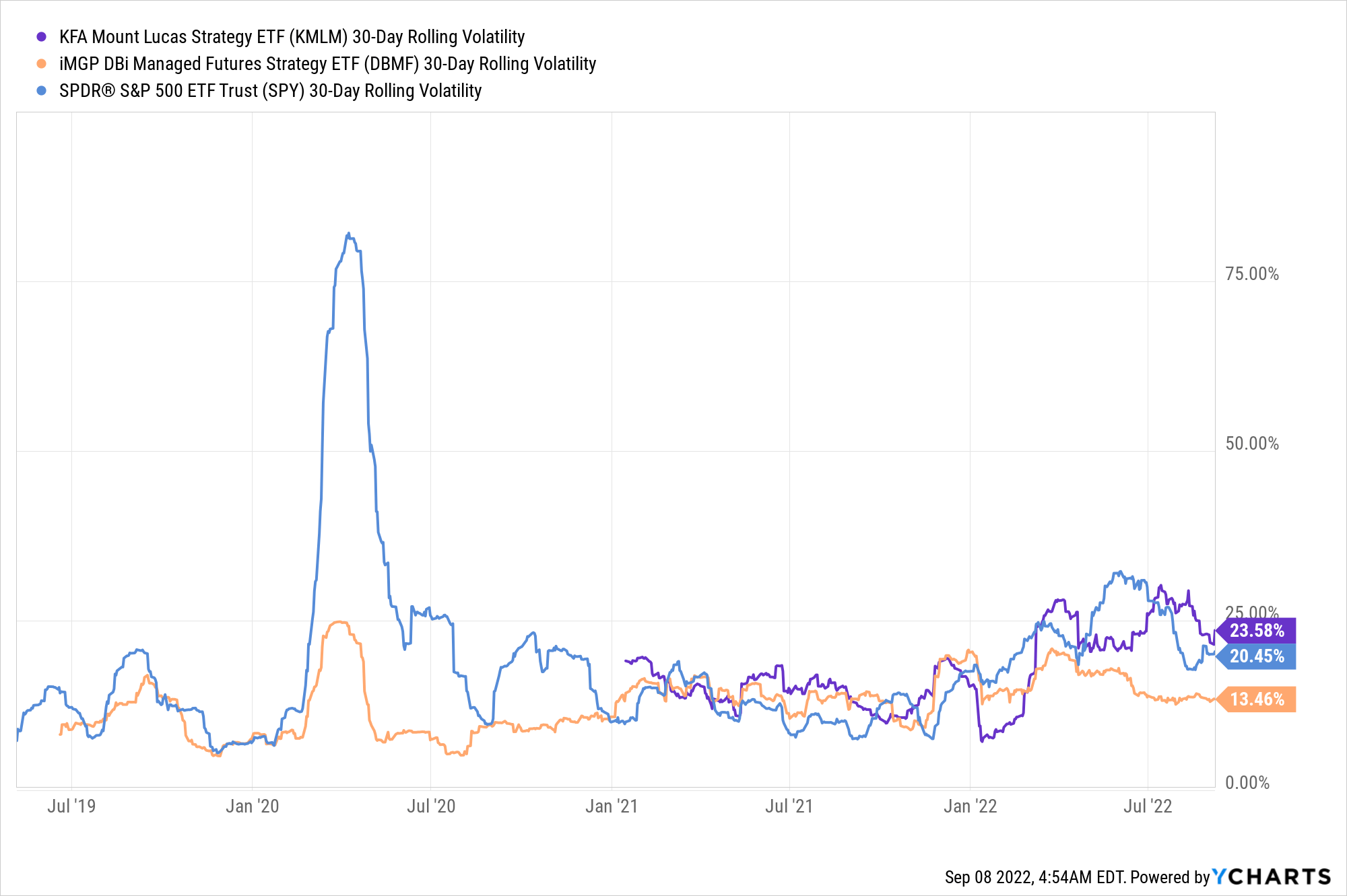

As a matter of fact, KMLM is more volatile than DBMF, and this is likely one of the reasons it has outperformed since its inception date.

Bottom Line

We like these ETFs.

We think they provide a different, refreshing, approach that most retail investors have no access to and/or can't afford outside of these ETFs.

Therefore, this alternative investing approach is (for us) a welcome investing approach.

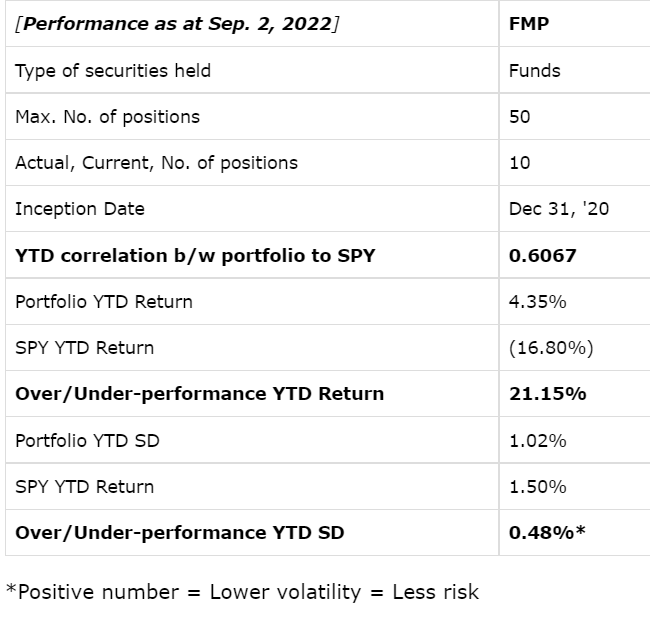

In many ways, they remind us of our Funds Macro Portfolio ("FMP") which also uses long and short positioning, across the same asset-classes, potentially (but not necessarily) employing leverage, mitigating risk, while attempting to outperform the market.

Taking into consideration what we believe in and how we operate, we can't dislike these ETFs.

Similar to DBMF and KMLM, our FMP has also managed to significantly outperform SPY so far this year. Nonetheless, unlike these ETFs, we are way less aggressive in terms of both direction (for/against certain asset-class/es) as well as size (not leaning so heavily into one side).

{kind=link}

We have restrictions regarding how much we can be long, short, or net - no matter how bullish, bearish, or neutral we are. Moreover, we wouldn't put all the eggs in one basket (e.g. all-in short) as these ETFs are willing to do.

More than anything, we're very minded of risk, and so are these ETFs (at least conceptually). For that reason, we can very much appreciate that the two ETFs are managing to be as or even less volatile than SPY is (Same goes for our FMP which is significantly less volatile than SPY).

{kind=link}

Note that over recent months, DBMF has recorded significantly lower volatility compared to KMLM, but KMLM has significantly outperformed. So clearly, there's some trade-off in here between risk and performance.

Delivering a higher return while taking a lower risk is the "holy grail" of investing, and the two ETFs (as well as our FMP) are not only aspiring for this, but (as evident) capable of it.

At the moment, DBMF (and to a lesser extent KMLM) looks to be positioned very aggressively. Aside of being ~6.8% long SPX, everything else (>180% of DBMF's AuM) is short - across the (asset-class) board: Fed Funds, UST2Y, UST10Y, long-duration bonds, EUR, JPY, EM, Gold, even oil (a bit)...

As long as this is working - everybody is happy, but the question is: What if things go the other way, all at once, in an unexpected way?

Our FMP is currently about 50% net long (which is the lowest level we normally run). DBMF and KMLM are about 180% net short, with very little long positions hedging these shorts.

If suddenly the U.S. dollar starts weakening, yields fall, and commodities rise - these ETFs might lose a lot of steam, very rapidly. Of course, they can change their positioning - and perhaps they will - but principally, there's a risk of a quick U-turn that may cause severe losses (largest drawdown since inception they report on is -5.04%, which is a very small one taking into consideration what has happened in Q1/2020).

Another concern is that in 2020 (in which KMLM wasn't yet launched), it doesn't seem like DBMF responded (at all) to the COVID shock. The return in 2020 is almost a flat line throughout the year (point to point). So Kudos for them for losing way less in Q1 but where were you then after?

All in all, we like these ETFs, because we always like/prefer managers that think and are creative over managers that simply copy/follow a path without bringing much of their own (brain) to the table. Moreover, the results show that they're doing a decent job and certainly are very minded of risk which for us is the most important aspect.

We wouldn't bet the farm on any of these ETFs, but we certainly think they deserve a place (allocation in the single digits) in one's portfolio as they provide a good hedge and something that traditional long-only investing strategies don't and can't deliver.

For further details see:

DBMF And KMLM: 2 Alternative ETFs We Simply Can't Dislike