DBSDY - DBS Group: A Good Place To Be Invested For Dividend Safety

2023-10-04 15:54:11 ET

Summary

- DBS delivered record-breaking financial results with a 45% increase in net profit and a 19.2% ROE in Q2 2023.

- The bank's NIM continues to rise, and the volume of interest income has grown significantly.

- DBS increased its dividend, which is considered safe with a yield of 5-6%.

Investment thesis

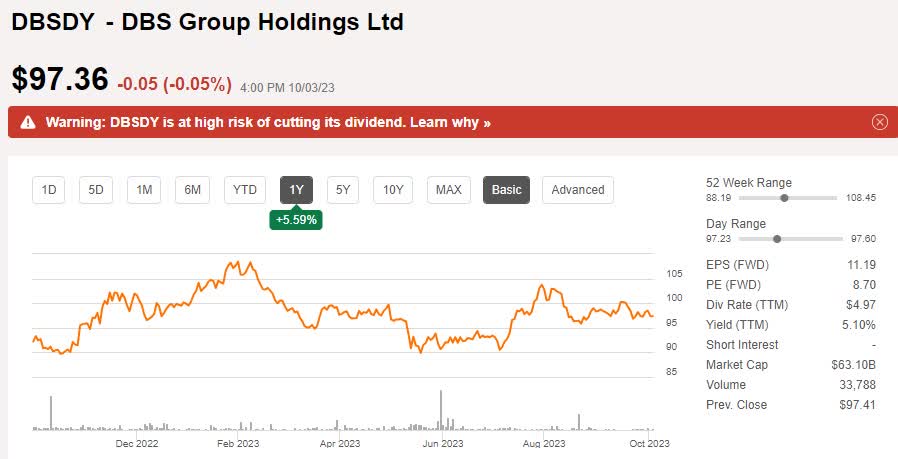

Back in May this year, we upgraded DBS Group ( DBSDY ) from a Hold to a Buy.

It has since then gone up in price by 5.9% and given investors a total return of 7.4% when dividends are included. Bear in mind that DBS is the only Singapore bank that pays quarterly dividends. All the others pay one interim and one final dividend.

{kind=link}

With the bank coming out with its first-half 2023 results, it is a good time to revisit the thesis.

We shall also explore the Seeking Alpha quant findings and its warning about the dividend.

FH 2023 financial results

Whenever we report on DBS and its performance, we sound like a broken record player that keeps repeating itself.

DBS keeps breaking records. Yes, you have seen it before. Right here.

In FH 2023 they delivered another record net profit. This time it came in at S$ 5.26 billion, which was 45% higher Y-o-Y. Their ROE in Q2 was as high as 19.2%.

We stated in our last analysis that we wanted to monitor the bank’s NIM, as we had a concern that the net interest-rate margin might have peaked. Fortunately, it has still been rising.

DBS - Net Interest Rate Margin development (DBS FH 2023 Financial Results - CFO presentation)

We hope we can get our reader's views on whether the interest rate now has peaked and if it will stay high for longer.

However, it is not only NIM that matters. The volume of interest income is also important. This has grown from S$2.45 billion in Q2 of 2022 to S$3.43 billion in Q2 this year.

However, there has been a slight reduction in both loans and deposits from FH 2022 to 2023. Loans shrunk by S$9 billion Y-o-Y and deposits shrunk by S$8 billion. It is Casa that reduced the most, as these accounts are typically accounts that carry zero interest rates. When customers were getting less than 1% on fixed income they cared less, but now that cash suddenly is worth something, money moved out of Casa accounts. It has reduced by as much as S$90 billion in one year. That does not necessarily mean it has left DBS but it is no longer money that DBS can utilize for free without paying their customer for it.

We want to move on to comment on the Non-performing Loans, known as NPLs.

In our recent article on one of DBS’s main competitors, which is UOB , we showed that that bank in fact records lower ratios of NPLs.

It is the same story with DBS. Their NPL ratio is down from 1.3% in FH 2022 to 1.1% in FH 2023. Total NPA as of the end of Q2 was S$4.99 billion. The formation of new NPAs over the FH this year was only S$384 million compared to S$736 million the year before.

The record-breaking profits for DBS have also led the bank to increase the dividend again.

Dividends – and the matter of safety

Shareholders were treated to a special dividend for the bank's 2022 performance and it hiked the quarterly dividend from S$0.42 to S$0.48.

Based on a share price of S$33.35 we get a yield of 5% on a TTM basis, without taking into account the Special Dividend. Should we include it, the yield becomes 6.5%. Assuming the dividend stays put at the present level, the FWD yield is 5.76%.

DBS hiking the dividend again (DBS FH 2023 Financial Report - CFO Presentation)

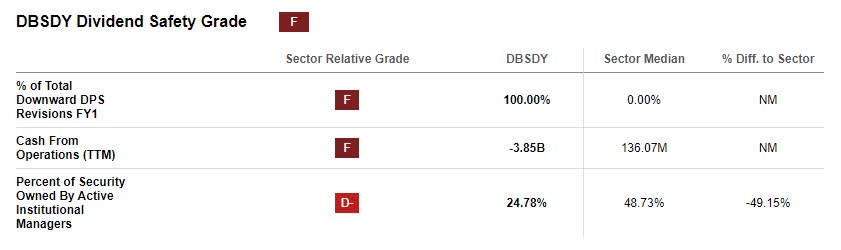

On the 11th of September, Seeking Alpha Quant put out a warning that DBSDY might reduce its dividend.

It gave it an F grade in terms of dividend safety.

{kind=link}

How the algorithms can come to a conclusion that its dividend safety is the lowest grade you can get, is beyond my understanding. In their warning, they state that you should be careful about relying on this dividend for your income.

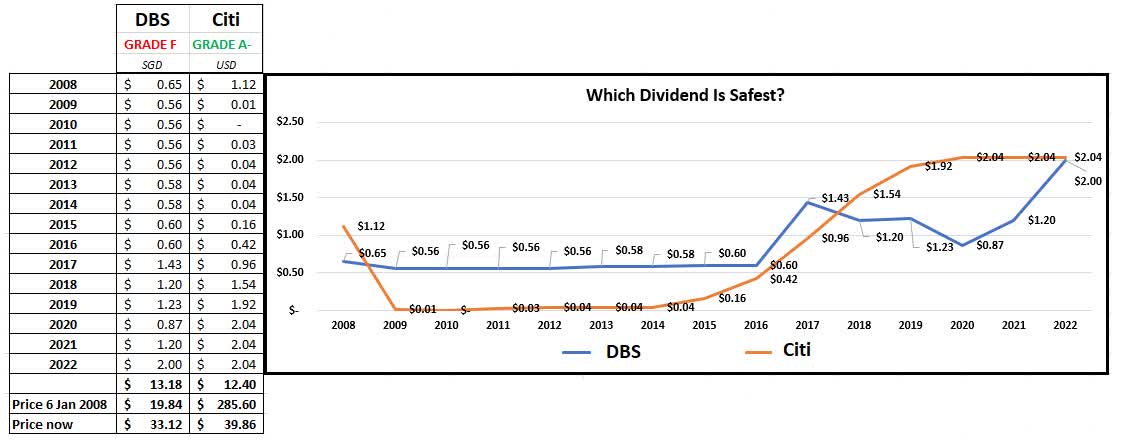

Let us say we have two retirees. One lives in the U.S. We call him John Doe. Another retiree lives in Singapore and we call him Mr. Lim. On the 6th of January 2008, they both decided to invest 10,000 dollars in one of the largest banks in their home country.

Mr. Doe bought Citi ( C ) while Mr. Lim bought DBS. Both did not reinvest the dividends; they just used it to pay some of their living expenses.

Mr. Lim paid SGD 19.84 per share of DBS and got 504 shares. Mr. Doe paid USD 285.60 per share of Citi, and in return received 35 shares. When we take into account the various stock splits that Citi has done, it is perhaps not fair to compare it with DBS, which in 2019 was awarded as the world’s safest bank. Citi has undergone as many as 8 stock splits since 1993. DBS never had to do any stock splits.

But let us just focus on dividend safety, even though I think it is far more important for “a person that relies on dividends as income” that he/she first and foremost protects the money invested, regardless of dividends. Remember, the return OF capital is far more important than the return ON capital. This we will show in this simple example here.

Which dividend is safest? (Data from SA and DBS. Graph by author)

{kind=link}

Mr. Lim’s 504 shares are now worth 66.9% more than what he paid for them as they are worth S$16,692

The picture is not as pretty for Mr. Doe’s 35 shares in Citi which are now worth 86% less than what he paid for them. They are only worth $1,395

Mr. Doe got zero dividends from his shares in 2010 he did not even get the quarterly 1 cent. Mr. Lim on the other hand, was rewarded with dividends every year that he held his shares in DBS. Throughout the GFC of 2008/2009 and the pandemic.

Every investor has to realize that almost every company's earnings and the ability to pay dividends are cyclical. When they make less money, shareholders cannot expect to be remunerated as much as they are when times are good.

We let you be the judge on which bank’s dividend is the safest of the two.

DBS exposure to China

DBS needed to grow the pie by looking outside of Singapore. They are a well-established local bank in Hong Kong, and growing their businesses in India and mainland China as well as Taiwan. This time we shall focus on China.

The media is full of horror stories about how bad the economy is in China, especially in regards to real estate developers like China Evergrande ( EGRNF ), which at one point was the world’s largest real estate developer. The problem was that it was fueled by too much debt. No matter what the outcome is for them, lots of people will lose money having done business with them. Hopefully, people will learn lessons from it.

How big is DBS’ exposure to China?

Their total loan book for mainland China is S$52.9 billion. There is no breakdown of how much of this is to real estate investments and developers. What we do know is that their present ECL, or estimated credit losses, in China that falls under stage 3 is only S$46 million.

During a recent interview, DBS’s excellent CEO Piyush Gupta reaffirmed the bank’s commitment to continue to invest in China , as they are long-term investors.

Singapore economy

In our recent article on UOB, we have covered the development of the economy of Singapore. If you have an interest in DBS, you may want to read this from the link above.

In addition to the update about the Singapore economy you would get by reading the UOB article, we would like to highlight the fact that Singapore does have low unemployment.

According to the Singapore Ministry of Manpower, the latest unemployment rate was 2.8% as of July 2023.

Risks and conclusion

For income investors, DBS does offer an attractive present yield between 5 and 6%. We also think that it is a relatively safe place to be invested.

There are risks that the share price may either stay put or fall if economies, locally or globally, get hit by a prolonged and deep recession. No one knows. We should not focus too much on this.

What we do want to focus on is holding shares in companies that are financially strong, which DBS is, well managed, which it also is, and then we will stay invested in them throughout the different cycles.

Our Buy stance remains.

For further details see:

DBS Group: A Good Place To Be Invested For Dividend Safety