DBSDY - DBS Group Holdings: Tapping The Emerging Market Opportunity

2023-06-06 14:45:02 ET

Summary

- DBS Group benefits from inflows to Singapore but a few challenges are looming on the horizon.

- DBS is aggressively expanding in India to capture the SME opportunity.

- Recent acquisitions have positioned DBS to capture the growing consumer banking opportunity in Taiwan.

- DBS Group offers investors the opportunity to gain exposure to emerging Asian markets with a certain level of stability because of its roots in Singapore.

Investing in international stocks is easier said than done. Even when we find a company that we believe is undervalued, we still have to account for geopolitical, currency exchange, and sovereign risks before pulling the trigger. I believe this is one of the main reasons Americans prioritize U.S. stocks despite knowing that international markets offer lucrative opportunities. I keep an eye on international markets, however, to find opportunities that are likely to deliver market-beating returns even after accounting for the risks associated with investing globally.

At a time when many investors are not keen on investing in the financial services sector, I found DBS Group Holdings Ltd ( DBSDF ), a banking giant based in Singapore, an appealing bet on the future of Asia.

The Business

DBS Group Holdings, the parent company of DBS Bank, is an esteemed investment company that boasts one of Asia's largest and most reputable banking groups. The company operates in various regions, including Singapore, Hong Kong, Greater China, South and Southeast Asia, and internationally. The company operates through several segments, including:

- Consumer Banking/Wealth Management – this segment offers a wide range of banking and financial services tailored to individual customers. These services encompass checking and savings accounts, fixed deposits, loans and home finance, cards, payments, investment, and insurance products.

- Institutional Banking - this segment focuses on providing financial services and products to bank and non-bank financial institutions, government-linked companies, large corporates, and small and medium-sized businesses. Its offerings include short-term working capital financing, specialized lending, cash management, trade finance, securities, fiduciary services, treasury and markets products, corporate finance and advisory banking, as well as capital markets solutions.

- Treasury Markets - this segment is involved in structuring, market-making, and trading a diverse range of treasury products. This segment plays a crucial role in managing and optimizing the bank's treasury activities.

With a comprehensive range of financial services catering to individuals, businesses, and institutions, DBS Bank has become a prominent player in the financial industry in Asia and was recognized as the World's Best Bank by Global Finance in 2022.

DBS Group Benefits From Inflows But Challenges Are Looming On The Horizon

DBS Group Holdings reported record-breaking first-quarter profits of S$2.57 billion ($1.9 billion), up 43% compared to the corresponding quarter previous year. This remarkable growth was driven by a higher net interest margin, sustained business momentum, and resilient asset quality. The bank's CEO, Piyush Gupta, attributed the impressive performance to safe-haven deposit inflows during a period of increased market volatility. Singaporean banks have been benefiting from deposits flowing in as depositors seek a safe haven amidst global banking system turmoil and uncertainty surrounding the world economy and geopolitics. In the past two years, individuals from mainland China, Hong Kong, and Taiwan have contributed to a surge in capital inflows into the city-state. The recent banking crisis, with Credit Suisse ( CS ) being integrated into Swiss rival UBS, has prompted wealthy families to re-evaluate their banking providers. This shake-up, coupled with the collapse of Silicon Valley Bank which supported many Asian startups, has led to a reassessment of financial institutions.

Singapore is expected to attract wealthy individuals, especially from neighboring Asian countries, with its high-quality infrastructure and second-to-none safety standards. Henley & Partners, in its 2022 Global Citizenship Report , revealed that Singapore added 2,800 HNWIs last year, bringing the total to 241,000, ranking the city-state fifth among the top 20 cities with the highest number of millionaires worldwide. This trend is expected to have a long-lasting impact on the local economy, including rising demand and property values.

Exhibit 1: Citizenship and PR issued by Singapore

{kind=link}

Aided by favorable migration trends and rising interest rates, DBS achieved a new high in return on equity reaching 18.6% compared to 13.1% in the same period the previous year, highlighting the strong profitability profile of the bank. DBS expects full-year return on equity to exceed 17%.

While family office assets at Singaporean banks are increasing, there is a notable lack of investment in the local capital markets. This presents an opportunity to stimulate job creation and generate the fees necessary to sustain the financial sector. Consequently, fee income trends were mixed for DBS Group. While card fees experienced a significant increase of 21% compared to the previous year, wealth management fees fell by 11% in January, influenced by geopolitical concerns and interest rate uncertainties. Transaction service fees remained stable with overall net fee income in the first quarter being 4% lower compared to the previous year.

The bank's net interest margin reached 2.12% for the first quarter, however, it anticipates a gradual decline going forward. According to management, the rate hike cycle has largely concluded. The company also foresees potential impacts on housing loan bookings due to recent cooling measures implemented by the government. Singapore has announced new measures to address concerns about surging property prices that could potentially outpace economic fundamentals. In a bid to cool the market, the government has raised taxes for property purchases, affecting both local and foreign buyers of residential properties. This marks the third round of cooling measures implemented by Singapore, as previous efforts had only a moderate impact on property prices, which showed signs of renewed acceleration in the first quarter of the year. Notably, the doubling of stamp duties for foreign buyers from 30% to 60% aims to moderate investment demand and ensure a more balanced housing market. Singaporean citizens and permanent residents will also face increases in stamp duties, albeit at smaller rates. These measures are part of broader efforts to ramp up the housing supply and alleviate the tight market conditions for both homebuyers and renters.

The new stamp duty rates are expected to affect approximately 10% of private residential property transactions, based on 2022 data. The government's objective is to curb investment demand, both foreign and local, which has been driving up housing prices and creating challenges for Singaporean citizens seeking affordable homes. Singapore has been grappling with soaring residential rental prices, particularly for Housing Board flats and private homes. According to CEIC data , Singapore house prices grew 11.4% year-over-year in March 2023.

Exhibit 2: Singapore house prices

{kind=link}

Rent increases have been substantial since 2021, with the COVID-19 pandemic exacerbating delays in housing projects. However, significant progress has been made to address these delays and ensure that a substantial housing supply will be available in the coming years. The government remains committed to adjusting its policies as needed to maintain a sustainable property market and ensure their continued relevance in promoting housing affordability and market stability. These measures aim to strike a balance between meeting the housing needs of Singaporean citizens and managing the impact of investment demand on property prices.

Despite these challenges, DBS Group Holdings remains well-positioned to adapt to evolving market conditions with new acquisitions in emerging markets.

Expanding Lending Opportunities In India's SME Sector

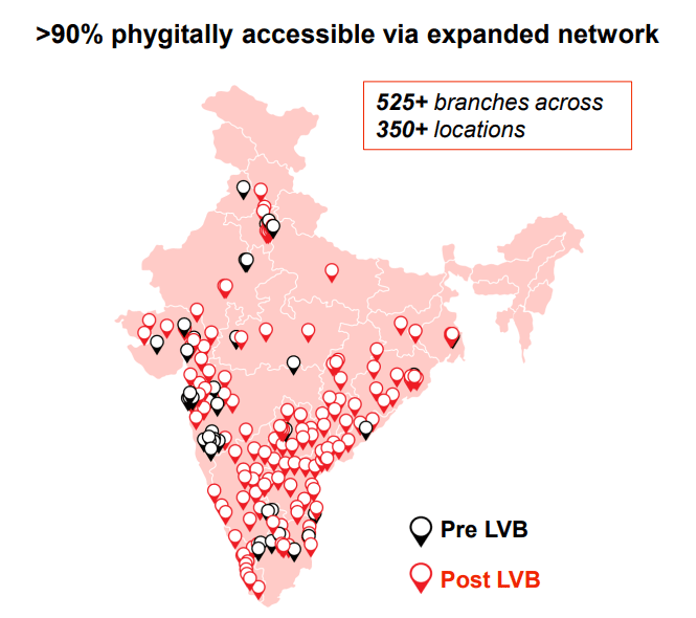

DBS Group Holdings' acquisition of Lakshmi Vilas Bank Ltd. in 2020 has opened doors for the bank to explore lending opportunities in India's small and medium-sized enterprises (SMEs). The expanded network resulting from the acquisition positions DBS Group as an ideal partner to provide efficient access to financing for smaller companies. India's lending regulations, which limit funding for mergers and acquisitions, have created a fertile ground for private credit. DBS Group recognizes the potential of private credit and aims to leverage its acquisition to tap into India's cash-hungry SME sector. By offering private credit, the bank aims to address the challenges faced by SMEs in accessing traditional borrowings. Moreover, the bank's foray into private credit aligns with its broader strategy of using innovative financial solutions as a catalyst for growth.

During the Investor Day 2023 event, the bank provided insights into its digital strategy and market opportunities in India. The bank initially ventured into the digital-only approach in India back in 2017 through the launch of Digibank, India's first mobile-only bank for consumers. However, the experience revealed the importance of having a broader physical presence to achieve optimal results. In 2017, the bank further expanded its offerings in India by partnering with Tally to introduce e-payment integration with accounting software for SMEs.

As of March 2023, the bank boasts one million retained customers through Digibank and has successfully migrated 1.4 million customers from LVB (Lakshmi Vilas Bank). Notably, 83% of new accounts were opened digitally, indicating the growing preference for digital banking solutions. The bank's revenue per customer has experienced an impressive 5x growth, driven in part by strategic partnerships.

Recognizing the immense potential of the Indian market, the bank estimates that it will provide access to an attractive market opportunity with annual revenues ranging from S$200-250 billion, projected to grow at a rate of approximately 10%. The bank has already captured around 70% of its target market through expanded capabilities.

Exhibit 3: The India opportunity

{kind=link}

Looking ahead to 2026, the bank anticipates significant growth in its loan portfolio, with an expected overall increase of 2.2 times. Consumer and SME loans are projected to grow at a compound annual growth rate of 40%. The bank also aims to achieve a 100 basis point net interest margin expansion, enabling a higher rate deposit growth strategy, and doubling overall deposits. These ambitious targets reflect the bank's confidence in the Indian market and its strategic initiatives to capture its growth potential.

Exhibit 4: Loan book and deposit mix predictions for 2026 (DBS India)

{kind=link}

DBS India will prove to be a growth engine for the bank in the years to come, and investing in DBS Group stock offers investors the opportunity to gain indirect exposure to India while enjoying the stability associated with Singapore.

Citibank Taiwan Acquisition To Capitalize On Taiwan's Surging Card Payments Market

The projected growth of Taiwan's card payments market presents a significant opportunity for DBS. With the market value expected to reach $172.8 billion by 2026, driven by factors such as the increasing preference for electronic payments, the surge in contactless payments, and the efforts of local authorities to boost cashless transactions, DBS can capitalize on this trend to expand its presence and offerings in Taiwan. DBS Bank Taiwan recently acquired Citibank Taiwan Ltd.'s consumer banking business which positions Taiwan as DBS Bank's third-largest market, following Singapore and Hong Kong.

DBS Bank Taiwan plans to retain all 2.77 million Citibank Taiwan cardholders and facilitate their transition to DBS Taiwan cards over the next year. By expanding its client base, the bank aims to enhance its digital banking services and further strengthen its consumer banking division. The acquisition also allows DBS Bank Taiwan to offer improved rewards and partnerships to Citibank cardholders, ensuring a seamless transition. Additionally, the bank is exploring opportunities to introduce a new credit card to maintain its growth momentum and keep up with the intense competition in the local credit card market. As the market grows at a compounded annual growth rate of 7.9% between 2022 and 2026, DBS can strategically position itself to capture a substantial share of this expanding market. According to Global Data, the estimated value of card payments in Taiwan in 2022 was $127.5 billion , indicating a 6.2% growth compared to the previous year. Of particular interest is the expected rise in credit card usage, with the average number of annual transactions projected to increase to 64 per card by 2026, up from the current average of 45 times per year in 2022. Credit cards currently dominate the market, accounting for 92.2% of card payments, while debit cards hold the remaining 7.8% market share. DBS can leverage its expertise in digital banking and innovative payment solutions to meet the evolving needs and preferences of Taiwanese consumers.

Takeaway

DBS Group Holdings continues to cement its position as a leading banking group in Asia and projects annual earnings of over S$10 billion ($7.4 billion) over the next three to five years, underpinned by a robust balance sheet and ongoing digital transformation efforts. The bank expects a return on equity between 15% and 17% in the medium term. By leveraging acquisitions and tapping into underserved markets, DBS Group Holdings is poised to capitalize on opportunities in India's SME sector and Taiwan's consumer banking industry. The bank's strong first-quarter net income and impressive return on equity validate its strategy and ability to deliver sustainable profitability. At a trailing P/E of around 9.0, DBS Group is cheaply valued compared to many of the leading financial services companies in the Asian region.

For further details see:

DBS Group Holdings: Tapping The Emerging Market Opportunity