DBMF - DBMF: Driving Through The Rearview Mirror

2023-03-17 12:03:05 ET

Summary

- DBMF offers access to the Commodity Trend asset class.

- DBMF's strategy works by analyzing the returns of top performing CTAs to identify trades that can replicate those performances. By design, there is a lagged effect.

- With market volatility rapidly rising to 2008/2009 levels, I think investors should consider raising cash instead of looking to CTA strategies like DBMF to save the day.

In November, I downgraded the iM DBi Managed Futures Strategy ETF ( DBMF ), as I saw the main trends the fund was betting on was inflecting and based on DBMF's methodology, it could take months before the portfolio adjusts to the new reality.

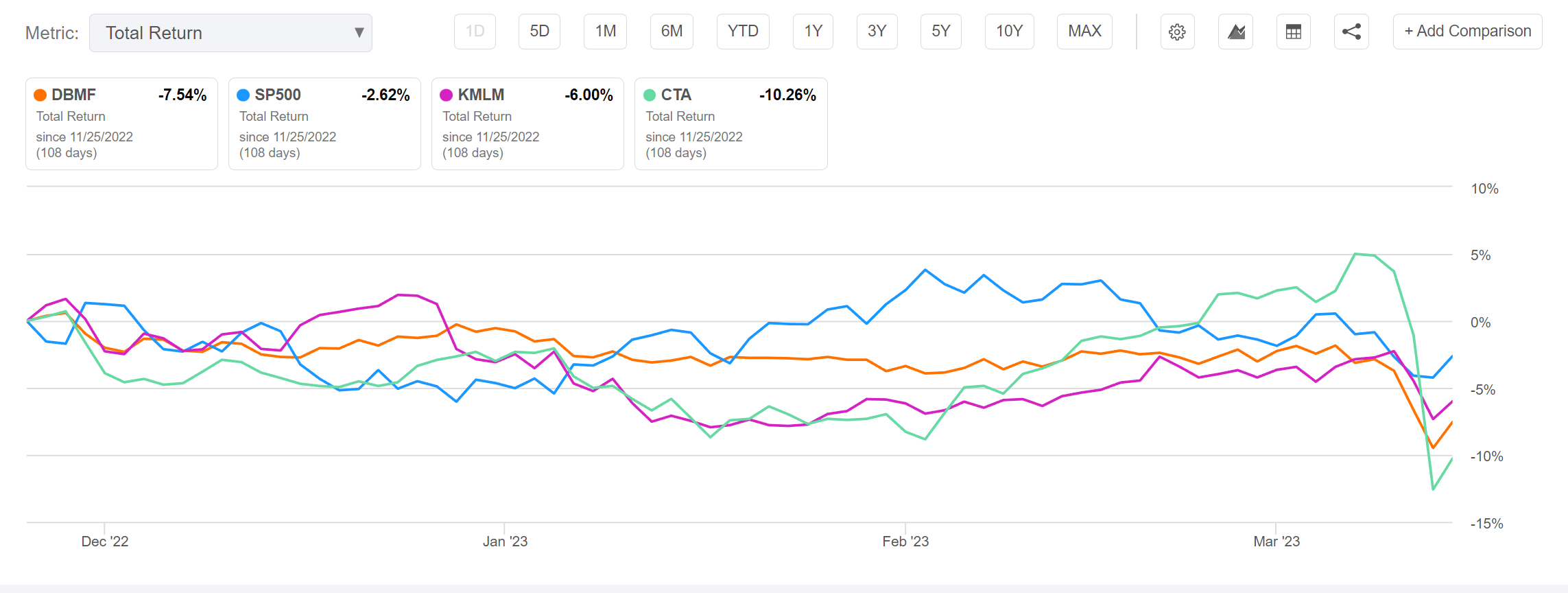

Since my downgrade, DBMF's performance has been poor, as the fund failed to latch onto any sustainable new trend. However, DBMF wasn't alone in its misery, as other CTA-based funds like the Simplify Managed Futures Strategy ( CTA ) and the KFA Mount Lucas Strategy ETF ( KMLM ) have also significantly underperformed the market (Figure 1).

{kind=link}

Figure 1 - DBMF vs. peers (Seeking Alpha)

What caused these CTA strategies to underperform and will their underperformance continue?

CTAs Need Trends

Managed Futures, or more commonly referred to as commodity trading advisor ("CTA") strategies, is a quantitative investment discipline that primarily employs trend-following or momentum strategies across a range of assets. Rather than look at 'fundamentals' like valuation or growth, CTAs are typically concerned only with 'price momentum' of the asset. CTAs are just as comfortable going 'short' an asset class as going 'long'. By being able to short, CTAs generally have low correlations to traditional portfolios and can act as a portfolio diversifier.

Why Does Trend Following Work

Trend-following / momentum investing has worked remarkably well over long periods of time, defying academic theories of efficient markets. Some possible explanations for trend-following's success could be the fact that new information takes time to be incorporated into security prices, which can lead to price trends as many investors adjust their positions with varying speed.

Furthermore, investors tend to react in a similar fashion to news and events, which can create a 'bandwagon' effect pushing winners to trend higher and losers to trend lower. Finally, investors may behave in well-defined ways to regime shifts, especially during periods of risk-off markets. For example, during market sell-offs, asset correlations tend to increase because investors reduce risk across the board, which can lead to trending prices across different asset classes.

A basic trend-following strategy is to buy an asset above a long-term 200d moving average, and short the asset below the price-trend line (Figure 2).

Figure 2 - illustrative trend following strategy (PIMCO)

The main idea to realize is that in order for CTA strategies to generate positive returns, there needs to be 'trends' they can capitalize on. Unfortunately, after trending for most of 2022, many assets globally have been caught in various forms of 'mean-reversion' or 'counter-trend' movements in the past few months, either rallying strongly like stocks, bonds, and gold, or plunging like the US dollar and crude oil (Figure 3).

{kind=link}

Figure 3 - Global assets have put in large reversals (stockcharts.com)

For CTAs, the past few months have been a terrible period, as they were first stopped out of successful 2022 trades like short the Japanese Yen, and then when they switched to a long position in those assets, they were whipped around by 2-way volatility.

Volatility Continue To Increase

Unfortunately, we appear to be entering a period of increased macro volatility, as shown by the rapid increase in the BofA Merrill Lynch MOVE Index, a measure of interest rate volatility (Figure 4). Interest rate volatility is rapidly climbing and approaching levels last seen in the Great Financial Crisis in 2008/2009.

{kind=link}

Figure 4 - Volatility is approaching 2008/2009 levels (investing.com)

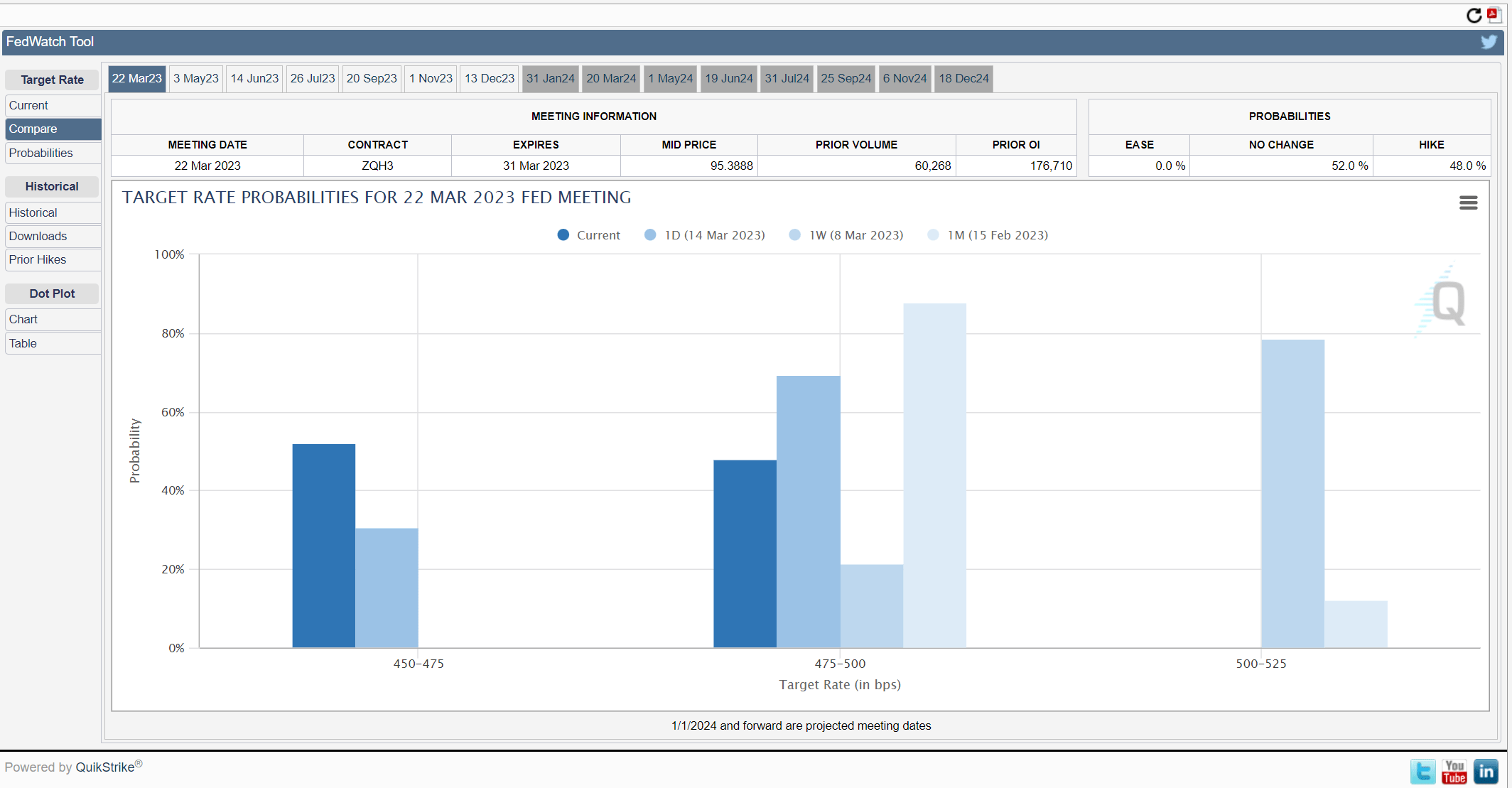

Asset classes are becoming increasingly more correlated and can flip on a moment's notice. For example, in just the past week, we have seen investors go from believing the Fed will maintain a 'higher for longer' policy by assigning a 79% probability of a 50 bps rate hike at the March FOMC meeting, to believing the Fed will 'pivot' (author's note, some traders are jokingly calling the Fed/Treasury's new lending facility BTFP, 'Buy-The-F*-Pivot' ) by assigning a 52% probability of zero rate hikes in March (Figure 5).

{kind=link}

Figure 5 - Interest rates behaving extremely erratically (CME)

The extreme interest rate volatility was caused by the shocking collapse of the regional bank SVB Financial Group ( SIVB ) last week, as well as the near collapse of Credit Suisse ( CS ) on March 15, 2023. This interest rate volatility is feeding through to other asset classes like oil (which fell 5% on March 15th) and currencies.

Increased 2-way volatility means that trend-following CTAs can easily become offsides on their trades from day to day. For example, the SG CTA Index suffered its worst performance ever on March 13th, 2023, (Figure 6).

Figure 6 - SG CTA Index suffered its worst performance ever (Saxo Bank)

Until markets stabilize, investors should continue to expect increased daily volatility, which could negatively impact CTA strategies that depends on following trends.

Driving Through The Rearview Mirror

The other main issue I see with DBMF's strategy is that by design, DBMF operates with a lag against other CTAs. DBMF's positions are determined by a proprietary quantitative model called the 'Dynamic Beta Engine' that uses regression analysis on the trailing returns of a pool of top performing CTA hedge funds to identify a portfolio of financial instruments that can deliver performances similar to those funds.

In my opinion, DBMF's strategy is akin to driving by looking in the rearview mirror. When the road is straight and wide, DBMF can perform extremely well, and can even outperform the reference CTA hedge funds. This is because traditional CTA hedge funds are constantly betting on baskets of different assets. Naturally, some will perform and some will not. By analyzing and regressing the best performing funds against their underlying asset classes, DBMF's Dynamic Beta Engine can weed out the poorly performing trades.

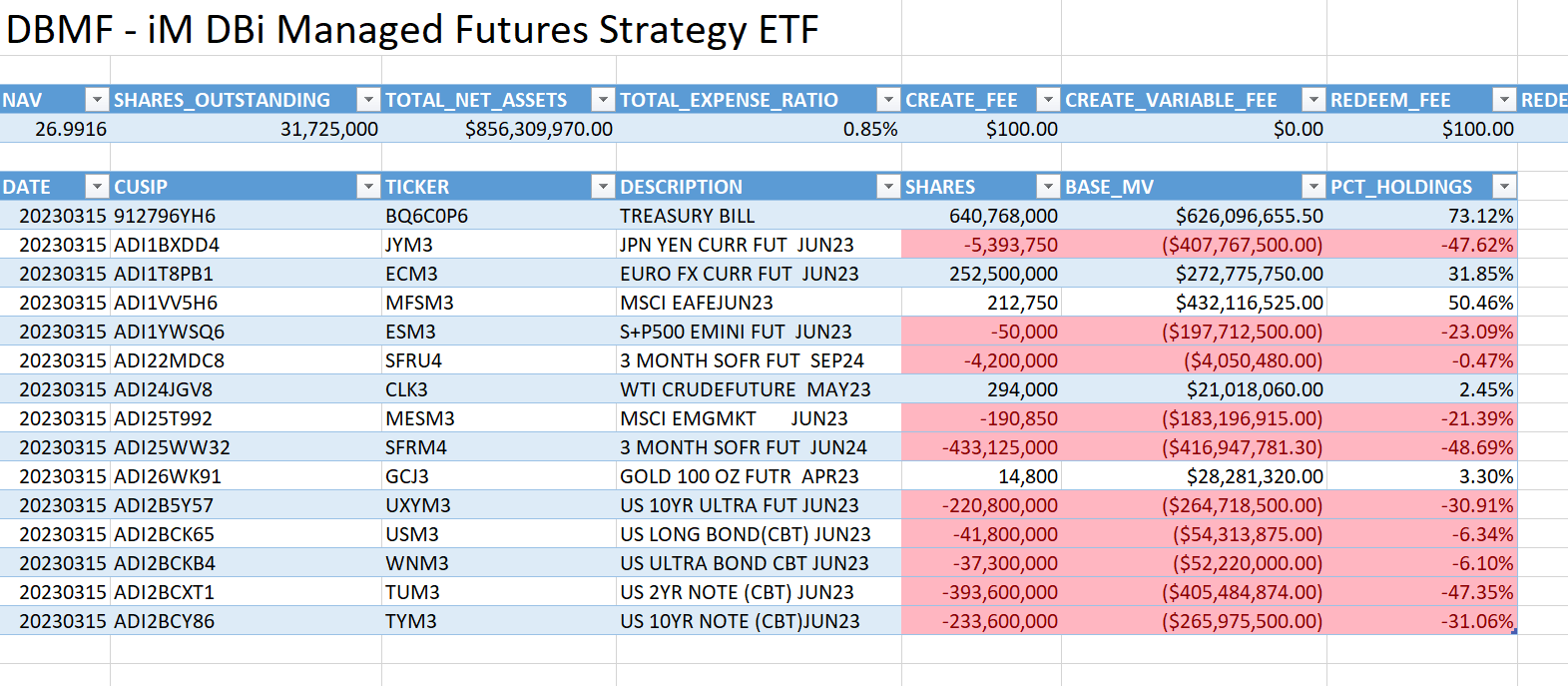

However, the Dynamic Beta Engine can get into trouble when the road has lots of turns and zigzags. For example, DBMF's current portfolio is heavily short bonds, especially the 2Yr Treasury Note (Figure 7). However, in a flight to safety, bonds have been rallying strongly in the past few days.

{kind=link}

Figure 7 - DBMF current portfolio (imgpfunds.com)

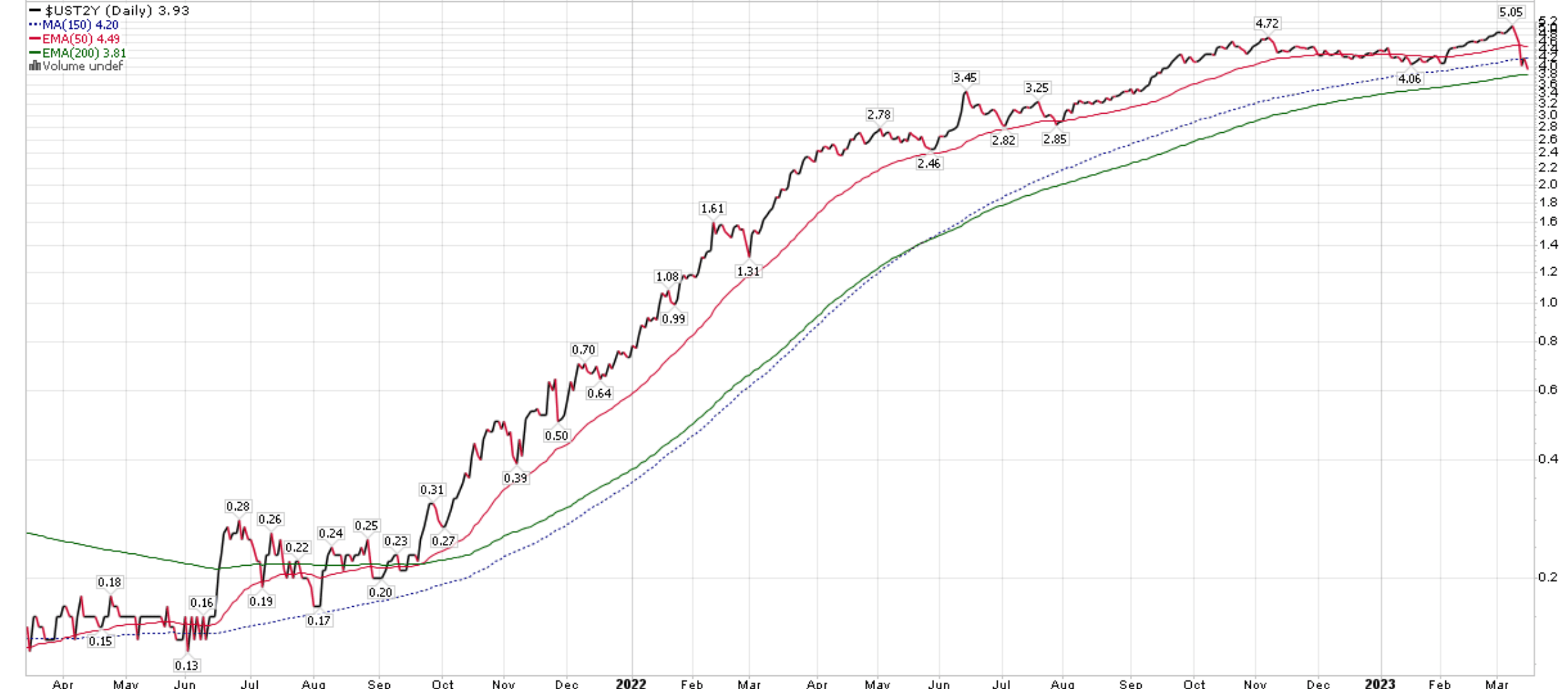

While a normal CTA hedge fund may be stopped out of their short 2Yr Treasury Note trade when the 2Yr treasury yield drops below the 50d moving average, for example in figure 8 below, the 2Yr treasury yield fell through the price trend on Monday March 13th and would have likely stopped out many fast acting CTAs, DBMF will continue holding its position until its Dynamic Beta Engine no longer sees the 2Yr Treasury Note driving performance for the top performing CTA hedge funds it tracks. This process could take days or weeks, and could be obscured by heightened return volatilities.

{kind=link}

Figure 8 - 2Yr treasury note fell through 50d price trend on Monday (stockcharts.com)

Note, according to the fund's setup, DBMF's management does not have discretion to override the Dynamic Beta Engine. So investors in DBMF are stuck in a car turning left when the road has banked right, and vice versa.

Conclusion

CTA strategies need trends in order to perform. Unfortunately, we are currently stuck in a macro environment where one day, all assets could sink on some bank's failure while the next day, they soar on bailout headlines. In this environment, it is hard to see CTA strategies working and providing the portfolio hedge investors desire. Furthermore, with DBMF specifically, its Dynamic Beta Engine means it may still be 'zigging' when its peers have already 'zagged'. I think the best course of action for investors at the moment may be to raise cash instead of look to CTA strategies to save the day.

For further details see:

DBMF: Driving Through The Rearview Mirror