DBSDF - DBS Group: Recent Regulatory Challenges And Peak NIMs Mask Upside Potential

2023-11-14 14:46:40 ET

Summary

- DBS Bank faces regulatory challenges and penalties for digital banking service disruptions, but it has set aside funds to improve its systems.

- DBS Bank's long-term outlook is positive, with potential loan growth from the ASEAN region's emergence as a global supply chain hub benefiting net income.

- There is potential for a special dividend as DBS Bank carries excess capital on its balance sheet.

When I first covered DBS Group Holdings Ltd ( OTCPK:DBSDF ) back in June, I found the parent company of Singapore's largest bank attractively valued in the market. To recap, my investment thesis for the bank is centered around a few key factors, including the diversified products/services offered by DBS, inflows of funds into Singapore as the country welcomes new citizens and permanent residents, and the bank's diversification efforts in India. DBS stock has gained just over 3.5% since my article, with total returns hovering around 5%. Nothing to write home about, but I believe the stock has held up pretty well amid recent regulatory challenges stemming from the continued disruptions to digital banking solutions offered by DBS this year. More on that later. Looking beyond these regulatory challenges, I feel comfortable with the outlook for DBS and how the bank is positioning itself to grow sustainably in the long run.

Recent Regulatory Challenges

On November 1, The Monetary Authority of Singapore ("MAS") penalized DBS Bank for its failure to rectify a technological failure that caused digital banking services and some ATMs to malfunction for more than 4 hours. As part of the penalties imposed on DBS, the bank is not allowed to acquire any new businesses for six months and is barred from making non-essential IT investments through April 2024. The idea behind these penalties is to force DBS to focus on streamlining its existing systems before rolling out new technologies. The bank will not be allowed to shrink the size of its branch and ATM network until regulators approve the strategic plan formulated by DBS to prevent digital disruptions of this nature from occurring in the future.

During the third-quarter earnings release on November 6, DBS CEO Piyush Gupta pledged to work toward rectifying these system failures by implementing a new set of comprehensive measures to tackle digital disruptions through a focus on incident management and system resilience. The bank pledged its commitment to achieving service availability "over and above regulatory requirements. "

This, unfortunately, is not the first time DBS has found itself in a tough spot with regulators. In March 2022, MAS ordered the bank to hold S$930 million in additional regulatory capital following a similar incident where digital banking services were disrupted.

In response to the recent digital disruptions, DBS Bank will set aside S$80 million to improve its systems.

In the short term, I do not see these penalties materially impacting the bank's business. The bank, as far as I am aware, did not have any plans for new M&A deals in the foreseeable future when it was notified by MAS to avoid any such plans. DBS is currently focused on integrating the consumer business it acquired from Citi Taiwan last August and the business of Lakshmi Vilas Bank in India which it acquired in 2020. With DBS being the go-to bank in Singapore, I do not expect the recent digital disruptions to have a material impact on deposits as well.

As a long-term-oriented investor, however, I am concerned about the bank's inability to find the root cause of these continuous service disruptions. In case DBS fails to address these outages swiftly in the future, a notable deterioration of its brand value cannot be avoided.

The Long-Term Outlook Is Bright

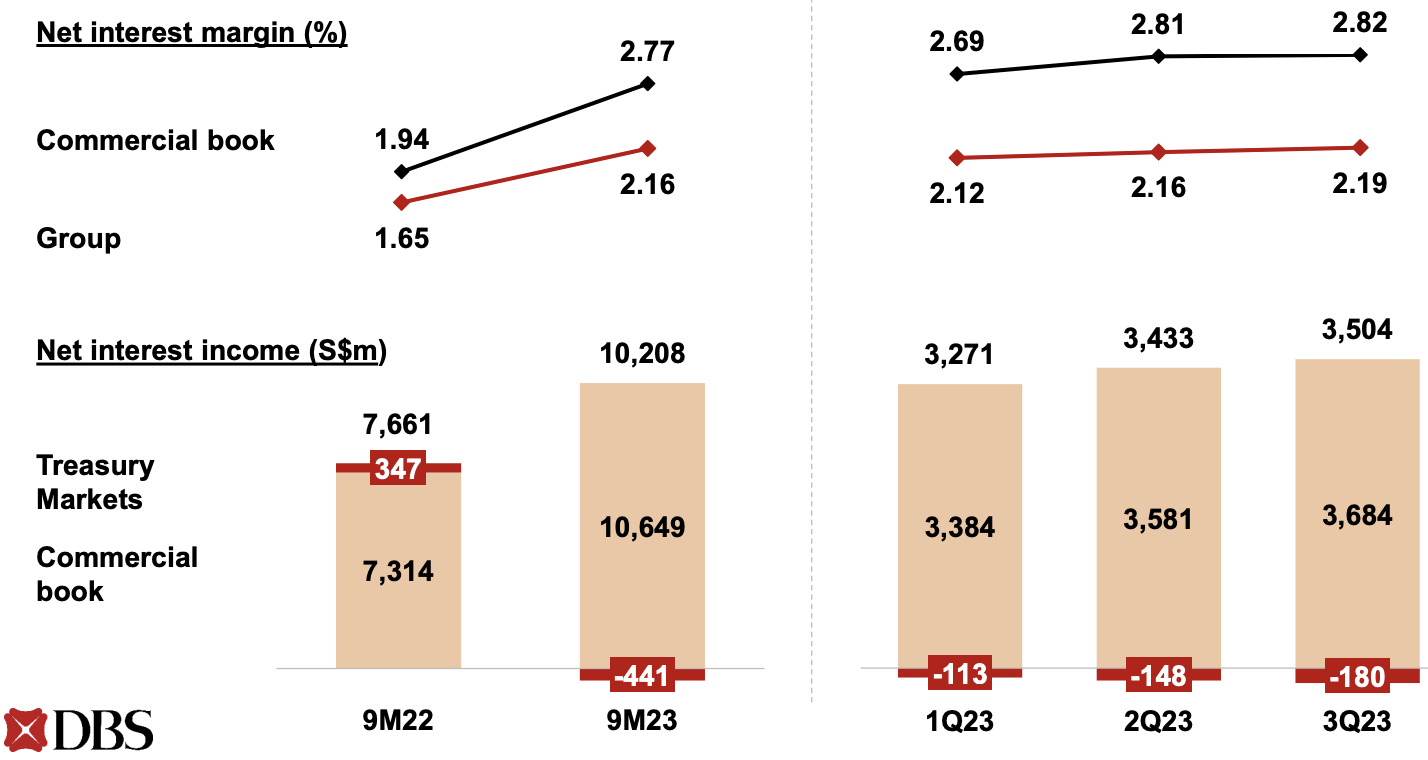

With interest rates rising since early 2022, the net interest margins of banks have trended favorably. DBS is not an exception. DBS Group NIM increased for the seventh consecutive quarter in Q3 to 2.19%, and the company reported a net profit of S$2.63 billion, a YoY increase of 18%. Encouragingly, 9-month net profit and ROE hit a record high for the bank despite net profits declining 2% compared to the second quarter.

Looking ahead, I believe investors should acknowledge that DBS Bank has already seen a near-term peak in net interest margins. Answering a question from an analyst during the third-quarter earnings call , Mr. Gupta shared the same views, highlighting that NIMs will not move higher from here unless we see aggressive rate hikes. The stage is set for central banks around the world to be less aggressive in 2024, a year in which policymakers are tipped to turn dovish to boost economic growth on the back of cooling inflation. DBS, in recent quarters, has benefited from higher NIMs, which is evident from its record profitability even at a time when the loan book has not grown much.

Exhibit 1: Net interest income and margin

{kind=link}

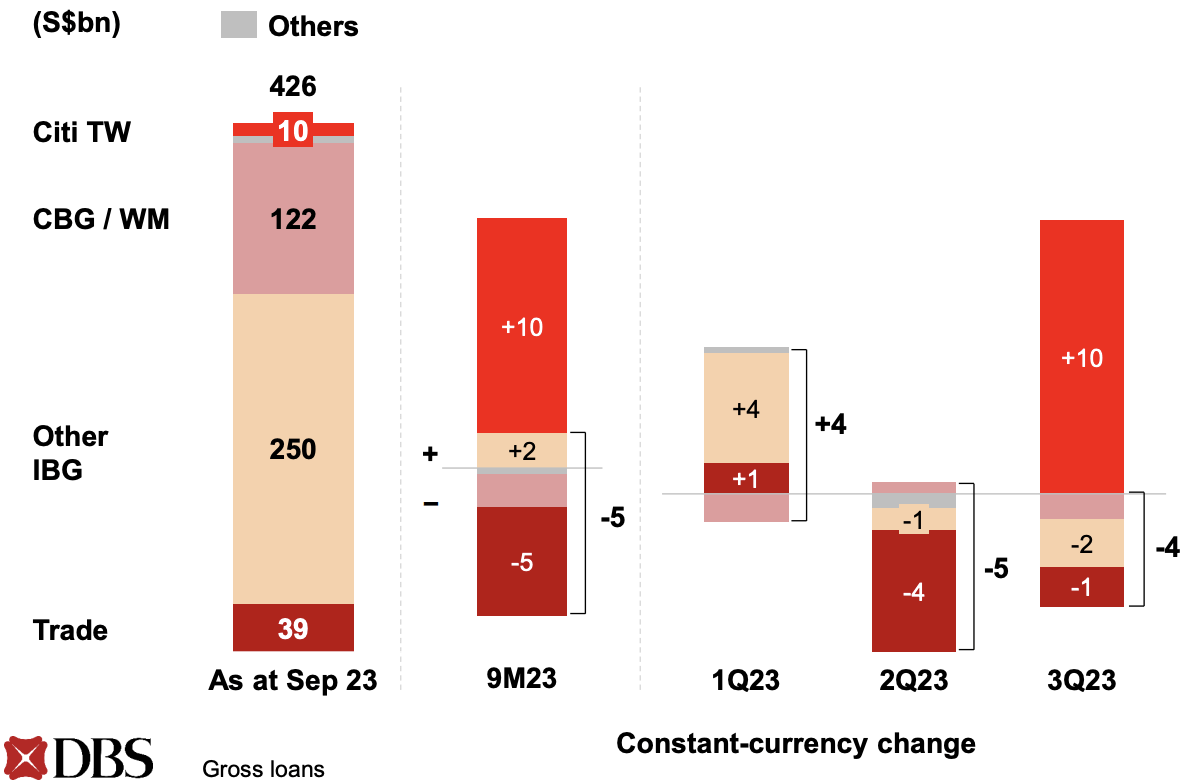

A potential bright spot for DBS in 2024 will be loan growth. Excluding the positive impact of Citi Taiwan integration, DBS would have reported a 9-month loan book decline of S$5 billion as non-trade corporate loan growth was more than offset by a decline in trade loans.

Exhibit 2: Gross loans

{kind=link}

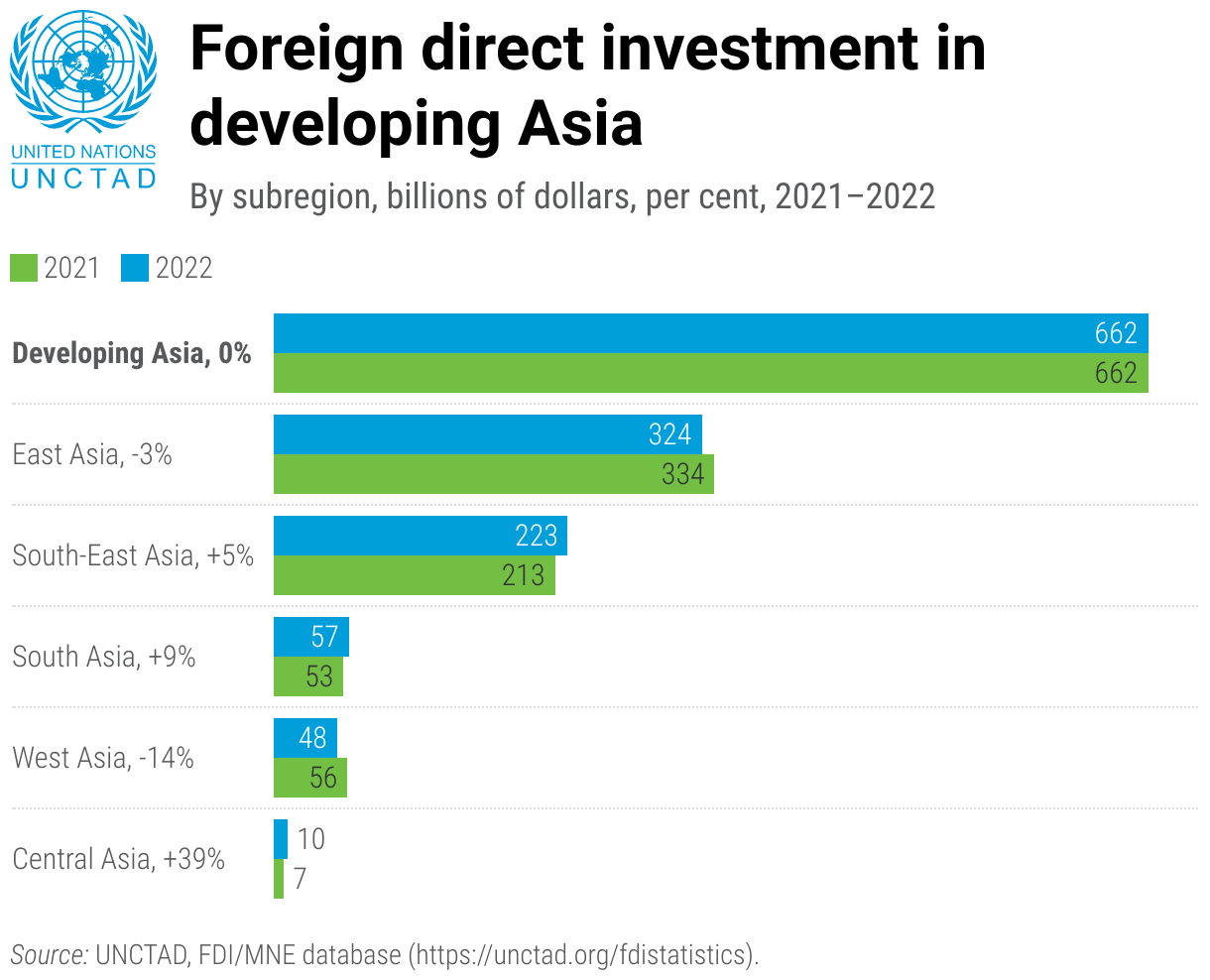

Starting from mid-2024, I expect loan growth trends to make a change for the better, with DBS expected to see stellar loan growth resulting from favorable macroeconomic developments. A key growth driver will be the major shift in the global supply chain in favor of the ASEAN region. The global pandemic, the Russia-Ukraine war, and the increasing tensions between the U.S. and China have forced companies around the world to rethink their supply-chain strategy. Southeast Asia has emerged as a formidable choice that could replace China as a global supply chain hub. A quick look at FDI inflows to different regions in Asia confirms how Southeast Asia is attracting substantial investments today amid this global supply chain shift.

Exhibit 3: FDI inflows to developing Asia in 2022

{kind=link}

In 2022, FDI inflows to Southeast Asia increased by 5% while South Asia, which accounts for inflows to India, saw investments grow by 9% compared to 2021. Granular data reveals Singapore was the largest recipient of FDIs in Southeast Asia in 2022 with the country attracting $141 billion in capital, a record high for the nation. For comparison, inflows to China rose by 5% to $189 billion. With the region expected to attract even higher FDIs in the coming years, I believe DBS is well-positioned to see stellar loan growth once rate cuts allow businesses in this region to invest aggressively to capture growth opportunities.

Several countries in Southeast Asia are already emerging as manufacturing hubs. For instance, Vietnam's rise as an electrical component manufacturer is unmistakable, while Malaysia has secured deals to manufacture desktop computers for both Dell Technologies ( DELL ) and HP Inc. ( HPQ ). Thailand's rise as a key OEM manufacturer for major Japanese carmakers is also noteworthy, with the country emerging as a key manufacturing hub for vehicles delivered across Asia, including the Middle East. Indonesia, on the other hand, is expected to play a key role in the electrification of the global vehicle fleet with its access to nickel, a commodity used in the production of EV batteries and charging infrastructure.

DBS, with its strong roots in the Southeast Asian region and aggressive diversification efforts in India, is poised to benefit from the rise of the region as a global manufacturing hub. 2024, in my opinion, will mark the beginning of a new growth phase for the company despite the expected pressure on NIMs, which I believe will be offset by stellar loan growth.

For dividend investors, there is hope for a special dividend as well. The company carries more than S$2 billion in excess capital on its balance sheet today, and the CEO recently claimed that a decision on distributing this excess capital will be made by the end of the year after taking into account the progress the bank makes in addressing recent regulatory challenges.

Takeaway

As Singapore inches closer to favorable credit policies for borrowers, DBS faces the risk of margin compression. As a long-term-oriented investor, however, I welcome a period of declining interest rates as the bank is well-positioned to see robust loan growth. The long-term macroeconomic outlook remains promising, and I feel comfortable with the bank's exposure to the commercial real estate market in China and Hong Kong. DBS Group remains undervalued and underappreciated in the market.

For further details see:

DBS Group: Recent Regulatory Challenges And Peak NIMs Mask Upside Potential