DBSDY - DBS Group: Dividend-Led Returns Potential Looks Appealing

2023-09-28 21:03:37 ET

Summary

- The largest bank in Singapore, DBS Group, offers attractive exposure to rising wealth and economic growth in Asia.

- Near-term earnings may come under pressure from deteriorating asset quality and the waning impact of higher interest rates on net interest income.

- Even so, with the shares yielding in excess of 5.5% against attractive capital returns guidance, these shares look appealing.

Investors looking for some discrete exposure to the long-term Asian growth story could do a lot worse than DBS Group ( DBSDY )( DBSDF ). The largest bank in Singapore, DBS is naturally leveraged to growth in the region on account of its geographic footprint, while its diversified product offering should also allow it to capitalize on rising trade, economic growth and wealth in the area.

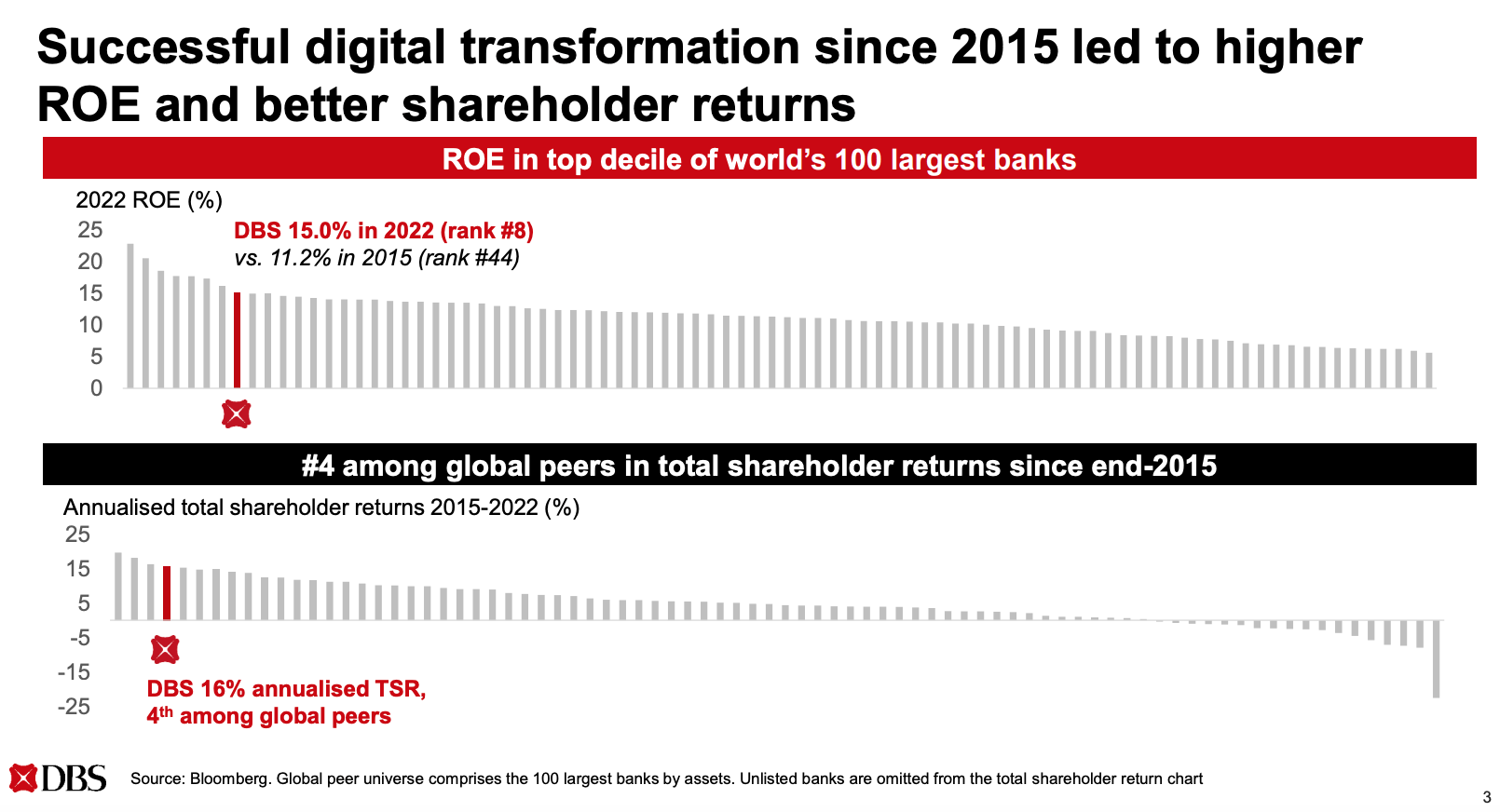

Notionally good growth prospects don't always translate into strong shareholder returns of course, but DBS has performed relatively well on that score too over the past decade or so, ranking #4 in total returns between 2015 and 2022 versus global large bank peers according to management.

Source: DBS Group 2023 Investor Day Presentation

{kind=link}

More importantly, that growth doesn't appear to be command any kind of premium valuation right now. Indeed, offering a 5.6% dividend yield on a modest payout ratio, I'd argue these shares are undervalued given the bank's capital returns potential. Buy.

Well Placed To Capture Regional Growth Prospects

DBS generates two-thirds of its income from Singapore and another 16% from Hong Kong. Although both developed economies, the former's open and trade-led economy and the latter's position as a financial conduit between China and the West makes DBS naturally geared to rising Asian economic growth.

Further, the bank does have direct exposure to faster growing developing markets in the region, generating circa 6% of its income in the rest of Greater China and another 7% in various markets across South & Southeast Asia.

DBS operates a diversified set of services and products, including lending to consumers, SMEs and large corporates, plus non-interest income lines like wealth management, card fees, transaction services and treasury products. Not only does this give the bank comprehensive exposure to rising economic activity, but it also supports solid through-the-cycle profitability (e.g. fee income can help moderate the negative impact of lower interest rates on interest income).

On profitability, DBS has always benefited from its strong deposit share in its home market. This provides the bank with a large source of low-cost current and savings accounts, which fund around 60% of customer lending despite balances dropping-off due to the impact of higher interest rates.

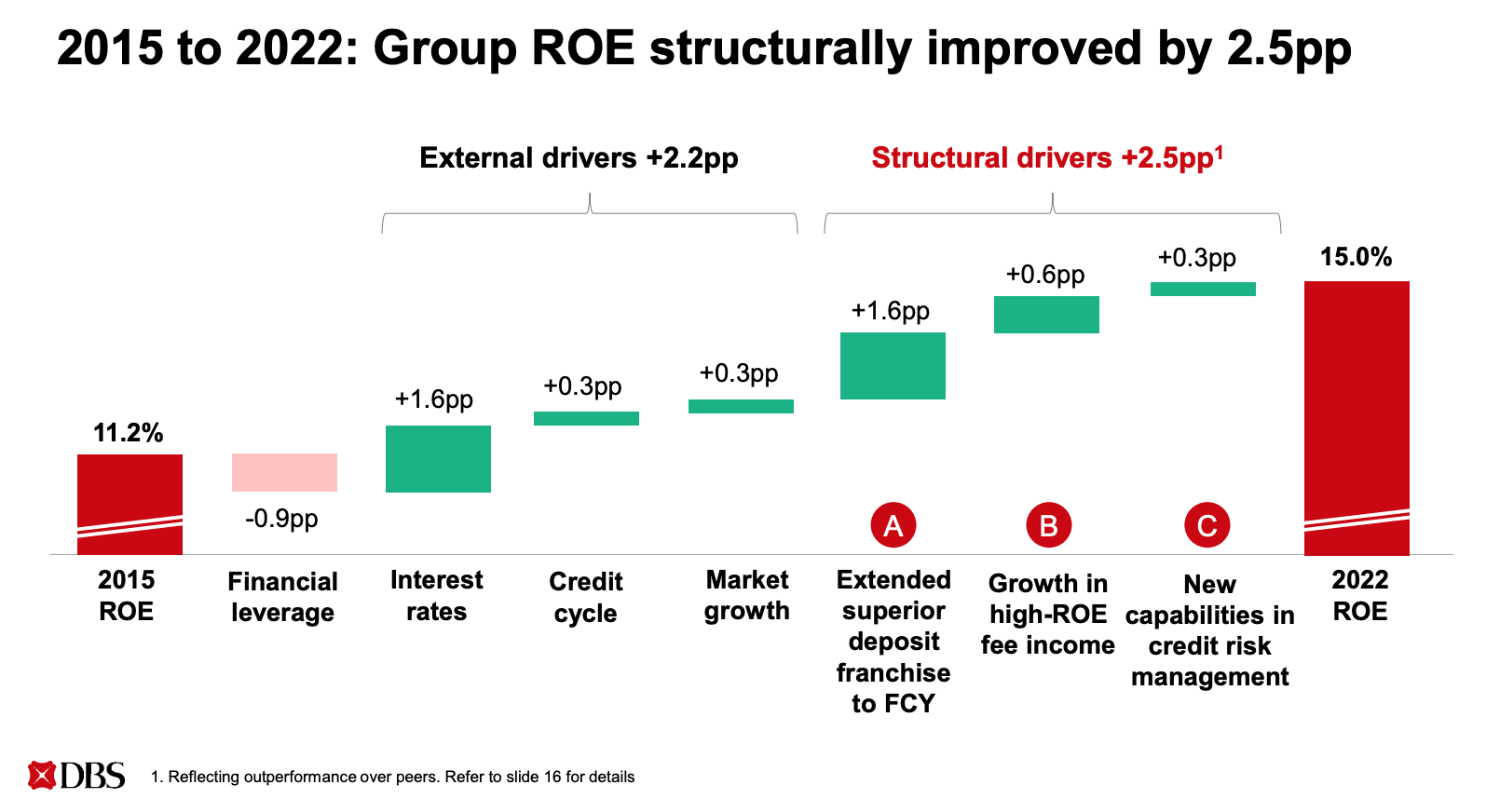

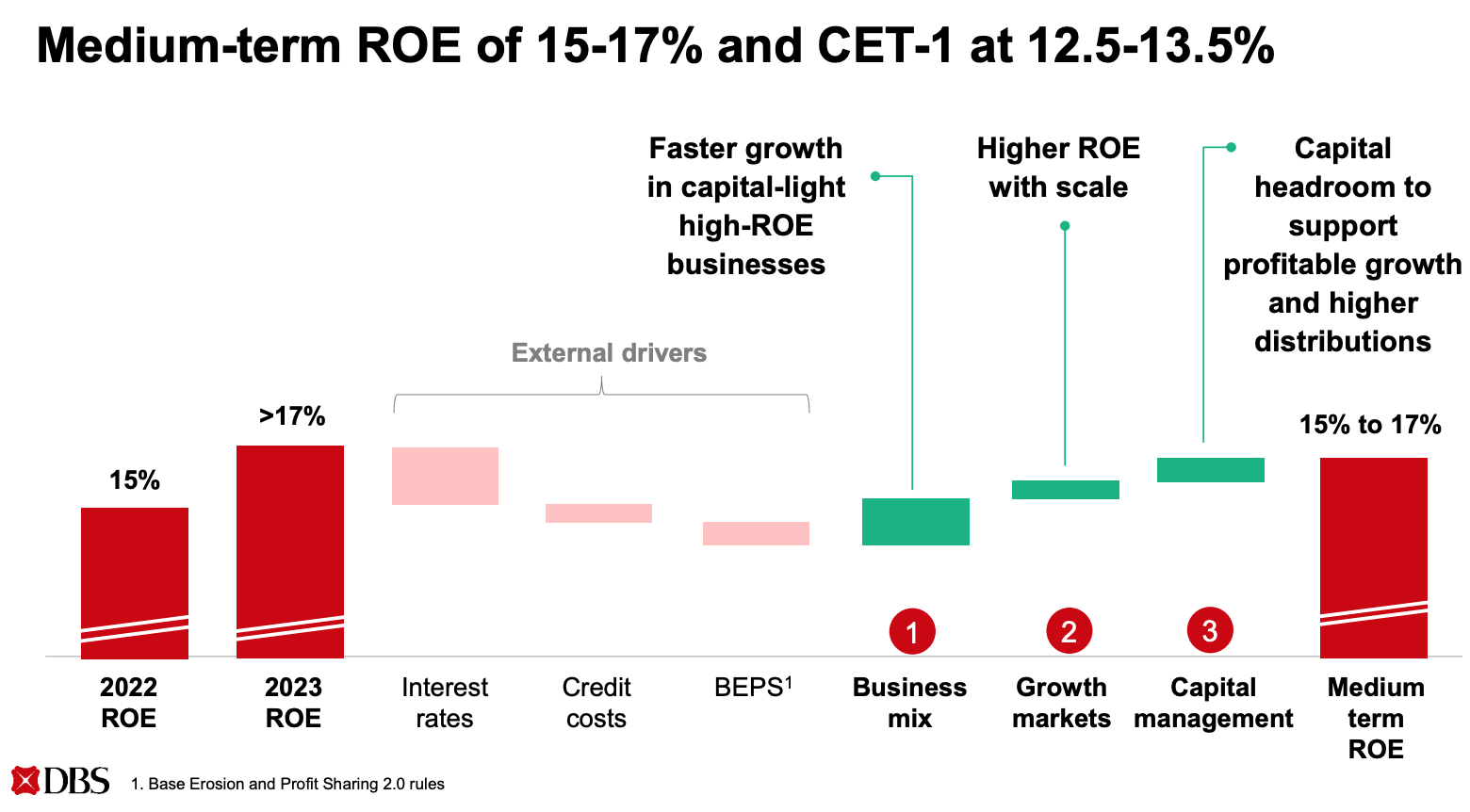

Structural trends also support increased profitability and have led management to boost medium-term return on equity ("ROE") guidance. These trends include ongoing digitization, credit risk management and the growth in higher ROE fee income business lines mentioned above.

Source: DBS Group 2023 Investor Day Presentation

{kind=link}

As a result, management estimates that the bank gained around 2.5ppt in structural ROE improvement between 2015-2022, and is now targeting a medium-term ROE of 15-17%.

Source: DBS Group 2023 Investor Day Presentation

{kind=link}

Growth May Slow In The Near Term

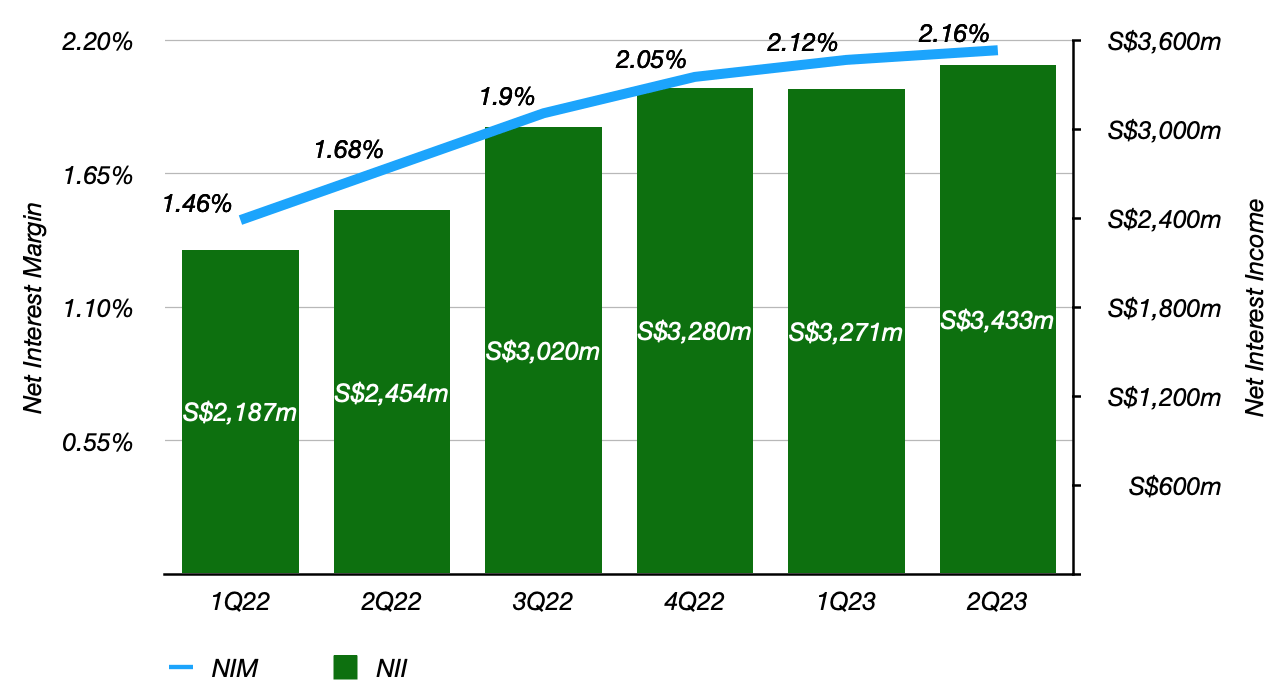

Higher interest rates have been a tailwind to income generation due to expanding net interest margins ("NIM"). Some US banks have recently seen higher funding costs eat into lending margins and net interest income, but NIM at DBS continued to expand on a sequential basis into Q2, driving continued growth in NII.

DBS Group: Quarterly NII & NIM

Data Source: DBS Group Quarterly Results Supplemental

{kind=link}

Combined with still-strong asset quality, this is supporting good growth in profits as well as ROE that is running around 2-4ppt higher than management's mid-cycle target reported above.

DBS Group: Quarterly Net Profit & ROE

Data Source: DBS Group Quarterly Results Supplemental

{kind=link}

Although bullish on DBS's long-term growth and total returns potential, the near-term outlook may prove sluggish. For one, NIMs will likely peak in either Q3 or Q4 based on management's comments, while asset quality will also probably deteriorate from current levels.

I think the peak will be this year based on one more Fed hike. While there is additional benefit from lagged asset repricing, it will be offset by albeit slower deposit repricing. So we might have some NIM upside between now and year-end, but I doubt it will continue into next year.

Piyush Gupta, DBS Group CEO, 2Q23 Earnings Call

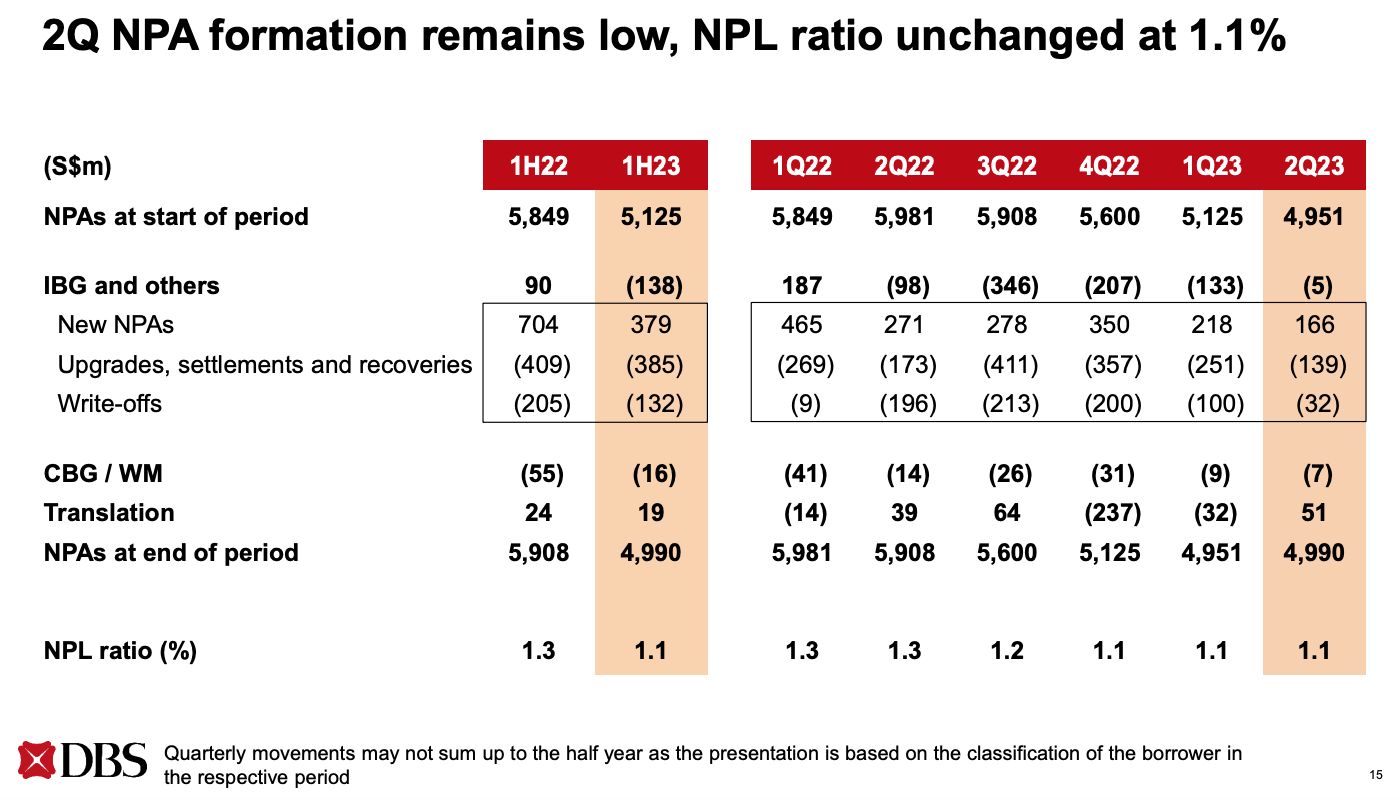

With that, current allowances for bad debt equate to around 130% of non-performing assets, rising to around 230% taking into account collateral.

Source: DBS Group 2Q 2023 Results Presentation

{kind=link}

That looks prudent at this point in the cycle, with the bank still sitting on higher levels of general provisions that were built in response to COVID.

Source: DBS Group 2Q 2023 Results Presentation

{kind=link}

While that means a downturn is unlikely to threaten its capital position, the combination of waning benefits from higher interest rates and downside from asset quality means that DBS's near-term earnings growth may be more muted than in recent quarters.

Attractive Dividend-Led Returns Potential

Although growth might reasonably be expected to slow in H2 and into 2024, DBS nonetheless possesses attractive dividend-led total returns potential. Based on the current quarterly rate, the total FY23 payout should be at least SGD 1.86 per share (~USD 1.36 per "DBSDY" ADS), which maps to a yield of just under 5.6% at the prevailing SGD 33.50 share price.

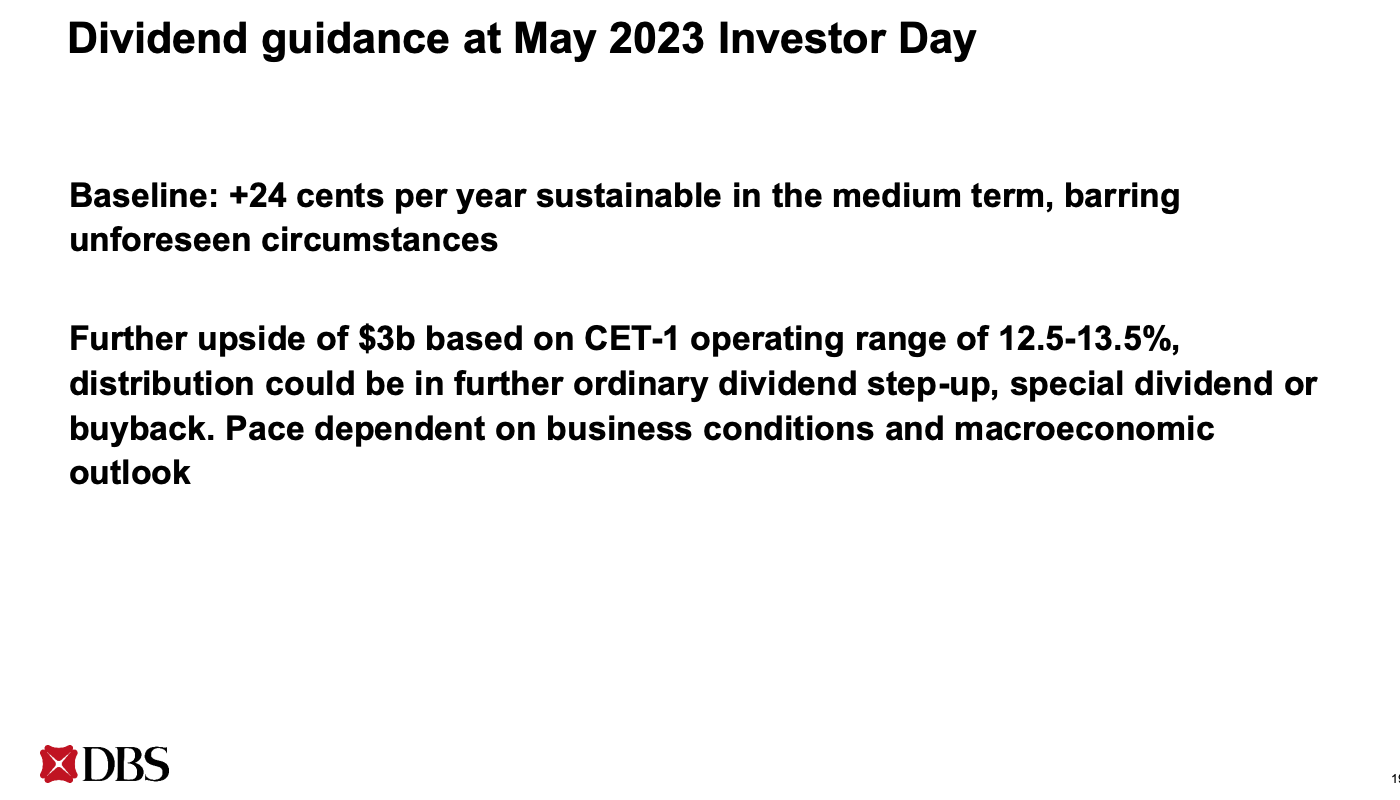

Management aims to grow this by SGD 0.24 per share each year over the medium-term. What's more, the bank's CET1 capital ratio is also around 1ppt higher than its target, which works out to around SGD 3 billion (~USD 2.20 billion), or SDG $1.20 per share (~USD 3.50 per ADS) in surplus capital.

Source: DBS Group 2023 Investor Day Presentation

{kind=link}

Management wants to distribute that to shareholders over the next few years. Although buybacks and special dividends have also been touted as possible methods for this capital distribution, a higher rate of ordinary dividend growth is probably the most likely option.

On the dividend, we said during the investor day we are pretty confident we can increase it by $0.24 a year. But on top of that, we have another $3 billion or $1.20 per share of excess capital that we can return over the next few years, either through buybacks, special dividends or stepping up the ordinary dividend.

Piyush Gupta, DBS Group CEO, 2Q23 Earnings Call

The above implies solid double-digit per annum dividend per share growth over the medium term. Combined with a base yield of around 5.6%, that means total returns would likely land at an equally attractive double-digit annualized clip.

Is this realistic? The usual caveats obviously apply - a worse than expected slowdown/recession would impede the timing and probably magnitude of capital returns, for example - but it looks doable. Based on Q2 earnings, the current dividend only maps to a payout ratio of around 36%. Now, those earnings are admittedly at cycle highs. The bank earned a 19% ROE in Q2 due in part to a favorable macro environment that won't be in place throughout the cycle. Still, normalizing earnings down to the low-end of its 15-17% ROE target only increases the payout ratio to around 55%. Earning 15% on its retained earnings would be enough to generate high single-digit per annum growth, with the gap filled by an expanding payout ratio. The risk is a nasty recession, but with upside pointing to strong double-digit annual returns that is a risk that looks worth taking. Buy.

For further details see:

DBS Group: Dividend-Led Returns Potential Looks Appealing